What Is a Contra Account and Why Does It Matter?

When you look at your business's financial statements, you want the real story, right? Not just a partial picture. That’s precisely where contra accounts come in—they add the context and detail needed to see your finances clearly.

Think of it this way. Imagine your service business invests in a powerful new server for $50,000. You log it on your books as a $50,000 asset. Simple enough. But a few years down the road, is it really worth that original price? Of course not; technology ages.

Instead of just deleting the old value and penciling in a new one—which would erase important history—you use a contra account. In this case, it’s called Accumulated Depreciation. This account holds the $20,000 in value the server has lost over time.

Now your books tell the complete story: you own a server you bought for $50,000, it has since depreciated by $20,000, and its current book value is $30,000. You see the original cost and its present value, all without losing any information.

The Importance of Financial Transparency

This method isn’t just about being neat; it's about being honest with yourself, your partners, and any potential lenders. By using contra accounts, you preserve the historical cost of an asset or the gross amount of sales while clearly showing any adjustments that have been made.

A contra account’s primary job is to provide financial clarity. It prevents you from overstating the true value of your assets and revenue, giving you a realistic understanding of your company's net worth and performance.

Without them, your financial reports could easily become misleading. For example, your Accounts Receivable might show a huge number, making it seem like you have a ton of cash coming in. But what if some of those clients never pay? An Allowance for Doubtful Accounts—another contra account—sets aside a realistic estimate for this bad debt, giving you a much truer forecast of your actual cash flow.

How Contra Accounts Drive Better Decisions

At the end of the day, clean books lead to smarter choices. Contra accounts are a key tool for making accurate, data-driven decisions. They help you:

- See the True Value: Understand the net book value of your assets, not just what you paid for them.

- Measure Real Revenue: See the difference between your gross sales and the net sales you actually pocket after returns and discounts.

- Maintain Compliance: Stick to Generally Accepted Accounting Principles (GAAP), which require this kind of financial transparency.

- Gain Deeper Insights: Analyze the health of your business with more precision, because you can see both the starting figures and all the adjustments along the way.

To really get how these accounts work, it helps to understand the system they live in. The principles of Double Entry Bookkeeping Explained are the foundation of all modern accounting. Once you’re comfortable with that, you’ll see how contra accounts fit perfectly into creating a reliable financial picture. You can learn more by checking out our own guide on double-entry bookkeeping.

Exploring the Four Types of Contra Accounts

So, we’ve established that a contra account is basically a financial counterbalance. Now let's dig into the four main types you’ll run into while doing your books. Each one is designed to work with a parent account to give you a much more honest and complete financial picture.

Think of it this way: each category is like a different lens you can use to look at your business. One lens helps you see your assets with more clarity, while another shows you what’s really happening with your revenue. We’ll go through each one with some real-world examples that every service business owner can relate to.

Contra Asset Accounts

A contra asset account is used to reduce the value of an asset on your balance sheet. Why not just change the asset’s original value? Because that erases important historical information. This account tracks the reduction separately. It has a credit balance, which is the exact opposite of a typical asset account.

The two you’ll see most often are:

- Accumulated Depreciation: This tracks the total loss in value of a long-term asset, like your company vehicle or computer equipment, since you first started using it.

- Allowance for Doubtful Accounts: This is your best guess of how much of your accounts receivable you realistically won’t be able to collect. It’s a dose of reality that keeps you from overstating the cash you have coming in.

Let’s say your consulting firm buys $20,000 in new office furniture. That’s a fixed asset. As that furniture gets older, you’ll record a Depreciation Expense on your income statement and credit the Accumulated Depreciation account on your balance sheet. This shows the asset’s value is decreasing over time without you having to forget what you originally paid for it.

Contra Revenue Accounts

Next up are contra revenue accounts. Their whole job is to lower your gross sales number to get to your true net sales. For any service business, what you bill isn't always what you end up keeping. These accounts help you track that important difference.

They carry a debit balance, which goes against the normal credit balance you see in a revenue account. They help you answer the critical question, "After all the refunds and discounts, how much did we really make?"

Common examples include:

- Sales Returns: When a client is completely unsatisfied and you issue a full refund, this account tracks it.

- Sales Allowances: This is for when you give a partial refund to smooth things over with a client—for instance, giving them 20% off a project fee because you missed a deadline.

- Sales Discounts: If you offer clients a small discount for paying their bills early (you might see terms like "2/10, n/30"), this account tracks how much those discounts cost you.

Think of an account like "Sales Returns and Allowances" as your satisfaction guarantee's financial footprint. It shows how much revenue you sacrificed to keep your clients happy. It’s far more insightful to track this separately than to just quietly reduce your sales total. When you review your reports, you can spot if client satisfaction is starting to dip.

These adjustments are often handled by issuing a credit memo, which is the official document reducing what a customer owes. You can get a closer look at how that works in our guide on credit memo samples.

Contra Equity Accounts

A contra equity account brings down the total value of the owner's equity in the business. Most equity accounts, like Retained Earnings, have a credit balance. True to form, contra equity accounts do the opposite—they have a debit balance. They show reductions in equity that have nothing to do with day-to-day business expenses.

Here are the most common ones:

- Treasury Stock: This account is for corporations that buy back their own shares from the market. It shows the company is reinvesting in itself, but it also reduces the total equity held by outside shareholders.

- Owner's Draws: For sole proprietors and partners, this is where you track any money the owner takes out of the business for their own personal use.

An Owner's Draw is not a salary or an expense. It's a direct reduction of the owner's capital investment in the company. Using a contra equity account keeps this transaction separate from your business's operational performance on the income statement.

For example, if you own an LLC and transfer $5,000 from the business checking account to your personal account to cover living expenses, it gets recorded in the Owner's Draw account. This gives you a clean record of the reduction in your equity stake without making it look like your business is less profitable than it actually is.

Contra Liability Accounts

Last but not least are contra liability accounts. These are by far the least common of the four, but they work on the same principle: reducing the balance of a parent account. In this case, they reduce a liability.

Since a liability account normally has a credit balance, a contra liability account carries a debit balance. The main place you’d ever see one is in complex corporate finance.

- Discount on Bonds Payable: If a company issues a bond for less than its face value (to make it more attractive to investors), this account tracks that discount. The discount is then slowly written off over the bond's life, bringing the liability's carrying value up to its full face value by the time it matures.

Honestly, for most service businesses, you’ll probably never need to create a contra liability account. Your main focus will be on mastering contra asset, contra revenue, and contra equity accounts. Getting those right is key to keeping your financial statements transparent and accurate.

Contra Asset Accounts in Action for Service Businesses

For service-based businesses, contra asset accounts aren't just accounting jargon; they're essential tools for managing your cash flow and making smart decisions about where to invest your money. Let's get practical and see how these accounts work in the real world for businesses like yours.

We'll focus on the two most common and critical examples you'll run into.

First, picture a marketing agency with $100,000 in Accounts Receivable. On paper, that looks amazing—a huge chunk of cash is supposedly on its way. But as any experienced business owner knows, not every single invoice gets paid.

Ignoring this hard truth can create dangerous gaps in your cash flow when you count on money that never shows up. This is exactly where the Allowance for Doubtful Accounts comes in. It's a contra asset account that helps paint a more realistic financial picture.

Example 1: The Marketing Agency and Uncollectible Invoices

Let's say our agency pulls its accounts receivable aging report. Looking at past payment history, they estimate that about 3% of their total receivables will probably never be collected. This happens for all sorts of reasons—clients go out of business, dispute the work, or just plain disappear.

Instead of waiting to see which specific invoices go bad, the agency proactively creates an allowance. It makes an adjusting journal entry to account for the $3,000 ($100,000 x 3%) in expected bad debt.

- The Result: The balance sheet still shows the full $100,000 in Accounts Receivable, but it's immediately paired with the $3,000 in the Allowance for Doubtful Accounts.

- The Net Value: This gives the business a Net Accounts Receivable of $97,000.

This one simple adjustment brings immense clarity. The owner now has a much more accurate cash flow forecast. They can budget based on the $97,000 they realistically expect to collect, not the overly optimistic $100,000 sitting in their invoicing software.

This is a critical practice for service businesses, which tend to have higher bad debt rates. In fact, data shows service industries often see bad debt rates of 1.5-3%, noticeably higher than manufacturing's average of 0.8%. This is partly because service payment terms can stretch out for 45 or even 60 days. You can discover more insights about managing credit risk on opibari.it.

Example 2: The Tech Consultancy and Depreciating Assets

Now, let's switch gears to another common scenario. A tech consultancy invests $50,000 in powerful new servers to support its client projects. This is a major purchase, recorded on the books as a fixed asset. The problem is, that equipment doesn't stay worth $50,000 for long.

This is where Accumulated Depreciation becomes so important. It's a contra asset account that keeps a running total of how much of an asset's cost has been "used up" over time.

Think of accumulated depreciation as telling the story of an asset's life. It shows how much of its value has been converted into an expense as it helped your business generate revenue.

Let's assume the servers have a useful life of five years. Using the simple straight-line method, the annual depreciation expense is $10,000 ($50,000 / 5 years). Each year, the consultancy records this expense.

- Year 1: The Accumulated Depreciation account shows a credit balance of $10,000. The equipment's net book value is now $40,000 ($50,000 – $10,000).

- Year 3: The Accumulated Depreciation balance grows to $30,000. The net book value has dropped to $20,000 ($50,000 – $30,000).

By using this contra account, the consultancy keeps the server's original $50,000 purchase price (its historical cost) on the books, which is important for tax and insurance reasons. At the same time, it gives a true and fair view of the asset's current worth on the balance sheet.

This clarity is vital for planning future tech upgrades and managing the company's asset base effectively.

How Contra Accounts Appear on Financial Statements

It’s one thing to talk about contra accounts, but seeing them on your financial statements is where it all really clicks. These accounts aren't hidden away in some complex report. Instead, they show up right next to their parent accounts to tell a more complete financial story.

This placement is completely intentional. By pairing a contra account directly with its related account, your financial statements show you two things at once: the original, historical value and the current, adjusted net value. It’s a simple but powerful way to get an accurate financial picture.

On the Balance Sheet

The balance sheet is a snapshot of your company's assets, liabilities, and equity at a specific point in time. This is where you'll find contra asset accounts, usually listed right below the asset they adjust.

Let's use a common example. Imagine your service business bought a new server rack for $50,000. Two years go by, and you've recorded $20,000 in depreciation. In the Property, Plant, and Equipment (PP&E) section of your balance sheet, it would look like this:

- Equipment (at cost): $50,000

- Less: Accumulated Depreciation: ($20,000)

- Net Equipment: $30,000

See how Accumulated Depreciation is clearly labeled and subtracted? The parentheses around ($20,000) show it's a reduction. This format instantly tells anyone reading the report the original investment, how much of its value has been used, and the asset's current book value.

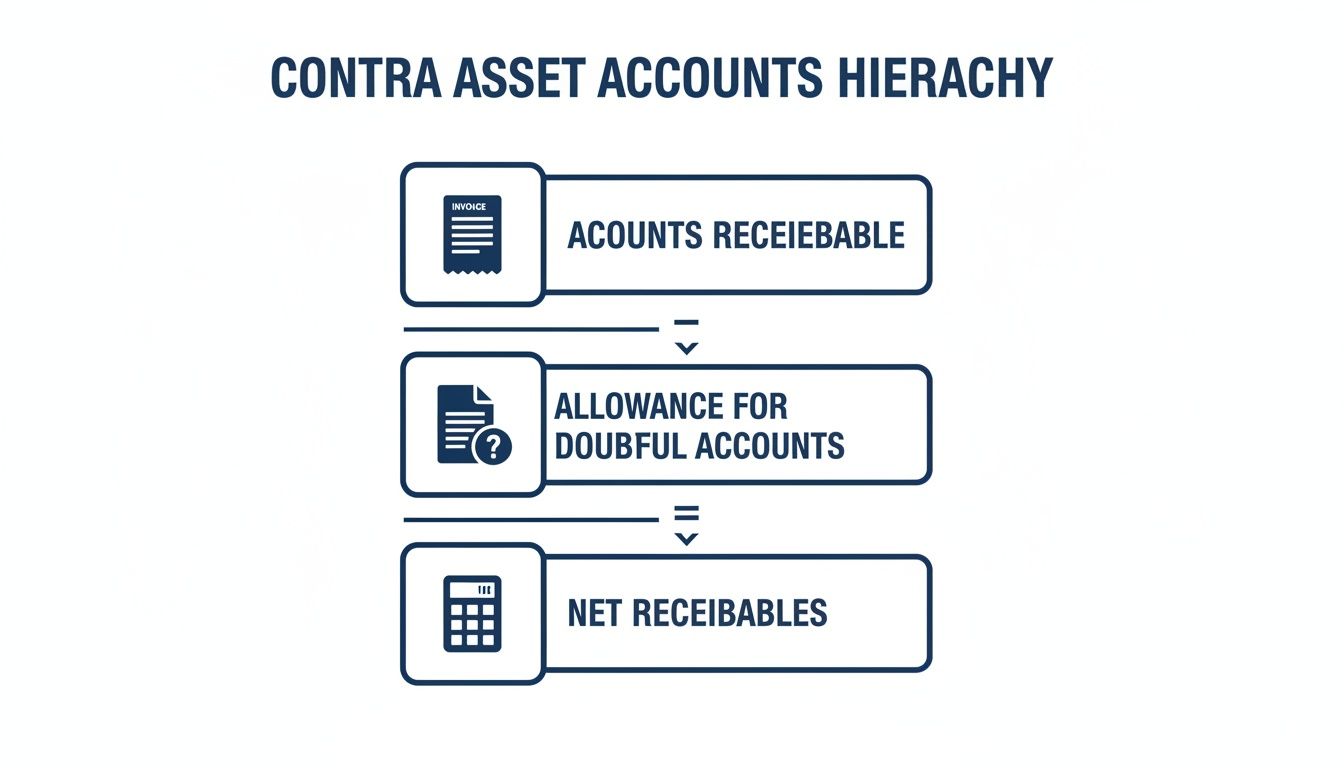

The same idea applies to your Accounts Receivable. A contra account gives you a much more realistic view of what you actually expect to collect from clients.

This diagram shows how an Allowance for Doubtful Accounts is subtracted from your total Accounts Receivable, giving you a more accurate Net Receivables number for your financial planning.

By presenting information this way, the balance sheet doesn't just give you a number; it tells a story. It shows the journey of your assets from their initial cost to their present-day value, which is essential for making informed decisions about future investments and managing cash flow.

On the Income Statement

The income statement, on the other hand, measures your company's financial performance over a period, like a month or a quarter. This is where contra revenue accounts come into play. Their job is to adjust your gross sales to reflect the revenue you actually earned and kept.

You'll find contra revenue accounts at the very top of the income statement, right under your total sales figure. They are subtracted from gross revenue to calculate Net Sales, which is the real starting point for figuring out your profitability.

Let's say a consulting business generated $100,000 in gross revenue last quarter. In that time, they also issued a $2,000 refund for a project delay (a sales allowance) and gave clients $3,000 in early payment discounts.

Here’s a simplified look at their income statement:

- Gross Sales: $100,000

- Less: Sales Allowances: ($2,000)

- Less: Sales Discounts: ($3,000)

- Net Sales: $95,000

This is so much more useful than just seeing a single revenue number of $95,000. By breaking out the allowances and discounts, you can spot trends. Are your sales allowances climbing? That could point to problems with project delivery. Are discounts going up? Maybe your early payment offers are working, but it also shows you the cost of getting that cash faster.

This level of detail, made possible by contra accounts, turns your financial statements from a simple report card into a powerful diagnostic tool for your business.

Setting Up Contra Accounts in Your Accounting Software

Knowing what a contra account is in theory is one thing, but putting that knowledge into practice is what really matters for clean, accurate books. If you don't set these accounts up correctly in your software from the very beginning, your financial reports won't give you the true picture you need to run your business well.

The good news is that most modern accounting software, like QuickBooks, makes this process pretty straightforward. The real secret is making the contra account a sub-account of its parent account. This simple move links them together forever, ensuring they always show up together on your financial statements and provide that clarity we've been talking about.

Creating a Contra Asset Sub-Account

Let's walk through the most common setup: creating an Allowance for Doubtful Accounts to sit alongside your Accounts Receivable. The steps are very similar for other contra accounts, like Accumulated Depreciation.

- Head to Your Chart of Accounts: This is the master list of all your financial accounts.

- Create a New Account: Look for the option to add a new account.

- Choose the Right Account Type: This part can feel a little strange. For Allowance for Doubtful Accounts, you'll select "Accounts Receivable" as the account or detail type. For Accumulated Depreciation, you'd choose "Fixed Asset."

- Name the Account: Be specific. "Allowance for Doubtful Accounts" or "Accumulated Depreciation – Servers" are great examples.

- Make It a Sub-Account: This is the most critical step. Find the checkbox or dropdown menu that says "Is sub-account." You have to check this box and then choose the correct parent account (like Accounts Receivable or the specific fixed asset).

Getting your chart of accounts right is the foundation of all good bookkeeping. If you want to dig deeper into this core element, you can learn more about https://steingardfinancial.com/how-to-create-a-chart-of-accounts/.

Here’s a look at the new account screen in QuickBooks, where you can see the option to make it a sub-account of a parent.

By checking that "Is sub-account" box and picking the parent, you guarantee your contra account will always appear neatly tucked under its parent on the balance sheet.

Software and Best Practices

While we've used QuickBooks as an example, these principles apply to almost any accounting platform. For businesses in the UK, options from accounting software like Sage 50 and Sage 200 follow the same logic, even if the menus look a bit different.

Key Takeaway: The goal isn't just to create an account. It's to build a logical hierarchy. A contra account that isn't properly linked to its parent is just a confusing, free-floating number on your reports.

Keep these best practices in mind:

- Be Consistent: Make your adjusting entries for things like depreciation and potential bad debt every month or quarter. You can often set up rules to help automate this.

- Use Clear Naming: "Accumulated Depreciation" is good, but "Accumulated Depreciation – Office Equipment" is much better.

- Review Regularly: Take a look at your allowance for doubtful accounts at least quarterly. Does the amount still make sense for your business and your clients?

When you get the setup right from the start, you're building a system that can grow with your business, ensuring your financial data stays reliable and your decisions are always based on solid numbers.

Answering Your Top Questions About Contra Accounts

Even with a solid grasp of the basics, business owners often run into the same practical questions when putting contra accounts to work. Let's clear up some of the most common points of confusion so you can manage your books with confidence.

These are the real-world questions we hear from business owners just like you when they start using these important accounting tools.

Is a Contra Account the Same as an Expense?

This is a great question, and the short answer is no. While they might feel similar, they play very different roles in your financial statements.

An expense, like "Rent Expense" or "Software Subscriptions," is a cost your business incurs in a specific period, like a month or a quarter. It shows up on your income statement and directly lowers your profit for that time.

A contra account, however, is a balance sheet account. Its job isn't to record a new cost but to reduce the book value of another account. For example, "Accumulated Depreciation" chips away at the value of an asset like "Equipment" over its entire useful life.

Key Distinction: An expense tells you what your business spent in a period. A contra account tells you how much an asset's or revenue's value has changed over time.

Think about depreciation. The "Depreciation Expense" on your income statement shows the value lost just for the current year. But the "Accumulated Depreciation" on your balance sheet shows the grand total of all depreciation you've recorded since you first bought the asset. One is a periodic cost; the other is a cumulative reduction.

How Do I Calculate My Allowance for Doubtful Accounts?

For service businesses, figuring this out is crucial for forecasting your cash flow accurately. The most reliable way to do this is the percentage of receivables method, which starts with an accounts receivable (A/R) aging report.

Here’s a simple, step-by-step way to do it:

- Run an A/R Aging Report: This report sorts your outstanding invoices into buckets based on how long they've been past due (e.g., current, 1-30 days, 31-60 days, 61-90 days, 90+ days).

- Assign Risk Percentages: Based on your business’s collection history, you'll assign a percentage of expected non-payment to each aging bucket. The older an invoice is, the higher its risk percentage.

- Calculate the Allowance: Multiply the total receivables in each bucket by its risk percentage, then add up the results to get your total allowance.

Your breakdown might look something like this:

- Current: 1% risk

- 1-30 Days Past Due: 3% risk

- 31-60 Days Past Due: 10% risk

- 61-90 Days Past Due: 25% risk

- Over 90 Days Past Due: 50% risk

If your business is new and doesn't have much collection history, starting with industry averages is a good move. For most service companies, an allowance of 1-3% of your total receivables is a reasonable starting point. The important thing is to review this allowance at least quarterly to make sure it still reflects your actual experience.

Why Not Just Reduce the Asset Account Directly?

This question gets to the core of why contra accounts are so important for honest financial reporting. It might seem easier to just edit the asset's value on your books, but doing that would erase critical financial history.

Preserving an asset's historical cost—the original price you paid—is a fundamental part of good accounting for a few key reasons:

- Financial Analysis: Important metrics like Return on Assets (ROA) depend on knowing the original cost of your assets to be calculated correctly.

- Insurance Purposes: If an asset is ever damaged or destroyed, your insurance provider will likely ask for proof of its original purchase price for the claim.

- Tax Reporting: The IRS requires you to calculate depreciation for tax purposes based on an asset's original cost, not its current book value.

Using a contra account like Accumulated Depreciation tells the full story. It clearly states, "We bought this piece of equipment for $50,000, and so far, $20,000 of its value has been used up." If you simply reported a net asset value of $30,000, you lose all that important context, making your financial history much harder to analyze.

What Are the Most Common Mistakes with Contra Accounts?

Contra accounts are incredibly useful, but they can create big problems if they aren't handled correctly. Knowing the common pitfalls can save you from a major cleanup project later.

The single biggest mistake is simply not using them at all. Many small businesses don't record monthly depreciation or set up an allowance for bad debt. This results in overstated assets and net income, which paints a misleading and overly optimistic picture of the company's financial health.

Another common error is setting them up incorrectly in your accounting software. A classic mistake is booking "Accumulated Depreciation" as a standard expense account instead of a sub-account of its related fixed asset. This kind of error completely throws off the balance sheet.

Finally, a "set it and forget it" mindset always leads to trouble. If you don't regularly review your "Allowance for Doubtful Accounts" against your actual collections, you could face a sudden cash flow crisis when revenue you were counting on never arrives. Regular reviews and adjustments are essential.

Managing these details is exactly what a dedicated bookkeeping partner does best. The team at Steingard Financial ensures your chart of accounts is set up correctly from day one, your adjusting entries are made on time, and your financial statements always tell the true story of your business's health. Visit us at https://www.steingardfinancial.com to learn how we can give you peace of mind and data you can trust.