What Are T Accounts A Practical Guide for Modern Bookkeeping

If you've ever felt a bit lost in the world of accounting, you're not alone. But some of the most powerful tools are actually the simplest. The T-account is a perfect example—it’s a basic visual organizer that bookkeepers use to track the financial activity within a single account.

Its name is no mystery; it literally looks like a capital "T." This shape neatly separates the left side (debits) from the right side (credits), giving you a clear, at-a-glance view of what's happening.

Breaking Down T-Account Basics

Think of a T-account as a mini-ledger for just one category in your business. If you have an account for Cash, its T-account will show all the money that came in on one side and all the money that went out on the other. This visual separation is what makes it so useful.

These simple "T"s are the foundational building blocks of double-entry bookkeeping. This is the accounting method where every transaction has an equal and opposite entry in another account, which keeps your books perfectly balanced. You can learn more about this core principle in our double-entry bookkeeping explained guide.

The Purpose of a T-Account

At its heart, a T-account helps you isolate and analyze the activity in one specific part of your business. By focusing on one account at a time, it becomes much easier to:

- Track increases and decreases in your assets, liabilities, and equity.

- Gather the numbers needed to prepare key financial statements.

- Spot errors or inconsistencies when you're reconciling your books.

A T-account simplifies complex financial data into a digestible, two-sided format. It transforms abstract numbers into a clear story about what an account is doing—is it growing or shrinking?

To help you get comfortable with the layout, this table breaks down the core components of every T-account.

| The Anatomy of a T-Account |

| :— | :— | :— |

| Component | Location | Purpose |

| Account Title | Top Center | Identifies the specific account (e.g., Cash, Accounts Payable). |

| Debit Side | Left Side | Records increases to assets/expenses and decreases to liabilities/equity. |

| Credit Side | Right Side | Records increases to liabilities/equity and decreases to assets/expenses. |

Each part has a distinct role, but together they create a complete picture of an account's activity over a specific period.

Historical and Modern Relevance

This concept isn't some new-fangled idea; it's been a cornerstone of accounting for centuries. During the U.S. industrial boom from 1880-1920, T-accounts were essential for tracking costs as massive railroad companies managed incredible growth, hauling over 1 billion passengers annually by 1900.

Back then, accountants used these simple diagrams alongside new adding machines to make sure every dollar was accounted for.

Today, even with advanced software, understanding T-accounts is still incredibly valuable. To see how they apply in the real world, it helps to know the difference between concepts like Accounts Payable vs Accounts Receivable, as each one will have its own T-account in your books.

Mastering the Rules of Debits and Credits

To really get what T-accounts are all about, we first have to unlearn a common assumption. In the world of bookkeeping, debit and credit don't mean "bad" and "good" or "subtract" and "add." Think of them simply as directions: a debit is an entry on the left side of the T-account, and a credit is an entry on the right side. That’s it.

This two-sided system is the engine that powers all modern accounting. It's the core of double-entry bookkeeping, a method where every transaction always impacts at least two accounts. To keep the books balanced, every debit entry in one account must have an equal, opposite credit entry in another.

A Simple Mnemonic to Remember the Rules

At first, remembering which accounts go up with a debit and which go up with a credit can feel like a puzzle. This is where a fantastic little mnemonic comes in handy: DEALOR.

This acronym neatly splits the six main account types into two groups, making the rules much easier to recall.

- DEA (Dividends, Expenses, Assets): These accounts increase with a Debit (a left-side entry) and decrease with a Credit (a right-side entry).

- LOR (Liabilities, Owner’s Equity, Revenue): These accounts increase with a Credit (a right-side entry) and decrease with a Debit (a left-side entry).

Let's think about your business's cash, which is an Asset. When you get paid by a customer, your cash increases, so you debit your Cash account. When you spend that money on supplies, your cash decreases, so you credit the Cash account.

Applying the Debit and Credit Rules

Now, let's see how these rules play out for each account type in the DEALOR framework. Getting this logic down is the single most important step to recording any business transaction accurately.

Accounts Increased by Debits (DEA)

- Assets: These are the resources your company owns, like cash in the bank, equipment, or money owed to you (Accounts Receivable). When you get more of an asset (like a customer paying an invoice), you debit that asset account to increase it.

- Expenses: These are all the costs of running your business—think rent, salaries, or marketing costs. When you pay a bill, you've incurred an expense, so you debit the right expense account.

Rule for Assets & Expenses: An increase is recorded as a debit (on the left side of the T-account). A decrease is recorded as a credit (on the right side).

Accounts Increased by Credits (LOR)

- Liabilities: This is money your business owes to someone else. It could be a bank loan or an unpaid bill from a vendor (Accounts Payable). When you take out a loan, your debt increases, so you credit that liability account.

- Owner's Equity: This represents the owner's stake or investment in the business. When an owner puts their own money into the company, you credit an equity account to show that increase.

- Revenue: This is the income your business earns from selling goods or providing services. When you finish a project and send an invoice, you've earned money, so you credit a revenue account.

If you'd like to dive deeper, our detailed post on understanding debit and credit in accounting provides additional examples and context. Applying these rules consistently is the key to ensuring your financial records are always accurate and perfectly balanced.

Putting T-Accounts to Work with Real-World Examples

Theory is one thing, but the real "aha!" moment comes when you see T-accounts in action. To make this all click, let's walk through a few everyday transactions for a fictional service business. This is the best way to see how debits and credits are just two sides of the same coin, working together to keep your books perfectly balanced.

We’ll follow along and record five common business events:

- The owner makes an initial investment.

- The business buys new equipment.

- Services are provided to a client on credit.

- The client pays their invoice.

- A utility bill is paid.

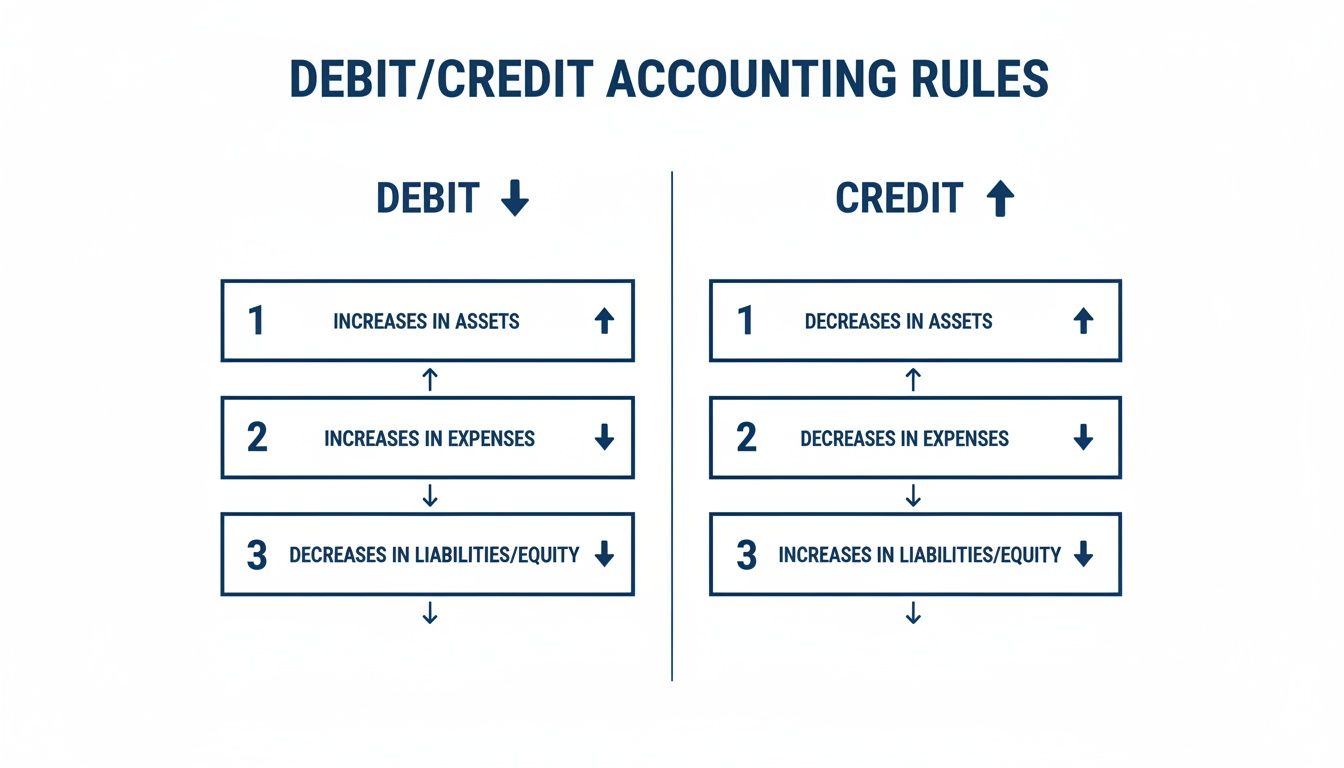

This infographic is a great visual cheat sheet for the debit and credit rules we'll be using.

As you can see, the left side (debit) is used to increase assets and expenses. The right side (credit) is for increasing liabilities, equity, and revenue.

Example 1: Owner Investment

To get the business off the ground, the owner puts $10,000 of their own money into the company's bank account. This single action affects two accounts: Cash (an Asset) and Owner's Equity.

- Cash: This is an asset, and it just went up. So, we debit the Cash account for $10,000.

- Owner's Equity: The owner's stake in the business also increased. We credit Owner's Equity for $10,000.

The debit and credit match perfectly, and our accounting equation stays balanced. Simple as that.

Example 2: Purchasing Equipment

Next up, the business buys a new computer for $2,000, paying with cash. This is a classic example of swapping one asset for another.

- Equipment: The business now owns a new asset, so the Equipment account goes up. We debit it for $2,000.

- Cash: The business used cash to buy the computer, so that asset account goes down. We credit it for $2,000.

Notice how the total value of assets didn't change—the value just moved from one account to another.

Example 3: Billing a Client

The business finishes a project and sends the client an invoice for $5,000. The client hasn't paid yet, but we've earned the money and need to record it.

This transaction creates an account called Accounts Receivable. It’s a crucial asset for any service business, representing money that is owed to you. T-accounts make it easy to track who owes you what.

Here's how we log it:

- Accounts Receivable: This is an asset (money people owe you), and it just increased. We debit it for $5,000.

- Service Revenue: You've earned income, which increases your revenue. We credit Service Revenue for $5,000.

Even though no cash has changed hands yet, your books now accurately reflect that you've earned that income.

Example 4: Receiving Client Payment

A few weeks go by, and the client pays their $5,000 invoice in full. This is another asset swap—the client's promise to pay is being converted into actual cash.

- Cash: Your bank account balance just went up, so you debit the Cash account for $5,000.

- Accounts Receivable: The client no longer owes you this money, so that asset account decreases. We credit Accounts Receivable for $5,000.

If you were to look at the Accounts Receivable T-account for this specific client, its balance would now be zero. Mission accomplished.

Example 5: Paying a Bill

Finally, the monthly internet bill for $150 is due, and the business pays it with cash. This transaction involves an expense and a decrease in an asset.

- Utilities Expense: Your expenses have increased for the month. We debit the Utilities Expense account for $150.

- Cash: You paid the bill from your bank account, so your cash has decreased. We credit the Cash account for $150.

While we've used simple T-accounts, this is the exact logic that powers modern accounting software. For the service businesses we work with at Steingard Financial, getting this foundation right in a QuickBooks setup is non-negotiable. In fact, 70% of small businesses report fewer headaches with reconciliation once their chart of accounts is properly optimized. It makes tracking AP/AR and running payroll through tools like Gusto so much clearer.

These core principles have been around for centuries, and you can learn more about the evolution of accounting practices to see just how durable these ideas are.

How T Accounts Generate Financial Statements

So, you’ve tracked all your business activities using T-accounts, and now you have a collection of balanced entries. But how do these individual accounts transform into the financial reports you need to actually run your business? This is where the real magic of accounting happens.

It all starts by figuring out the final balance of every single T-account. For Cash, Accounts Receivable, Service Revenue, and every other account, you just add up the debits, add up the credits, and find the difference. That single number represents the account's final standing for the period.

Creating the Trial Balance

Once you have a final balance for each account, you’ll put them all together in a document called a trial balance. Think of it as a master checklist for your entire accounting system. It’s a simple two-column list: one column for all the accounts with debit balances and another for all those with credit balances.

The trial balance has one job: to prove that your books are, well, in balance. You add up the total of the debit column and the total of the credit column. If they match, it confirms your fundamental accounting equation has held true across every transaction.

A balanced trial balance is your green light. It’s the first major checkpoint that tells you your debits equal your credits across the board, which means you're ready to build your financial statements. If the totals don't match, it’s an immediate red flag that an error is hiding somewhere in your books.

From Trial Balance to Final Reports

With a balanced trial balance confirmed, creating your main financial statements is mostly an exercise in sorting. The accounts on your trial balance are simply moved to their designated report—either the income statement or the balance sheet.

- Income Statement: All your revenue and expense accounts (like Service Revenue or Utilities Expense) go here. When you subtract your total expenses from your total revenues, you get your net income or loss.

- Balance Sheet: All your asset, liability, and equity accounts (like Cash, Equipment, and Owner's Equity) are organized on the balance sheet. This report gives you a snapshot of your company's financial position at a specific moment in time.

This orderly flow from transaction to T-account to trial balance is what gives you confidence in your financial reports. At Steingard Financial, we use this same underlying logic in QuickBooks to deliver faster month-end closes for our clients. In fact, after we optimize their systems, 78% of our clients see their close process speed up by 50%, even while we manage AP/AR volumes that are growing 40% year-over-year. The history of accounting has always been about creating systems for clarity, a topic you can explore further on The Street.

The final step is making sure everything ties together. The net income calculated on the income statement flows into the equity section of the balance sheet, completing the cycle and ensuring both statements are perfectly reconciled. To see this process laid out in more detail, take a look at our guide on how to prepare financial statements.

Finding and Fixing Common T-Account Mistakes

Look, nobody's perfect. Even the most seasoned bookkeepers make mistakes, so it's a completely normal part of learning. Since the whole point of double-entry is that debits must always equal credits, even one small slip-up can throw your entire trial balance out of whack.

The good news is that these imbalances almost always leave behind clues. Instead of getting frustrated, think of it like a puzzle. Learning to spot the patterns is a key skill for keeping your books clean and accurate.

Identifying Transposition and Slide Errors

Two of the most common culprits behind an unbalanced trial balance are transposition errors and slide errors. They sound technical, but they're just simple typos.

- A transposition error is when you accidentally flip two digits in a number. For example, you meant to write $87 but typed $78 instead.

- A slide error, or a decimal point error, is when you put the decimal in the wrong spot. For instance, you record $100.00 as $1,000.00 or maybe $10.00.

Here’s a great trick to find them. First, calculate the total difference between your debits and credits. If that difference is cleanly divisible by 9, you're almost certainly looking at a transposition error. If the difference is divisible by 99, or if it’s a number with a bunch of zeros and one digit (like $900), you probably have a slide error. This little math hack can save you hours of searching.

Correcting Reversed Entries

Another mistake that happens all the time is just getting your debits and credits backward. Say a customer pays their invoice; you should debit Cash (to increase it) and credit Accounts Receivable (to decrease it). It's easy to accidentally do the exact opposite.

You’ll usually spot this when an account balance just doesn't look right. You might see a negative Cash balance (which is impossible unless you're overdrawn) or a credit balance in an expense account. These are huge red flags.

The fix is simple: you’ll make a correcting journal entry. This entry does two things. First, it reverses the incorrect entry to zero it out. Then, it records the transaction the right way. This keeps your audit trail clean and ensures your T-accounts tell the true story.

By knowing what to look for, you can quickly find and fix your own work. The logic of T-accounts is actually designed to help you catch these very mistakes, building your confidence and ensuring your financial records are always reliable.

How Modern Accounting Software Uses T Account Logic

You’ll probably never need to draw a physical T-account for your business, but that doesn't mean they aren't there. T-account logic is the invisible engine running inside all modern accounting software. Platforms like QuickBooks don't show you the literal "T," but they rely on its double-entry principles for every single transaction you record.

Think of your Chart of Accounts as a massive, digital collection of T-accounts working silently in the background. When you create an invoice, pay a bill, or run payroll through an integrated app like Gusto, the software automatically makes the correct debit and credit entries to the right accounts. You're just filling out a simple, user-friendly form, while the system does the heavy lifting of keeping everything in balance.

This is precisely why understanding the concept of a T-account is so important. It’s the foundational logic that ensures every number on your financial reports is accurate, reliable, and makes sense.

The Hidden Power of Automation

The real strength of this system is its consistency. By automating the debit and credit rules, software all but eliminates the human errors that can throw your books out of balance. This ensures every transaction is categorized correctly from the start, giving you real-time data you can actually trust to make decisions.

This structured approach isn't just a modern convenience; it has a long, proven history of helping businesses build resilience. Historical data shows that firms using double-entry T-account logic saw 25% higher survival rates during economic downturns. That same principle holds true today, where 82% of startups using structured bookkeeping successfully avoid the early-stage cash flow crises that sink so many others. You can explore more about the long history of accounting and see how these core ideas have evolved.

Frequently Asked Questions About T Accounts

Even after you get the hang of T-accounts, a few practical questions almost always come up. Here are some of the most common questions we hear, which can help clarify how T-accounts fit into the world of modern accounting.

Do Professionals Still Use Manual T-Accounts?

While you won’t find an accountant at Steingard Financial sketching out T-accounts on paper for daily bookkeeping, the concept is anything but outdated. Today, T-accounts are mainly used as a teaching tool because they are so effective at explaining the rules of double-entry accounting.

The real value is in the logic. That same logic is what powers professional accounting software like QuickBooks. If you understand how a manual T-account works, you’ll have a much better grasp of why your software records transactions the way it does. It helps you become a smarter, more confident user of these essential tools.

What Is the Difference Between a T-Account and the General Ledger?

The easiest way to think about it is like a single chapter versus the entire book. A T-account is like one chapter, focused entirely on a single account, such as "Cash" or "Office Supplies." It shows you every increase and decrease for just that one category.

The general ledger, on the other hand, is the complete book. It is the full collection of every single T-account your business has. When you need to see the complete financial story, you turn to the general ledger, which holds all the transactions recorded across all your accounts.

Can a T-Account Have Only Debits or Only Credits?

Yes, that happens all the time. It’s very common for an account to only have entries on one side during a certain period, especially when an account is new.

For example, if you create a new "Utilities Expense" account, it will probably only have debits (which increase an expense) for the first month or two. Likewise, if you take out a new loan, that new liability account will only show credits until you begin making payments.

Ready to get your books in order with experts who understand the logic from the ground up? Steingard Financial offers meticulous bookkeeping and payroll services to give you accurate data and peace of mind. Visit us at https://www.steingardfinancial.com to learn how we can help.