Full Cycle Accounting: Master the full cycle accounting workflow

Full cycle accounting is the entire journey your business’s money takes, from the moment a transaction happens to the final reports that tell you how you’re doing. It’s a complete, A-to-Z process. This isn’t just about logging numbers; it’s about creating a clear, accurate story of your company’s financial health, from start to finish.

What Full Cycle Accounting Really Means

Think about building a house. You don’t just throw up some walls and call it a day. You have to pour a solid foundation, frame the structure, run the plumbing, and handle the electrical work—all in a specific order. Each step builds on the last.

That’s exactly how full cycle accounting works. It’s the complete construction project for your business’s finances, making sure every single “brick” is laid perfectly.

This method takes all the raw financial data—like receipts, invoices, and payroll stubs—and turns it into a meaningful story. It’s the difference between having a jumbled pile of numbers and having a detailed blueprint that shows exactly where you stand with profitability, cash flow, and overall stability. Without the full cycle, you’re just guessing.

To give you a better idea of the whole process, here’s a quick overview of what each stage involves.

The Full Accounting Cycle at a Glance

This table breaks down the eight core stages, what happens in each one, and what it means for you as the business owner.

| Stage | Core Activity | Business Outcome |

|---|---|---|

| 1. Transactions | Capturing all sales, purchases, and payments. | A complete record of every dollar that moves. |

| 2. Journal Entries | Recording transactions in the general ledger. | Organized, chronological financial records. |

| 3. Posting | Transferring journal entries to specific accounts. | A clear view of balances for assets, liabilities, etc. |

| 4. Trial Balance | Checking if total debits equal total credits. | An initial accuracy check before closing the books. |

| 5. Adjusting Entries | Making corrections for accruals and deferrals. | A more accurate picture of revenue and expenses. |

| 6. Adjusted Trial Balance | Verifying accuracy after adjustments are made. | Confidence that your adjusted numbers are balanced. |

| 7. Financial Statements | Generating the P&L, balance sheet, etc. | The final, official story of your financial performance. |

| 8. Closing the Books | Resetting temporary accounts for the next period. | A clean slate to start the next accounting cycle. |

As you can see, it’s a systematic process where each step is crucial for the next. This structure is what creates reliable financial intelligence.

Moving Beyond Simple Bookkeeping

Most business owners are familiar with the basics, like logging expenses or sending out invoices. Those tasks are critical, but they’re just the beginning.

True financial clarity only comes when you complete the entire cycle. This includes the more complex steps like bank reconciliations, making adjusting entries for things like prepaid expenses, and generating the official financial statements.

(If you want a refresher on the foundational tasks, check out our guide on bookkeeping basics for small business.)

A proper, full cycle system solves some of the biggest headaches service business owners deal with:

- Messy books that turn tax season into a complete nightmare.

- Uncertainty about cash flow, making it impossible to know when it’s safe to hire or invest.

- Constant compliance worries and the fear of making a costly mistake.

The Foundation for Confident Decisions

At the end of the day, full cycle accounting is about giving you control. When you have a reliable and repeatable process for your finances, you can finally make strategic decisions with confidence.

You can get clear answers to critical questions like, “Can we actually afford that new team member?” or “Do we have enough cash reserves to invest in new software?”

The value of this process is huge. The U.S. accounting services market, which handles these cycles for businesses everywhere, has grown into a $145.5 billion industry. For service businesses that depend on tools like QuickBooks Online or Gusto, that number proves one thing: accurate, full cycle accounting isn’t a “nice-to-have”—it’s the engine that drives growth.

By seeing your financial story unfold from start to finish, you shift from just reacting to problems to proactively managing your business with real data. This structured approach is what turns your financial numbers into your most powerful asset.

Exploring the Eight Stages of the Accounting Cycle

The term “full cycle accounting” can sound a bit intimidating, but it’s really just a methodical, step-by-step process. Think of it as a complete financial health checkup for your business that happens every single month. Each of the eight stages builds on the last, turning the raw data from your day-to-day operations into a clear picture of how your company is really doing.

Let’s walk through the entire cycle, from start to finish. We’ll use real-world examples that a service business owner would see every day, breaking down each stage to show you not just what to do, but why it’s so critical for making smart, confident decisions. This system is designed to make sure nothing ever falls through the cracks.

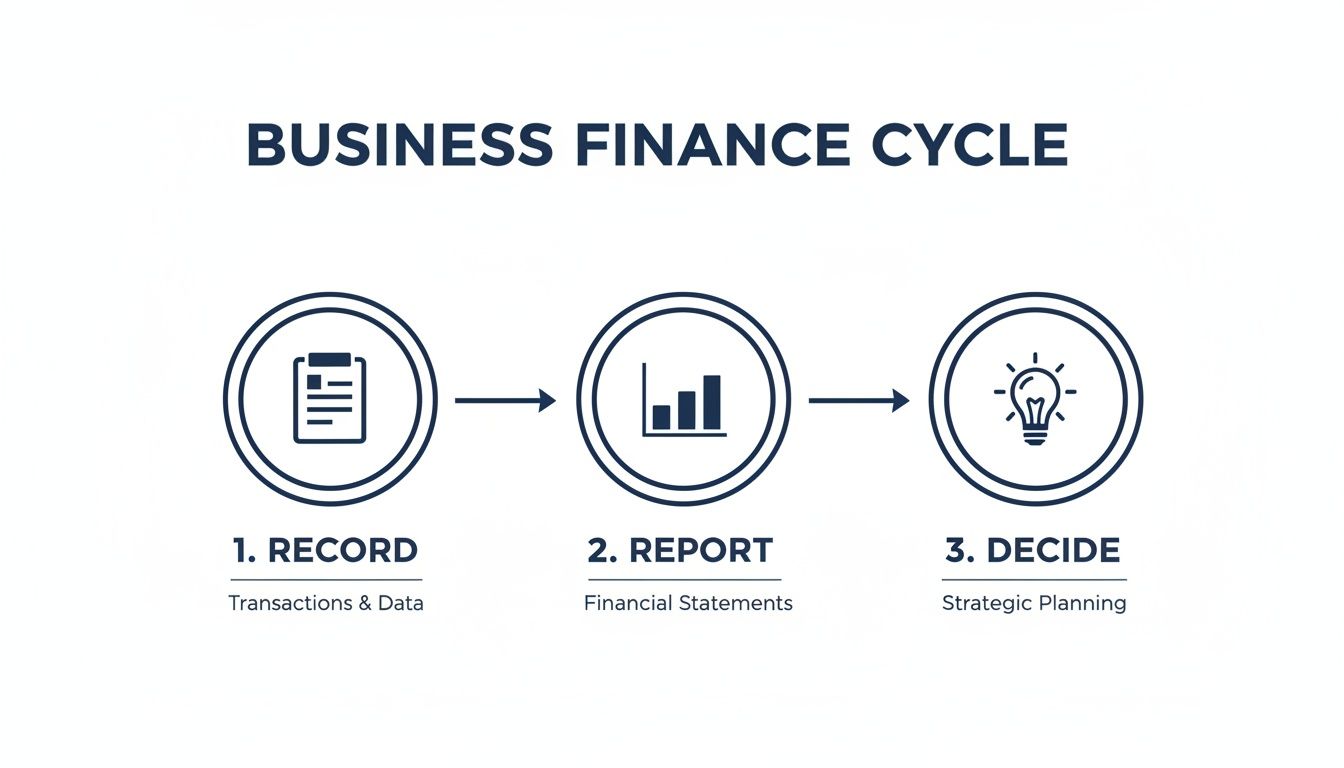

At its core, the entire business finance process really comes down to three things: recording what happened, reporting on it, and then using that information to decide what to do next.

This simple cycle shows just how important that first step is. If your recording isn’t accurate, your reports will be misleading, and your big decisions will be based on nothing more than guesswork.

Stage 1: Capturing and Identifying Transactions

This is ground zero. Every single financial event in your business—big or small—has to be identified and documented. This covers everything from a client paying an invoice to you grabbing a coffee with a potential partner.

For a service business, these transactions might look like:

- A client pays your $5,000 invoice with a bank transfer.

- You pay the $150 monthly subscription for your project management tool.

- An employee submits a $65 expense receipt for a client lunch.

These source documents—invoices, bank statements, receipts—are the raw ingredients for your entire accounting process. Without them, you have no record, and you have no proof.

Stage 2: Recording Transactions with Journal Entries

Once you have the proof, it’s time to get it into your company’s books. We do this with journal entries, which serve as the first official record of a transaction. The gold standard here is a system called double-entry bookkeeping, where every transaction always affects at least two accounts.

For example, when that client pays your $5,000 invoice:

- Your Cash account (an asset) goes up by $5,000.

- Your Accounts Receivable account (money people owe you) goes down by $5,000.

One account gets a debit, the other gets a credit. This simple but powerful system is what keeps your books perfectly balanced at all times.

Stage 3: Posting to the General Ledger

Think of your general ledger (G/L) as the master file cabinet for your finances. After a transaction is logged as a journal entry, that information gets “posted” to the specific accounts inside the G/L. All cash transactions get filed under the “Cash” account, all sales revenue under “Sales Revenue,” and so on.

This step is all about organization. It groups all your journal entries by account, making it incredibly easy to see the total activity and current balance for any piece of your business. For instance, you can pull up your Accounts Payable ledger and see exactly how much you owe all your vendors in an instant. Managing this efficiently is a game-changer, which is why a streamlined accounts payable workflow is so important for keeping vendor payments on track.

Stage 4: Creating the Unadjusted Trial Balance

At the end of the accounting period (typically a month), it’s time for the first big check-in. You’ll prepare an unadjusted trial balance, which is a simple report listing every account from your general ledger and its ending balance.

The purpose is dead simple: to make sure the grand total of all your debit balances equals the grand total of all your credit balances. If they don’t match, you know an error slipped in somewhere during the recording or posting stages, and you can go find it.

This step is your first line of defense against messy books. It won’t catch every type of error—you could have debited the wrong account, for example—but it confirms the basic math is solid before you move on to more complex steps.

Catching errors here saves you a massive headache later on.

Stage 5: Making Adjusting Entries

Business doesn’t always fit neatly into calendar months. Maybe you finished a project at the end of the month but haven’t sent the invoice yet. Or maybe you paid for your annual insurance policy back in January but need to expense it month by month.

Adjusting journal entries (AJEs) are made at the end of the period to handle these kinds of timing differences. They are essential for making sure your financial statements are based on the accrual method of accounting—which means you recognize revenue when it’s earned and expenses when they’re incurred, not just when cash finally moves.

Common adjustments include:

- Accrued Revenue: Recognizing income from a project you completed in March, even if you won’t bill for it until April.

- Accrued Expenses: Recording wages for the last week of the month that your team earned but won’t get paid for until the following month.

- Prepaid Expenses: Spreading out the cost of a $1,200 annual software license into $100 monthly expenses over the year.

Without these adjustments, you’re not getting a truly accurate picture of your performance.

Stage 6: Preparing the Adjusted Trial Balance

After all your adjusting entries are posted, you run the numbers again. This new report is called the adjusted trial balance. Just like before, the goal is to confirm that your total debits still equal your total credits.

This updated list now reflects all the accruals and deferrals you just made. It’s the final, verified set of numbers you’ll use to build your official financial statements.

Stage 7: Generating Financial Statements

Now for the main event. With a balanced and accurate set of numbers from your adjusted trial balance, you’re finally ready to create your financial statements. These are the reports that tell the story of your business’s financial performance.

The three core financial statements you’ll generate are:

- The Income Statement: This shows your revenues and expenses, telling you if you made a net profit or loss for the period.

- The Balance Sheet: This is a snapshot in time showing what you own (assets), what you owe (liabilities), and your net worth (equity).

- The Statement of Cash Flows: This report breaks down how cash came in and went out of your business through operations, investing, and financing activities.

These reports are the ultimate output of the full cycle accounting process. They’re what you, your leadership team, lenders, and investors will use to judge the health of the company.

Stage 8: Closing the Books

The final step is to formally close the books for the period. This process involves zeroing out all of your “temporary” accounts—your revenue and expense accounts—and moving the net income or loss for the period into a permanent equity account called Retained Earnings.

This closing process effectively hits the reset button on your income statement, so you can start the next month with a clean slate. Your balance sheet accounts (assets, liabilities, and equity) are permanent; their ending balances just roll over to become the opening balances for the new period. And with that, the cycle is complete and ready to begin all over again.

The Technology That Powers Modern Accounting

Full-cycle accounting is a powerful framework, but what really brings it to life is modern technology. Gone are the days of manual ledgers and shoeboxes full of paper receipts. Today, we have a dynamic, interconnected system of cloud-based tools that handle the tedious tasks, cut down on errors, and give you instant financial insights. This isn’t just about being more efficient; it’s about turning your financial operations from a chore into a real strategic advantage.

At the center of all this is what we call a tech stack. Think of it as a combination of specialized software platforms that all talk to each other, sharing data to create a single, reliable source of truth for your business finances.

Core Platforms for Service Businesses

For most service-based businesses, a strong and flexible tech stack is built around two key platforms. These two handle the heavy lifting for the entire full-cycle accounting workflow.

- QuickBooks Online (QBO): This is the command center for your financial world. As your general ledger, QBO is where every transaction gets recorded, categorized, and reconciled. It holds your Chart of Accounts and is the system you’ll use to generate those crucial reports like the Profit & Loss Statement and Balance Sheet.

- Gusto: This platform is a specialist in everything related to your people. Gusto takes care of payroll processing, tax filings, employee benefits, and HR compliance. Its biggest strength is automating one of the most complex and error-prone parts of running a business.

The real magic, though, happens when you connect them.

The Strategic Value of Integration

Integration is the bridge that lets specialized tools like Gusto communicate directly with your main accounting system, QuickBooks Online. This connection gets rid of manual data entry, which is not only slow but also a huge source of costly human errors.

Take the payroll process, for example. When you run payroll in Gusto, an integrated system automatically creates a journal entry in QuickBooks. It correctly assigns the funds to wages, payroll taxes, and benefits without anyone having to do a thing.

This automated sync does more than just save time. It ensures that your financial reports are always up-to-date with the latest payroll expenses, giving you a real-time, accurate view of your labor costs and overall profitability.

This level of accuracy is essential for making smart business decisions. Instead of waiting weeks for your books to be updated, you can see the immediate financial impact of a new hire or a round of raises. To get even deeper insights, businesses can use specialized Profit and Loss Analyzer tools to efficiently generate key reports from this data.

There’s a reason the business accounting software market has grown at 6% annually since 2020. It’s because of this capability. Modern platforms automate reconciliations, AP/AR, and payroll, allowing for a “continuous close” model instead of a frantic, last-minute rush at the end of the month. This shift is crucial for staying nimble in a changing economy.

Building a Competitive Advantage

A well-designed tech stack does more than just smooth out your accounting process; it builds the foundation for a more resilient, data-driven business. When your tools are integrated, you have immediate access to the numbers that really matter.

This instant visibility lets you:

- Monitor Cash Flow in Real Time: Know exactly where your cash stands at any moment, helping you manage expenses and plan for the future.

- Improve Decision-Making Speed: Answer critical questions about profitability and budget without having to wait for month-end reports.

- Scale with Confidence: As your business grows, your automated systems can handle more transactions without needing a proportional increase in administrative work.

Ultimately, the right technology turns your financial back office from a cost center into a source of reliable intelligence. It empowers you to navigate challenges and jump on opportunities with much greater confidence.

Why Smart Businesses Outsource Full Cycle Accounting

Trying to manage your company’s entire financial cycle on your own is a huge undertaking. While some business owners try to juggle it all, a much smarter approach is to bring in a dedicated team. Outsourcing your full cycle accounting isn’t just about clawing back a few hours each week; it’s a strategic decision that pays off in cost savings, deeper expertise, and most importantly, peace of mind.

Think about it this way: you wouldn’t represent yourself in a complex legal battle or try to build your own office from scratch. You hire experts because they bring specialized knowledge that you simply don’t have. Accounting is no different. When you partner with a firm, you transform your back office from a necessary cost into a strategic asset.

This approach immediately frees you and your team from worrying about reconciliations and reports. Instead, you can get back to focusing on what you do best—serving your clients and growing your business.

Gaining Expertise Without the Hiring Headaches

One of the biggest hurdles for any growing business is finding—and affording—top talent. This is especially true in the fiercely competitive accounting field. Hiring an experienced, full-time controller or senior accountant comes with a steep price tag that includes salary, benefits, payroll taxes, and ongoing training.

Outsourcing gives you immediate access to an entire team of professionals, from meticulous bookkeepers to high-level CPAs, for a fraction of what it costs to hire a single senior-level employee. You get the benefit of their collective experience without the heavy overhead and long-term commitment of a W-2 hire.

This isn’t just a cost-saving move; it’s a talent upgrade. You’re getting a team that stays current on the latest tax laws, compliance rules, and accounting software, which reduces your risk and improves your financial accuracy.

On top of that, the current job market makes finding qualified financial professionals incredibly difficult. The talent pool is shrinking while the demand for skilled experts is at an all-time high.

Unemployment rates for these roles are far below the national average of 4.2%. For accountants and auditors, it’s just 1.3%. For accounts receivable clerks, 1.4%, and for financial managers, only 1.9%. This talent crunch hits service businesses particularly hard, where 63% of finance and accounting jobs demand on-site work, forcing firms to get creative with hybrid solutions integrated with tools like Gusto and QuickBooks for smooth payroll and reporting. You can read the full research on finance and accounting roles to learn more.

From Cost Center to Strategic Investment

Viewing accounting as just another expense to be minimized is a common—and costly—mistake. When done right, your accounting function is the engine that provides the critical data you need to make smart, strategic decisions. An outsourced partner elevates your financial operations beyond just keeping the books.

Here’s what that strategic shift looks like in the real world:

- Reduced Risk: A professional firm ensures your books are always compliant with the latest regulations, cutting down the risk of expensive penalties from audits or incorrect filings.

- Improved Scalability: As your business grows, an outsourced team can easily scale their services up or down to match your needs, without the friction of hiring or firing.

- Actionable Insights: You get more than just reports. A good partner helps you understand what the numbers actually mean and gives you insights to improve cash flow, control costs, and boost your bottom line.

By handing over the financial reins to a dedicated team, you aren’t just offloading tasks; you’re investing in financial clarity and stability. Our services focused on outsourced accounting for small business are designed to provide exactly this level of strategic support. It allows you to build your company on a rock-solid financial foundation, giving you the confidence to chase down new growth opportunities.

How Steingard Financial Brings Full Cycle Accounting to Life

It’s one thing to talk about the theory of full cycle accounting, but it’s another thing entirely to see it in action. At Steingard Financial, we take these ideas and turn them into a practical service that gives you total confidence in your numbers. It’s all built on transparency, real expertise, and knowing what service businesses like yours actually need to succeed.

This isn’t just about ticking boxes and processing transactions. We’re building a reliable financial engine for your company, one piece at a time, starting from our very first conversation.

The Client Journey From Day One

Our partnership always starts with a simple discovery call. This first chat is incredibly important—it’s where we listen. We want to hear about your challenges, your goals, and any frustrations you’ve had in the past. Are you dealing with a mess left by a previous bookkeeper? Or maybe you’re launching something new and need a chart of accounts that can grow with you? We get into the details to make sure our solution is the right fit.

From there, we map out a custom tech stack. We almost always build our systems around two industry-leading platforms:

- QuickBooks Online: This is the heart of your financial world, where every single transaction gets categorized and reconciled.

- Gusto: This becomes the command center for your team, handling everything from payroll and benefits to HR.

We can work with what you already have, whether you’re on these platforms or need help moving over. The goal is to create a smooth, integrated system that gets rid of manual data entry and gives you information in real-time.

A common headache for new clients is a messy chart of accounts. It’s either too simple to give them any real insight or so complicated that it’s useless. We specialize in designing and cleaning these up, ensuring every report you pull is clear, relevant, and helps you make a decision.

Solving Real-World Financial Challenges

Once your system is up and running, our real work begins. We don’t just maintain your books; we actively manage your entire financial cycle to give you the clarity you need for those big decisions.

Think about a common situation we see: a growing marketing agency with unpredictable cash flow. Their books are a couple of months behind, and they have no idea if they can afford to hire that new designer they desperately need. This is exactly where our full cycle accounting process makes a difference.

Here’s how we’d tackle that problem:

- Historical Cleanup: First, we go back and meticulously clean up and reconcile their past books. This creates a trustworthy baseline and fixes any old errors that have been causing problems.

- Process Implementation: Next, we put a simple process in place for capturing all income and expenses as they happen. This ensures the data is always current.

- KPI-Focused Reporting: Finally, we deliver weekly and monthly reports that focus on the numbers that matter, like Gross Profit Margin, Cash Runway, and Accounts Receivable Aging.

This straightforward approach turns their financial data from something that causes anxiety into a powerful tool. Instead of guessing, the agency owner can now see exactly where their money is going, who hasn’t paid them yet, and what their true profitability looks like. They can make the call on that new hire with confidence, using accurate, up-to-the-minute information. Our process isn’t just about looking backward; it’s about giving you the forward-looking insight you need to grow.

Your Checklist for Implementing Full Cycle Accounting

Moving to a complete full cycle accounting system can feel like a huge undertaking. But when you break it down into clear, manageable steps, the whole process becomes much less intimidating. Think of this checklist as a roadmap to get your financial house in order.

This guide will help you build a solid foundation for financial clarity, giving you the confidence to make smarter business decisions.

Whether you’re setting things up for the first time or just looking to tighten up your existing system, following these steps will create the consistency and accuracy you need. It’s about turning your financial data from a source of stress into a trustworthy asset.

Phase 1 Initial Setup and Configuration

This is the foundational phase, and it’s all about getting your tools and processes right from the start. A strong setup here prevents countless headaches later on and ensures your data is clean from day one.

- Configure Your Chart of Accounts: The first step is to design a detailed Chart of Accounts in QuickBooks Online that truly reflects how your business operates. This means creating specific categories for your different income streams and expenses.

- Integrate Your Tech Stack: Connect your core platforms so they can talk to each other. A great example is linking Gusto to QuickBooks to automate the flow of payroll data and other key transactions.

- Establish an Expense Submission Process: Create a simple, clear policy for how your team should submit receipts and expenses. Using digital tools to capture this data makes reimbursement smooth and keeps records tidy.

Phase 2 Monthly Processes and Routines

With the foundation built, the focus shifts to creating consistent monthly habits. These routines are the engine of your accounting cycle, making sure your books stay current and accurate all the time.

The goal of these monthly tasks is to move from reactive, chaotic bookkeeping to a proactive, predictable financial rhythm. Consistency here eliminates the month-end scramble and builds confidence in your numbers.

- Schedule Weekly Transaction Categorization: Set aside a specific time each week to review and categorize all bank and credit card transactions. This simple habit prevents a massive backlog from piling up.

- Perform Bank and Credit Card Reconciliations: At the end of every month, reconcile each account. This means ensuring your books match the bank’s records down to the penny. No exceptions.

- Review Accounts Receivable and Payable: Pull aging reports for both AR and AP. This helps you stay on top of overdue invoices from clients and effectively manage payments to your vendors.

Phase 3 Quarterly and Annual Reviews

Finally, it’s time to zoom out. These higher-level reviews are where you shift from just processing data to using it strategically to guide your business. It’s all about analyzing performance, ensuring compliance, and planning for what’s next.

- Schedule a Monthly Financial Review: Put a recurring meeting on the calendar to review your key financial statements. Use this time to see how you’re performing against your budget and discuss any important trends.

- Prepare for Tax Compliance: Work with your accounting partner to review your financials quarterly. This allows you to make any necessary adjustments and plan for tax obligations well ahead of any deadlines, avoiding last-minute surprises.

Common Questions About Full Cycle Accounting

Even when the stages seem clear, practical questions always come up when business owners think about putting a full cycle accounting process in place. Here are a few of the most common ones we hear, which might help you decide on the best path forward for your own company.

What Is the Difference Between a Bookkeeper and Full Cycle Accounting

A bookkeeper usually handles the first few steps of the accounting cycle. They’re focused on the day-to-day work of recording transactions and categorizing expenses. This is absolutely critical work for capturing your raw financial data correctly.

Full cycle accounting, on the other hand, covers the entire process from beginning to end. It includes everything a bookkeeper does, plus the more complex tasks like making adjusting entries, performing reconciliations, generating official financial statements, and formally closing the books each month.

Think of it this way: a bookkeeper writes the individual chapters of your financial story. A full cycle accounting provider writes, edits, and publishes the entire book, ensuring the whole narrative is complete, coherent, and accurate.

When Should My Business Implement This Process

The best time to start is from day one. When you establish a proper system from the very beginning, you avoid the messy, disorganized books that lead to expensive and stressful cleanups later on.

But it’s truly never too late to get organized. Most businesses realize it’s time for an upgrade when they suddenly need reliable financial reports for a specific reason—like applying for a loan, bringing on investors, or making a big strategic decision. If you ever feel uncertain about your numbers or you’re spending too much time on financial admin, that’s a huge sign it’s time for a change.

Can I Manage Full Cycle Accounting Myself Using QuickBooks

While QuickBooks is an incredibly powerful tool for business owners, you really need a solid foundation in accounting to manage the full cycle correctly. Many entrepreneurs can handle the basic data entry and transaction sorting just fine.

The trouble usually starts in the more technical stages. Things like handling accruals and deferrals, performing detailed bank and credit card reconciliations, and preparing GAAP-compliant financial statements require specialized knowledge. A professional makes sure these critical steps are done right so you have reliable data you can actually trust to run your business.

Ready to gain complete confidence in your financial numbers? The expert team at Steingard Financial delivers meticulous full cycle accounting services that turn your financial data into a strategic asset. Learn more about how we can bring clarity to your business.