Difference between cash basis and accrual basis: Explained

When you get down to it, the difference between cash basis and accrual basis accounting is all about timing. Cash basis accounting is simple: you record revenue and expenses only when money actually changes hands. Accrual basis, on the other hand, records revenue when you earn it and expenses when you incur them, whether or not the cash has moved.

Think of it this way: one method tracks your bank balance, while the other tracks your overall financial commitments and promises.

Defining the Two Methods of Accounting

Choosing between cash and accrual accounting really determines the kind of story your financial statements tell. One gives you a live look at your cash flow, while the other provides a much deeper view of your profitability over a specific period. Getting this difference right is the first step in building a financial reporting system that’s actually useful for your service business.

Cash Basis Explained

The cash basis method is definitely the more straightforward of the two. It works just like your checkbook register. Income gets recorded when a client’s payment hits your bank account, and expenses are recorded when you actually pay the bill.

If you finish a big project in December but don’t get paid for it until January, that revenue belongs to January. This approach gives you an immediate, clear picture of how much cash your business has right now, which is why it’s so popular with small businesses, freelancers, and sole proprietors who just want simplicity and a clear view of their bank balance.

Accrual Basis Explained

Accrual basis accounting paints a much more accurate picture of your company’s actual financial health and performance over time. Using this method, you record revenue as soon as you’ve earned it—meaning, when you’ve delivered a service—even if the client hasn’t paid you yet. Expenses work the same way; they’re recorded when you incur them, not necessarily when you pay for them. For instance, if you get a software bill in June but don’t pay it until July, that expense is still a June expense.

This is where you start seeing important accounts like Accounts Receivable (money that’s owed to you) and Accounts Payable (money you owe to others). It’s a bit more complex, but it follows the matching principle, which pairs revenues with the expenses that helped generate them. This gives you a much truer sense of your profitability.

The accrual method is required by Generally Accepted Accounting Principles (GAAP) because it provides a more consistent and comparable view of a company’s performance, which is critical for investors, lenders, and internal strategic planning.

To make these ideas even clearer, here’s a quick side-by-side look.

Quick Comparison Cash Basis vs Accrual Basis Accounting

This table breaks down the core differences at a glance, helping you see how each method impacts your financial reporting.

| Attribute | Cash Basis Accounting | Accrual Basis Accounting |

|---|---|---|

| Revenue Recognition | Recorded when cash is received from customers. | Recorded when revenue is earned, regardless of payment. |

| Expense Recognition | Recorded when cash is paid for an expense. | Recorded when an expense is incurred, regardless of payment. |

| Complexity | Simple and easy to maintain; mirrors cash flow. | More complex; requires tracking receivables and payables. |

| Financial Picture | Shows current cash position accurately. | Shows long-term profitability and financial health. |

| Best Suited For | Small businesses, freelancers, and companies with no inventory. | Growing businesses, companies with inventory, and those seeking loans. |

Ultimately, the best method depends entirely on your business’s size, complexity, and goals for the future.

How Each Method Impacts Your Financial Statements

Your choice between cash and accrual accounting fundamentally changes the story your financial statements tell. It’s not just a technicality about timing; the method you pick directly shapes how your profitability, assets, and liabilities are presented on paper. Getting this right is critical for interpreting your financial health correctly and making smart business decisions.

The difference between cash and accrual reporting echoes across both your income statement and your balance sheet. While a statement of cash flows is always important, it becomes especially crucial under the accrual method to bridge the gap between reported profit and the actual cash sitting in your bank account.

Income Statement Differences

Your income statement, often called the Profit & Loss (P&L), shows how your company performed financially over a specific period. This is where the two accounting methods can paint dramatically different pictures.

Under the cash basis, the P&L is a straightforward record of cash movement. Revenue only shows up when a customer’s check clears, and expenses are only recorded when you actually pay a bill. This often leads to a lumpy, sometimes confusing, view of your profitability.

On the other hand, the accrual basis offers a much smoother and more accurate picture by following the matching principle. Revenue is recognized when you earn it (like when you finish a client project), and expenses are matched to the period they helped generate that revenue. This approach prevents a single large payment from making one month look incredibly profitable while the next looks like a loss, giving you a truer sense of your operational health.

Key Insight: Accrual accounting smooths out revenue and expense recognition, offering a more reliable measure of a company’s performance. A cash-basis income statement might show high profit one month and a loss the next, simply due to payment timing, not a change in business activity.

Balance Sheet Transformation

The balance sheet is a snapshot of your company’s financial position at a single moment in time—what it owns (assets) and what it owes (liabilities). The accrual method introduces a couple of critical accounts that simply don’t exist under the cash method.

With accrual accounting, two key accounts come into play:

- Accounts Receivable (AR): This is an asset. It represents money your clients owe you for services you’ve already delivered but haven’t been paid for yet.

- Accounts Payable (AP): This is a liability. It represents money you owe to your vendors or suppliers for goods or services you’ve received but haven’t paid for yet.

A cash-basis balance sheet is much simpler, mostly just showing your cash balance, physical assets, and any loans. It gives you zero visibility into future cash coming in from completed work or upcoming bills you need to pay. The accrual basis, by including AR and AP, provides a far more complete picture of your company’s total assets and financial obligations.

Impact on Financial Statements by Accounting Method

This table provides a clear, at-a-glance comparison of how each accounting method alters your key financial reports.

| Financial Statement | Impact of Cash Basis | Impact of Accrual Basis |

|---|---|---|

| Income Statement | Profitability is tied to cash flow. Can show volatile swings based on payment timing, not business performance. | Profitability is tied to business activity (matching principle). Provides a smoother, more accurate view of operational performance. |

| Balance Sheet | Simpler. Lacks Accounts Receivable and Accounts Payable, providing an incomplete view of assets and liabilities. | More comprehensive. Includes AR (what you’re owed) and AP (what you owe), giving a true picture of financial position. |

As you can see, the accrual basis builds a much more detailed and accurate financial picture, which is essential for any business looking to grow or secure funding.

A Practical Service Business Example

Let’s look at a simple scenario for a consulting firm in March to see how this plays out in the real world.

Scenario:

- On March 15th, you complete a project and send a $5,000 invoice to your client.

- On March 20th, you receive a $1,500 bill from a subcontractor for work on that project, due in April.

- The client pays your $5,000 invoice on April 5th.

- You pay the $1,500 subcontractor bill on April 10th.

Here’s how March’s net income would look under each method:

| Accounting Method | March Revenue | March Expenses | March Net Income |

|---|---|---|---|

| Cash Basis | $0 | $0 | $0 |

| Accrual Basis | $5,000 | $1,500 | $3,500 |

Using the cash method, your March books show zero activity because no money actually changed hands. But with the accrual method, you see a $3,500 profit because you earned the revenue and incurred the expense within that month. This is a far more accurate reflection of your performance in March.

These transactions create the initial entries that are summarized in your books. For a deeper dive, you can learn more about the proper trial balance format to see how these debits and credits are structured. This foundational report ensures your books are balanced before creating the main financial statements. The accrual method clearly shows the true financial outcome of your work during the period it occurred.

Navigating Tax Rules and Regulatory Compliance

Choosing between cash and accrual accounting isn’t just a matter of preference; it’s a decision that has to align with tax laws and regulatory standards. Your choice has big implications for how you report income to the IRS and how your company’s financial health looks to lenders, investors, and other official bodies. Getting this right is fundamental to staying compliant and making smart financial moves.

The two main players setting the rules are the Internal Revenue Service (IRS) and the Financial Accounting Standards Board (FASB), which oversees the Generally Accepted Accounting Principles (GAAP). Each has its own set of standards, and these often determine which accounting method a business must use, especially as it gets bigger and more complex.

IRS Rules and the Gross Receipts Test

When it comes to your taxes, the IRS offers some flexibility, but only up to a point. It allows small businesses with average annual gross receipts below a certain threshold to use cash basis accounting, which definitely simplifies the bookkeeping process for smaller companies.

However, once a business grows beyond that threshold or deals with inventory, the IRS generally requires a switch to accrual accounting for federal income tax reporting. You can find more detailed guidance on how the IRS views the cash vs. accrual accounting difference on GBQ.com. This is a critical point because it’s often the first time a growing business is forced to change its accounting method.

The cash basis method can also open up some unique tax planning strategies. Because income is only counted when cash actually hits your bank account, you can sometimes defer income into the next fiscal year by waiting to send invoices. On the flip side, you can accelerate expenses by paying bills before the year ends, which can help lower your taxable income for the current period.

Important Note: While these tax planning tactics are perfectly legal, you need to handle them with care. The idea is to legitimately time your cash flow, not to misrepresent your financial position. It’s always a good idea to chat with a tax professional to make sure you’re staying on the right side of the rules.

GAAP Requirements and Investor Expectations

Even if the IRS gives you the green light for cash accounting, the world of investors and lenders plays by a different set of rules. Generally Accepted Accounting Principles (GAAP) are the gold standard for financial reporting in the U.S., ensuring that financial statements are clear and consistent across the board.

GAAP requires most companies to use the accrual method. This isn’t an arbitrary rule; it’s based on the need for a transparent and accurate picture of a company’s performance. Accrual accounting provides this by matching revenues with the expenses that were incurred to earn them—a core concept known as the matching principle.

This creates a much more reliable view of profitability, which is essential for:

- Investors who want to gauge a company’s long-term earning power.

- Lenders who need to see if a business can repay debt based on its operational results, not just the cash it has on hand.

- Public companies that are required to provide consistent financial statements to the public.

If you’re running on a cash basis, you’ll find it nearly impossible to attract serious investment or secure a large loan. Your financial statements simply won’t meet the standards that these external stakeholders expect to see.

When a Transition Becomes Necessary

The journey from a small startup to a growing company often involves a mandatory switch from cash to accrual accounting. This change is usually triggered by a few key events.

The most common reasons for making the switch include:

- Exceeding the IRS Gross Receipts Threshold: Once your average annual revenue goes over the IRS limit (currently $29 million for 2023), switching becomes a tax compliance issue you can’t ignore.

- Seeking External Funding: If you’re pitching to venture capitalists or applying for a big bank loan, they’ll want to see GAAP-compliant financial statements. That means you’ll need to be on the accrual method.

- Managing Inventory: Any business that holds a significant amount of inventory is generally required by the IRS to use an accrual method to properly account for purchases and sales.

- Preparing for an Audit or Sale: When you’re getting ready for an audit or looking to sell your business, you’ll need the kind of financial accuracy that only accrual accounting can offer.

Making this transition is a major step. It requires careful planning to adjust your books for things like accounts receivable and accounts payable. It’s a sign that your company is maturing and moving toward more robust and credible financial management.

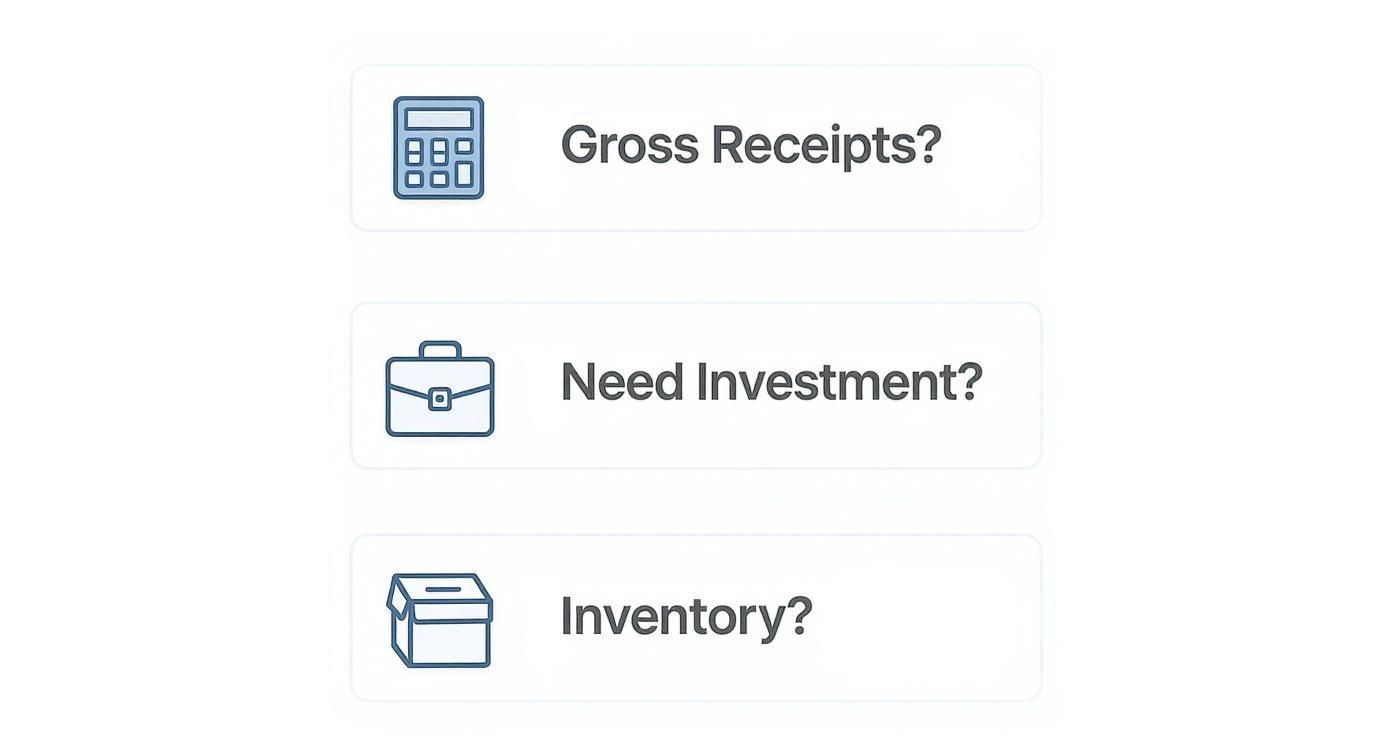

Choosing the Right Method for Your Business Stage

Picking between cash and accrual accounting isn’t just a technical detail for your bookkeeper. It’s a strategic decision that needs to line up with your company’s size, complexity, and where you’re headed. The right method gives you the clarity to make smart financial moves, but the wrong one can easily hide what’s really going on with your performance.

It really comes down to matching the method to where your business is right now. For most owners, the choice hinges on a few key operational facts. This infographic lays out a simple decision tree to help you see which path makes sense based on your gross receipts, funding plans, and whether you’re dealing with inventory.

As you can see, the bigger and more complex your business gets, the more you’ll be pushed toward accrual accounting. It’s a natural part of scaling up.

When Cash Basis Is the Ideal Choice

For many small service-based businesses, cash basis accounting is the perfect place to start. It’s simple and gives you an immediate, clear picture of your cash flow—which, as we all know, is the lifeblood of any new company.

This method works best for:

- Freelancers and Solopreneurs: If you’re an independent professional, just tracking money in and money out is often all you need for solid financial management and easy tax prep.

- Startups in Early Stages: New businesses with simple operations and no immediate plans to chase outside funding can thrive on the simplicity of cash basis bookkeeping.

- Service Businesses with No Inventory: Think consultants, designers, and other service providers. If you don’t buy and sell physical products, you can manage your finances just fine without the extra layers of accrual accounting.

The biggest win here is that your books are a direct reflection of your bank account. You can see your cash position at a glance. Mastering these foundational steps is a key part of good financial management, and you can learn more in our guide on bookkeeping basics for small business. This approach keeps things simple when that’s exactly what you need.

When Accrual Accounting Becomes Non-Negotiable

As a business grows, its financial reporting needs change. Simplicity starts to take a backseat to the need for a more precise and detailed view of performance. Accrual accounting becomes absolutely essential once your operations hit a certain scale or you start talking to outside stakeholders.

This is the point where you have to look beyond just the cash in the bank. You need a true picture of your profitability.

A switch to accrual is often triggered when your business:

- Starts Managing Inventory: The IRS actually requires businesses that hold inventory to use accrual accounting. This is to properly match the cost of your goods with the revenue they generate.

- Seeks Investment or Loans: Banks, investors, and venture capitalists won’t really take you seriously without financial statements that are GAAP-compliant. That means using the accrual method, period.

- Needs to Track Profitability Accurately: If you truly want to understand your profit margin on a specific project or for a particular month, you have to match revenues with the exact expenses that created them. Only accrual accounting can do that.

- Is Preparing for a Sale or Acquisition: Potential buyers are going to demand a clear and accurate financial history. Accrual basis gives them this by smoothing out income and expenses, offering a reliable look at long-term health instead of just short-term cash swings.

Ultimately, making the move from cash to accrual is a sign that your business is maturing. It signals that you’re ready for more sophisticated financial management and are positioning the company for its next phase of growth and opportunity.

Making the Switch from Cash to Accrual Accounting

At some point, the simplicity of cash accounting just doesn’t cut it anymore. As your business grows, sticking with a cash-based view can actually hide what’s really going on with your financial health. Moving to the accrual method is a big step, a sign that you’re ready for serious growth, potential investment, and much deeper financial insights.

This isn’t about just flipping a switch in your software. It’s a fundamental change in how you think about, record, and interpret your company’s financial story.

To make this change work, you need a clear, structured plan. The goal is to get a perfect snapshot of your financial position at a specific moment in time so your new accrual-based books start off on the right foot.

Key Steps for a Smooth Transition

The whole point of the switch is to account for all the financial activity that has already happened but hasn’t been settled with cash yet. This process creates the starting point for a much more detailed and accurate balance sheet.

Here’s a straightforward guide to get it done:

- Choose a Transition Date: Pick a definitive cutoff, usually the first day of a new fiscal year or quarter (like January 1st). Everything before that date stays on the cash basis; everything after is recorded using the accrual method.

- Calculate Accounts Receivable (AR): Pull together a complete list of every single outstanding invoice. These are for services you’ve already delivered but haven’t been paid for as of your transition date. The grand total is your opening AR balance.

- Calculate Accounts Payable (AP): Do the same thing for your own bills. List out every unpaid invoice from vendors for goods or services you’ve already received. That total becomes your opening AP balance.

- Identify Accrued Expenses and Prepaid Items: Don’t forget the other stuff. This includes expenses you’ve incurred but haven’t been billed for yet (like employee wages earned but not yet paid out) and things you’ve paid for in advance (like your annual insurance premium).

- Make Adjusting Journal Entries: Once you have these numbers, you’ll make a few one-time adjusting entries in your accounting system. These entries officially set up your opening balances for AR, AP, and other new accrual accounts. If you’re new to this, our guide explaining double-entry bookkeeping offers some great background.

Following these steps ensures your financial statements give you a true picture of your company’s performance and position.

Using Software like QuickBooks and Gusto

Modern accounting tools are a huge help here. A platform like QuickBooks Online can generate both cash and accrual reports, but it’s up to you to feed it the right data in the first place.

- In QuickBooks: You can change your default report setting under

Account and Settings > Advanced > Accounting method. But to really operate on an accrual basis, your team has to get in the habit of creating invoices for AR and entering bills for AP as soon as they happen. - With Gusto: When you connect Gusto to QuickBooks, it automatically syncs payroll liabilities and expenses. This is a lifesaver for properly recording accrued payroll and matching your labor costs to the right period.

Crucial Tip: Just changing a setting isn’t enough. This is a process change. Your team needs to be trained to enter invoices and bills on the day they are created, not when the money finally moves.

Common Pitfalls to Avoid

Moving from cash to accrual can be tricky, and a few common mistakes can really mess up your financial data. Just knowing what they are is half the battle.

One of the biggest tripwires is getting the starting AR and AP balances wrong. If you miss an invoice or forget about a big vendor bill, it will throw off your opening balance sheet and skew your financial reports for months.

Another all-too-common issue is a lack of team training. If your staff keeps thinking in cash terms—waiting to enter a bill until it’s due—your whole accrual system falls apart. The difference between cash basis and accrual basis is procedural, not just a technicality. Without help from a firm like Steingard Financial, these small slip-ups can snowball into major reporting errors and compliance headaches.

Answering Your Lingering Questions

Even after getting the basics down, you probably have a few specific questions popping into your head. That’s normal. Applying these accounting methods to the real world is where the nuances really show up. Let’s tackle some of the most common questions business owners ask when deciding between cash and accrual.

Getting these details sorted is the last step to feeling truly confident in how you manage your financial reporting.

Can I Use a Mix of Both Methods?

Yes, in some cases you can. This is called the hybrid accounting method, and it blends pieces of both the cash and accrual systems. The IRS does allow this, but only under specific rules. It’s most often seen in small businesses that handle inventory but want to keep the rest of their bookkeeping as simple as possible.

With a hybrid model, you would typically use the accrual method just for your inventory. This means you record the cost of goods sold when you earn the revenue from a sale, which lines up with the matching principle and gives a much truer picture of your product profitability. For everything else—like services income or regular operating expenses—you’d stick with the straightforward cash basis. It offers a middle ground, but it’s not a free-for-all.

Important Clarification: The IRS is very strict about who can use the hybrid method and exactly how it needs to be applied. It’s absolutely critical to talk to a tax professional to make sure you’re compliant and setting your books up correctly from day one.

How Does This Choice Affect My Business’s Valuation?

Your accounting method has a huge say in what investors, lenders, and potential buyers think your company is worth. When it comes to a formal valuation, financial analysts and appraisers are almost always going to insist on accrual basis accounting. Why? Because it aligns with Generally Accepted Accounting Principles (GAAP) and shows a far more stable and accurate picture of your company’s financial health.

Accrual accounting smooths everything out, matching revenues and expenses to the periods they were actually earned or incurred. This makes it much easier to spot reliable performance trends. A business on a cash basis might show wild profit swings that are just tied to when clients pay their bills, not the actual work being done. For an investor, that can be a major red flag.

Bottom line: If you want to get the highest and most credible valuation for your business, you need to switch to accrual accounting. Making that transition well before a sale or funding round isn’t just a good idea—it’s practically a requirement for any serious deal.

Can I Run Both Cash and Accrual Reports?

Absolutely, and it’s a very common practice for smart internal management. Modern accounting software like QuickBooks Online makes it incredibly easy to switch between cash and accrual views with just a click. This gives you the best of both worlds.

- Cash Basis Reports: These are your go-to for daily cash flow management. They show you exactly how much cash you have in the bank right now to pay bills, make payroll, and cover other immediate needs.

- Accrual Basis Reports: These are for strategic planning. They give you the real story of your profitability, help you analyze performance over time, and are what you’ll need for banks, investors, or to be GAAP compliant.

Many savvy business owners live in their cash reports for day-to-day decisions but use their accrual reports for monthly and quarterly financial reviews. This lets them keep a tight grip on their bank balance while also understanding the deeper performance trends of the business.

What’s the Hardest Part About Switching Methods?

The single biggest challenge in switching from cash to accrual is the incredibly detailed work needed just to get started. It’s not as simple as flipping a switch in your software. The move requires a fundamental change in how you and your team think about and record transactions.

The main job is to accurately find, calculate, and record every single outstanding financial item on your official transition date. This means every unpaid customer invoice (your accounts receivable), every bill you owe to vendors (your accounts payable), and any other accrued expenses, like wages earned by employees but not yet paid. One mistake here will mess up your opening balance sheet and throw your financial reports off for months.

Beyond just the numbers, getting your team on board is a big hurdle. They have to be retrained to think in terms of “earned” and “incurred,” not just “money in” and “money out.” This shift in process is often where businesses stumble, which is why getting professional guidance during this critical transition is so valuable.

Understanding and choosing the right accounting method is foundational to your business’s success. If you’re working through these complexities, the team at Steingard Financial can provide the expert bookkeeping and advisory support you need to ensure your financial data is accurate, compliant, and ready for growth. Learn how we can build a scalable back office for your service business.