A Guide to Payroll Cards for Employers in 2026

Payroll cards are a modern answer to an old problem: how to pay your team efficiently and securely. You can think of them as reloadable debit cards that you, the employer, load with an employee's wages each payday. It’s a straightforward, digital alternative to printing paper checks or even managing direct deposits.

What Are Payroll Cards and Why They Matter Now

The process is simple. Instead of cutting a check or initiating a bank transfer, you electronically send an employee's net pay right onto their payroll card. From there, they can use it just like any other debit card—swiping it at stores, paying bills online, or getting cash from an ATM.

This approach is a game-changer for certain industries. If you run a business with a mobile workforce, like in construction, logistics, or hospitality, you know the headache of getting checks to people who are never in one place. Payroll cards solve that, ensuring everyone gets paid on time, no matter where their work takes them.

A Modern Solution for a Changing Workforce

Payroll cards are especially helpful for reaching unbanked or underbanked employees. These are team members who don't have a traditional checking or savings account. For them, a paper paycheck is a hassle. It means a special trip to a check-cashing store, which almost always charges steep fees that eat into their take-home pay.

By offering a payroll card, you give them immediate access to their money without the extra cost and frustration. This isn't just a nice perk; it’s a powerful way to show you understand the real-world financial challenges your team faces. In a competitive market, that kind of support can make all the difference in attracting and keeping great people.

The move toward payroll cards is part of a much bigger shift to digital payments in the workplace. This trend has grown incredibly fast. Back in 2017, there were already 5.9 million active cards with $42 billion loaded onto them. Looking ahead, the global market is expected to hit a staggering $1,608.4 billion by 2035. This growth is fueled by a 72% adoption rate among the unbanked and the fact that 68% of employers are working to digitize their payroll.

This shift from paper to plastic brings real advantages to both you and your employees. For your business, it means less administrative work and lower costs. For your team, it means faster, more secure access to their earnings. Getting your payment process right with the right payroll services for small business can make these benefits even stronger.

Payroll Cards At a Glance

To really see how payroll cards work for everyone, it helps to put the benefits side-by-side. They solve different, but related, problems for both the business and its staff, creating a true win-win.

| Aspect | Benefit for Employers | Benefit for Employees |

|---|---|---|

| Payment Process | Eliminates check printing, distribution, and postage costs. | Instant access to wages on payday; no need to wait for checks. |

| Financial Inclusion | Provides a viable payment option for unbanked employees. | Avoids high fees from check-cashing services. |

| Security | Reduces risks of lost or stolen checks and check fraud. | Safer than carrying large amounts of cash after cashing a check. |

| Administration | Simplifies payroll administration and reduces paperwork. | Can be used for online purchases and bill payments like a debit card. |

As you can see, the benefits are clear. Payroll cards simplify operations for you while providing a modern, convenient, and inclusive way for your team to get paid.

The Business Case for Adopting Payroll Cards

Sure, payroll cards are a great option for a modern workforce, but the real reason so many businesses are making the switch comes down to dollars and sense. Moving away from paper checks isn't just a "green" initiative; it's about redirecting your time and money from slow, administrative work to tasks that actually grow your company.

When you adopt payroll cards for employers, you’re making a smart business decision based on real cost savings and a serious boost in efficiency.

The most obvious win is the immediate drop in costs. Just think about everything that goes into a single paper check: buying the check stock, printing it, stuffing it in an envelope, paying for postage, and all the staff hours spent managing the process. That doesn't even include the headache and fees for stop-payments on lost checks and the time it takes to reissue them.

Payroll cards completely sidestep these costs. By loading wages directly onto a card, you cut out the entire paper supply chain. A tedious, multi-step process becomes a single, straightforward digital transaction.

Driving Financial and Operational Efficiency

For most employers, the biggest appeal of payroll cards is how much they save compared to writing old-school paper checks. They get rid of printing, postage, and administrative costs because you just load an employee's salary directly onto their card.

The global market for these cards is expected to hit USD 1,364.19 billion by 2034, and that massive growth is happening for a reason. For businesses in the U.S., especially those using payroll software like QuickBooks Payroll or Gusto, it means simpler bookkeeping, better reporting, and no more chasing down lost checks. You can get a full rundown of the financial details by reading up on the pros and cons of payroll cards.

This efficiency goes beyond just saving money on paper. If you're in an industry with high turnover, like retail or restaurants, payroll cards make offboarding so much easier. There's no final paper check to deal with. You can load the final paycheck onto the employee’s card instantly, keeping you compliant with final pay laws without any logistical stress.

Plus, paying digitally creates a clean, immediate data trail. This gives you a real-time look at your payroll expenses and makes bank reconciliation a breeze—a huge plus for any business owner who needs accurate financial oversight.

Gaining a Competitive Advantage in Hiring

In a tight job market, how you pay your team is a part of your company's brand. Offering modern, flexible payment options like payroll cards can really make you stand out, especially if you're trying to hire a younger or more tech-focused workforce. It shows your company is in tune with what employees actually want.

This becomes even more powerful when you pair payroll cards with other smart tools. A key reason to adopt paycards is to make your whole payroll process smoother, and using something like a digital time clock for employees ensures your payroll calculations are accurate from the start. When these systems work together, you create a seamless experience from the moment an employee clocks in to the moment they get paid.

Think about these strategic wins:

- Better Recruiting: Mentioning "instant digital pay" or "payroll card options" in your job postings can attract more applicants, especially people who don't have a traditional bank account.

- Higher Retention: When you give your team a financial tool that saves them time and money on check-cashing fees, they're more likely to stick around.

- Easier Remote Payroll: For companies with employees spread out everywhere, payroll cards get rid of the headache of mailing checks across the country. Everyone gets paid on time, no matter where they are.

Ultimately, the case for payroll cards is about more than saving a few bucks on postage. It’s about building a smarter, more efficient financial operation that supports your team and strengthens your entire business.

Navigating Payroll Card Compliance and Regulations

Thinking about offering payroll cards? It’s a great idea for many businesses, but you can't just pick a vendor and start handing out plastic. There's a mix of federal and state laws that dictate exactly how you can offer and manage these cards.

Getting the rules wrong can lead to some pretty hefty fines and legal headaches. The good news is that once you understand your main responsibilities, the whole process becomes much more straightforward.

The biggest federal law you need to know is the Electronic Fund Transfer Act (EFTA), specifically a part of it called Regulation E. This is the main set of rules for all electronic payments, and it’s designed to protect consumers—in this case, your employees—by making sure everything is fair and transparent.

Key Federal Requirements Under Regulation E

Getting federal law right is your first and most important step. Regulation E is very clear about what employers must do when offering payroll cards. These aren't just suggestions; they're mandatory rules that protect your employees' right to their wages.

First and foremost, using a payroll card must be completely voluntary. You can never force an employee to accept their wages on a card. You are legally required to offer another choice, like direct deposit or a paper check. The payroll card should always be positioned as an option, never a requirement.

Next, you have to provide clear, easy-to-read disclosures of all associated fees before an employee agrees to the card. This needs to include everything from potential ATM withdrawal fees to monthly service charges. Transparency isn't just a good policy here—it's the law.

Finally, your employees must have a way to access their full wages for free at least once per pay period. This could be through a network of fee-free ATMs, a withdrawal from a bank teller, or another method that costs them nothing.

The main idea is simple: An employee has the right to get every dollar they earned without having to pay a fee to access it. This is a fundamental protection under federal law.

State Laws The Other Half of the Puzzle

While federal law creates the foundation, you also have to pay close attention to the rules in your specific state. Many states have their own laws for payroll cards, and they are often even stricter than the federal requirements.

For example, some states have specific rules about:

- Written Consent: Requiring employers to get an employee's explicit, written permission before issuing them a payroll card.

- ATM Access: Mandating a certain number of fee-free ATMs within a reasonable distance of the employee’s home or workplace.

- Prohibited Fees: Some states completely ban certain fees, like charges for inactivity or for loading funds onto the card.

- Paper Statements: A state might require you to provide free paper statements if an employee requests them, even if federal law doesn't.

Because these laws can differ so much from one state to another, what works in Texas might not be compliant in California or New York. It’s always a good idea to check your state’s labor laws or talk to a payroll compliance expert. Staying on top of these duties is a huge part of overall payroll compliance, protecting both your business and your team.

Beyond wage laws, remember that other financial duties are just as serious. Failing to handle payroll taxes correctly, for instance, can lead to major issues. Understanding potential liabilities like the Trust Fund Recovery Penalty is critical for keeping your business in good financial standing.

A Quick Compliance Checklist

To make sure you're setting up your payroll card program correctly, use this checklist as a guide. It covers the essential steps for staying compliant.

- Confirm Voluntary Choice: Always offer an alternative like direct deposit or a paper check.

- Provide Full Fee Disclosure: Give employees a written list of all potential fees before they sign up.

- Ensure Free Access to Funds: Make sure there is at least one way for employees to get their full pay for free each pay period.

- Research State and Local Laws: Look into any extra requirements for the states where your employees work.

- Choose a Compliant Vendor: Work with a payroll card provider that knows and follows all federal and state regulations.

A Step-by-Step Guide to Implementing Payroll Cards

Moving to a payroll card program might seem like a big undertaking, but if you break it down into a few clear steps, the process is much more manageable. A good plan is key to making the switch without disrupting your business, while also keeping you compliant and getting your team on board.

This guide will walk you through everything you need to know to implement payroll cards, from the initial research to getting your employees set up and paid.

Step 1: Research and Select a Compliant Provider

Your first job is to find the right partner. The payroll card provider you choose will have a big impact on your administrative workload and how your employees feel about the program.

When you're looking at different vendors, here are the critical things to focus on:

- Fee Structures: Look closely at any and all fees—for both you and your employees. You want a provider with clear, low-cost options, like a large network of fee-free ATMs and no monthly maintenance charges.

- Compliance Expertise: Your provider must know federal Regulation E and all state laws inside and out. Ask them directly how their program ensures you stay compliant, especially when it comes to voluntary employee choice and free access to wages.

- Features and Support: Do they have a good mobile app for employees? What happens if a card is lost or stolen? Solid customer support for both you and your team is a must.

Once you have a couple of options, ask for references. Talking to other business owners who use the service can give you real insight into how reliable they are.

Step 2: Integrate with Your Payroll System

After you’ve picked a provider, the next step is to connect their system with your payroll software. Most modern payroll card programs are built to work directly with major platforms like Gusto and QuickBooks Payroll, which simplifies things quite a bit.

The integration process usually looks something like this:

- System Setup: You’ll work with the provider to add the payroll card as a payment option inside your payroll platform.

- Employee Enrollment: Any employee who opts in will be added to the new system, and their card will be linked to their profile in your payroll software.

- Running Payroll: When payday comes, you run payroll just like you always do. For employees using paycards, you'll just select "payroll card" as their payment method instead of "direct deposit."

The system then automatically sends the correct net pay to each employee's card. This removes the manual work of printing checks and makes sure funds are transferred on time.

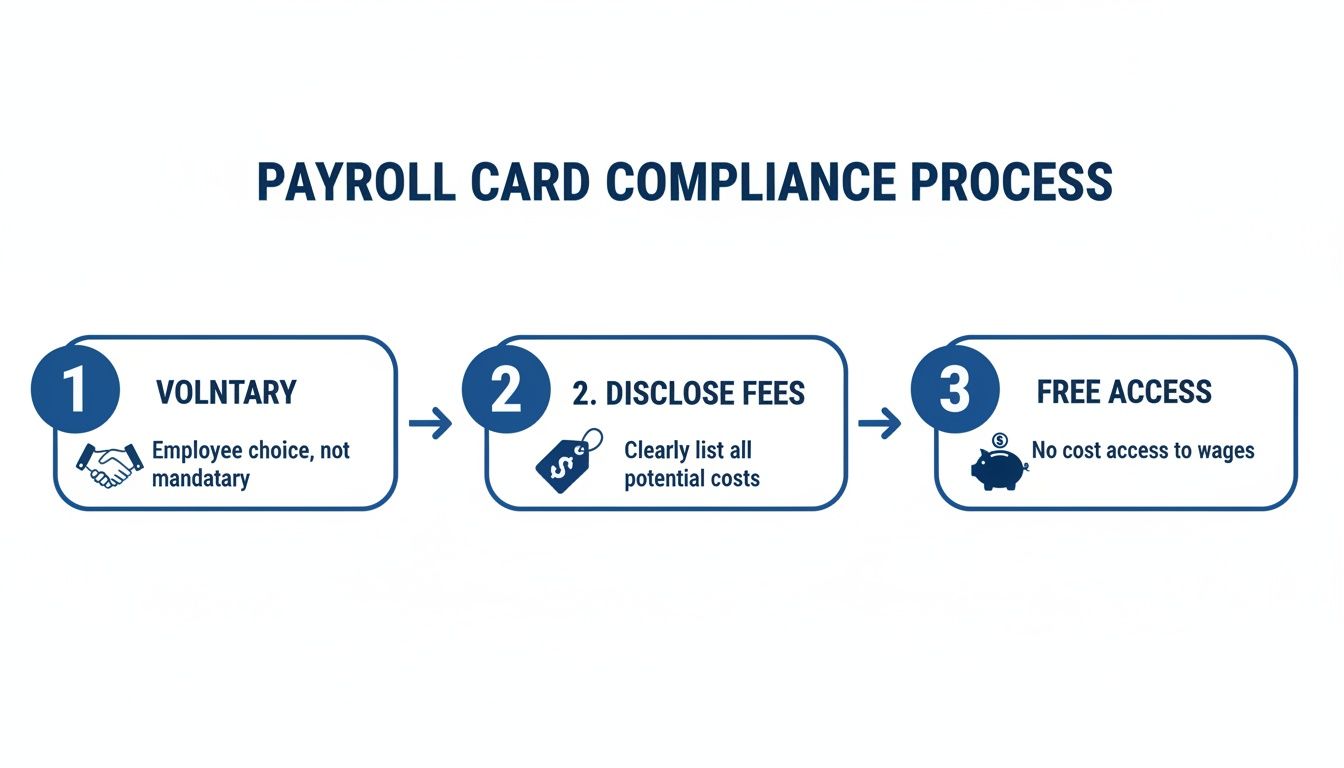

The image below shows the core compliance steps you must follow. Your chosen provider should support this entire process.

This process highlights the three essential parts of a legal payroll card program: making sure participation is voluntary, providing total transparency on fees, and guaranteeing employees can access their full wages for free.

Step 3: Onboard and Support Your Employees

A successful rollout isn't just about the software—it’s about your people. The final step is to explain the new option to your employees, get them signed up, and offer support as they get used to it.

A strong onboarding process is crucial for building trust. Employees need to see the payroll card as a benefit that makes their lives easier, not a confusing new requirement.

Your plan for rolling this out to employees should include:

- Clear Communication: Hold informational meetings and create simple handouts that explain how the cards work, the benefits (like no more check-cashing fees), and the complete fee schedule.

- Simple Opt-In Process: Make it easy for employees to sign up if they're interested. Give them the required disclosure forms and any enrollment paperwork from the provider.

- Training and Resources: Show your team how to activate their cards, check balances, and use the mobile app. Make sure they know who to call—both at your company and at the card provider—if they run into any issues.

Finally, have a clear plan for what to do when common problems pop up, like a lost card or an incorrect transaction. If you're prepared, you can solve these issues quickly and show your team you’re there to help.

How to Communicate the Change to Your Employees

Rolling out a new payment method goes way beyond just a technical update. This kind of change hits close to home for your team—it's about their money and their financial stability. A successful launch of payroll cards for employers really comes down to clear, honest communication and earning your employees' trust.

Your goal is to make sure they see this as a valuable new benefit, not a confusing requirement they're being forced into. It's all in how you frame it. Start by zeroing in on the benefits that will make the biggest difference in their day-to-day lives. For many, this is the end of paying high check-cashing fees and the beginning of having instant access to their wages on payday.

Crafting a Positive and Transparent Message

Your communication plan needs to be proactive and, above all, transparent. Try to get ahead of their questions and address them directly before they bubble up into bigger concerns. This is your chance to show your team that you’ve thought through their needs during this process.

When you introduce the payroll card option, stick to simple, clear language. Ditch the jargon and focus on the real-world advantages.

Here are a few key points to build your announcement around:

- Instant Access to Pay: Let them know that on payday, their money is on their card and ready to use immediately. No more waiting for a check to clear or having to make a special trip to the bank.

- Saving Money: For employees who don't have a traditional bank account, this is a huge win. Highlight that this eliminates the need for expensive check-cashing services, which can save them a significant amount of money over the course of a year.

- Convenience and Security: Position the card as a modern, secure way to handle their money. Explain that it works just like a debit card from a bank—they can use it for online shopping, paying bills, and at any store that accepts debit cards.

The most critical message you need to deliver is that this program is 100% voluntary. You have to reassure your team that direct deposit and paper checks (if you offer them) are still available. This is a choice, not a command.

Addressing Common Employee Concerns

It's only natural for employees to have questions, and some might even be a little skeptical at first. Your job is to listen, understand their perspective, and give them clear, honest answers. The most frequent worries usually center on hidden fees and how to get cash without getting charged for it.

Be ready to answer questions like:

- "Are there hidden fees I need to worry about?"

- "How do I get my cash out without paying a fee?"

- "What happens if I lose my card?"

The best way to tackle these concerns is to provide a simple, one-page document that clearly lays out the fee schedule. Make sure to highlight all the free services, like withdrawals at in-network ATMs, checking their balance on a mobile app, and at least one way they can get their full pay for free each pay period.

A thoughtful communication strategy is a core part of effective employee onboarding best practices, even when you're introducing something new to existing staff. Holding short, in-person info sessions can work wonders. These meetings give you a chance to walk through the program, show them how the mobile app works, and answer questions on the spot. By providing clear materials (in multiple languages, if needed), you build confidence and help ensure your team feels good about this modern payment solution.

When to Partner with a Payroll Expert for Implementation

While you might be able to implement payroll cards on your own, knowing when to call in a professional is a smart business move. For a company operating in one state with a simple payroll, a DIY approach can work just fine.

However, as soon as your business starts to grow or get more complicated, it’s often best to get help from an expert.

Navigating Complexity and Ensuring Compliance

One of the most common reasons to hire a payroll expert is if you have employees in multiple states. Each state has its own specific regulations on payroll cards for employers, which can create a real compliance headache. An expert helps you navigate these different rules so you don’t accidentally break the law.

Rapid growth is another trigger. When your business is scaling, your team is already busy. Adding a major project like implementing a new payroll system can be overwhelming. They have to research vendors, handle integrations with Gusto or QuickBooks, and manage employee communications.

An expert partner like Steingard Financial can take the implementation burden off your team. We have the experience and resources to manage the project efficiently, letting you focus on running your business.

Here are a few other signs that it's time to call for professional help:

- Messy Historical Books: If your past financial records are a mess, you need to clean them up before switching to a new payroll system. An expert can handle this first, ensuring a smooth transition.

- Lack of In-House Expertise: Many small businesses don't have a dedicated HR or payroll specialist. A payroll partner fills this knowledge gap, making sure your rollout is compliant and successful.

- Complex Integrations: You need to ensure your payroll card system works seamlessly with your accounting and HR software. An expert can manage the technical side of the integration to prevent data errors and extra manual work.

Partnering with a payroll expert isn't about admitting you can't do it yourself. It's a strategic choice to get the implementation done right the first time, saving you time, money, and future compliance issues.

Frequently Asked Questions About Payroll Cards

Even after seeing the benefits, you probably still have a few questions about how payroll cards work in the real world. Let's walk through some of the most common things business owners ask so you can move forward confidently.

Can I Require My Employees to Use Payroll Cards?

No. Federal law (Regulation E), along with most state laws, is very clear on this: you can't force an employee to be paid via a payroll card. You must always offer at least one alternative, like direct deposit or a paper check.

Think of it as adding another voluntary option to your payment toolkit. Pushing for mandatory adoption can land you in legal trouble, so it's always best to position paycards as a choice that gives your team more flexibility, not less.

What Are the Most Common Fees with Payroll Cards?

While most day-to-day use is free, some fees can pop up. The usual suspects include fees for using an out-of-network ATM, monthly maintenance charges if a minimum balance isn't kept, card replacement fees if one gets lost, or charges for requesting paper statements.

Federal law requires that every employee must be able to access their full pay for free at least once per pay period. Your job as the employer is to find a provider with a simple, fair fee structure and make sure you explain all potential costs to your team before they sign up.

How Do Payroll Cards Integrate with Gusto or QuickBooks?

Good news here. Most payroll card providers are built to connect smoothly with popular software like Gusto and QuickBooks. The setup process is simple and works just like adding any other payment method.

It usually breaks down into these three steps:

- Provider Setup: You'll add your new paycard vendor as a payment option inside your payroll software.

- Employee Selection: For any employee who chooses this option, you just select "payroll card" as their payment method in their profile.

- Payroll Run: When you run payroll, the system does the rest. It sends the funds to the right place—to bank accounts for direct deposit employees and loaded onto the cards for paycard users.

This automation means that adding payroll cards won't create extra manual work for you. It just becomes another seamless part of your existing process.

Navigating the details of payroll card setup and compliance can feel like a lot. Working with a dedicated partner ensures your program is built correctly from day one. Steingard Financial specializes in creating scalable back-office solutions for service businesses, helping you integrate systems like payroll cards with Gusto and QuickBooks for accurate, headache-free financial management. Learn more about how we can support your financial health and growth.