What Is Capital Outlay for a Service Business?

When you're running a business, money is always flowing in and out. But not all spending is created equal. Think of it this way: renting a car for a quick business trip is one thing. Buying a brand-new company vehicle is something else entirely. One is a short-term cost to get a job done; the other is a long-term investment in your business's future.

That big purchase—the company car—is what we call a capital outlay.

Understanding Capital Outlay in Your Business

A capital outlay, also known as a capital expenditure or CapEx, is a significant chunk of money you spend on a major asset that will benefit your business for more than one year. This isn't your everyday spending like utility bills, rent, or employee salaries. Those are the costs of keeping the lights on.

Instead, a capital outlay is a strategic purchase. It's the money you spend to buy, upgrade, or extend the life of major physical assets that will help you generate value for years to come. Getting this distinction right is crucial for your bookkeeping, your tax returns, and how you understand the overall financial health of your company.

A capital outlay fundamentally changes your financial landscape. It converts cash into a tangible asset on your balance sheet, increasing the company's net worth rather than simply reducing its profit for the month.

These aren't just small potatoes, either. Across the entire economy, these investments are massive. The U.S. Census Bureau reported that total capital expenditures for U.S. businesses hit an incredible $1,706.4 billion in 2020. That's a 37.3% jump from 2011. You can dig into more of this data on capital spending patterns on the Census Bureau's website. This just goes to show how vital these long-term investments are for growth.

For a service business owner, figuring out what counts as a capital outlay versus a regular operating expense is the first step to clean books and smart tax planning. Let’s look at the key differences side-by-side.

Capital Outlay vs Operating Expense At a Glance

This table breaks down the core differences between a capital outlay (CapEx) and an operating expense (OpEx). It’s a quick reference to help you categorize your spending correctly from the get-go.

| Attribute | Capital Outlay (CapEx) | Operating Expense (OpEx) |

|---|---|---|

| Time Horizon | Provides value for more than one year | Consumed within one year or less |

| Financial Impact | Becomes an asset on the balance sheet | Reduces profit on the income statement |

| Tax Treatment | Cost is spread out over years (depreciation) | Cost is fully deducted in the current year |

| Purpose | To acquire, upgrade, or extend asset life | To maintain day-to-day business operations |

As you can see, the main split comes down to time and financial impact. One is a long-term investment you own; the other is a short-term cost you use up. Understanding this will make your financial reports—and your life—much clearer.

Capital Outlay vs. Operating Expenses Explained

To really get a handle on your business's finances, you have to understand the difference between a capital outlay and an operating expense. This isn't just some boring accounting rule; it fundamentally changes how you report your finances, how much tax you pay, and how you see your company’s real value.

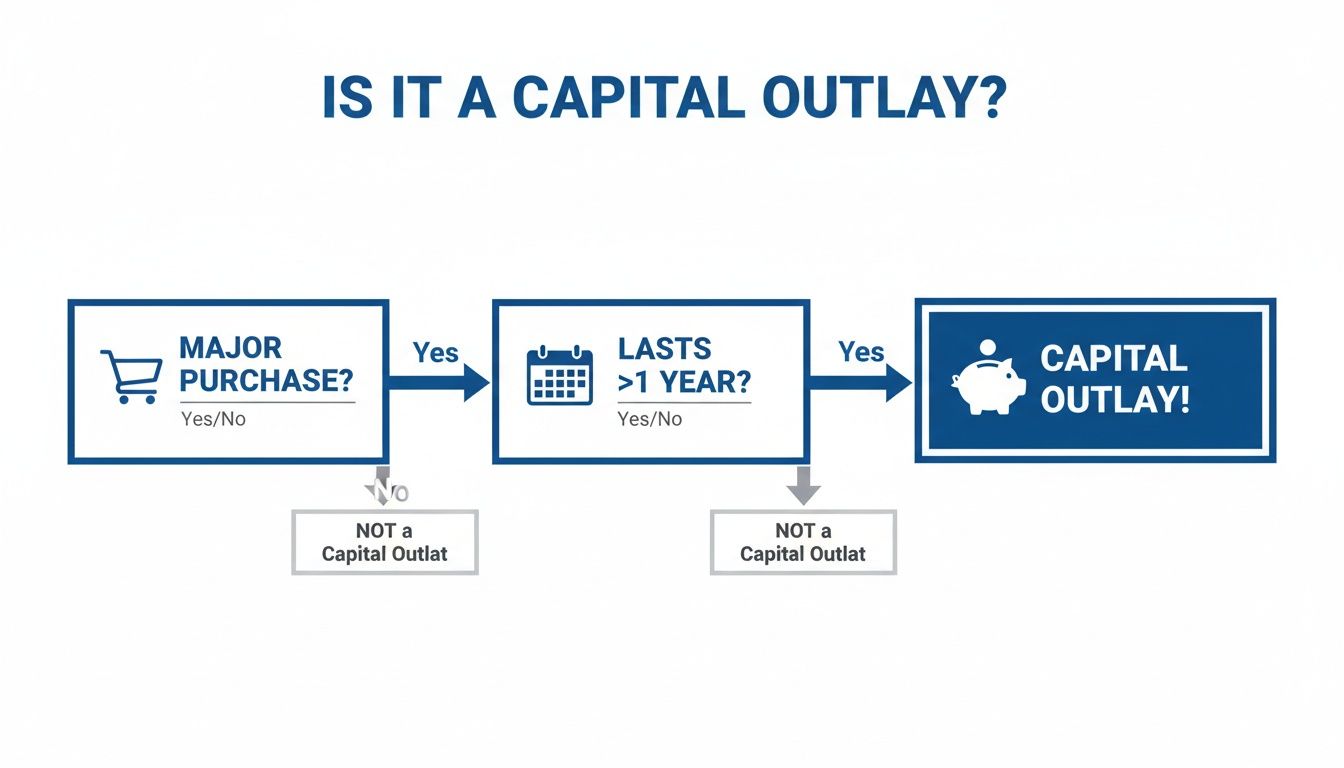

Think of it this way: Your marketing agency spends $10,000 on a powerful new server. That’s a capital outlay. That same month, you also pay the $200 subscription for your project management software. That's a classic operating expense (OpEx). Both are costs of doing business, but your accounting system treats them worlds apart.

This flowchart breaks down the basic decision process for how to classify your spending.

As you can see, the core idea is pretty simple. A capital outlay is a major purchase that provides value for a long time, not a small, everyday cost that gets used up quickly.

Financial Reporting: The Core Difference

That $10,000 server, your capital outlay, doesn't just vanish from your books or immediately tank your profits for the month. Instead, it’s recorded as a fixed asset on your balance sheet, which is the document that gives a snapshot of your company's net worth. It’s now a long-term resource you own.

On the other hand, the $200 software fee—your operating expense—goes straight to your income statement (often called a profit and loss or P&L). It directly reduces your revenue for that period, which in turn lowers your taxable profit right away.

A capital outlay converts cash into a long-term asset, increasing the value of your company. An operating expense is simply the cost of doing business, consumed in the short term.

This isn't a new concept. As businesses have evolved, the focus has shifted from pure expansion to maintaining and replacing the assets they already have. In fact, the ratio of capital consumption (using up assets) to gross capital formation (buying new ones) grew from about 40% in the early 20th century to over 75% after WWII. For today’s service businesses, this just goes to show that your capital outlay decisions are strategic choices that support the long-term health of your company. You can dig into the numbers yourself with this historical economic analysis from NBER.

The Capitalization Threshold: Your Internal Rule

So, how big does a purchase have to be to count as "major"? This is where you need a capitalization threshold.

A capitalization threshold is a dollar amount you set as your official company policy. Any purchase that costs more than this amount gets treated as a capital outlay. Anything below it is simply expensed, even if it’s an item that will last more than one year.

This isn't just a random number you pick out of a hat. It's a critical internal policy that keeps your financial reporting consistent and accurate. For most small businesses, a common threshold is somewhere between $500 to $2,500. The key is to set a policy and stick to it, which prevents confusion and ensures your financial statements are reliable from one year to the next.

How Capital Outlays Affect Your Taxes

So you’ve made a big investment in your business, like buying new equipment or a company vehicle. What happens next? More importantly, how does a capital outlay impact your tax bill at the end of the year?

The key to understanding this is a concept called depreciation. It’s one of the most important tax planning tools for any business owner.

Instead of writing off the entire cost of a major asset in the year you buy it, depreciation lets you spread that cost out over the asset’s “useful life.” This makes perfect sense, as the asset will be generating value for your business for several years, not just one.

By expensing a portion of the cost each year, you get to lower your taxable income, which reduces your tax liability over time.

Depreciation in Action

Let’s walk through a clear example. Imagine your video production company purchases a new high-end camera package for $10,000. The IRS generally views this type of equipment as having a useful life of five years.

Here's how that works out using a simple "straight-line" depreciation method:

- Total Cost: $10,000

- Useful Life: 5 years

- Annual Depreciation Expense: $2,000 ($10,000 / 5 years)

For the next five years, you can deduct $2,000 as a depreciation expense on your tax return. This lowers your taxable income by that amount each year, directly reducing how much tax you owe.

Strategic depreciation isn't just an accounting task; it's a tax planning tool. It systematically lowers your taxable income over time, directly impacting your company's cash flow and profitability.

Tax Incentives to Accelerate Deductions

Spreading out the deduction is good, but what if you could get a much bigger tax break right away? The good news is, you often can. The IRS offers powerful incentives that let businesses accelerate these deductions, which can provide a huge cash flow boost in the year you make the purchase.

Two of the most common incentives you'll hear about are:

- Section 179 Deduction: This fantastic rule lets you treat a capital outlay as a regular expense, allowing you to deduct the full purchase price of qualifying equipment in the year it’s placed into service (up to certain limits).

- Bonus Depreciation: This is another powerful tool that lets you deduct a large percentage of an asset's cost immediately—sometimes up to 100%, depending on the current tax law.

In the UK, a similar concept is prominent through reliefs such as proactively claiming the Annual Investment Allowance. These rules are powerful but can be complex and are subject to change, so staying on top of them is crucial.

Having a solid grasp of these options is a major part of how you can prepare for tax season without the stress. It’s always smart to consult with a tax professional to make sure you’re taking full advantage of every incentive available to your business.

Of course. Here is the rewritten section, tailored to the specified human writing style and formatting requirements.

Common Capital Outlay Examples for Service Firms

Theory is a good starting point, but seeing how capital outlay works in the real world is what truly makes the concept stick. For service-based businesses, capital outlays aren't about smokestacks or factory equipment. They're the key investments in the tools you need to deliver your expertise.

Understanding these examples will help you identify capital expenditures in your own business. This ensures they are recorded correctly from the very beginning, not as simple purchases, but as long-term assets that fuel your company’s growth.

Technology and Equipment Investments

For almost any modern service business, technology represents the biggest category of capital outlay. Think of these as the workhorses your team depends on every day to serve clients and produce quality results.

- High-Performance Computers and Workstations: When a design agency buys new Macs for its creative team or a software firm purchases powerful developer laptops, these are clear examples. The machines have a useful life well beyond a single year and are fundamental to delivering the service.

- Servers and Network Infrastructure: A tech consulting firm that invests in a new server rack or overhauls its network with new switches is making a major capital outlay. This infrastructure is the backbone of its entire operation.

- Specialized Professional Equipment: This could be a high-end camera and lighting setup for a video production company, professional podcasting microphones for a marketing agency, or specific diagnostic tools for an IT support firm.

A simple way to think about it is to ask: "Is this a major purchase that we will use for multiple years to generate revenue?" If the answer is yes, you are almost certainly looking at a capital outlay.

Property and Physical Space Upgrades

Even if your business rents its space, significant investments you make to your physical office can often be capitalized. These are expenditures that improve the long-term value and day-to-day function of your home base.

- Leasehold Improvements: These are major upgrades made to a rented space. Real-world examples include building out new internal offices, installing custom cabinetry, or completing a significant electrical or plumbing project. The cost is capitalized and then depreciated over its useful life or the remaining term of the lease, whichever is shorter.

- Office Furniture: Buying a full set of desks, chairs, and conference room tables for a new office is a capital expenditure. These are durable items that you expect to use for many years.

- Company Vehicles: For any service business that travels to client sites—like a managed IT service provider or an on-site consultant—purchasing a company car or van is a classic capital outlay.

Tracking Capital Outlays in Your Books

Okay, so you know what a capital outlay is and can spot one in your own business. That’s a great start. But the real work begins when you need to track these big investments in your accounting software.

This isn't just about punching in numbers. It’s about building a system that gives you—and anyone else looking at your books—a true, accurate picture of your company's financial strength and value.

Getting this right is absolutely critical for clean financial statements and a much less stressful tax season. It also sends a powerful signal to lenders and potential investors that you’re a serious operator who knows how to manage your assets for the long haul.

Setting Up Your Chart of Accounts

The entire foundation for tracking capital outlays is your Chart of Accounts (CoA). Think of this as the complete index for every dollar that moves through your business. To handle capital spending correctly, you can’t just throw a new computer purchase into a generic "office expense" bucket.

Instead, you need to set up dedicated Fixed Asset accounts. These accounts belong on your balance sheet, not your profit and loss statement, because they represent long-term value.

For example, you’ll want to create separate Fixed Asset accounts for different types of assets, like:

- Computer Equipment

- Office Furniture

- Company Vehicles

- Leasehold Improvements

Here is an example of what setting up asset accounts might look like within an accounting system like QuickBooks Online.

By creating these specific categories, you can see exactly where your big investment dollars are going and manage the depreciation for each asset class correctly. If you need a more detailed walkthrough, our guide on how to create a chart of accounts is the perfect next step.

The Journal Entry Process

With your CoA properly configured, the next step is recording the actual purchase. Let's say you buy a new server for $5,000. You aren't just "spending" that money; you are essentially swapping one asset (cash) for another (equipment).

The initial purchase of a capital asset is a balance sheet transaction. It shifts value from your cash account to a fixed asset account, with no immediate impact on your monthly profit and loss.

It's only later that your bookkeeper will make periodic entries to record depreciation. This is the process that moves a slice of the asset's value from the balance sheet to your income statement as a depreciation expense, which in turn reduces your taxable income for that period. Keeping a clean record of all your business expenses, including these major purchases, is vital. Using tools like a receipt maker app can help you digitize and organize all the necessary documentation.

Budgeting for Major Business Investments

Excellent financial management isn't just about looking back at what you’ve already spent. It's really about looking forward. This is where budgeting for your capital outlay, or CapEx, comes into play, shifting your business from being reactive to proactive. It's simply the process of planning for your company's future growth and big-ticket needs.

Think of a capital budget as more than just a wish list. It’s a concrete plan that anticipates your long-term asset purchases, whether that's replacing old computers or buying new equipment to launch a new service. This kind of planning makes sure you have the money set aside when you need it most.

Building Your CapEx Budget

Putting together a solid capital budget doesn't have to be complicated. It boils down to a few key steps and is often a team effort to match your financial reality with your business goals.

- Forecast Future Needs: Take a look at the assets you already have. When are those team laptops going to give out? Is your current server getting pushed to its limit? Getting ahead of these replacements keeps your operations running smoothly.

- Identify Growth Investments: What major purchases could really push your business forward? This might be new video gear to expand your marketing services or a company car to make client visits easier and more professional.

- Secure Executive Buy-In: When you present your budget, make a clear business case for it. Explain how each proposed capital outlay helps the company hit its goals, improves efficiency, or will eventually pay for itself.

A well-thought-out capital budget is more than a financial document—it’s a roadmap for where your company is headed. It shows lenders and investors that you’re serious about sustainable growth.

How Lenders and Investors View Capital Spending

The way you handle capital spending says a lot about your business. When lenders or potential investors look at your financials, they pay close attention to how you manage these large investments. Regular, planned capital spending shows them you're reinvesting in the business to stay sharp and competitive.

These purchases also show up on your financial statements. A new asset gets recorded on your balance sheet, which increases your company's total assets. The cash you spent appears on the statement of cash flows under "investing activities." To get a better handle on this, check out our guide on how to calculate capital spending. It will help you see exactly how your budget connects to your financial reports.

Frequently Asked Questions About Capital Outlay

Once you have a handle on the basics of capital outlay, a few common questions almost always come up. Here are some quick answers to the things business owners ask us most often.

What Is a Typical Capitalization Threshold?

There isn't a one-size-fits-all answer, but many small service businesses find a capitalization threshold between $500 and $2,500 works well. If an item costs less than your set amount, you just treat it as a regular expense, even if you’ll use it for more than a year.

The most important part is to create a formal, written capitalization policy and stick to it. Your bookkeeper or CPA is the best person to help you decide on the right threshold for your business size and industry.

Can I Claim a Tax Deduction in the Purchase Year?

Yes, in many cases, you can. While the standard accounting practice is to depreciate an asset over its useful life, the IRS offers some powerful tools to help businesses. The Section 179 deduction is a big one, allowing you to deduct the entire cost of qualifying equipment in the same year you buy it, up to a certain limit.

Bonus depreciation is another great option that can let you deduct a large chunk of an asset’s cost right away. This can be a huge boost to your cash flow. Just remember that tax laws change, so it's critical to talk to a tax professional to make sure you're following the current rules.

How Is a Leasehold Improvement Handled?

Leasehold improvements are a great example of a capital outlay that isn't always obvious. These are major upgrades you make to a space you rent, like:

- Building out new office walls

- Installing permanent lighting or shelving

- Upgrading the electrical or plumbing systems

Because you don't own the building itself, you capitalize the cost of the improvements and then depreciate them. The depreciation period is usually the shorter of the asset's useful life or whatever time is left on your lease. This is a tricky area, so it's vital to have your bookkeeper categorize these expenses correctly from the start.

At Steingard Financial, we help service businesses like yours master these concepts, ensuring your books are accurate and your financial strategy is sound. Let us build a dependable financial back office for your business. Visit us at https://www.steingardfinancial.com to get started.