A Guide to Internal Controls for Small Business

Internal controls are the unsung heroes of a healthy business. Think of them as the policies and procedures you set up to guard your company’s assets, keep your financial reporting honest, and stop fraud in its tracks. These aren’t just for massive corporations; they are a critical defense for any small business serious about sustainable growth.

Why Internal Controls Are Your Business’s Best Defense

Let’s get straight to the point: running your business on trust alone is a recipe for disaster. Too many owners I talk to think of internal controls as corporate “red tape”—something they’ll get to “later” when the business is bigger. This is a huge, and potentially costly, mistake. In reality, these are practical, everyday safeguards that are most needed when a business is in its vulnerable growth stages.

Imagine a marketing agency right here in San Jose that’s starting to take off. As bigger clients come in, the owner is pulled in a million directions. Invoices go out, payments come in, and bills get paid, but there’s no second set of eyes on anything. An employee could easily pay a vendor twice by accident. Worse, they could invent a fake vendor and start paying themselves. Without basic controls, these problems could bleed cash for months before anyone notices.

The Real-World Cost of Doing Nothing

This isn’t just some made-up story; it’s a painful reality for many. Did you know a shocking 42% of fraud cases in small businesses happen because there are no real internal controls? That’s a huge jump compared to just 25% in larger companies. This statistic highlights a major vulnerability. Small businesses, often working with smaller teams and informal habits, lean too heavily on trust instead of structured systems.

On the flip side, studies show that putting core controls in place can actually boost profitability by 15-20%. This comes from catching errors, preventing losses, and making smarter decisions because you can finally trust your financial data. One of the most powerful reasons to get started is to implement effective internal controls to prevent fraud and protect the assets you’ve worked so hard to build.

“Thinking you’re too small for internal controls is like thinking you’re too small to have your assets stolen. The risk is always there; the only question is whether you have a defense.”

This is where the principles behind internal controls really shine. It’s not about adding bureaucracy; it’s about building a smart, scalable foundation for financial security.

Breaking Down the Core Principles

For a service business owner, these principles aren’t abstract concepts. They translate directly into actions that protect your revenue. Let’s look at what they mean in practical terms.

- Control Environment: This all starts with you—the “tone at the top.” It’s about showing that financial integrity is non-negotiable. This means having a clear code of conduct, leading by example, and making it clear that shortcuts on financial processes are not okay.

- Risk Assessment: You can’t guard against threats you haven’t identified. This is about looking at your business and asking, “Where are we most vulnerable?” Is it in how you handle cash? Your payroll process? The way you approve and pay bills?

- Control Activities: These are the specific things you do to manage those risks. Think of them as the actual locks on your doors. Examples include requiring owner approval for any payment over $500, reconciling the bank account every single month, or having one person send invoices and a different person record the payments.

- Information and Communication: This is about making sure everyone on your team understands their role in protecting the company. It means writing down your financial policies—even if they’re simple—and explaining to your team why these rules are important.

- Monitoring: Controls aren’t something you just set and forget. Monitoring is about regularly looking at your financial reports, making sure the controls are being followed, and tweaking them as your business grows or changes.

Putting these principles into practice turns your financial weak spots into strengths. It ensures your financial reports are accurate, giving you the clarity to make smart, strategic moves. Most importantly, it creates a scalable foundation, so you can grow with confidence, knowing your financial house is in order. Working with a partner can make all the difference, helping you design a system that secures your business without slowing you down.

Building Your Internal Control Blueprint

Putting internal controls in place for your small business isn’t about building a corporate fortress overnight. Think of it more like drawing up a custom blueprint—one that’s designed specifically for your goals and weak spots. The first move is always to get crystal clear on what you’re trying to protect.

Before you can build any defense, you have to know what’s valuable. Are you most worried about someone making an unauthorized cash withdrawal? Is the accuracy of your project invoicing the top priority? Or maybe it’s just making sure payroll is processed correctly for your growing team. Your financial objectives point the way for everything else.

This is about more than just listing assets; it’s about connecting your financial operations to your business’s mission. For example, a solid objective might be, “Ensure all client invoices are accurate and paid within 30 days to keep cash flow healthy.” An objective that specific makes it way easier to spot potential roadblocks.

Conducting a Practical Risk Assessment

Once you know your goals, it’s time for a hands-on risk assessment. This is where you pinpoint the specific weak points in your financial processes. Don’t overcomplicate it. Just start by brainstorming what could go wrong in your most critical areas.

Think through your day-to-day operations. Where does money come in, and where does it go out? Who has access to bank accounts, company credit cards, or your accounting software? These are the places where risks love to hide in plain sight.

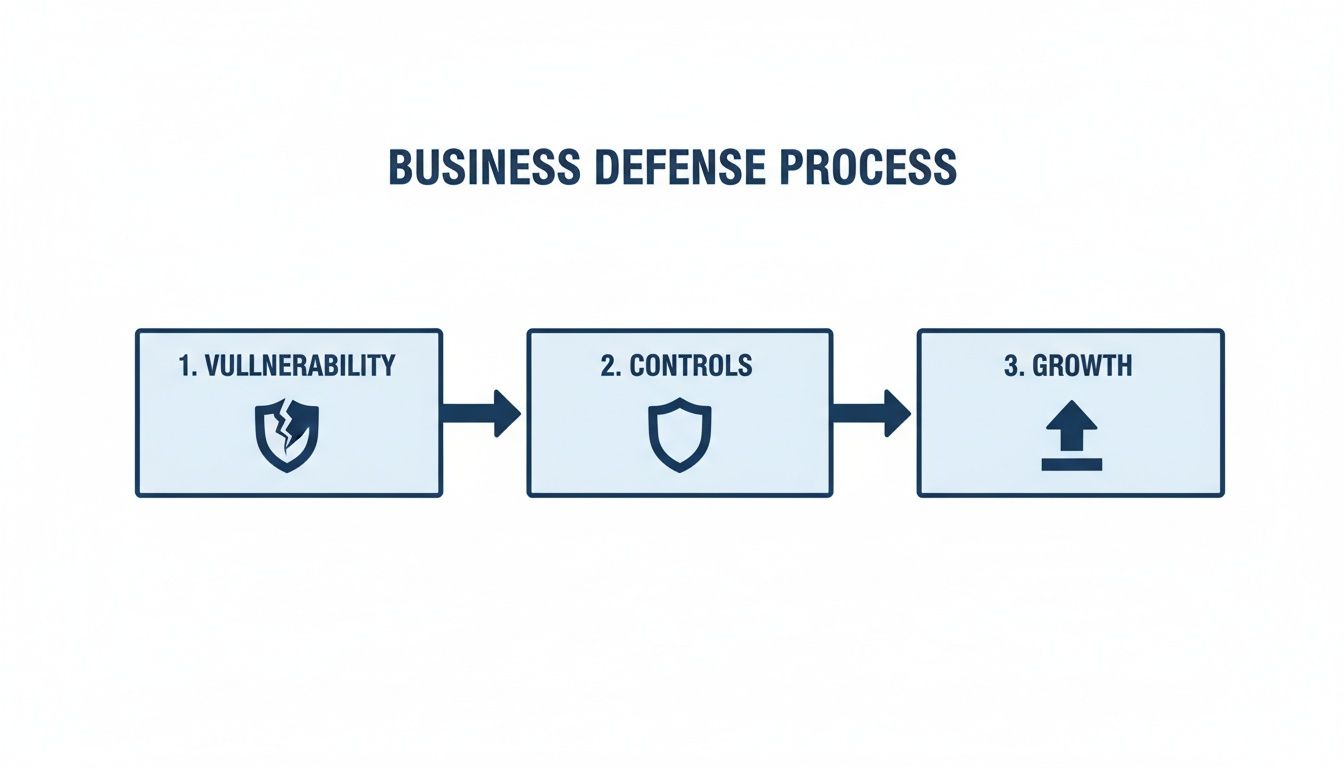

This flowchart shows how finding those vulnerabilities is the first step toward creating controls that actually help you grow.

As you can see, controls aren’t just a defensive shield. They’re the bridge that turns a potential weakness into a real business advantage.

Prioritizing Your Biggest Financial Risks

You can’t fix everything at once—and you don’t need to. The trick is to prioritize. A simple risk assessment helps you focus on what really matters by looking at two things for each risk you’ve identified: its potential impact and its likelihood.

- Potential Impact: If this happened, how bad would it be? A fraudulent $10,000 wire transfer is obviously a high impact. A minor invoicing error might be low impact.

- Likelihood: How likely is this to actually happen? If multiple team members share the same login for your bank account, the likelihood of an unauthorized transaction is pretty high.

Mapping your risks this way gives you a clear action plan. The high-impact, high-likelihood risks jump to the top of your list. This ensures you’re spending your limited time and resources shoring up the biggest vulnerabilities first. A key part of this is getting your books in order; understanding what a chart of accounts is is a foundational step in building that financial backbone.

A risk assessment isn’t about perfectly predicting the future. It’s about making educated guesses to guide your defense, focusing your energy where it will do the most good.

Here’s a simple template you can use to start mapping this out for your own business. Just walk through your key financial areas and think through what could go wrong.

Small Business Risk Assessment Matrix Template

| Business Area (e.g., Payroll, AP, Cash) | Specific Risk Example | Potential Impact (Low/Med/High) | Likelihood (Low/Med/High) | Priority for Control |

|---|---|---|---|---|

| Accounts Payable (AP) | An employee pays a fake invoice from a personal account. | High | Low | Medium |

| Cash Handling | Cash from a daily deposit goes missing before it hits the bank. | Medium | Medium | High |

| Payroll | An hourly employee’s overtime hours are calculated incorrectly. | Low | High | Medium |

| Accounts Receivable (AR) | Invoices are not sent to clients in a timely manner. | High | Medium | High |

This exercise isn’t meant to be exhaustive, but it will quickly reveal where you need to focus your attention first.

Creating a Phased Implementation Plan

With your prioritized risk list in hand, you can build a realistic, phased plan. The goal here is progress, not perfection. Start with the one or two controls that will neutralize your highest-priority risks.

For instance, if your biggest risk is unauthorized payments, your Phase 1 could look like this:

- Implement Owner Approval: The owner must personally approve any payment over $1,000 before it goes out the door.

- Review Bank Transactions Weekly: The owner will log in and review all bank and credit card activity every Friday morning without fail.

Once those new habits are locked in, you can move on to Phase 2 and tackle the next risk on your list. This step-by-step approach keeps you from getting overwhelmed and ensures the controls you create are practical, effective, and perfectly suited to the real risks your business faces.

Practical Control Activities You Can Implement This Week

Theory is great, but real security comes from taking action. This is where we stop talking about blueprints and start building. Let’s focus on specific, high-impact internal controls for small business that you can put into place right away. Don’t worry, these aren’t stuffy corporate procedures; they are practical safeguards designed for a growing service business like yours.

The idea is to weave these activities into your weekly and monthly routines until they’re second nature. Each one is designed to target a specific risk, creating layers of defense that protect your cash, keep your data clean, and ultimately, let you sleep better at night.

Fortifying Your Core Bookkeeping

Think of your bookkeeping as the foundation of your financial house. If it’s shaky, everything built on top of it is at risk. The strongest control you can implement here is a consistent, independent review.

The single most effective control for any small business is the mandatory monthly bank reconciliation. This is more than just making sure the numbers line up. It’s a detective control that can spot unauthorized transactions, bank errors, or even duplicate payments before they snowball into serious issues.

Here’s the critical part: the person reconciling the accounts cannot be the same person who handles daily deposits or writes checks. If you have a bookkeeper, you, the owner, must be the one to personally open and review the final reconciliation report and the bank statement every single month. No exceptions.

Pro Tip: Inside QuickBooks Online, run the “Reconcile” feature and make sure you save the PDF reconciliation report each month. I recommend creating a dedicated digital folder where you store both the report and the corresponding bank statement. This builds a clean, permanent audit trail you’ll be thankful for later.

This simple, non-negotiable habit is your first and best line of defense against a surprisingly wide range of financial shenanigans.

Smarter Payroll and HR Controls in Gusto

Payroll is usually a business’s biggest expense, making it a hot spot for both errors and fraud. With a small team, the risk of “ghost employees” or inflated pay rates is higher than you’d think. This is where a platform like Gusto can be a huge help.

A key preventative control is setting up dual approvals for new hires and any changes to pay rates. You can configure Gusto so that one person can enter a new employee’s details, but a second person—ideally the owner—has to give the final approval before they’re officially added to payroll. This simple step makes it nearly impossible for one person to create a fake employee and siphon funds to their own bank account.

Here are a couple of other Gusto-specific controls to set up:

- Role-Based Permissions: Don’t just give everyone “Full Admin” access. Assign limited roles. An office manager might need permission to run payroll, but they shouldn’t be able to change employee pay rates or direct deposit information.

- Run Payroll Reports: After every single payroll run, the owner should pull and review the “Payroll Journal” report. It’s a clean summary that shows exactly where every dollar went, making it easy to spot anything that looks off.

These tech-based controls essentially create a digital segregation of duties, giving you checks and balances even if you don’t have enough people for a traditional setup.

Locking Down Accounts Payable

Accounts payable (AP) is the main pipeline for cash flowing out of your business, so it needs to be airtight. The biggest risk here is paying for things you shouldn’t, whether it’s a phony invoice, a double payment, or an unauthorized purchase. The classic defense against this is the three-way match.

This process is all about making sure you only pay legitimate, authorized bills by verifying three documents against each other:

- The Purchase Order (PO): This shows what your company agreed to buy in the first place.

- The Receiving Report: This is your proof that you actually received the goods or services.

- The Vendor Invoice: This is the bill from the vendor for what they delivered.

When all three of these documents are in sync, you can pay the bill with confidence. Now, that might sound a little intense for a small service business, but you can use a simplified version. At a minimum, every single invoice should be formally approved (an email is fine!) by the person who requested the service before it gets entered for payment. You can dive deeper into this in our full guide to improving your accounts payable process.

Streamlining Accounts Receivable

With accounts receivable (AR), the main dangers are revenue that goes unbilled and a failure to actually collect the cash you’re owed. When your invoicing is all over the place, it leads to confused clients, payment delays, and a weak cash flow. Your best control here is standardization.

Create a simple, repeatable invoicing process. This means using a standard invoice template in QuickBooks Online that includes everything needed: an invoice number, date, due date, a clear description of the services, and your payment terms. This ensures every client gets a professional, clear, and consistent bill every time.

You also need a routine for collections. This isn’t about hassling clients; it’s about systematic, professional follow-up. For instance, you can set up QuickBooks to automatically send a reminder email when an invoice is one day past due, and then schedule a personal email from you at seven days past due. This consistency works wonders for improving collection times.

If you’re wondering why this all matters so much, consider this: a staggering 28% of small businesses are hit by fraud, and the average loss is $150,000 per incident. For a small firm, a blow like that can be devastating. These statistics underscore why having good internal controls isn’t just “nice to have.” As you can see from these examples, putting just a few smart controls in place can dramatically cut your risk of theft while also making your entire operation run more smoothly.

Solving the Segregation of Duties Dilemma on a Small Team

Segregation of duties is a bedrock principle for strong internal controls for small business. The concept is pretty simple: you don’t want one person controlling a financial transaction from beginning to end. This separation is your best defense against both honest mistakes and deliberate fraud.

But if you’re a small business owner with a lean team, this can sound completely impossible.

When you’ve only got one person handling the books, how can you possibly split up the work? This is one of the most common—and most legitimate—challenges I hear from clients. The good news is, you don’t need a big accounting department to build effective checks and balances. You just have to be a little creative.

The solution is a practical mix of smart task division, dedicated owner oversight, and leveraging technology. We call these “compensating controls,” and they can give you a surprisingly strong level of security, even if you can’t hit that textbook ideal of perfect segregation.

Strategic Task Division Even on a Small Scale

Even if your team is just you and one or two other people, you can still divide financial tasks in a way that significantly lowers your risk. Your goal isn’t to split every little thing, but to break the chain of control at the most critical points in your cash flow.

Think about the journey money takes into and out of your business. The real key is to separate the person who records the transactions from the person who can authorize them or reconcile the accounts.

Here are a few practical ways to divide duties:

- Accounts Payable: The team member who enters vendor bills into QuickBooks shouldn’t be the same one who approves the payment run or signs the checks.

- Cash Receipts: If you get checks in the mail, the person opening the mail and logging the checks should be different from the person who prepares the actual bank deposit.

- Bank Reconciliations: The person responsible for reconciling the bank account every month should not have the ability to approve payments or sign checks.

The Power of Compensating Controls

When you can’t fully separate duties, you can bridge the gap with compensating controls. These are simply extra review steps designed to catch the very issues that segregation would normally prevent. For any small business, the most powerful compensating control is active owner involvement.

You, as the business owner, are the ultimate backstop. Your consistent, hands-on review of the finances acts as a powerful deterrent and a crucial detection tool.

By setting aside a little time each week for oversight, you dramatically reduce your vulnerability to fraud. It sends a powerful signal that someone is watching, which is often all it takes to prevent problems before they even start.

Some high-impact compensating controls you can implement right away include:

- Mandatory Owner Review: You must personally open and look through every single bank and credit card statement each month. No exceptions. This is your chance to spot odd charges or unapproved withdrawals.

- Surprise Spot-Checks: Every so often, do a quick “mini-audit.” For example, randomly pull five payments from the previous month and ask to see the supporting invoices and proof of approval.

- Approval Thresholds: Require your direct approval for any payment over a specific dollar amount, like $500. This ensures you stay looped in on all significant cash outflows.

Your Technology Ally QuickBooks and Gusto

Modern accounting software is your best friend in this scenario. Platforms like QuickBooks Online and Gusto have features specifically designed to create a digital separation of duties, even if one person is doing most of the day-to-day work.

For example, you can set up role-based user permissions in QuickBooks to allow your bookkeeper to enter bills but restrict them from actually making payments or editing transactions after the books are closed. In Gusto, you can establish workflows where you, the owner, must approve any new employee added to payroll or any changes to pay rates.

Ignoring these safeguards comes with a real cost. Studies have shown that a lack of financial expertise and controls can cause profitability to drop by 30-40%. On the flip side, businesses that implement simple segregation, like separating invoice approval from payment, have seen a 60% reduction in fraud. Good controls can also help detect fraud 50% faster, minimizing potential damage.

In the end, achieving “perfect” segregation of duties isn’t really the point. The objective is to build a smart, layered system of internal controls for small business that makes it incredibly difficult for one person to make a major error—or commit fraud—without being noticed.

For many small teams, the best way to do this is by bringing in an outside partner. You can learn more about how to outsource your bookkeeping and create that crucial, independent layer of review.

Keeping Your Controls Effective for the Long Haul

Putting a new set of internal controls in place is a massive step forward, but it’s definitely not a “set it and forget it” kind of project. Your business is a living thing—you bring on new clients, your team changes, and your processes have to adapt. To keep your financial safeguards from becoming just another dusty binder on the shelf, you need a simple, repeatable way to monitor them.

Think of your controls as a garden. They need regular tending to stay healthy and effective. This doesn’t mean you need to launch a massive internal audit every month. It’s more about building smart, consistent review habits into the financial rhythm you already have. The goal is to create routines that help you spot trouble early, long before a small issue can snowball into a real problem.

Building Sustainable Monitoring Routines

Effective monitoring all comes down to consistency. When you build simple checks into your weekly and monthly schedule, you create a surprisingly powerful detection system. These routines don’t have to eat up your day, but they do have to be non-negotiable.

Here are two high-impact routines you can start with:

- Weekly Cash Flow Review: Block off 15 minutes every Friday to review cash in and cash out. Just pull up your bank balances and scan the recent transactions. This quick check-in keeps you plugged into your company’s financial pulse and makes it easy to spot an odd withdrawal or a customer payment that hasn’t hit yet.

- Monthly Budget-to-Actual Analysis: As soon as the month closes, run a “Budget vs. Actuals” report in QuickBooks. Think of this report as your financial scorecard. It instantly flags where spending is creeping up or where revenue might be lagging, letting you ask the right questions while the details are still fresh.

These simple habits can transform monitoring from a dreaded chore into one of your best strategic tools.

Using a Month-End Close Checklist

A “Month-End Close Checklist” is the best way to bring some structure to your monthly review. This isn’t just a to-do list for your bookkeeper; it’s a critical tool for you, the owner, to personally verify that key controls are being followed correctly. It turns an abstract idea like “monitoring” into a concrete set of actions.

To ensure your controls remain effective, using a formal internal audit checklist can seriously improve both your compliance and overall efficiency.

Your checklist has to be about verification, not just completion. It’s not enough to know the bank was reconciled. You need to actually see the report and confirm it ties out perfectly. For a small business owner, that hands-on review is a powerful control in itself.

Here’s a sample of what the owner’s portion of the checklist might look like:

| Task | Verification Step |

|---|---|

| Review Bank Reconciliation | Open the final PDF reconciliation report for all bank and credit card accounts. |

| Analyze Budget vs. Actuals | Look at the P&L Budget vs. Actual report. Question any variances over 10%. |

| Scan AP & AR Aging Reports | Check the Accounts Payable aging report for any overdue bills and the Accounts Receivable report to make sure collections are on track. |

| Spot-Check a Transaction | Randomly pick one large payment and ask to see the approved invoice that goes with it. |

The Importance of Communication and Training

At the end of the day, your controls are only as strong as the team that uses them. It’s so important that everyone on your team understands not just what the rules are, but why they exist in the first place. Clear communication and a little bit of training help reinforce that protecting the company’s finances is a responsibility everyone shares.

When you bring on a new team member who will touch any financial tasks, make a conversation about your internal controls a standard part of their onboarding. Explain the “why” behind things like requiring two people to approve a payment or always using a specific invoice template. Giving them that context helps build buy-in and makes it more likely the procedures will be followed carefully.

This is where a trusted financial partner can really help. Here at Steingard Financial, we support our clients by providing clean, easy-to-read reports that make these monitoring routines painless. We can also help you conduct periodic reviews to test your controls and suggest adjustments as your business grows, giving you the confidence to focus on what you do best.

Common Questions About Small Business Controls

Even with the benefits laid out, I find that most business owners still have a few nagging questions. It’s completely normal. Let’s tackle some of the most common concerns I hear, so you can feel confident putting your own internal controls for small business into place.

My Business Is Tiny. Are Internal Controls Really Necessary?

Absolutely. In fact, they might be even more critical when you’re small. When you only have a few people on the team, it’s very easy for one person to end up with way too much control over the finances, and that creates a major weak spot.

Simple controls can give you crucial oversight and stop costly mistakes or fraud before they happen. The point isn’t to wrap your business in red tape, but to build a few smart, simple checks and balances that protect your hard-earned assets right from the start.

Think of it this way: a single undetected mistake or a fraudulent transaction can have a devastating impact on a small business’s cash flow. For a larger corporation, it might be a blip. For you, it could be a crisis. Basic controls are your financial safety net.

How Can I Implement Controls Without Slowing My Business Down?

The trick is to build controls directly into your existing processes and let technology do the heavy lifting. A well-designed control system should actually make you more efficient over time, not slow you down.

For example, setting up approval rules in your software isn’t some extra, annoying step. If you use a platform like QuickBooks Online or a dedicated bill-pay service, you can automate the review process. This prevents a bad payment from ever leaving your bank account, which is far faster and less painful than trying to recover misspent money later on.

Start with your highest-risk areas first. Implement the controls that give you the biggest bang for your buck in terms of protection with the least amount of friction. Good controls reduce errors, make it clear who’s responsible for what, and give you much more reliable numbers for making faster, better decisions.

What Are the First Three Controls I Should Implement Right Now?

If you’re starting from scratch and want to make the biggest impact immediately, focus on these three. They are the bedrock of protecting your cash and making sure your financial records are trustworthy.

- Owner Review of Bank Statements: The business owner (or a trusted partner who isn’t involved in day-to-day bookkeeping) must personally open and look over every single bank and credit card statement, every month. This is a simple but incredibly powerful way to spot any funny business.

- Dual Payment Authorization: No single person should ever be able to both set up a payment and approve it. For old-school paper checks, this might mean requiring two signatures. For online payments, it means using software with built-in approval workflows to get a second set of eyes on all outgoing cash.

- Regular Bank Reconciliations: Your books need to be formally reconciled against your bank statements every single month, without fail. Critically, the person doing this job should not be the same person who handles cash receipts or payments. This provides an essential, independent check on your financial records.

Ready to move from questions to action? I get it—implementing these controls can feel like a lot, but you don’t have to figure it all out on your own. The team at Steingard Financial specializes in creating scalable back-office systems for service businesses, building in the right controls from the very beginning. Learn how we can give you peace of mind and help protect your business.