What Is a 940? Your Guide to the FUTA Tax Form

You hired people, set up payroll, and started running the business. Then the tax forms started showing up.

For many service business owners, Form 940 is one of those forms that gets handled in the background until something feels off. A payroll report does not match your records. A deposit looks smaller or larger than expected. Your year-end filing asks questions you have not thought about since onboarding your first employee.

That is where a lot of confusion starts.

If you have searched what is a 940, the short answer is simple. It is the annual federal unemployment tax form. The more useful answer is this: Form 940 is not just a filing requirement. It is one of the best year-end checkpoints for spotting payroll mistakes before they turn into penalties, notices, or messy cleanup.

Understanding Your Employer Tax Responsibilities

Hiring your first employee changes your tax life.

Before payroll, most business owners only think about income taxes, sales taxes, and maybe estimated payments. Once you become an employer, you take on a separate set of responsibilities tied to wages, reporting, deposits, and tax forms. Some of those amounts come out of employee paychecks. Others are paid by the business itself.

Form 940 belongs in the second category.

Owners often assume every payroll tax works the same way, which is incorrect. Some taxes are withheld from employees. Some are shared between employer and employee. Some are employer-only. Form 940 deals with an employer-only federal unemployment tax.

Why this catches owners off guard

Individuals typically learn about payroll through pay stubs. They see withholding for income tax, Social Security, and Medicare. That makes those taxes feel visible.

FUTA is different. It usually does not show up as an employee deduction. It is more like a behind-the-scenes cost of having staff.

That is why owners can miss it until year-end.

A practical way to think about employer payroll obligations is to split them into three buckets:

- Employee withholdings: Amounts taken from employee pay and remitted to tax agencies.

- Employer match or employer-paid taxes: Amounts the business owes because it has employees.

- Reporting and reconciliation forms: The forms that tie your wage records and tax payments together.

If you want a broader grounding in how these responsibilities fit together, this overview of payroll compliance issues is useful: https://steingardfinancial.com/tag/what-is-payroll-compliance/

Good systems reduce stress

Form 940 gets easier when payroll is set up cleanly from the start.

That means using payroll software that tracks taxable wages correctly, separates employer taxes from employee withholdings, and keeps deposit history easy to review. If you are comparing systems, this roundup of top payroll providers gives a practical starting point.

Tip: The biggest Form 940 problems usually begin months before filing. They start with payroll setup, wage mapping, or missed tax deposits.

What Is Form 940 and the FUTA Tax

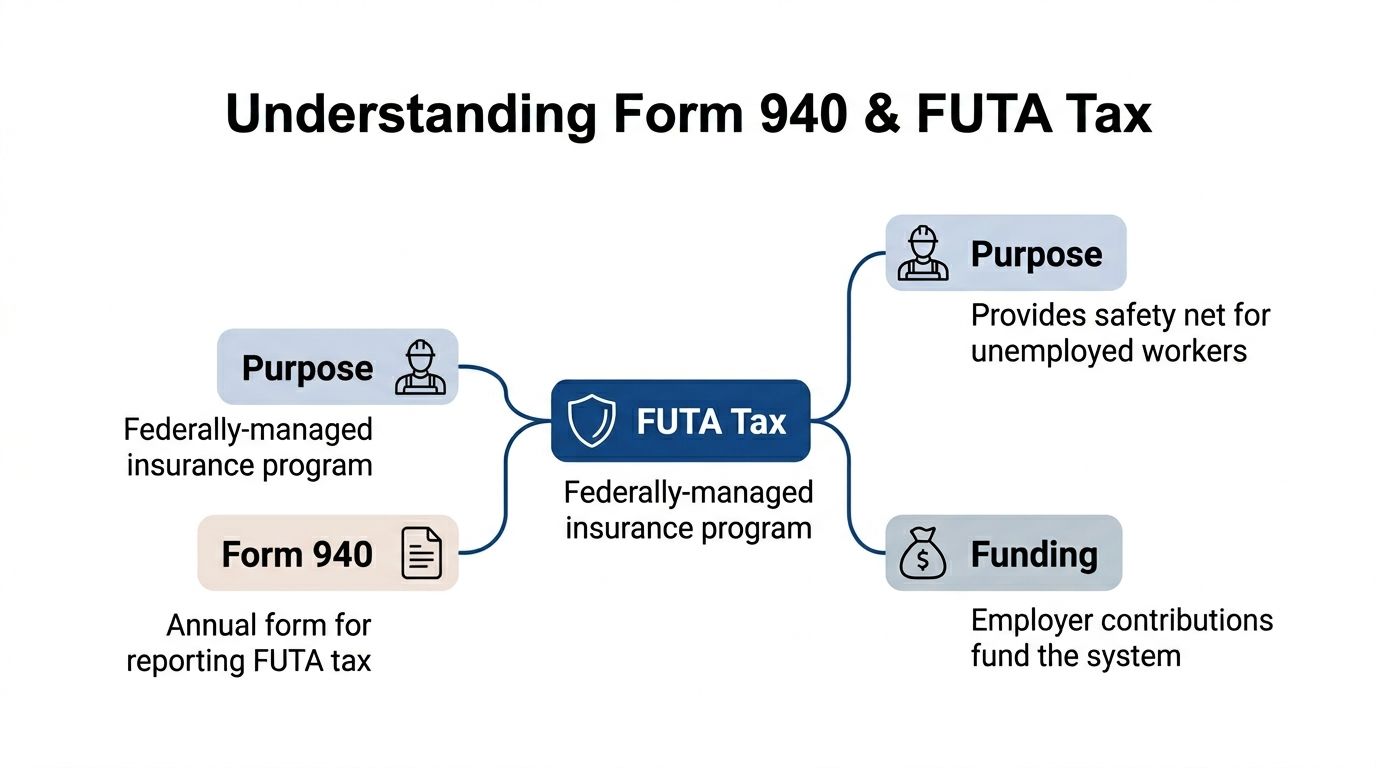

IRS Form 940 is the Employer's Annual Federal Unemployment (FUTA) Tax Return. Most U.S. businesses with employees use it to report and pay federal unemployment tax. It is an annual employer-paid form, not an employee withholding form, and it affects over 6 million employers annually according to Paychex.

Think of FUTA like an employer-funded safety net

FUTA functions as a federally managed insurance system.

Employers fund the system through federal unemployment tax. That money supports the broader unemployment framework that helps workers who lose their jobs. You do not take FUTA out of employee wages. The business pays it.

That one distinction clears up a lot of confusion.

Form 940 is not Form 941

Owners often mix up these two forms because both deal with payroll.

They serve different jobs:

- Form 940 reports federal unemployment tax for the year.

- Form 941 reports withheld federal income tax, Social Security, and Medicare taxes on a quarterly basis.

A simple analogy helps. If payroll were a car, Form 941 would be your regular dashboard checks throughout the year. Form 940 would be the annual inspection focused on one specific system.

Who usually has to file

A business generally files Form 940 if either of these apply:

- You paid wages of $1,500 or more in any calendar quarter, or

- You had employees for part of a day in 20 or more different weeks in the current or prior year

That coverage includes full-time, part-time, and temporary workers. Partners in partnerships are excluded.

What confuses owners most

The phrase "annual form" makes some owners assume they can ignore FUTA until January.

That is risky.

Form 940 is annual, but the tax it reports may need attention during the year. Your payroll records, wage categories, and deposit history all feed into the final form. If those records are off, the annual filing will expose it.

Key takeaway: When someone asks what is a 940, the technical answer is "the annual FUTA return." The practical answer is "your year-end report card for federal unemployment tax."

How to Calculate Your FUTA Tax Liability

A busy owner often looks at Form 940 in January and wonders why the number on the page feels disconnected from the payroll run they approved all year.

The answer is that FUTA follows its own logic. It is less like a percentage of total payroll and more like a year-end diagnostic check on how each employee moved through your wage records. If the setup was clean, the math is straightforward. If it was messy, Form 940 usually exposes the weak spots.

Start with the frame. The IRS applies FUTA to the first $7,000 of wages paid to each employee for the year, and the statutory FUTA rate is 6.0%, as explained in the IRS Form 940 instructions. That means the maximum gross FUTA tax for one employee is $420 before any credit for state unemployment taxes.

Here is the simplest way to calculate it:

- Identify each employee’s FUTA-taxable wages.

- Stop counting wages for that employee after they reach $7,000 for the year.

- Multiply those taxable wages by 6.0%.

- Subtract any allowed credit for state unemployment taxes paid on time.

One employee makes the pattern easy to see.

If an employee earns $50,000 for the year, FUTA does not apply to all $50,000. It applies only to the first $7,000. At 6.0%, the gross FUTA amount is $420. If you qualify for the full state unemployment credit, your effective federal rate usually drops to 0.6%, which brings that employee’s net FUTA cost down to $42.

Now scale that up to a team.

If 10 employees each earn at least $7,000 during the year, your gross FUTA liability is $7,000 × 10 × 0.06, or $4,200 before credits. With the full credit, the net amount usually falls to $420. That is why two businesses with the same annual payroll can have different FUTA results. Employee count, turnover, and how quickly each worker reaches the wage base all affect the outcome.

For service businesses, that matters more than many owners expect. A stable office with a small long-term team may hit a predictable pattern early in the year. A business with seasonal hiring, part-time staff, or frequent replacements may keep creating new batches of first-$7,000 wages. That raises FUTA exposure even if total payroll does not change much. Form 940 becomes useful beyond filing by helping you spot payroll patterns that increase tax cost.

Wage classification errors are common. So are setup errors in payroll software. FUTA should stop calculating for an employee after the wage base is reached, but exempt payments must also be handled correctly. Depending on the facts, certain fringe benefits, group-term life insurance, and dependent care assistance may be excluded from FUTA wages under the IRS instructions.

If your books need a clearer framework for how these amounts sit on the balance sheet before payment, this guide to payroll liabilities gives the broader bookkeeping context.

Here is a video walk-through that can help make the moving parts feel less abstract.

Deposits also belong in the calculation conversation because timing affects cost. The IRS states that if your undeposited FUTA tax is more than $500 at the end of a quarter, you generally must deposit it by the last day of the following month. Owners who wait until year-end to review FUTA often learn that the math was right but the deposit timing was wrong, which can lead to penalties and interest.

A practical routine helps. Review FUTA by employee each quarter. Confirm who has already reached the $7,000 cap. Check whether exempt wage items were coded correctly. Then compare your payroll reports to what Form 940 will eventually require.

Practical advice: Calculate FUTA during the year, not just at filing time. Used that way, Form 940 works like an annual payroll checkup. It shows whether your wage caps, tax settings, and deposit habits are keeping your business compliant or creating avoidable cost.

Why Your FUTA Rate Might Be Higher Than 0.6%

A lot of guides stop at the happy path.

They say the FUTA rate is effectively 0.6% after the normal credit and move on. That is incomplete. Some employers pay more than that because the credit can be reduced.

The credit is not automatic in every situation

Many guides mention that employers can often reduce the FUTA rate to 0.6%, but they do not explain when that credit is unavailable or reduced. In FUTA credit reduction states, the effective rate can rise well above the commonly cited 0.6%, which creates a real budgeting issue for service businesses according to HR for Health.

Here is the plain-English version.

If a state has borrowed from the federal government for unemployment benefits and has not repaid those loans on time, employers in that state may lose part of the normal FUTA credit. That means the federal unemployment tax bill goes up.

Why this matters in real life

This issue often catches growing employers by surprise for two reasons.

First, payroll software may show a familiar FUTA framework all year, so owners assume the standard effective rate applies. Second, businesses operating in more than one state may not realize they need extra review at year-end.

For employers with multi-state operations, Schedule A on Form 940 is the place where credit reduction issues get reflected.

A better way to budget for FUTA

Do not budget FUTA using only the headline rate you have heard from generic guides.

Instead, review:

- Where employees worked: Multi-state payroll creates extra complexity.

- Whether any operating state has credit reduction status: This can raise the effective federal cost.

- Whether payroll reports tie to state unemployment filings: Mismatches can reduce confidence in your numbers.

Key takeaway: The widely quoted 0.6% rate is a common outcome, not a universal promise.

Navigating Form 940 Filing and Deposit Schedules

The easiest way to avoid Form 940 trouble is to separate filing from depositing in your mind.

They are connected, but they are not the same deadline.

Annual filing deadline

Form 940 is due January 31 each year.

If all required FUTA taxes were deposited on time, the filing deadline extends to February 10.

That extension helps, but it only helps employers who stayed current during the year.

Deposit timing

Even though the return is annual, deposits may be due during the year when your FUTA liability is high enough.

Use this rule:

- If quarterly FUTA liability is more than $500, deposit by the last day of the month after the quarter ends.

- If it is $500 or less, carry it forward to the next quarter.

A simple timeline looks like this:

| Quarter | Quarter ends | Deposit timing if liability is over $500 |

|---|---|---|

| First | March 31 | Due by the last day of the following month |

| Second | June 30 | Due by the last day of the following month |

| Third | September 30 | Due by the last day of the following month |

| Fourth | December 31 | Due by the last day of the following month, unless carried into filing |

Where owners mix things up

Many owners hear "annual FUTA form" and assume they only need to think about it once.

That leads to missed deposits.

Others deposit correctly but fail to file the actual form on time. Both sides matter. The deposits pay the tax. The form reconciles and reports it.

If you also handle quarterly payroll tax filings, this guide to Form 941 e-filing helps clarify the difference in cadence between annual and quarterly payroll forms: https://steingardfinancial.com/form-941-electronic-filing/

Beyond Compliance How Form 940 Reveals Payroll Health

The strongest reason to take Form 940 seriously is not just compliance.

It is reconciliation.

When you prepare the form properly, you compare total wages paid, taxable wages, exempt wages, and deposits already made. That process often reveals issues that stayed hidden all year.

What Form 940 can uncover

Form 940's critical function is reconciliation. It forces employers to reconcile wages paid against deposits made, and that process frequently surfaces payroll errors, misclassified workers, or missing deposits according to Cypress Benefit Solutions.

That makes it much more than a form you file and forget.

A clean reconciliation can confirm that your payroll process is working. A messy one can point to deeper operational problems.

Common red flags during the reconciliation process

These are the kinds of issues that often show up when owners or bookkeepers review Form 940 carefully:

- Deposits do not match payroll reports: The tax may have been calculated but not paid correctly.

- Taxable wages look too high: FUTA wage caps may not have been applied properly.

- Exempt wage categories were missed: Benefits or other excluded amounts may still be sitting in taxable totals.

- Payroll changed providers mid-year: Data may not have transferred cleanly between systems.

- State and federal unemployment records do not align: This can lead to credit problems or filing confusion.

Why this matters for service businesses

Service businesses often have changing schedules, part-time workers, seasonal staffing, and frequent onboarding. Those realities create more opportunities for payroll coding errors.

If you use QuickBooks Payroll, Gusto, or a combination of software plus manual adjustments, Form 940 becomes a year-end checkpoint on your payroll process. It can show whether your system is scalable or whether it is being held together by workarounds.

Tip: Treat the 940 review like an annual payroll audit. If the numbers reconcile cleanly, that is reassuring. If they do not, fix the process, not just the form.

Common Questions About IRS Form 940

Some questions come up again and again, especially for owners managing payroll for the first time.

Form 940 vs. Form 941 at a glance

| Attribute | Form 940 | Form 941 |

|---|---|---|

| Purpose | Reports federal unemployment tax | Reports withheld income tax plus Social Security and Medicare taxes |

| Filing frequency | Annual | Quarterly |

| Who pays the tax | Employer only | Includes amounts tied to employee withholding and employer payroll tax responsibility |

| Employee withholding involved | No | Yes |

| Main focus | FUTA | Federal employment taxes from regular payroll cycles |

Do employees pay FUTA tax

No. Form 940 covers an employer-paid tax.

Employees do not have FUTA withheld from their paychecks.

What if I made a mistake on a prior Form 940

If a previously filed Form 940 needs correction, the usual approach is to file an amended return by checking the amended return box on Form 940.

Do not ignore the mistake and hope the next filing smooths it over. Year-end payroll forms are built to reconcile specific periods.

Do owners of S corporations count

S corporation owner wages for services rendered are included in wages for FUTA purposes. The tax still applies only to the first portion of annual wages that are subject to the FUTA wage base.

Do partners in a partnership count

No. Partners in partnerships are excluded for this purpose.

What if my payroll company files everything

You still need to understand what is being filed.

Payroll providers help with calculation, deposits, and filing, but the employer remains responsible for making sure the data is right. If your books, payroll reports, and tax filings do not agree, the issue belongs to the business even if software prepared the form.

Is what is a 940 a question only new employers ask

Not at all.

Established businesses ask it too, usually after a provider switch, a state notice, a rapid hiring stretch, or a year-end reconciliation problem. The form itself is straightforward. The surrounding payroll data is where complexity tends to build.

If your payroll reports, tax deposits, and year-end filings do not line up cleanly, Steingard Financial can help you sort out the underlying issue, clean up the records, and build a payroll process that stays accurate as your business grows.