If you're a sole proprietor, tax season often arrives the same way. You know you earned money. You know you spent money to run the business. But when it's time to file, your records live in too many places: a bank feed, a credit card, a payment app, email receipts, and maybe a notebook full of mileage and client notes.

That's why many owners struggle with how to file sole proprietor taxes. The forms matter, but the forms usually aren't the actual problem. The core problem is turning a year of messy transactions into clean, supportable numbers that belong on a tax return.

For service businesses, this gets harder when income comes from more than one source. Platform deposits, direct client payments, cash, transfers between accounts, and reimbursements can all blur together. As Carry notes in its discussion of sole proprietor tax filing, many guides don't spend enough time on reconciling deposits from multiple sources or matching 1099-K and 1099-NEC reporting to the books, even though that's often where filing errors start.

Your Guide to Navigating Sole Proprietor Taxes

A sole proprietor tax return is the final output of your bookkeeping. If the books are wrong, incomplete, or inconsistent, the return will be too.

That's the part new business owners often underestimate. They assume filing means filling in Schedule C, adding expenses, and moving on. In practice, the harder job is proving what your actual business income was, separating owner activity from business activity, and making sure your expense categories hold up if anyone ever asks how you got those numbers.

Filing starts long before the forms

A clean sole proprietor return depends on a few unglamorous habits:

- Separating transactions: Business income and expenses need their own trail.

- Categorizing consistently: Software subscriptions, contractor payments, travel, and supplies shouldn't land in random buckets.

- Reconciling deposits: Every deposit has to be identified correctly. Was it revenue, a transfer, a refund, or owner money moving between accounts?

- Keeping support: Receipts, invoices, and information returns need to match what's in the books.

When those basics are in place, tax prep becomes a review process. When they aren't, tax prep turns into forensic accounting.

The hardest part of filing often isn't completing Schedule C. It's producing a defensible income picture from incomplete records.

What works and what usually fails

What works is simple bookkeeping done early and repeated consistently. Download statements monthly. Match deposits to invoices or sales records. Save receipts when the transaction happens, not months later. Review your profit regularly so taxes don't become a surprise.

What usually fails is the year-end scramble. That's when owners try to rebuild everything from memory, guess at categories, and rely too heavily on whatever came through the bank account. Bank activity is useful, but it doesn't explain intent. A transfer can look like income. A reimbursement can look taxable. A personal charge can slip into business expenses if nobody catches it.

For a sole proprietor, the business and the owner meet on the same tax return. That makes good records more important, not less.

A practical way to think about the process

If you want a usable framework for how to file sole proprietor taxes, think of it in this order:

- Clean the books

- Reconcile income

- Review deductions

- Confirm tax payments already made

- Prepare the return from finalized numbers

That sequence saves time and reduces mistakes. It also gives you something more valuable than a filed return. It gives you confidence that the return is built on records you can effectively defend.

Gathering Your Financial Arsenal for Tax Season

Before preparing any tax form, gather the records that tell the story of the year. If something is missing here, the return will either be delayed or built on estimates that invite trouble later.

The strongest starting point is a dedicated business bank account. Clean separation between business and personal activity is the highest-value compliance control. Guidance for self-employed taxpayers also emphasizes early bookkeeping, preserving receipts and 1099s, and reserving roughly 25% to 30% of net income for taxes to reduce balance-due surprises, as summarized in this TurboTax guide for the self-employed.

Start with the records that define the year

If I'm reviewing a sole proprietor file, I want the source documents before I want tax software entries.

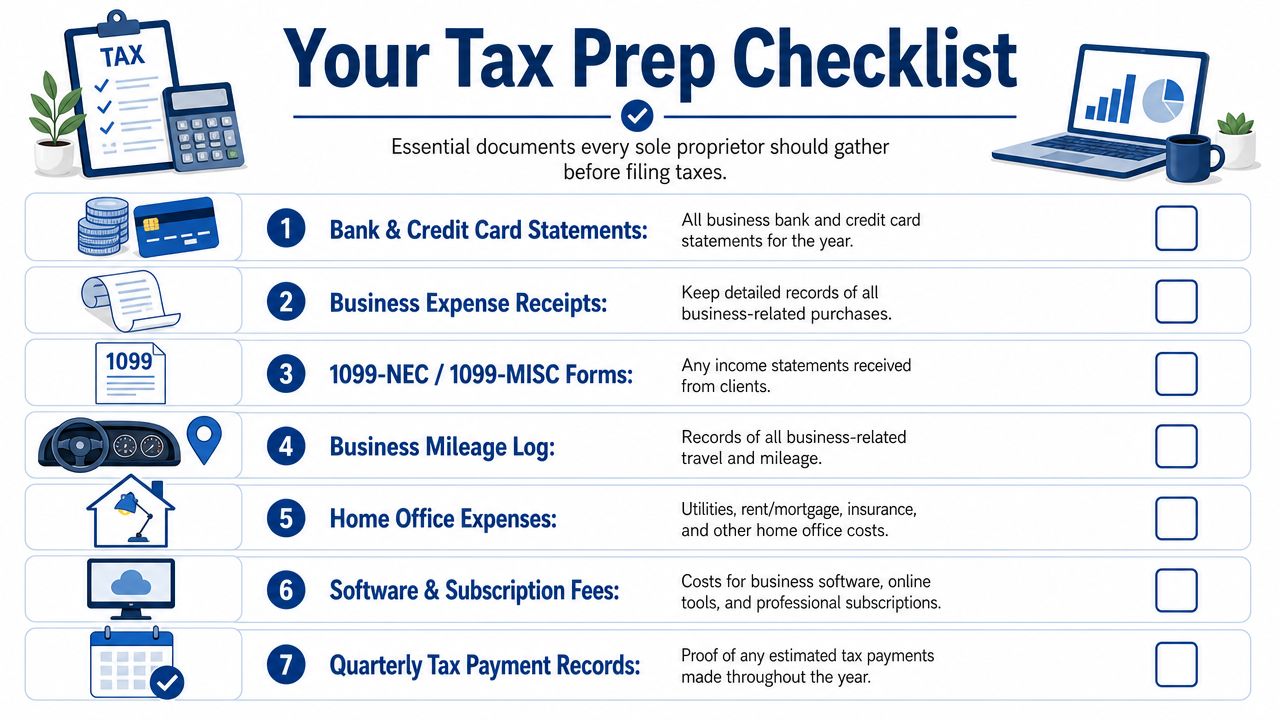

Here's the practical checklist:

- Business bank statements: Every month for the year. These help trace deposits, transfers, owner draws, and recurring expenses.

- Business credit card statements: Especially important when owners run software, travel, ads, or subscriptions through a card.

- Income records: Client invoices, payment processor reports, and every 1099 received.

- Expense support: Receipts, bills, and vendor statements for deductible costs.

- Mileage records: If vehicle use is part of the business, the log matters more than memory.

- Home office support: Utility bills, rent or mortgage records, insurance, and anything else tied to the business-use portion of the home.

- Quarterly tax payment confirmations: You want proof of what was already paid before the return is finalized.

Why each category matters

Bank and credit card statements show movement of money. They do not fully explain tax treatment. That's why they need backup.

A payment processor deposit might combine customer revenue with fees, refunds, and prior-period activity. A credit card statement may show a charge to Adobe, Zoom, or QuickBooks, but you still want confidence that the charge was business-related and not split with personal use. Tax prep gets smoother when each statement line already has a category and support behind it.

Practical rule: If a transaction would confuse you six months later, document it now.

The account separation issue

Owners sometimes resist opening a separate bank account because they think it's one more administrative step. In reality, it removes hours of cleanup later. Mixed accounts force you to review every transfer, every debit card charge, and every ambiguous deposit one by one. That isn't efficient bookkeeping. It's preventable cleanup.

If your records still need work, a structured pre-tax review helps. A year-end checklist like this tax season preparation guide is useful because it forces you to collect the documents that drive the return, not just the ones that are easiest to find.

What to fix before you file

Use this quick review before you move into tax preparation:

| Item | What you're checking |

|---|---|

| Income | Every deposit is identified and matched to revenue, transfer, refund, or reimbursement |

| Expenses | Charges are categorized and supported by receipts or vendor records |

| 1099s | All forms received are accounted for in your books |

| Payments | Estimated tax payments are documented |

| Accounts | Personal and business activity are separated as much as possible |

If that table looks messy for your business, stop there and clean it up first. That decision saves more trouble than rushing to the forms.

The Core Filing Mechanics Schedule C and Schedule SE

Clean books turn tax filing into a reporting exercise instead of a reconstruction project. By the time you reach Schedule C and Schedule SE, the hard part should already be done. The return is only as accurate as the records feeding it.

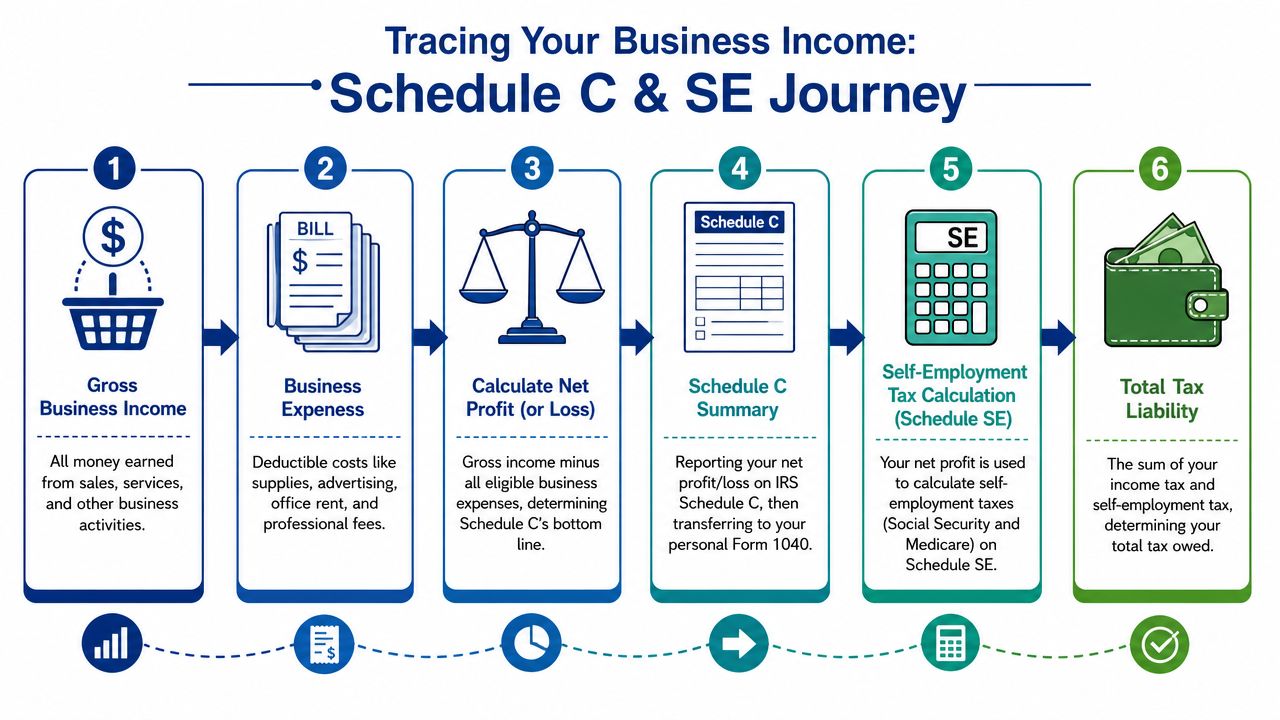

A sole proprietor usually reports business income and expenses on Schedule C, attaches it to Form 1040, and calculates self-employment tax on Schedule SE. If you make estimated payments during the year, those are handled through Form 1040-ES. If the business has employees, payroll filings sit outside this process and need separate attention.

How Schedule C and Schedule SE work together

Schedule C reports the results of your business activity for the year. Gross receipts go in. Ordinary and necessary business expenses come out. What remains is your net profit or loss.

That net profit carries real weight.

It flows onto your individual tax return, and it also feeds the self-employment tax calculation on Schedule SE. If the number on Schedule C is off, both your income tax and your self-employment tax can be off.

For service businesses, I see the same problems repeatedly. Deposits are missing because the owner relied on memory instead of reconciliation. Personal charges sit in business expense categories. Contractor payments are booked loosely. Refunds, reimbursements, and transfers get counted as income when they were never revenue in the first place. None of those mistakes starts on the tax form. They start in the bookkeeping.

A simple example of the flow

A freelance consultant finishes the year with $80,000 of gross business income and $20,000 of deductible business expenses. Schedule C shows $60,000 of net profit.

That $60,000 moves to Form 1040 as business income. It also becomes the starting point for Schedule SE.

The filing mechanics are straightforward. The preparation behind them is what determines whether the result is right.

If your books do not produce a supportable net profit number, filing the return becomes an exercise in cleaning up old errors under deadline pressure.

Where sole proprietors make mistakes on the forms

Most filing errors are not complicated tax law issues. They are recordkeeping issues that show up on tax forms late in the process.

Common examples include:

- Misclassified expenses: Software, meals, supplies, and contractor costs are booked in the wrong category.

- Unreconciled income: Bank deposits, processor payouts, refunds, and owner transfers are not separated correctly.

- 1099 mismatches: Income reported to the IRS does not line up with the books.

- Missing vehicle records: Owners claim mileage without a contemporaneous log. If that applies to you, use a business mileage tracking method that stands up at tax time.

- Contractor compliance gaps: Payments to freelancers were deducted, but related reporting was missed.

If you want a plain-English outside reference on avoidable filing errors, this guide to common Schedule C mistakes is a helpful supplement.

What to review before you sign the return

Before filing, confirm that Schedule C agrees to the books you intend to stand behind. That means total income matches your reconciled records, expense categories are reasonable and supported, and any 1099s received have been traced into revenue. It also means checking whether owner-paid business expenses, reimbursements, home office costs, or mileage were handled consistently.

This is the part many online guides rush past. They jump from “you need Schedule C” to “fill in the boxes.” In practice, the boxes are the easy part. The actual work is making sure each number has a clean trail back to your bank activity, invoices, receipts, and year-end adjustments.

That is why I tell clients to treat filing as the final output of their bookkeeping, not a separate annual task. If the records are clean, Schedule C and Schedule SE usually follow in an orderly way. If the records are messy, those same forms expose every unresolved issue at once.

Maximizing Your Business Deductions Strategically

Most owners ask, “What can I deduct?” The better question is, “Which ordinary business costs am I already paying, and have I tracked them well enough to claim them properly?”

That shift matters. Deductions aren't a scavenger hunt. They're the tax expression of how your business operates.

The deductions service businesses often overlook in practice

A consultant working from home may already be paying for internet, software, cloud storage, a second monitor, Zoom, scheduling tools, design tools, and professional liability coverage. A marketing agency owner may be spending on subcontractors, ads, training, web hosting, and business meals tied to client work. A therapist, coach, or bookkeeper may have recurring platform fees, licensing or membership costs, and a dedicated office setup inside the home.

These expenses usually aren't hidden. They're just scattered.

That's why clean categorization matters more than clever year-end deduction hunting. If the bookkeeping is weak, small recurring expenses disappear. If the bookkeeping is strong, legitimate deductions surface naturally because the system has been capturing them all year.

Categories worth reviewing carefully

Some deductions deserve extra attention because they're common and easy to mishandle:

- Mileage and vehicle use: If you drive for client meetings, site visits, or other business trips, keep a real log. Don't reconstruct it from memory at year-end. A detailed process for that is easier if you use a system like the one outlined in this business mileage tracking guide.

- Home office costs: If part of your home is used for business, the underlying records need to be organized. The deduction begins with documentation, not with a guess.

- Software and subscriptions: QuickBooks, Microsoft 365, Google Workspace, Canva, Adobe, CRM tools, project management apps, and industry software often add up meaningfully over a year.

- Professional services: Fees paid to a bookkeeper, accountant, attorney, or business consultant are often part of normal operations.

- Marketing and sales costs: Website hosting, ad spend, email tools, printed materials, and branding work belong in the books if they support the business.

A missed deduction usually isn't about tax law. It's about poor records.

What doesn't work

Two habits cause trouble.

First, owners try to claim expenses they didn't document. Second, they mix personal and business use without any method for separating the business portion. That's where deductions become vulnerable.

A streaming subscription used mostly for personal entertainment won't become deductible because it occasionally inspired work ideas. A phone bill may include business use, but if you haven't tracked or supported the business portion, the deduction becomes harder to defend. Good tax prep is conservative where the facts are weak and confident where the records are solid.

A better year-end review

Before finalizing deductions, review expenses through this lens:

| Question | Why it matters |

|---|---|

| Was the expense tied to running the business? | Business purpose drives deductibility |

| Do you have support for it? | Receipts and statements back up the claim |

| Was any part personal? | Mixed-use items need careful treatment |

| Is it categorized consistently? | Clean books lead to cleaner tax preparation |

Owners who do this well don't just reduce taxable income. They get clearer insight into how the business spends money.

Navigating Estimated Taxes and Critical Deadlines

A common sole proprietor scenario looks like this. Revenue was strong, the bank account never looked empty, and then tax season arrives with a balance due that feels far larger than expected. In my experience, that problem usually starts months earlier in the books, not on the tax return.

Estimated taxes matter because sole proprietors usually do not have taxes withheld from each payment they receive. The return is only the final calculation. The actual work happens during the year as income is recorded, expenses are categorized, accounts are reconciled, and profit is measured with enough accuracy to support quarterly payments.

The payment dates are straightforward. The harder part is paying from reliable numbers.

Estimated taxes start with reconciled books

Many guides jump straight to Form 1040-ES and due dates. That skips the step that determines whether the payment is even reasonable.

Before estimating taxes, reconcile the business bank account, credit cards, payment processors, and loan activity. Confirm that owner transfers are not sitting in expense categories. Make sure income is recorded once, not twice. Check that large purchases, reimbursements, and contractor payments are classified correctly. If those items are off, the tax estimate is off too.

That is why I tell clients to treat quarterly tax planning as a bookkeeping checkpoint. Clean records produce better estimates. Messy records produce surprise balances and preventable penalties.

A practical system that works

Set up a monthly routine:

- Reconcile all business accounts to statements

- Review net income, not just cash in the bank

- Move a set percentage of profit into a separate tax savings account

- Revisit the percentage if income rises, margins change, or deductions were lower than expected

That last point matters. A service business with steady margins can often use a simple reserve method. A business with uneven revenue, subcontractor labor, equipment purchases, or mixed personal transactions usually needs closer review.

If you hire freelancers, keep those records current during the year rather than trying to rebuild them in January. This guide to generating 1099s for contractors can help if your contractor reporting process still needs structure.

The deadline calendar to keep visible

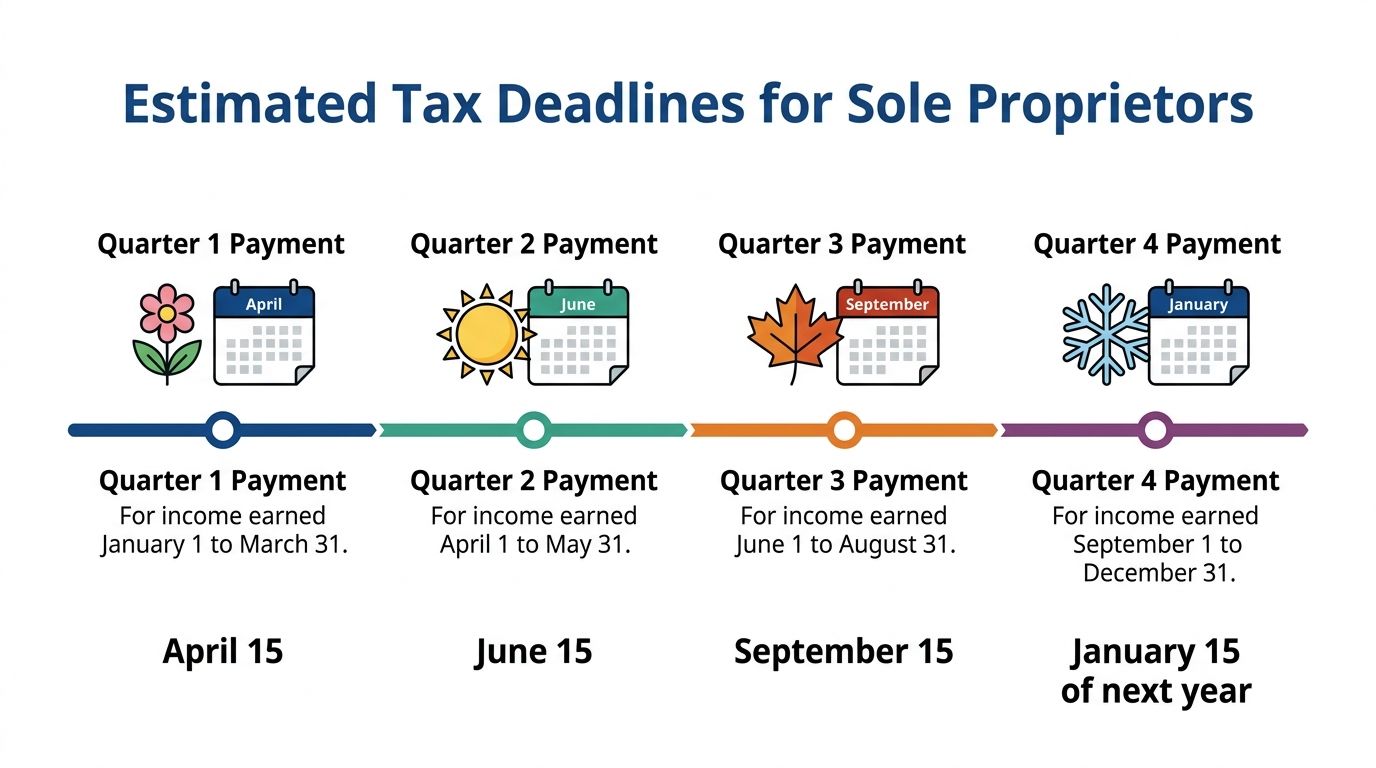

For most sole proprietors, estimated payments are generally due on:

- April 15

- June 15

- September 15

- January 15 of the following year

If a date falls on a weekend or holiday, the due date may shift to the next business day. Check the IRS instructions for the filing year before submitting payment.

For a quick overview of the estimated tax rhythm, this video gives a useful visual explanation:

What missed deadlines usually signal

A missed estimated payment is rarely just a calendar problem. It often points to one of three issues. The books are not current, the owner is using gross deposits instead of actual profit, or cash reserves were never separated from operating funds.

Those problems can usually be fixed, but they get more expensive as the year goes on. Catch-up payments strain cash flow. Late bookkeeping forces rushed decisions. A year-end scramble also makes it harder to spot issues like unrecorded income, duplicate expenses, or missing contractor reporting.

Some owners can manage this process themselves once their bookkeeping routine is stable. Others are better served by periodic review from a professional, especially when income is volatile or cleanup is involved. If you want a broader view of the benefits of hiring a business accountant, that overview is a useful complement to the tax side of this decision.

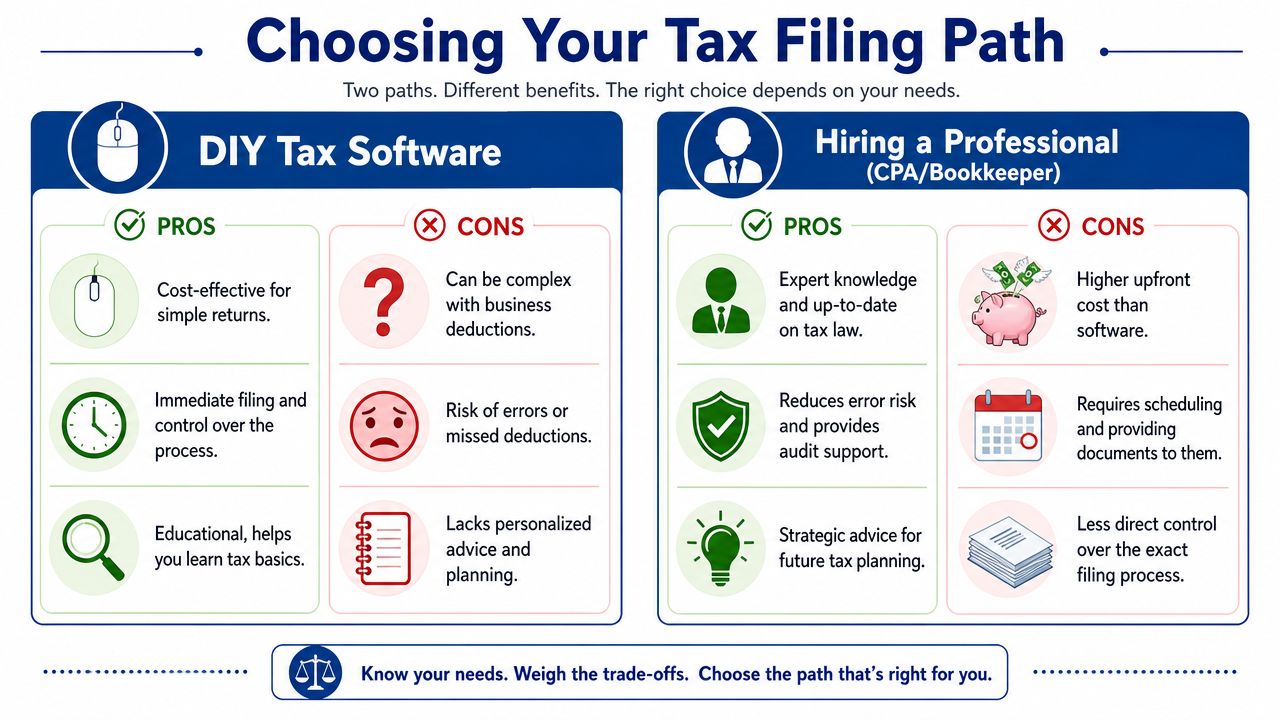

DIY Tax Software vs Hiring a CPA or Bookkeeper

At some point, every sole proprietor has to decide whether to file alone or bring in help. Both paths can work. The right choice depends less on personality and more on bookkeeping quality, business complexity, and your tolerance for cleanup work.

When DIY software makes sense

DIY software can be a reasonable choice when:

- Your books are already clean: Transactions are categorized, reconciled, and supported.

- Your income sources are simple: You're not sorting through multiple platforms, mixed deposits, or frequent reimbursements.

- Your deductions are straightforward: You know what belongs in the business and have records to support it.

- You want direct control: Some owners prefer entering and reviewing everything themselves.

In that situation, software can be efficient. It walks you through inputs, checks for obvious omissions, and gives you visibility into the return.

When professional support is worth it

A CPA or experienced bookkeeper earns their keep when the issue is judgment, cleanup, or structure.

That usually means:

| Situation | Why a professional helps |

|---|---|

| Mixed personal and business activity | Cleanup requires careful review and defensible classification |

| Multiple payment sources | Reconciliation is harder than form entry |

| Contractor payments or payroll issues | Compliance extends beyond the income tax return |

| Weak historical books | Corrections should happen before the return is prepared |

| Growth year | Better planning matters as much as filing |

A good professional doesn't just key in numbers. They pressure-test the books behind the numbers.

If you want a broader outside perspective on where professional support adds value, this overview of the benefits of hiring a business accountant is a useful read.

The real trade-off

The key comparison isn't software versus accountant. It's entry help versus judgment.

Software is good at prompting. It's less good at deciding whether a deposit was income, whether a payment belongs in contractor costs or another category, or whether your books are clean enough to trust. If the earlier parts of this article felt manageable, DIY may be fine. If the bookkeeping and reconciliation parts felt heavy, that's usually your answer.

A sole proprietor return is often simple after the books are right. Getting the books right is where experience pays off.

If your books are messy, your payments come from multiple sources, or you want a cleaner year-round system instead of another rushed tax season, Steingard Financial can help you turn raw transactions into accurate, tax-ready records. Their team supports service businesses with bookkeeping, reconciliations, payroll, reporting, and the kind of cleanup that makes filing easier and decisions better all year.