Guide: Difference Between Invoice and Receipt Every Business Must Know

The fundamental difference between an invoice and a receipt really boils down to timing. An invoice is a request for payment that you send before a client pays you, while a receipt is proof of payment you issue after the money has changed hands.

Think of it this way: an invoice says, “You owe me money,” and a receipt says, “Thanks, I got the money.”

Understanding the Fundamental Difference

It’s easy to see why people use “invoice” and “receipt” interchangeably, but they represent two completely separate stages of a transaction. Each one plays a distinct role in your business’s financial workflow.

An invoice officially kicks off the payment process. It breaks down what a client owes you for the products you sold or the services you provided. A receipt, on the other hand, closes that loop. It’s the formal acknowledgment that the debt has been paid in full.

Getting this right isn’t just about using the correct terminology. It’s absolutely critical for accurate financial management and solid record-keeping. Using these documents properly is how you track revenue, manage your cash flow, and make sure you’re ready when tax season rolls around.

Core Distinctions at a Glance

To make it even clearer, this table breaks down the essential role each document plays. Mastering these concepts is a huge step toward mastering the bookkeeping basics for small business that really drive growth and stability.

| Attribute | Invoice (A Request for Payment) | Receipt (A Proof of Payment) |

|---|---|---|

| Purpose | To request payment from a client for goods or services. | To confirm that a payment has been received and a transaction is complete. |

| Timing | Issued before payment is made. | Issued after payment has been received. |

| Role in Workflow | Manages accounts receivable and tracks outstanding money owed to the business. | Confirms cash received and serves as a record for both buyer and seller. |

In short, the invoice starts the conversation about money owed, and the receipt finishes it by confirming the transaction is done. Both are non-negotiable for a healthy, organized business.

How Invoices Drive Your Business Workflow

An invoice is much more than just a bill. Think of it as a strategic tool that actively manages your company’s cash flow. It’s the document that officially kicks off the payment cycle and serves as the primary record of money owed to you, forming the very foundation of your accounts receivable.

A well-crafted invoice doesn’t just ask for payment; it communicates your professionalism and sets clear expectations. Getting these details right from the start significantly reduces any friction in getting paid on time. This is your main tool for tracking revenue coming into the business.

Each invoice you issue creates a vital paper trail. This allows you to monitor outstanding payments, follow up on accounts that are past due, and forecast your financial position with far greater accuracy. Without a consistent invoicing process, it’s easy to lose track of what you’re owed, leading to unpredictable cash flow and major administrative headaches down the road.

The Anatomy of a Professional Invoice

To be effective and get you paid faster, an invoice needs to have specific information that leaves no room for confusion. Every professional invoice should clearly display these key fields to ensure prompt and accurate payment:

- A Unique Invoice Number: This is absolutely critical for tracking and referencing payments.

- Detailed Service or Product Descriptions: Be specific. Itemize everything you provided, including quantities, rates, and totals for each line.

- Your Business Information: Make sure your company name, address, and contact details are easy to find.

- Client’s Information: List the full name and address of the person or business you’re billing.

- Clear Payment Terms and Due Date: State exactly when you expect payment (e.g., Net 30, Due upon receipt).

This level of detail not only helps your client understand exactly what they’re paying for but also protects you if a payment dispute ever comes up. The clarity of these fields directly impacts how quickly you get paid.

An invoice is the starting point for your entire accounts payable workflow. Its clarity and accuracy set the stage for a smooth transaction, while ambiguity creates delays and potential conflicts that strain client relationships.

For instance, a marketing agency might bill a client in stages. An invoice for “Project Phase 1” should detail specific deliverables like “Market Research Report” and “Initial Ad Creative,” each with its own cost. This granular breakdown prevents confusion and shows the client the transparent value of your work.

Automating for Efficiency and Insight

Manually creating and tracking invoices is not only incredibly time-consuming but also full of opportunities for human error. Modern accounting software can transform this chore into a simple, automated process. These platforms generate professional invoices, send out automatic payment reminders, and give you a real-time dashboard of your accounts receivable.

This automation is more than just a convenience; it’s a significant cost-saver. By the numbers, manual invoice handling can average $22.75 per document. AI-driven systems can slash this cost by over 60%, showing a clear return on your investment.

By automating your invoicing, you get instant visibility into your financial health. This empowers you to make smarter, data-driven decisions for your business. To see how this fits into your bigger financial picture, explore our guide on creating an effective accounts payable workflow.

The Critical Role of Receipts in Record-Keeping

If an invoice is the start of a financial conversation, the receipt is the final word. This document is your undeniable proof of payment, confirming that a deal is done and the money has changed hands. For both you and your client, it’s a critical final step.

On your side of the table, receipts are the bedrock of solid financial management. Trying to track your business expenses without them is a recipe for disaster. Every single receipt—whether it’s for new software, a ream of paper, or that lunch where you closed a big deal—is a building block for clean, auditable books.

This collection of receipts is what backs up your tax deductions and keeps your accounting straightforward. When it’s time to do a financial health check, that paper trail is non-negotiable. You can see exactly how these documents play a part in the bigger picture by reading our guide on how to reconcile bank accounts.

What Makes a Receipt Valid

Of course, not just any slip of paper will cut it. For a receipt to hold up for accounting and tax purposes, it needs to have some very specific information confirming the transaction details.

A valid receipt must always include:

- Business Details: The name and address of the business that was paid.

- Date of Transaction: The exact date the payment cleared.

- Itemized List: A clear breakdown of what was purchased.

- Total Amount Paid: The final amount, including any sales tax.

- Payment Method: How the money was paid (e.g., credit card, cash, bank transfer).

This level of detail doesn’t leave any room for confusion. It’s concrete proof that a specific amount was paid for a specific service on a specific date, protecting everyone involved.

A receipt isn’t just a formality; it’s the final, authoritative record of a transaction. For a business, it’s the primary evidence used to verify expenses, justify tax deductions, and maintain a clean audit trail.

To make managing all these little pieces of paper easier, it’s worth looking into technologies like optical character recognition (OCR). Modern tools can scan a receipt and pull all the key data automatically, saving you hours of tedious data entry. To see how it works, check out this excellent guide to OCR for receipts. Using a system like this ensures your financial history is not only complete but also easy to search and verify, which is fundamental to running a sound business.

A Deeper Comparison of Timing, Purpose, and Legal Standing

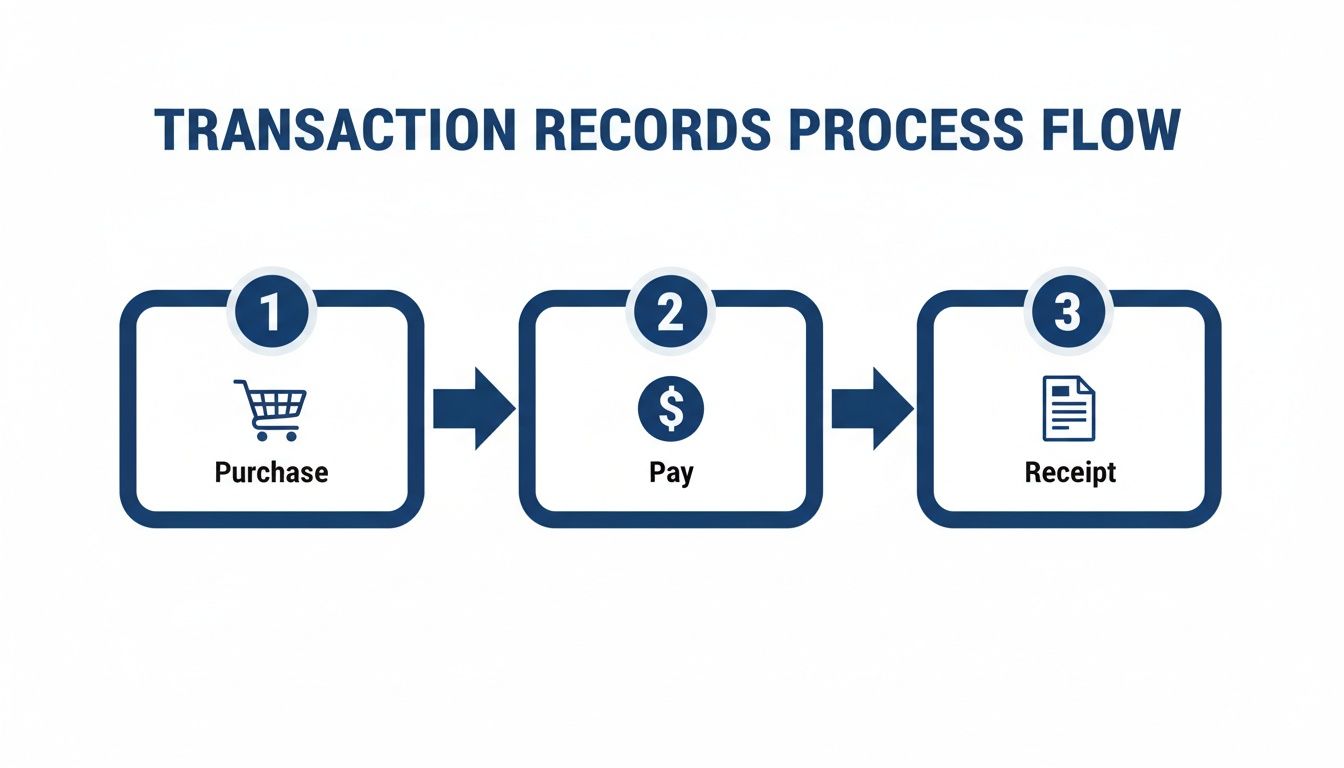

It’s easy to think of invoices and receipts as just two sides of the same coin, but when you dig into their timing, purpose, and legal weight, they’re fundamentally different beasts. Getting these documents right isn’t just about good paperwork; it’s critical for your financial health and legal protection. The whole transaction journey flows from a need, to a request for payment, and finally to a confirmation that the deal is done.

An invoice is the starting gun. It formally kicks off the payment process before any money has actually moved. On the flip side, a receipt is the finish line. It’s the definitive proof of payment issued only after the transaction is complete. This sequence is the bedrock of solid accounting and clear client communication.

This simple flow chart really nails down where each document fits in.

As you can see, the invoice acts as the crucial bridge between the agreement to buy something and the actual payment. The receipt is what closes the loop, marking the transaction as officially settled.

Contrasting Business Functions

Each document’s purpose is tied directly to its timing in the transaction. An invoice is a forward-looking tool you use to manage and track your accounts receivable. It’s your official record of who owes you money, helping you forecast cash flow and chase down late payments.

A receipt, however, is all about the past. Its job is to confirm something that has already happened—payment has been received. For the customer, it proves they’ve paid their bill and is essential for tracking their own accounts payable or personal expenses. For you, the seller, it confirms the income and finalizes the sale in your books.

An invoice is an instrument of action, prompting payment and managing future cash flow. A receipt is an instrument of record, providing final, indisputable proof that a financial obligation has been settled.

Understanding this functional divide is everything. An invoice drives your revenue, while a receipt proves it.

Functional Showdown: Invoice vs. Receipt

Let’s break down the core functions in a head-to-head comparison. While both are transaction documents, their roles couldn’t be more different when it comes to the nitty-gritty of accounting and legal standing.

| Feature | Invoice | Receipt |

|---|---|---|

| Primary Purpose | To request payment for goods or services provided. | To confirm that payment has been received. |

| Timing | Issued before payment is made. | Issued after payment is made. |

| Accounting Entry | Debits Accounts Receivable; Credits Revenue. | Debits Cash; Credits Accounts Receivable. |

| Legal Role | A legally binding request for payment; enforceable. | Proof of payment; settles a financial obligation. |

| Call to Action | “Pay this amount by the due date.” | “This confirms your payment was received.” |

| For the Buyer | A bill to be paid (Accounts Payable). | Proof of purchase; needed for returns/warranty. |

| For the Seller | A tool to track money owed (Accounts Receivable). | A record of income received. |

This table makes it crystal clear: an invoice initiates and tracks a debt, while a receipt extinguishes it. They are two distinct, non-interchangeable steps in a healthy financial workflow.

Legal Weight and Enforceability

The most critical difference between an invoice and a receipt lies in their legal standing. An invoice, when backed by a contract or a formal agreement, is a legally binding request for payment. It’s an enforceable document you can take to collections or even court to demand what you’re owed for your work.

A receipt, on the other hand, is your shield in a payment dispute. It is concrete evidence that a debt has been paid, protecting the buyer from being double-charged and the seller from false claims that payment was never made. Think of it as a defensive document, not a proactive one.

This legal distinction isn’t just a best practice; it’s backed by regulations worldwide. A great example is Brazil’s e-invoicing mandate back in 2008, which required tax authorities to pre-approve invoices before they could be sent. This move cemented the invoice’s status as a formal fiscal document needing government oversight—a level of scrutiny that has never been applied to a simple receipt. You can learn more about how invoicing has evolved globally on Tailride.so. This kind of regulatory treatment shows just how seriously the invoice is taken as a formal, legally significant request.

Navigating Tax and Accounting Implications

The difference between an invoice and a receipt goes much deeper than just paperwork; it has a huge impact on how you manage your books and handle your taxes. Each document kicks off a completely different process in your accounting system, directly affecting the accuracy of your financial statements.

When you send an invoice (assuming you’re using accrual accounting), you’re not just asking to be paid—you’re officially recognizing revenue. This one action creates a debit in your Accounts Receivable account, which is an asset, and a matching credit to your Revenue account. This shows that you’ve earned the income, even if the cash hasn’t hit your bank account yet.

On the flip side, a receipt you get for a business purchase does the opposite. It backs up an expense, creating a debit to an expense account (like “Office Supplies” or “Software Subscriptions”) and a credit to your Cash or Bank account. This entry confirms that money has left your business for a legitimate operational cost.

How Tax Authorities View These Documents

When it comes to taxes, invoices and receipts have completely separate, non-negotiable roles. Tax agencies like the IRS see them as evidence for two different parts of your financial story. Invoices are what you use to prove the income you’re reporting, creating a clear trail of the revenue you earned all year.

Receipts, however, are your proof for claiming tax-deductible business expenses. Think about an audit: an invoice proves you earned money, but only a receipt for something you bought can prove you’re entitled to a deduction. If you can’t produce a valid receipt, a perfectly legitimate business expense can be thrown out, leaving you with a higher tax bill.

For tax purposes, an invoice supports your income, while a receipt defends your deductions. Confusing the two can lead to inaccurate reporting, missed deductions, and significant compliance issues during an audit.

This distinction is only getting more important as governments around the world tighten up digital compliance. We’re seeing a major trend toward electronic documentation, with the e-invoicing market expected to hit $62.68 billion by 2031.

Rules in places like Brazil and across Europe are cementing the invoice’s role as a formal fiscal document for tracking tax obligations. Meanwhile, the receipt remains the final proof that a transaction is complete. As more businesses go digital, understanding requirements like UAE E-Invoicing: A Practical Guide for FTA Compliance is essential for staying on top of your document management and tax planning. This global shift just reinforces how unique and critical each of these documents is in modern finance.

Common Document Management Mistakes to Avoid

Knowing the textbook difference between an invoice and a receipt is just the first step. The real challenge is avoiding the common, everyday mistakes that can throw a wrench in your cash flow, create accounting headaches, and even cause friction with your clients.

Even the most buttoned-up business owners can fall into these traps. These slip-ups often come from simple misunderstandings, but they can have surprisingly big financial consequences. Staying clear of these common pitfalls is absolutely key to keeping your finances clean, professional, and audit-proof.

Sending the Wrong Document at the Wrong Time

This is hands-down the most frequent error we see, and it almost always leads to client confusion and payment delays.

- The Mistake: You send a receipt when a client actually needs an invoice to get it processed by their accounts payable team. This brings their internal process to a screeching halt because a receipt implies the bill is already paid.

- The Solution: Simple. Always issue an invoice to request payment for your services. You should only send a receipt after you’ve received and successfully processed their payment.

Creating Vague or Incomplete Invoices

Ambiguity is the enemy of getting paid on time. When an invoice is missing key details, it forces your client to stop and ask questions, which only delays money getting to your bank account.

An unclear invoice creates an unnecessary obstacle to payment. The more questions a client has to ask, the longer it takes for the money to reach your bank account.

The fix is to use standardized, itemized descriptions for every single service. Instead of a vague line item like “Marketing Services,” break it down into specifics: “Social Media Management,” “PPC Campaign Setup,” and “Content Creation.” Most accounting software lets you save these service items for reuse, which builds consistency and clarity into every invoice you send. It’s a simple habit that makes it much easier for clients to approve and pay your bills without a second thought.

Neglecting Expense Receipt Collection

It’s so easy to overlook small cash purchases or forget to save the digital receipts from online subscriptions. The problem is, every single receipt you miss is a potential tax deduction you can’t claim. This disorganization makes it impossible to get a true picture of your business expenses.

A really practical solution is to start using a receipt-capture app on your phone. Tools like Dext or Expensify let you snap a photo of a receipt the moment you get it. The app automatically pulls the important data and syncs it right to your accounting software. This small tweak to your routine ensures every deductible expense gets recorded, maximizing your tax savings and making your bookkeeping so much simpler.

Frequently Asked Questions

Even when you feel like you’ve got the hang of invoices and receipts, real-world situations can still leave you scratching your head. Let’s tackle a few of the most common questions business owners run into.

Can One Document Serve as Both an Invoice and a Receipt?

Technically, yes, but it’s not a great habit to get into. You’ll sometimes see this in retail where a customer pays on the spot. The document lists what they bought and is immediately stamped “Paid in Full”.

While this shows a zero balance and acts like a receipt, it muddies the waters for your bookkeeping. For a clean, professional audit trail, it’s always better to issue two separate documents. Send an invoice to request the payment, and once the money hits your account, send a distinct receipt to confirm it. This keeps your records crystal clear.

What Is a Pro Forma Invoice?

Think of a pro forma invoice as a “pre-invoice” or a good-faith estimate. It’s a document you send to a client before any work is done or finalized, outlining what you expect the project will cost.

A pro forma invoice is not a legal demand for payment. It’s a quote, not a bill, so it doesn’t get recorded in your accounts receivable. Its main job is to get everyone on the same page about costs before the project kicks off.

These are really useful for helping a client get budget approval internally or for handling customs declarations in international trade.

How Long Should My Business Keep Invoices and Receipts?

The official IRS guideline is to keep records supporting your income and deductions for three years from the date you file your taxes. However, ask any seasoned accountant, and they’ll tell you to aim for at least seven years.

Why the extra time? A seven-year window gives you a much safer buffer in case of an audit, a legal dispute, or any other financial inquiry that might pop up down the road. It ensures you have a complete, defensible history of every transaction, which is one of the best ways to protect your business.

At Steingard Financial, we transform your bookkeeping from a chore into a strategic asset. Our team handles everything from meticulous transaction categorization to payroll and HR support, giving you the accurate data you need to grow confidently. Learn more about our services.