Per Diem Taxable: A Guide for Service Businesses

Your field team is traveling more. That usually means the business is growing.

It also means someone on your side is asking a deceptively simple question. “If we pay a daily travel allowance instead of reimbursing every meal, is per diem taxable?”

That question causes trouble because per diem sits in two different worlds at once. In one world, it is a clean, tax-free reimbursement. In the other, it becomes wages, lands on a W-2, and creates payroll tax consequences. The difference is not intent. It is process.

For service businesses, this gets harder fast. You may have technicians, consultants, project managers, and sales staff on the road. You may also have a mix of employees in Gusto, contractors in QuickBooks, and an operations team trying to keep everyone moving without building a paperwork maze. The IRS does allow a practical path. But the rules are strict, and small admin misses can flip a valid reimbursement into taxable pay.

The Hidden Tax Trap in Employee Travel Pay

A common scenario looks like this.

You send an employee to a client site for several days. Rather than asking them to save every lunch receipt, you decide to pay a daily amount for meals and lodging. It feels efficient. The employee likes the simplicity. Your payroll team likes the speed.

Then a problem appears later. The trip was real. The work was real. But the employee turned in the expense report late, or the report did not show where they traveled, or the amount paid was higher than the allowed rate for that location. Suddenly, what you thought was a reimbursement starts looking like compensation.

Why business owners get tripped up

Per diem sounds like a travel shortcut. In practice, it is more like a preset reimbursement system with strict guardrails.

Owners often assume the key issue is the dollar amount alone. That is only part of the story. The IRS also cares about whether the payment is tied to business travel and whether the company collected the right documentation on time.

Three misunderstandings cause most of the pain:

- “We paid for a real business trip, so it must be tax-free.” Not always. A valid trip still needs proper documentation.

- “If the amount seems reasonable, payroll can leave it off the W-2.” Reasonable is not the standard. IRS rules are.

- “Per diem is simpler than receipts, so there is less compliance risk.” It can be simpler, but only if your policy and software setup are disciplined.

Why this matters financially

When per diem taxable treatment applies, the issue does not stay inside accounting. It affects people.

The employee may see additional taxable wages. The company may need to run the amount through payroll and withhold employment taxes. Your books also become messier because what looked like a reimbursement now needs wage treatment.

Key takeaway: Per diem is not automatically tax-free because you call it per diem. It stays non-taxable only when the payment method, records, and timing all line up.

For a busy service business, that means travel policy is not just an HR document. It is a payroll control.

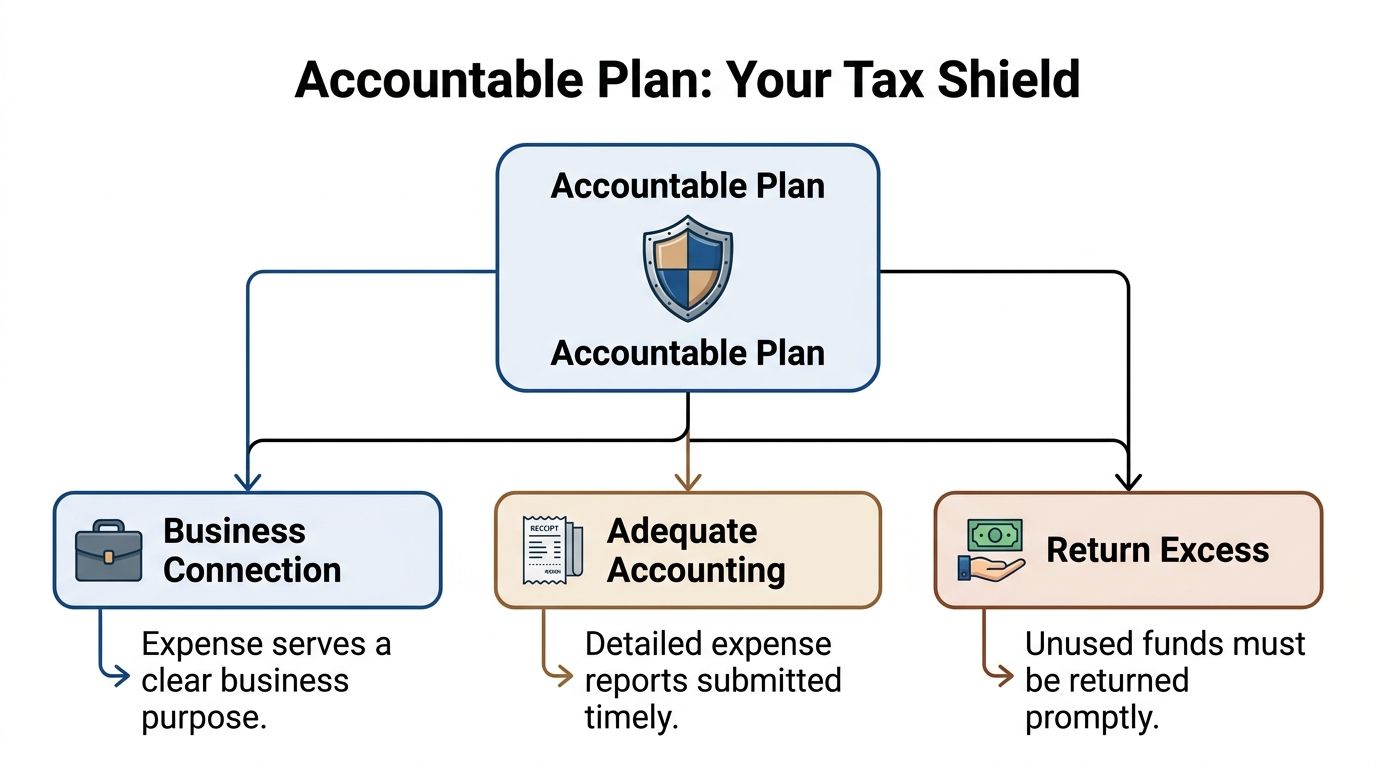

The Accountable Plan Your Shield Against Taxable Per Diem

The cleanest way to think about an accountable plan is this. It is the IRS rulebook for reimbursements.

If your business follows that rulebook, per diem can stay outside taxable wages. If your business does not, the payment can lose that protection. That is why I call it your shield. Not because it is fancy, but because it blocks avoidable tax problems before they hit payroll.

The three records the IRS cares about

The IRS states that non-taxable per diem depends on three documentary elements: business purpose, date and place of travel, and timely filing within 60 days in the IRS per diem FAQs.

That creates a strict result. If any one of those elements is missing, the tax treatment can fail even if the trip itself was legitimate.

Here is the practical version.

Business purpose

The report should show why the trip happened. Client meeting, project installation, training, site visit, or sales presentation are the kinds of details that matter.Date and place

“Traveled for work” is too vague. The record should show when the employee traveled and where they went.Timely filing

The IRS standard in the cited guidance is within 60 days. Miss that timing, and you can have a tax issue even when the amount itself was fine.

The part owners forget

Most owners focus on the employee submitting a report. They forget the plan also needs a discipline for handling overpayments.

If you advance or pay more than what fits the allowed reimbursement rules, the excess cannot just sit there. You need a process to identify it and treat it correctly.

That is where good record design matters. If your team needs a practical framework for receipts, reports, and approvals, this guide on record keeping for small business is a useful companion to your travel policy.

Consider it a company credit card policy

A company card is not “free money.” It is a controlled business tool. Per diem works the same way.

You are giving employees a simpler way to cover travel costs, but in exchange, the IRS expects proof that the payment was tied to business travel and handled under clear rules.

A workable accountable plan usually includes:

- A written policy that states who qualifies for per diem and what travel counts.

- A standard expense report that captures business purpose, travel dates, location, and required receipts.

- A deadline rule that operations and payroll enforce.

- A correction process for excess amounts or incomplete submissions.

Why software setup matters

QuickBooks and Gusto will only do what your process tells them to do.

If your payroll team codes every travel payment as a non-taxable reimbursement without checking the report, your system can produce a clean payroll run with the wrong tax treatment. Software is not the shield. The accountable plan is. Software just carries out the policy.

Practical tip: Build your travel form so an employee cannot submit it without entering business purpose, destination, and travel dates. That simple design choice reduces the risk of per diem taxable treatment caused by incomplete reports.

The accountable plan is where IRS theory becomes a daily operating habit. Without it, per diem is much easier to misuse than most owners realize.

Understanding Federal Per Diem Rates and Substantiation

A field supervisor leaves for a three-night job in Denver. Payroll sees “travel pay” on the timesheet, pushes it through Gusto as a reimbursement, and no one checks whether the daily amount matches the federal rate or whether the trip details made it into the file. That is how a routine travel payment turns into a tax problem.

Federal per diem rates give you a shortcut, not a free pass. They let you reimburse travel without reviewing every meal receipt, but only if you match the payment to the right location and keep enough support in your records.

Standard rate vs. location-specific rates

The General Services Administration publishes the federal travel rates for continental U.S. locations, and those rates vary by city. Some locations use the standard CONUS rate. Higher-cost cities use non-standard rates. You can look up the current amounts in the GSA per diem rate tables.

For a service business, this matters more than many owners expect. A technician sent to a smaller market and a project manager sent to Los Angeles should not automatically receive the same daily allowance. If your team travels often, the cleanest process is to have operations identify the travel city first, then let payroll or AP apply the correct rate inside QuickBooks or Gusto.

That setup matters because software follows the coding you give it. If the trip is tagged to the wrong city, the reimbursement can be wrong even when the payroll run looks clean.

What substantiation means in plain English

Substantiation is the record that proves the payment was tied to real business travel. A good way to view it is as the travel version of a work order. If the trip record is incomplete, the payment is hard to defend.

Your file should generally show:

- Business purpose

- Travel dates

- Destination

- Employee name

- Lodging receipts, when required by the method you use

The IRS explains the substantiation rules for travel, meals, and listed expenses in Publication 463. That publication is a useful reference when you are building forms and approval steps.

Owners often get tripped up on receipts. Per diem can reduce the need to collect meal receipts, but it does not erase the need to document the trip itself. Lodging can also require different support depending on how your plan is structured. The safe habit is simple. Make sure every travel report captures who traveled, where they went, why they went, and the dates they were there.

If the same trip also includes driving to customer sites, keep your vehicle records just as clean. A separate process for tracking business mileage accurately helps keep travel reimbursements consistent across meals, lodging, and auto use.

The high-low method

Some businesses with frequent travel prefer the high-low substantiation method because it reduces city-by-city lookups. Instead of checking each destination against the full federal table, you apply one rate for high-cost localities and another for all other localities.

If current IRS rules are extended, the high-low method for the period through September 30, 2026, would use the rates the IRS publishes for that period. The current annual notice and related guidance are the right source to check before you build those amounts into payroll rules or reimbursement templates. You can review that guidance in IRS Notice 2024-68.

The tradeoff is control versus precision. High-low is easier to administer, but only if your staff knows when it applies and your system separates meals and incidental expenses from lodging when needed. In QuickBooks and Gusto, that usually means separate expense or payroll mapping, not one catch-all travel code.

Common mistakes that create tax risk

Most per diem problems start in operations, then show up in payroll.

| Common issue | What goes wrong |

|---|---|

| Using one daily rate for every city | The reimbursement does not match the federal rate for the travel location |

| Treating per diem like a standing allowance | The payment starts to look like extra compensation instead of travel reimbursement |

| Missing trip details in the report | Payroll cannot show business purpose, dates, or location if the payment is questioned |

| Putting all travel under one code in software | Meals, lodging, and taxable corrections become harder to track and fix |

The practical goal is consistency. Your dispatcher, office manager, bookkeeper, and payroll team should all be working from the same trip record. That is what turns IRS theory into a process your software can support.

When Good Per Diem Goes Bad Taxable Scenarios

A field tech finishes a three-day service job out of town. Your office pays a flat travel allowance through payroll. The trip was real, the employee did the work, and everyone assumes the per diem is tax-free. Then payroll reviews the file and finds the expense report came in late, the lodging night was missing, or the amount paid was higher than the federal rate. What looked like a clean reimbursement can turn into taxable wages.

That is the trap. Per diem rules do not fail only when someone makes up a trip. They often fail on ordinary admin details.

For a service business, this matters because the problem usually starts in operations and ends in payroll. A dispatcher enters the job. A manager approves the travel. Then QuickBooks or Gusto has to decide whether that payment belongs in a non-taxable reimbursement bucket or in taxable wages. If the trip record is weak, the software cannot fix the tax treatment on its own.

The IRS framework is simple in concept. The payment stays non-taxable only if the travel qualifies, the amount is within the allowed rate, and the employee substantiates the trip on time. If one of those pieces breaks, some or all of the per diem can become taxable. The IRS explains the rules for travel reimbursements and accountable plans in Publication 463.

Same trip, different tax result

Here is a simple comparison for a 3-day trip.

| Scenario Detail | Compliant (Accountable Plan) | Non-Compliant (Late Report) |

|---|---|---|

| Type of trip | Overnight business travel | Overnight business travel |

| Per diem amount | Within the applicable federal rate | Within the applicable federal rate |

| Expense report | Submitted on time with business purpose, dates, and place | Submitted late |

| Tax treatment | Non-taxable reimbursement | Can become taxable wages |

The trip did not change. The paperwork did.

That is what confuses many owners. They focus on whether the employee traveled, but the tax result also depends on whether your process can prove the trip met the accountable plan rules.

A common excess-rate problem

Another taxable scenario is easier to miss. The travel is valid, the report is timely, but your company pays more than the allowed federal rate.

In that case, the excess amount is generally treated as wages. The overage is the problem, not necessarily the full payment. For example, if your software is set to one companywide daily rate and a technician travels to a lower-rate city, the difference can become taxable compensation unless you correct it.

This often happens after a well-meaning shortcut. The office wants one travel amount for all jobs, so payroll gets a single recurring code. That is simple to run, but it creates cleanup work later.

Four situations that turn per diem taxable

1. No overnight stay

Per diem is tied to travel away from the employee's tax home that requires sleep or rest. A long day trip may feel like travel pay to the employee, but it does not get the same tax-free treatment.

2. Late or incomplete substantiation

A missing report, missing dates, or no business purpose can break accountable plan treatment. In practice, this is like handing payroll half an invoice and expecting the books to stay clean.

3. Assignment lasts too long

If an employee keeps working in the same area long enough, that location can stop being temporary for tax purposes. At that point, per diem for that location can shift from reimbursement to taxable pay. This is a point service companies should watch closely on recurring projects and long service contracts.

4. Payment exceeds the federal rate

Amounts above the allowed rate generally do not stay fully tax-free. Your payroll team needs a way to separate the non-taxable portion from the taxable excess.

What this looks like in QuickBooks and Gusto

Here, IRS theory meets day-to-day processing.

In QuickBooks, one travel expense account for everything can hide problems until month-end or year-end. In Gusto, one reimbursement or earning setting can do the same if your team uses it for both accountable and taxable travel payments. A cleaner setup usually separates non-taxable per diem, taxable travel adjustments, and contractor travel payments so each item lands in the right place.

That separation helps with employee payroll now and with contractor reporting later. If your company sometimes pays travel amounts to nonemployees, your year-end team should also understand how to generate 1099s for contractors so those payments are reviewed correctly.

Why the cost is bigger than the per diem itself

A taxable per diem issue does more than change one line on a paycheck. It can increase taxable wages, payroll tax expense, and W-2 corrections. Employees may also lose trust if they were told a payment was a reimbursement and later see it treated as income.

The practical fix is boring but effective. Review trip support before payroll is finalized. In per diem compliance, clean records work like a wiring diagram. If every stop is labeled correctly, QuickBooks and Gusto can route the payment to the right place. If not, the tax problem shows up after the money is already out the door.

Handling Per Diem for Contractors and State Rules

Many service businesses use a blended workforce. The travel rules get more complicated the moment you move from W-2 employees to 1099 contractors.

For employees, per diem can be non-taxable when the accountable plan rules are met. Contractors are different. Payments to contractors that exceed federal rates often end up as taxable income reported on Form 1099, and self-employed individuals also face a 50% deduction limit on the meals portion of per diem under IRC §274(n), based on the guidance summarized in this contractor-focused per diem article.

Why contractor treatment feels counterintuitive

Owners often assume they can mirror the employee policy for contractors. That is where trouble starts.

A contractor is not on your payroll in the same way an employee is. So the familiar “non-taxable reimbursement through payroll” logic does not always carry over cleanly. From a bookkeeping standpoint, contractor travel payments often need separate handling and careful 1099 review.

If your team needs help with year-end contractor reporting, this walkthrough on how to generate 1099 for contractors is a useful operational reference.

Industry-specific exceptions add another layer

Some industries have special rules. For example, verified guidance notes that transportation workers have a special M&IE rate within CONUS.

That does not mean every service business can borrow those rules. It means you should avoid assuming one-size-fits-all treatment when you have specialized labor categories, union arrangements, or a contractor-heavy model.

Do not ignore state treatment

State law is where many multi-state businesses get surprised.

Federal treatment is your starting point, but it is not always your finish line. States may follow the federal framework closely, or they may apply their own withholding and wage-reporting rules. If your employees and contractors travel across state lines, the safe approach is to verify state treatment before locking a policy into payroll.

For owners, the practical lesson is simple. “Per diem taxable” is not just a federal payroll question. It is a worker-classification and jurisdiction question too.

How to Set Up and Run Per Diem in QuickBooks and Gusto

Knowing the rule is one thing. Getting the software to reflect the rule is where compliance occurs.

In QuickBooks Payroll and Gusto, the main objective is to separate non-taxable reimbursements from taxable wages. If you blur those categories, your reports can look clean while the tax treatment is wrong.

Build two lanes in your payroll process

The cleanest setup uses two distinct paths.

Lane one is non-taxable per diem. Use this only for payments that satisfy your accountable plan requirements. That means the trip qualifies, the report is complete, and the amount fits the applicable method you are using.

Lane two is taxable travel pay. Use this for excess amounts, late reports, day-trip allowances, or any payment that does not meet your policy requirements.

That separation helps your payroll reports tell the truth.

What to configure

In high-level terms, your setup should include:

- A reimbursement earning or pay type for accountable-plan per diem that is treated as non-taxable

- A wage earning or pay type for taxable travel payments

- A review step before payroll approval so someone checks the travel report against the coding

- A clear mapping in the chart of accounts so reimbursements and wage-related travel costs do not get mixed

If you use the high-low substantiation method, payroll and bookkeeping need to reflect the correct M&IE allocation. The verified method uses $319 per day for high-cost localities with $86 allocated to M&IE, and $225 per day for low-cost localities with $74 allocated to M&IE, as described in this high-low method summary.

That matters most when the meals portion needs separate attention for tax reporting or deduction purposes.

A simple workflow that works

A practical monthly routine often looks like this:

- Operations approves the trip details.

- The employee submits the travel report and required support.

- Accounting checks the location and method used.

- Payroll codes the amount as reimbursement or wages.

- Bookkeeping reviews the posting after payroll.

Where QuickBooks and Gusto users slip

The common failure is not software capability. It is rushing.

Someone enters a travel amount directly into payroll because the trip “looks business-related,” but the report has not been reviewed. That is how non-taxable coding gets applied too early. Another issue is posting all travel amounts to one account, which hides whether the payment was a reimbursement or taxable compensation.

Practical tip: Do not let payroll be the first place a travel payment gets evaluated. Decide tax treatment before the payroll run starts.

When your software mirrors your policy, per diem becomes manageable. When the setup is loose, the same software turns small process mistakes into year-end cleanup.

Frequently Asked Questions About Taxable Per Diem

Is per diem taxable for a one-day trip

Usually, yes. The verified guidance says day trips without overnight stays are always taxable under these rules.

Do employees need meal receipts for per diem

Not always. Per diem is designed to reduce receipt collection for meals, but substantiation still requires trip details, and lodging support may still be required depending on the method used.

What if an employee keeps going to the same client site for a long time

If travel to the same location lasts more than one year, that place can become the employee’s tax home under the verified IRS framework. Once that happens, per diem may lose non-taxable treatment.

Is per diem above the federal rate always a problem

It creates a tax issue for the amount above the allowed rate unless it is handled as wages. The excess portion is where many businesses need payroll involvement.

Can contractors get tax-free per diem the same way employees do

Do not assume that. Contractor treatment is different, and travel payments can become taxable income for 1099 reporting purposes.

Steingard Financial helps service businesses build clean payroll and bookkeeping systems that work in practical scenarios, especially when travel reimbursements, contractor payments, QuickBooks, and Gusto all need to line up. If you want help setting up a compliant per diem process that protects both your team and your books, visit Steingard Financial.