When you're digging into your company's financials, two terms you'll constantly encounter are the general ledger and the trial balance. It’s easy to get them mixed up, but they play very different roles. The simplest way to think about it is that the general ledger is the complete, unabridged storybook of every single financial transaction your company makes.

The trial balance, on the other hand, is more like the table of contents or a chapter summary. It’s a snapshot report that lists all your account balances at a specific moment to make sure the books are balanced—that your total debits equal your total credits. The ledger is the diary; the trial balance is the quick check to see if the diary makes sense.

What Are the General Ledger and Trial Balance

The general ledger (GL) is the heart of your accounting system. It's the central hub where all your company's financial data lives, acting as the backbone for all your financial reporting. Every transaction gets recorded here in detail, following the rules of double-entry bookkeeping, where every entry has an equal and opposite entry in at least one other account. If you need a refresher on the mechanics, our detailed guide on double-entry bookkeeping explained can help clarify how transactions are recorded.

The GL gives you a complete historical record of every transaction, neatly organized by account—Cash, Accounts Receivable, Sales Revenue, you name it.

In contrast, the trial balance (TB) isn't a book where you record daily entries. It’s an internal report that your bookkeeper pulls together periodically, usually at the end of a month or quarter. It simply lists every account from the general ledger and its final debit or credit balance. Its main job is to do a quick mathematical check to confirm that total debits equal total credits before you move on to building formal financial statements like the income statement or balance sheet.

The core distinction is simple: The General Ledger is the source of truth containing every single transaction detail, while the Trial Balance is a verification tool that summarizes those details to check for mathematical balance.

Understanding this flow is crucial to the whole accounting cycle. Data from day-to-day transactions flows into the general ledger. Then, the summary balances from the ledger are used to create the trial balance.

Key Differences at a Glance

To really see how they fit into the bigger picture, it helps to break down their distinct jobs. This table cuts right to the chase, comparing their purpose, what they contain, and when you use them.

| Attribute | General Ledger | Trial Balance |

|---|---|---|

| Primary Purpose | To record all financial transactions in detail. | To verify the mathematical accuracy of the GL. |

| Content | Includes individual transaction details, dates, and descriptions. | Contains only the final balance for each GL account. |

| Timing | Updated continuously as transactions occur. | Prepared at the end of an accounting period. |

| Function | Serves as the main book of accounts. | Acts as an internal diagnostic and summary report. |

Exploring the General Ledger's Structure and Purpose

The general ledger (GL) is the central nervous system of your company's finances. Think of it as the ultimate book of record where every single transaction finds its permanent home. From a major equipment purchase to a small coffee run for the office, each event is sorted and filed into a specific account.

This detailed library is organized by your Chart of Accounts, which acts as the index for your entire accounting system. Every transaction is classified into one of five main account types, which together give you a complete financial picture of your business. Understanding these categories is key to grasping the GL’s foundational role.

The Five Pillars of the General Ledger

Every transaction in the GL is funneled into a specific account type. This organization is what makes the data so powerful and easy to analyze. The primary account types include:

- Assets: Everything the company owns that has economic value, like cash in the bank, machinery, and money owed to you (accounts receivable).

- Liabilities: Everything the company owes to others. This includes bank loans, vendor bills (accounts payable), and salaries you owe employees.

- Equity: The company's net worth. It’s what’s left for the owners after you subtract liabilities from assets (think Capital Stock and Retained Earnings).

- Revenue: All the income your business generates from its core operations, like sales or service fees.

- Expenses: The costs you incur to run the business and generate that revenue, such as rent, salaries, and marketing.

A clean, logical GL is impossible without a well-thought-out Chart of Accounts. To really dig into this, you should learn more about why your Chart of Accounts matters and how it directly impacts your financial reporting.

Tracing a Transaction into the General Ledger

Let's walk through a simple, everyday scenario for a small consulting firm to see this in action.

Imagine your firm finishes a project and sends an invoice to a client for $2,000. Your bookkeeper records this with a journal entry. This one business activity affects two different accounts in the general ledger:

- Accounts Receivable (an Asset account): This account is debited by $2,000. A debit here increases the balance, showing that the amount of money owed to your company has gone up.

- Service Revenue (a Revenue account): This account is credited by $2,000. A credit increases a revenue account, officially recognizing the income you've earned.

A few weeks later, the client pays the invoice. This triggers a second journal entry.

- Cash (an Asset account): Your cash account is debited by $2,000, increasing the cash on hand.

- Accounts Receivable (an Asset account): This account is credited by $2,000, which reduces the balance and shows the client no longer owes you that money.

The general ledger doesn't just give you the final numbers; it provides a detailed, chronological trail of every single debit and credit that got you there. This granularity is what makes it the go-to source for any deep financial analysis or audit.

Every single entry, no matter how small, gets posted to its correct account in the GL. This creates a continuous, detailed history of all financial activity, which is exactly the data the trial balance needs to do its job.

The Trial Balance: Your First Mathematical Checkpoint

Once every transaction is neatly logged in the general ledger, it's time for a critical reality check. This is where the trial balance comes in. Think of it as the first major checkpoint in your accounting cycle, a quick test to confirm the mathematical integrity of your books.

Its job is elegantly simple: to prove that the total of all debit balances from the general ledger equals the total of all credit balances. This is a direct test of the double-entry accounting principle we live by. Since every journal entry has an equal debit and credit, the final sum of all accounts should net to zero. The trial balance is the report that verifies this, giving you a high-level summary before you dive into building formal financial statements.

Preparing one is pretty straightforward. You just pull the final balance from every single account in the general ledger and list them out in two columns—one for debits and one for credits. For a closer look at getting the structure right, you can check out our guide on the proper trial balance format.

From General Ledger to Trial Balance

Let's jump back to our small consulting firm example. At the end of the month, the bookkeeper takes the ending balances from each general ledger account to create what's called an unadjusted trial balance.

Here’s what a simplified version looks like:

| Account | Debit Balance | Credit Balance |

|---|---|---|

| Cash | $15,000 | |

| Accounts Receivable | $5,000 | |

| Office Supplies | $2,000 | |

| Accounts Payable | $3,000 | |

| Service Revenue | $19,000 | |

| Total | $22,000 | $22,000 |

See how the total debits ($22,000) perfectly match the total credits ($22,000)? This means the books are "in balance." Getting this mathematical confirmation is a crucial quality check. In fact, companies that catch imbalances at this stage can cut down on financial statement errors by 20-25%. It stops bigger problems from developing downstream. For more on this, Patriot Software has a good breakdown of the relationship between the general ledger and trial balance.

Why a "Balanced" Report Isn't Always a "Correct" Report

Here’s the catch: just because a trial balance is perfectly balanced doesn't mean your financial records are 100% error-free. It’s a powerful tool, but it has its limits. Its focus is purely mathematical; it can’t spot conceptual errors or things you simply forgot to record.

A balanced trial balance confirms that your debits equal your credits. It does not confirm that those debits and credits went into the correct accounts, or that every single transaction was recorded in the first place.

This is a critical distinction to remember. The trial balance is just a summary, not a deep-dive audit. For instance, it will completely miss several common—and serious—accounting mistakes:

- Omitted Transactions: If a sale was never recorded in the general ledger, it won't be on the trial balance. The report will still balance perfectly without it.

- Incorrect Classification: Let’s say you debited "Office Supplies" for $500 when it should have been "Marketing Expenses." The total debits and credits are still equal, so the trial balance looks fine.

- Duplicate Entries: Accidentally recording the same invoice twice will also result in a balanced report, even though you’ve just overstated your revenue and accounts receivable.

At the end of the day, the trial balance is an essential first check—but it’s not foolproof. It validates the basic arithmetic of your bookkeeping before you move on to the more nuanced work of making adjusting entries and creating your final financial statements.

Comparing the General Ledger and Trial Balance Side by Side

While the general ledger and trial balance are deeply connected, they play fundamentally different roles in your accounting workflow. Think of it like this: the general ledger is the complete, detailed library of your company's financial story, while the trial balance is the one-page summary that proves the math adds up. The first holds every single detail; the second just confirms the totals.

This division of labor isn't new. The core accounting process has separated transaction recording from error-checking for centuries, a practice that dates back to the 1400s. If you want a fascinating look at the history, check out these insights on the origins of double-entry bookkeeping to see how relevant these foundational principles still are today.

Let's break down their differences across four key areas.

Purpose: Record-Keeping vs. Verification

The general ledger’s job is all about record-keeping. It is the single source of truth, the master file that meticulously documents every financial transaction a business makes. Consider it the official, unabridged financial history of your company.

On the other hand, the trial balance is purely for verification. It’s an internal check, a diagnostic tool used to confirm that the total debits in your general ledger equal the total credits. Its sole mission is to prove mathematical accuracy before you move on to creating your official financial statements.

Content: Detailed Transactions vs. Account Summaries

When you look at what's inside each one, the difference is all about the level of detail. The general ledger contains exhaustive information for every single transaction—dates, descriptions, amounts, and the specific accounts involved. If you need to track down a specific payment or investigate a sale, the GL is where you go.

The trial balance, however, simply lists the final balance of each account from the general ledger. It doesn’t show you the individual transactions that got you to that number. It gives you a high-level snapshot, answering the question, "What is the final balance of our Cash account?"—not "Which checks and deposits make up that balance?"

The GL is for digging into the "why" and "how" behind the numbers. The TB is for confirming the "what"—the final balance itself.

Timing: Continuous vs. Periodic

How often you use them also sets them apart. The general ledger is a living, continuous record. It’s updated constantly, in real-time, as you record daily business activities like sales, purchases, and payments.

In contrast, preparing a trial balance is a periodic event. You typically generate one at the end of an accounting period, whether that's a month, quarter, or year. It's a snapshot taken at a specific moment to kick off the month-end closing process.

Function: Data Source vs. Diagnostic Tool

Ultimately, they serve very different functions. The general ledger acts as the foundational data source for every accounting report you create, including the trial balance itself and, of course, the official financial statements (like the income statement and balance sheet).

The trial balance serves as a crucial diagnostic tool. It's the first step you take when closing the books, designed specifically to catch mathematical errors early on. A balanced trial balance gives you the green light to proceed with making adjusting entries and, eventually, producing your final, polished financial reports.

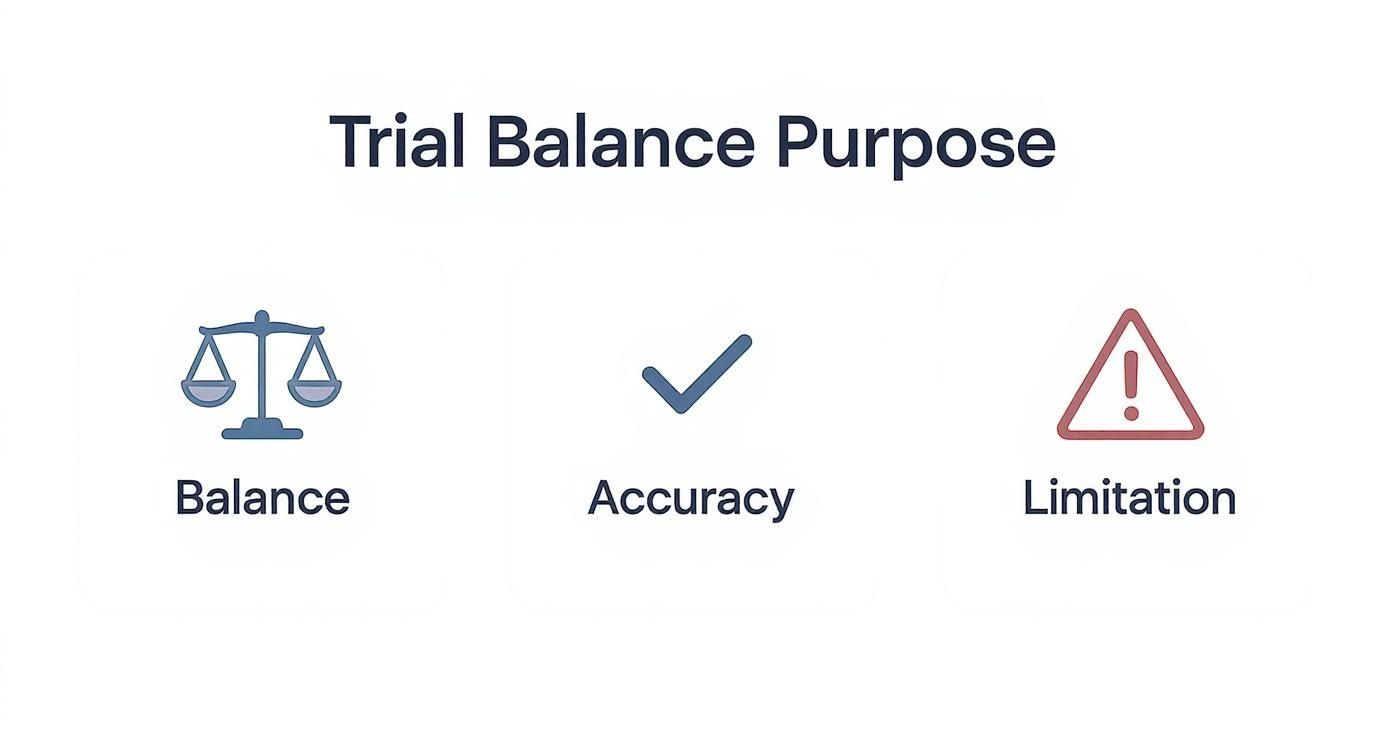

The infographic below neatly summarizes what the trial balance is all about: verifying the balance, checking for accuracy, and understanding its limitations.

This visual helps reinforce that while the trial balance is an essential mathematical check, it can't catch every type of error, like a transaction that was never recorded in the first place.

How They Work Together in the Month End Close

Think of the general ledger and the trial balance not as rivals, but as partners in the critical sequence of a month-end close. This process is what turns the raw, day-to-day transaction data from your GL into verified, accurate numbers ready for your financial statements. Their relationship is completely sequential—each step builds on the last to guarantee the integrity of your final reports.

The entire process always starts with the general ledger. All month long, every sale, purchase, and payment gets recorded in the GL as it happens. This makes the GL the living, constantly updated source of truth for all your company's financial activity.

Stage One From GL to Unadjusted Trial Balance

When the accounting period ends, the very first step is to pull an unadjusted trial balance. This report is created by taking the final debit or credit balance from every single account in the general ledger and listing them out. Its one and only job is to perform a quick mathematical check.

This first pass is essential for catching simple data entry mistakes, like a transposed number or a journal entry that was only posted on one side. If the debit and credit columns don't match, that’s an immediate red flag that something is wrong in the general ledger, and it has to be fixed before you can move on.

Stage Two Adjusting Entries and the Updated GL

Once the unadjusted trial balance confirms that debits equal credits, it’s time to make adjusting entries. These aren’t your typical daily transactions; they’re entries made to account for financial events that occurred over the period but weren’t captured in real-time. This includes things like:

- Accrued Expenses: Recording wages your employees earned but haven't been paid for yet.

- Accrued Revenue: Recognizing income you've earned from a project but haven't billed the client for.

- Depreciation: Allocating a portion of a large asset's cost to the current period.

- Prepaid Expenses: Accounting for the portion of a prepaid expense, like an annual insurance policy, that was "used up" during the month.

Here’s the key part: these adjusting entries are posted directly back into the general ledger. This action updates the balances of the affected accounts, making the GL a more accurate reflection of financial reality. The GL remains the central record, absorbing these adjustments.

This interplay is the heart of the month-end process. The trial balance is the diagnostic tool that checks for balance, but the general ledger is where the actual corrections and adjustments are made. This ensures your source data is always correct.

Stage Three The Final Check with an Adjusted Trial Balance

After all the adjusting entries have been posted in the GL, an adjusted trial balance is prepared. This is your final verification step. It's generated the exact same way as the unadjusted version, but this time it uses the newly updated account balances from the general ledger.

If the debits and credits on this adjusted report are equal, you have confirmation that all your adjustments were posted correctly and the books are mathematically sound. This final, balanced report provides the official numbers used to create your income statement, balance sheet, and statement of cash flows. The sequence is complete, with the GL and TB working together to ensure accurate financial reporting.

Using Accounting Tools for Accurate Reporting

Modern accounting software like QuickBooks has made life a lot easier, automating the creation of both the general ledger and the trial balance. These tools can generate reports in a few clicks that once took hours of painstaking manual work. But just because the process is automated doesn't mean it's foolproof.

Technology can't fix a broken setup. If your chart of accounts is poorly designed or transactions are consistently miscategorized, your trial balance will be misleading. The software will do its job and balance the wrong numbers, giving you a false sense of security while you make critical business decisions based on bad information.

The Value of Expert Oversight

This is where having a professional guide you becomes so important. An expert makes sure your system is set up correctly from the beginning, which helps prevent those foundational errors from ever taking root.

Automation without accuracy is just a faster way to get the wrong answer. Expert oversight transforms accounting software from a simple calculator into a strategic asset for growth.

Services like ours at Steingard Financial focus on keeping your general ledger accurate through regular clean-up and reconciliation. We help you actually understand the financial data your tools produce, turning those automated reports into clear, actionable insights. By making sure the data flowing from your general ledger to your trial balance is solid, we help you make confident decisions that move your business forward.

Your Questions, Answered

Still have a few questions about how the general ledger and trial balance fit together? You're not alone. Here are some clear, straightforward answers to the most common queries we hear from business owners.

Can a Trial Balance Be Correct If the General Ledger Is Wrong?

Yes, and this is a critical point that trips many people up. A trial balance can look perfectly fine—with debits equaling credits—even when the general ledger is riddled with errors. For example, if a $500 payment was accidentally debited to Office Supplies instead of Marketing Expenses, the totals would still match.

The trial balance only confirms that the math adds up. It can't tell you if transactions were misclassified, duplicated, or missed entirely.

How Often Should You Prepare a Trial Balance?

For most businesses, running a trial balance is a standard part of the monthly closing process. Think of it as a regular checkpoint to make sure your books are mathematically sound before you start generating your financial statements.

In high-transaction environments or during an audit, you might run one more often, maybe even weekly, to catch discrepancies sooner. The real key is to build it into your regular accounting cycle and be consistent.

Do I Still Need the General Ledger If My Software Creates Reports?

Absolutely. While modern accounting software is fantastic at automating reports, the general ledger remains the foundational record of your business. It's the ultimate source of truth.

If you ever need to investigate a specific transaction, figure out a discrepancy, or get through an audit, you'll be digging into the detailed history in the GL. Your software reports are just summaries; the GL has all the proof.

Ensuring your general ledger is accurate and your trial balance is clean is the first step toward confident financial decision-making. At Steingard Financial, we specialize in cleaning up historical books and implementing reliable bookkeeping processes. Contact us today to see how we can bring clarity to your financials.