Definition of Operating Cost: A Business Owner’s Guide

Your bank balance says the business is busy. Your calendar says the team is overloaded. Your revenue line looks respectable. But when you look for profit, the answer feels fuzzy.

That’s where a lot of service business owners get stuck.

A consulting firm can bill steadily and still feel cash-tight. A marketing agency can close new clients and still wonder why the owner isn’t seeing more take-home income. A professional services team can grow headcount and then realize too late that payroll, software, and admin costs rose faster than revenue.

The missing piece usually isn’t effort. It’s visibility.

If you understand the definition of operating cost, you stop treating your financials like a report card that arrives after the fact. You start using them like a dashboard. Instead of asking, “Where did the money go?” you can ask better questions. Are we priced correctly? Can we afford another hire? Are we carrying too much overhead? Which costs are necessary, and which ones are just habits?

For a service business, this matters even more because the biggest expenses often aren’t inventory or manufacturing. They’re people, systems, subscriptions, rent, and the support costs required to deliver work consistently.

A lot of owners think cost tracking is about cutting. It isn’t. Good cost tracking gives you control. It helps you protect margin, plan growth, and make decisions before your cash flow forces the issue.

Your Business's Financial Pulse

A common scene looks like this. You review the month, see solid sales, and expect the numbers to feel better than they do. Then you open the profit and loss statement and find a long list of expenses that all seem vaguely necessary.

Payroll feels necessary. Software feels necessary. Marketing feels necessary. Office costs, contractors, insurance, payroll taxes, bookkeeping, benefits, internet, recruiting, training. Necessary, necessary, necessary.

That’s exactly why operating cost matters.

Why owners feel confused

Most owners don’t struggle because they’re careless. They struggle because day-to-day spending happens in fragments.

One subscription gets added for project management. Another tool comes in for proposals. A new employee means payroll, benefits, onboarding time, and software seats. A client expansion leads to contractor support. None of those choices seem dramatic on their own.

Together, they shape the economics of the business.

Operating cost is one of the clearest ways to connect your daily decisions to your eventual profit.

When you know your operating costs clearly, you can spot patterns earlier. Maybe labor is rising faster than client billings. Maybe software has become bloated. Maybe your pricing worked when you had a smaller team but no longer supports the operation you’ve built.

Why this is a practical metric

For a service business owner, operating cost isn’t just an accounting term. It’s a way to answer questions like these:

- Hiring question: Can we add another account manager without straining cash flow?

- Pricing question: Are our current fees covering delivery and overhead?

- Efficiency question: Are we spending too much on support functions compared with revenue?

- Capacity question: Can this team serve more clients without another layer of cost?

The businesses that stay calm during growth usually aren’t the ones with perfect conditions. They’re the ones that know their numbers well enough to act early.

What Are Operating Costs Really

The formal definition of operating cost is simple. Operating costs are the day-to-day expenses a business incurs to maintain ongoing operations, calculated with the standard formula Operating cost = Cost of Goods Sold (COGS) + Operating Expenses (OPEX), as outlined by NetSuite’s explanation of operating cost and illustrated with a major tech company income statement showing revenue of $55,908,000, cost of revenue of $45,958,000, operating expenses including R&D of $463,000 and SG&A of $5,140,000, and operating income of $4,347,000 (NetSuite).

That definition sounds technical, but the idea is straightforward. Operating cost is what it takes to keep the business running in normal conditions.

A simple way to think about it

Think of your business like a car.

COGS is the cost tied to completing the trip itself. In a service business, that might be labor directly involved in client delivery, contractor support for a project, or other direct delivery costs.

OPEX is what keeps the car road-ready. Insurance, registration, maintenance, and routine upkeep don’t belong to one trip. They support all trips.

For most service businesses, OPEX gets most of the attention because direct production-style costs may be light or even minimal. The heavier burden often sits in payroll, admin salaries, software, rent, marketing, insurance, and support systems.

The two parts of the formula

Here’s the clean breakdown:

| Component | What it includes | Service business examples |

|---|---|---|

| COGS | Direct costs of delivering the service | Billable contractor costs, direct service labor, project-specific delivery tools |

| OPEX | Indirect costs that support operations | Admin payroll, rent, software subscriptions, insurance, marketing, utilities |

Owners often get tripped up here. They assume all payroll belongs in one bucket. It doesn’t.

A designer working directly on client work may be treated differently from an operations manager, office administrator, or business development lead. The exact treatment depends on your model and accounting setup, but the broader lesson is the same. Not all labor serves the same financial function.

Why this matters in real life

When you blur COGS and OPEX, your reports lose meaning. You may still have “expenses,” but you won’t know whether margin problems come from service delivery, overhead, or both.

That distinction affects decisions like:

- Pricing services

- Evaluating team utilization

- Comparing periods accurately

- Understanding whether overhead is expanding too fast

Paid time off can also be a hidden source of confusion in labor planning. If you’re trying to understand staffing-related overhead more clearly, a practical breakdown of the cost of annual leave can help you think through how time away from work affects your real operating structure.

Practical rule: If a cost helps you keep the business functioning on an ongoing basis, it probably belongs in your operating cost picture, even if it doesn’t tie neatly to one invoice or one client.

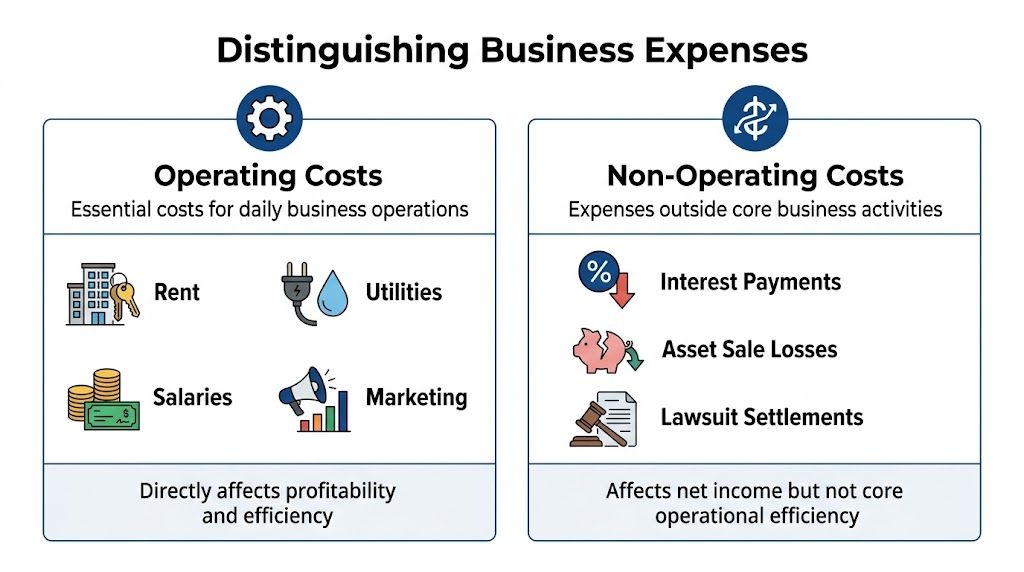

Distinguishing Operating Costs from Other Expenses

A lot of reporting problems start with one habit. Owners treat every outflow as if it belongs in the same category.

It doesn’t.

Some costs belong to regular operations. Some come from financing. Some are investments in long-term assets. If you mix them together, you can’t judge the business fairly.

Operating costs versus non-operating costs

In precise accounting terms, operating costs are the aggregate of COGS and OPEX. For service businesses using QuickBooks or Gusto, COGS may be minimal, shifting focus to OPEX, which often constitutes 60-80% of total operating costs, and a 15% rise in payroll due to inefficient staffing directly erodes operating profit (Happay).

Non-operating costs sit outside the core engine of the business. They still matter, but they tell a different story.

Here’s a clean comparison:

| Type | What it reflects | Typical examples |

|---|---|---|

| Operating costs | Running the core business | Payroll, software, rent, utilities, marketing |

| Non-operating costs | Financing or unusual items outside core operations | Interest payments, one-time legal settlements, losses unrelated to normal delivery |

| Capital expenditures | Long-term investments in assets | Buying major equipment, large technology implementations, property improvements |

If you want a fuller primer on business expense categories, this overview of https://steingardfinancial.com/what-are-expenses-in-business/ is a useful companion.

Why capital expenditures are different

A capital expenditure usually creates value over more than one period. You’re not consuming it immediately the way you consume rent, internet, or payroll in the current month.

That’s why a major server purchase, office build-out, or significant equipment buy usually isn’t treated the same way as your routine monthly expenses.

A simple test helps:

- Short-lived and consumed in current operations: usually operating cost

- Creates longer-term benefit: often capital expenditure

- Outside day-to-day operations: often non-operating

Why owners should care

This distinction isn’t academic. It changes how you read performance.

If a month looks weak because of a one-time financing cost, that tells a different story than a month where recurring payroll and software overhead climbed. If you classify a long-term asset purchase as a regular operating expense, your operating picture looks worse than it really is.

A clean profit and loss statement helps you diagnose the right problem. Bad categorization leads owners to fix the wrong one.

For service businesses, the danger zone is often OPEX creep. A little more payroll here, another admin tool there, a duplicate software stack somewhere else. Those costs can gradually thicken the business until growth no longer feels profitable.

Operating Cost Examples for Service Businesses

Manufacturing examples aren’t very helpful when you run an agency, consulting practice, law firm, accounting firm, IT services company, or professional services team. You need examples that match how your business works.

What COGS may look like in services

In a service business, COGS often includes costs directly tied to delivering client work.

Examples might include:

- Client delivery labor: Team members whose time is directly connected to billable service work

- Project-based contractors: Freelancers or specialists hired to complete client assignments

- Delivery-specific tools: Software used only for a particular client engagement or delivery process

- Implementation support: Temporary costs that exist because you’re actively providing a service

Some service firms keep COGS very light. Others rely heavily on direct labor and contractor networks. That’s why two companies with similar revenue can have very different cost structures.

What OPEX usually includes

For most service businesses, OPEX is where the action is.

Common examples include:

- Payroll for support roles: Operations managers, executive assistants, finance staff, HR support, sales staff

- Occupancy costs: Office rent, coworking memberships, utilities, internet

- Software subscriptions: QuickBooks, Gusto, Slack, Asana, CRM tools, proposal software, password managers

- Sales and marketing spend: Ad campaigns, website hosting, SEO support, sponsorships, branding work

- Professional services: Legal fees, bookkeeping, tax support, consultants

- Insurance and compliance: General liability, professional coverage, workers’ compensation, filing fees

- Administrative costs: Office supplies, postage, phones, team training, recruiting tools

A practical checklist

If you’re unsure whether something belongs in your operating cost review, ask three questions:

- Does this support day-to-day business activity?

- Would the business struggle to function normally without it?

- Is it part of regular operations rather than a rare event or long-term investment?

If the answer is yes, it probably belongs somewhere in your operating cost picture.

Where owners often miss costs

The easiest expenses to overlook are the ones that arrive automatically.

Monthly subscriptions are a good example. So are payroll add-ons, software seat increases, recurring marketing retainers, and small admin tools that no one reevaluates after the initial purchase.

Another blind spot is labor that isn’t directly client-facing but still expands as the company grows. A business can add coordinators, managers, recruiters, and support roles gradually until overhead changes the economics of every sale.

That doesn’t mean those hires were mistakes. It means they need to be visible.

Categorizing Costs in QuickBooks and Gusto

Knowing the definition is useful. Building your books so the definition shows up clearly is what makes it actionable.

Start with the chart of accounts

Your chart of accounts is the structure behind every report you read. If the structure is sloppy, the reporting will be sloppy too.

A service business usually benefits from separating operating costs into meaningful groups rather than dumping everything into broad buckets like “miscellaneous expense” or “general admin.”

Useful categories often include:

- Payroll and payroll taxes

- Employee benefits

- Software subscriptions

- Marketing and advertising

- Rent and occupancy

- Professional fees

- Contractor payments

- Insurance

- Office and administrative expenses

That level of separation helps you see what’s changing from month to month.

If you want a practical framework for structuring accounts cleanly, this guide on how to categorize business expenses is a helpful reference. For a deeper bookkeeping-specific setup, https://steingardfinancial.com/how-to-create-a-chart-of-accounts/ offers useful context.

Why account detail matters

Owners sometimes worry that too much detail creates clutter. The risk is the opposite.

If “software” and “contractors” sit in one catch-all line, you can’t tell whether overhead is rising because you added tools or because delivery costs increased. If payroll, benefits, and payroll tax entries are jumbled together inconsistently, labor reporting gets distorted.

A cleaner setup gives you cleaner questions.

- Are software costs rising because the team grew?

- Are contractor costs replacing employee labor?

- Did marketing spend increase, or did lead generation just become less efficient?

- Is admin overhead stable, or is it creeping upward?

How Gusto fits into the picture

Gusto typically feeds payroll-related data into your accounting records. That means wages, taxes, benefits, and related payroll items need to land in the right expense accounts.

For service businesses, payroll is often the largest recurring operating cost. If payroll data posts to generic or incorrect accounts, your financial statements become much less useful.

Clean payroll mapping turns payroll from a black box into a decision tool.

A good setup makes month-end review easier. Instead of scanning one giant payroll number, you can see which parts of labor belong to direct service delivery and which parts belong to operating overhead.

A practical monthly habit

Review categorized expenses regularly, not just at tax time.

A simple operating-cost review might include:

- Scan new vendors and assign them correctly.

- Check recurring charges for duplicates or outdated subscriptions.

- Review payroll postings for consistency.

- Reclassify unusual items before month-end closes.

- Compare this month to prior months and investigate large swings.

That routine does more than keep the books tidy. It makes your reports trustworthy.

Using Operating Cost Data for Better Decisions

The biggest mistake owners make is treating operating cost as a historical label. It’s much more useful than that.

Search results often define operating costs as backward-looking metrics. For service businesses scaling from 5 to 50 employees, the ability to track operating costs weekly or monthly directly impacts hiring decisions, pricing models, and service delivery capacity, including knowing what percentage of revenue should go to payroll versus software for a 10-person firm (The Forage).

Turn reports into operating decisions

Once your data is categorized well, you can use it to answer real management questions.

One of the simplest tools is the operating cost ratio, which compares operating costs to revenue. Even if you don’t need a complex dashboard, this relationship helps you judge whether costs are becoming heavier relative to sales.

A rising ratio can mean several things:

- Labor is growing faster than billings

- Overhead is expanding before revenue catches up

- Pricing hasn’t kept pace with your cost base

- A service line may be less profitable than expected

For the formula itself and a related explanation of operating expenses, this internal resource is useful: https://steingardfinancial.com/how-to-calculate-operating-expenses/

The questions this metric helps you answer

Operating cost becomes strategic at this point.

Hiring

Before adding a new employee, look at whether current revenue can support not just salary, but the surrounding operating costs that come with the role.

Pricing

If delivery and overhead keep climbing while margins thin out, your prices may reflect an older version of the business.

Service mix

Some clients or services look good at the top line but absorb disproportionate labor, software, or admin support.

Timing

A decision can be good in principle but bad in timing. Real-time cost visibility helps you decide when to act, not just what to do.

Owners make better decisions when they can separate “we’re growing” from “we’re getting more expensive.”

Weekly and monthly visibility beats annual hindsight

Annual financials are useful for tax filing and broad review. They’re too slow for most operating decisions.

A service firm that reviews costs only at year-end often misses the moment when a manageable trend becomes a structural problem. Weekly and monthly visibility gives you time to respond.

That response might be:

- tightening software spend

- adjusting staffing plans

- improving utilization

- revisiting pricing

- pausing a nonessential expense

- changing how work is delivered

The point isn’t to chase perfection. It’s to create enough visibility that you’re steering the business instead of reacting to surprises.

The real benefit

Good operating cost data doesn’t just help you cut. It helps you spend with intent.

You may decide to increase payroll, invest in systems, or expand marketing. The difference is that you’ll understand what those choices demand from revenue and margin. That’s a stronger position than making decisions based on instinct alone.

Frequently Asked Questions About Operating Costs

Is depreciation an operating cost

It can be, depending on how it appears in your financial statements and what the asset supports. The key distinction is that the original purchase of a long-term asset is typically not treated like a routine operating expense in the period you buy it. The accounting treatment over time is separate from the initial cash outlay.

Are income taxes operating costs

Income taxes generally aren’t viewed as part of core operating performance. They matter to net results, but they don’t tell you what it costs to run the day-to-day business.

Is payroll always an operating cost

Often, yes. But not all payroll serves the same role. Some labor may be tied directly to service delivery, while some belongs in overhead. That’s why consistent classification matters.

What about a one-time website redesign

Usually, the answer depends on whether it’s routine upkeep or a larger long-term investment. If the spending creates a longer-lasting asset or major improvement, it may need different treatment than ordinary monthly operating expenses.

Why do my profits look weak even when revenue is growing

Because revenue growth doesn’t guarantee cost discipline. Payroll, software, support roles, and administrative overhead can rise unnoticed. If those increases aren’t tracked clearly, growth can feel much less profitable than expected.

If you want accurate books, cleaner payroll reporting, and financial visibility you can use to run the business, Steingard Financial helps service companies build a dependable back office with bookkeeping, payroll, chart-of-accounts setup, and reporting that supports better decisions.