How to Reconcile Bank Accounts the Right Way

At its core, bank reconciliation is simply the process of comparing your business’s financial records to your bank statements. It’s a methodical check to make sure the cash balance in your books lines up perfectly with what the bank says you have. This process helps you spot any differences and make the necessary adjustments, leaving you with a complete and accurate financial picture.

Why Bank Reconciliation Matters More Than You Think

Before we jump into the “how-to,” it’s worth taking a moment to understand why this process is so much more than just an administrative chore. Think of it less like homework and more like a regular financial health checkup for your business. Honestly, it’s the single most effective way to keep a tight grip on your cash flow and protect your company’s most important asset.

Without this crucial check, you’re essentially flying blind. It’s shocking how quickly small discrepancies can snowball into significant financial problems. A minor accounting error, an unnoticed bank fee, or a sneaky fraudulent charge can completely distort your financial reality, leading you to make bad business decisions based on faulty data.

Safeguarding Your Business Capital

Consistent reconciliation is your front line of defense against both innocent errors and outright fraud. It’s how you catch a duplicate charge from a vendor or an unauthorized subscription before they quietly drain your account for months. Spotting these issues early doesn’t just save you money; it protects the integrity of your entire financial history.

Regular reconciliation transforms your bookkeeping from a historical record into a proactive management tool. It provides the clarity needed to make confident, data-driven decisions that fuel sustainable growth.

This process ensures that every single dollar is accounted for. It acts as a verification system, confirming that the money you think you have is actually sitting in the bank. This level of accuracy is fundamental for everything from managing daily operations to planning your next big investment.

The Foundation of Smart Financial Decisions

Accurate financial data is the bedrock of any sound business strategy. When your books are precisely aligned with your bank statements, you get a crystal-clear view of your true financial position. This clarity empowers you to:

- Manage Cash Flow Effectively: You’ll know exactly how much working capital is available to cover payroll, pay suppliers, and jump on new opportunities.

- Improve Budgeting and Forecasting: You can base your financial plans on real, verified numbers instead of guesswork. This leads to much more realistic budgets and attainable financial goals.

- Simplify Tax Preparation: Clean, reconciled books make tax time significantly less stressful. Your accountant will have exactly what they need to file accurately and on time, minimizing any risk of audits.

Ultimately, learning how to reconcile your bank accounts is about changing your perspective. It’s not just about balancing the books; it’s about building an empowering financial habit. This discipline delivers the clarity and confidence you need to navigate challenges, seize opportunities, and steer your business toward a stable, profitable future.

Setting the Stage for a Smooth Reconciliation

A successful bank reconciliation isn’t about some complex accounting magic; it all comes down to good preparation. Think of it like a chef getting all their ingredients prepped and ready before they even start cooking. You need to gather your financial documents before you start crunching numbers.

This simple habit can turn a frustrating task into a smooth, predictable process. Taking a few minutes to get organized upfront saves you from stopping halfway through to hunt for a missing statement or transaction detail, which is exactly where most mistakes—and headaches—begin.

Gathering Your Core Financial Documents

To properly reconcile your bank accounts, you need a few key documents. Each one tells a piece of your financial story, and when you put them together, you get the complete picture needed for an accurate comparison.

Here’s what you’ll need to have handy:

- Bank and Credit Card Statements: These are the official records from your bank. They show every single deposit, withdrawal, interest payment, and fee that cleared during a specific period.

- Your General Ledger or Accounting Records: This is your business’s internal log of all financial transactions. It’s the story of your finances as you’ve recorded it in your accounting software or spreadsheet.

- Notes on Pending Transactions: Always keep a running list of any checks you’ve recently written that haven’t been cashed yet, or deposits that are still in transit. These are the most common culprits behind initial discrepancies.

You can grab PDF or CSV versions of your statements right from most online banking portals, which is a lot easier than dealing with paper copies. Having this information organized is a fundamental principle we talk about in our guides on bookkeeping basics for small business.

To make it even easier, here’s a quick checklist of the documents you’ll need and why they’re important.

Your Reconciliation Document Checklist

| Document | What It Is | Why You Need It |

|---|---|---|

| Bank/Credit Card Statements | The official monthly record from your financial institution. | This is your source of truth for all cleared transactions. |

| General Ledger/Accounting Records | Your internal business record of income and expenses. | This is what you’ll be comparing against the bank statement. |

| List of Outstanding Checks | Checks you’ve written that haven’t been cashed by the recipient. | These won’t appear on your bank statement yet, but they’re in your books. |

| List of Deposits in Transit | Deposits you’ve made that haven’t cleared the bank yet. | Like outstanding checks, these are in your records but not yet on the bank’s. |

| Previous Reconciliation Report | The final report from your last reconciliation period. | This provides the correct starting balance for the current period. |

Having these items ready to go before you start is the single best way to ensure a quick and accurate reconciliation.

Choosing Your Cut-Off Date

Before you dive in, you have to set a consistent reconciliation period. For 99% of businesses, the best practice is to reconcile monthly. This lines up perfectly with your bank statement cycle and helps you build a manageable, repeatable routine.

Your cut-off date is simply the last day of the period you’re reconciling—for example, January 31st or February 28th. Every transaction you compare must fall within this specific timeframe (e.g., from January 1st to January 31st). Sticking to a strict cut-off date is non-negotiable; it prevents confusion from transactions that happen right at the beginning or end of the month.

The goal is to create a snapshot in time. By defining a clear start and end date, you ensure you are comparing the exact same period in your books and the bank’s records, eliminating a major variable.

This routine is more critical than ever. The average online business now uses more than seven different payment platforms, and each one creates its own stream of data that has to be verified. This fragmentation makes manual reconciliation a real challenge, underscoring the need for an organized approach.

Finally, put it on the calendar. Pick a recurring day—the second Tuesday of every month, the first Friday, whatever works for you—and stick to it. Consistency is king. Building this habit is the most effective step you can take to make your reconciliation process faster, more accurate, and a whole lot less stressful.

Navigating the Manual Reconciliation Process

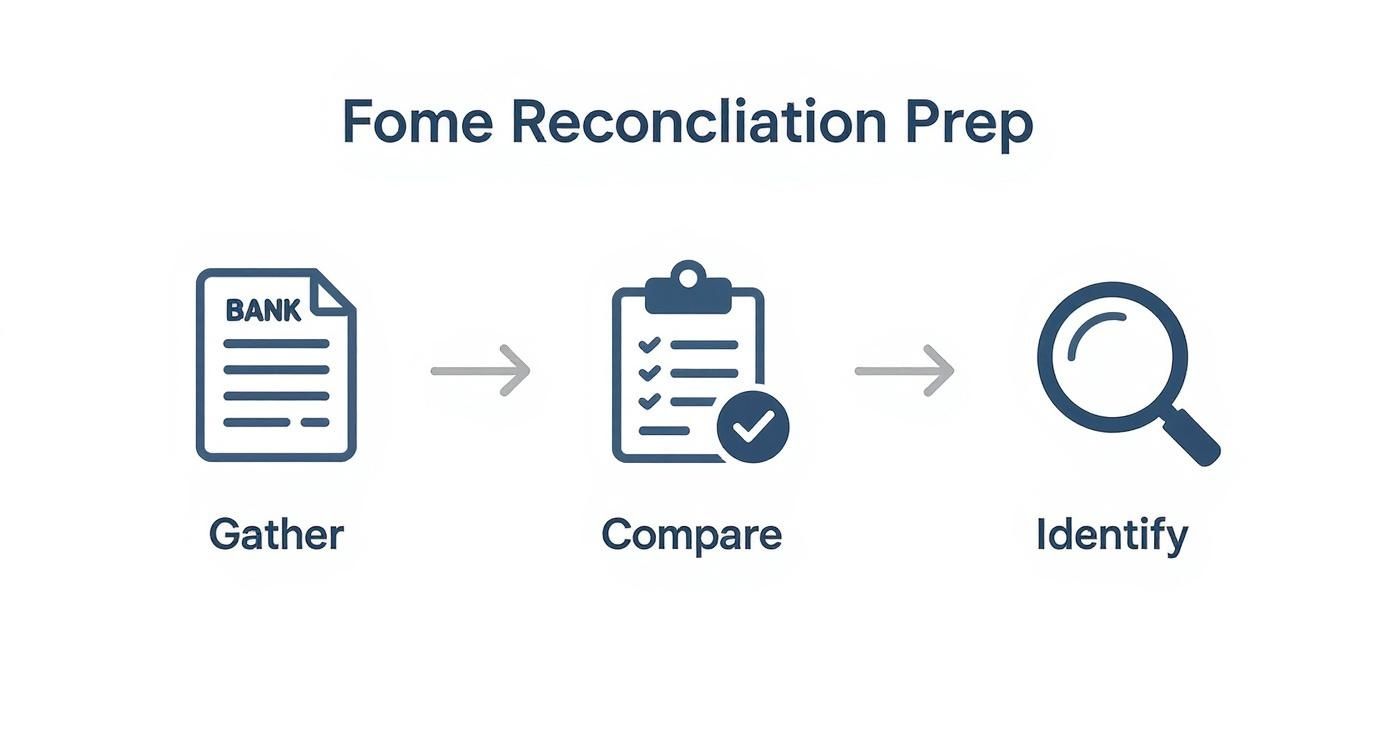

With your documents in hand, it’s time to roll up your sleeves and get into the actual reconciliation. This is where you put on your detective hat, comparing what you have in your books against what the bank says happened. It might seem daunting at first, but if you break it down into smaller, logical steps, it’s completely manageable.

Think of it like solving a puzzle. You have two different versions of your business’s financial story: your internal records and the bank statement. Your goal is to make sure those two stories line up perfectly. We’ll start with all the money that came in and then tackle all the money that went out.

This simple infographic below breaks down the flow: gather your data, compare it, and then zero in on any differences.

Seeing it visually helps reinforce that this isn’t one huge task. It’s a progression—a series of checks and balances that leads to a perfectly balanced account.

Matching Deposits and Incoming Funds

The easiest place to start is with your income. Go through your bank statement line by line, looking at every deposit, wire transfer, or electronic payment that hit your account during the statement period.

As you find each one, check it off against the matching income entry in your accounting software or ledger. For instance, if your books show a payment from “Client A” for $1,500 on March 28th, you’ll scan your bank statement for that exact amount around that date. Find it? Great. Check them both off and move on.

Of course, it’s not always that simple. Sometimes the bank might lump two smaller payments into one deposit, or a payment processor like Stripe might have taken a small fee before sending the money. These are the little mysteries you’ll need to solve.

Handling Deposits in Transit

One of the most common reasons your books don’t match the bank statement right away is because of deposits in transit. These are simply payments you’ve already recorded in your books, but they hadn’t actually cleared the bank by the statement’s cut-off date.

Imagine you deposited a client’s check for $2,500 on May 31st, the last day of the month. You did the right thing and logged it in your books that day. But the bank statement for May ends on the 31st, and that check didn’t officially post to your account until June 1st.

Here’s how that plays out:

- Your books for May will show that $2,500 income.

- Your May bank statement will not show that deposit.

This isn’t a mistake; it’s just a timing difference. During your reconciliation, you won’t check this item off. Instead, you’ll note it as a “reconciling item”—a deposit in transit—that explains part of the difference. It should then appear on next month’s statement, where you can finally reconcile it.

Comparing Withdrawals and Outgoing Payments

Next up, you’ll repeat the exact same process for all the money leaving your account. This includes every check you wrote, debit card purchase, automatic bill payment, and ATM withdrawal. Go through each withdrawal on your bank statement and find its matching expense entry in your ledger.

A classic trip-up here is forgetting to record the small, on-the-go purchases. That $5.75 coffee you bought for a client meeting with your debit card? It’s easy to forget, but it will be on your bank statement and needs to be accounted for in your books.

The entire point of reconciling is to confirm your internal records are accurate by matching them against an external, third-party source (the bank). This simple process is your best defense against errors, helps spot potential fraud, and gives you financial data you can actually trust.

This careful checking process makes sure every single expense is captured, which is crucial for knowing your true profit and loss—and for maximizing your tax deductions.

Identifying Outstanding Checks

Just like deposits in transit, outstanding checks are a primary reason for discrepancies. An outstanding check is one you’ve written and recorded as an expense, but the person or company you paid hasn’t cashed or deposited it yet.

Let’s say on April 20th, you wrote check #1045 to your office supply vendor for $350. You recorded it in your books right away. But the vendor was busy and didn’t deposit that check until May 5th.

When you reconcile your April bank statement:

- Your books will show the $350 expense, and your cash balance will be lower because of it.

- Your April bank statement will have no record of this transaction because the check hadn’t cleared.

This is an “outstanding” check. You’ll list it as another reconciling item to explain the difference. When it finally appears on your May statement, you can check it off as cleared.

Adjusting for Bank Fees and Interest

Finally, you have to account for transactions the bank initiated. These are items that will appear on your bank statement but probably aren’t in your books yet because you didn’t know about them until now.

These usually include things like:

- Monthly service fees: The standard fee your bank charges to maintain the account.

- Interest earned: If you have an interest-bearing account, this is income you need to record.

- Transaction fees: Charges for things like wire transfers or overdrafts.

These aren’t errors. You just need to add them to your general ledger to make your records whole. If the bank charged a $15 service fee, you’ll create a new expense entry for it. If you earned $2.50 in interest, you’ll add that as an income entry. Once they’re recorded in your books, you can check them off as reconciled.

Automating Reconciliation with QuickBooks Online

After walking through the manual steps, you can probably appreciate how tedious and detail-oriented the process is. While understanding the fundamentals is crucial, modern accounting software has completely changed the game, turning this monthly headache into a much faster, more accurate task.

Platforms like QuickBooks Online don’t just put the process on a screen; they actively automate huge chunks of it. This saves you hours of mind-numbing data entry and cross-referencing, freeing you up to focus on what the numbers actually mean for your business strategy.

The Power of Bank Feeds

The secret sauce behind this automation is a feature called bank feeds. This is simply a secure, direct link between your business bank and credit card accounts and your QuickBooks file. Once you set it up, the software pulls in all your cleared transactions automatically, every single day.

This direct connection is a game-changer. It completely eliminates the need to manually type in every debit card swipe, deposit, or wire transfer from a paper statement. More importantly, it slashes the risk of human error—no more typos or missed transactions throwing off your numbers.

The demand for this kind of efficiency is massive. The fintech industry, which builds these tools, is projected to skyrocket from USD 218.8 billion in 2024 to USD 828.4 billion by 2033. This growth is all about businesses needing faster, more accurate ways to handle core financial tasks like reconciliation. You can read more about the future of financial technology and its impact on business.

Navigating the QuickBooks Reconciliation Module

Inside QuickBooks, the reconciliation tool is an interactive screen that makes the matching process incredibly straightforward. Forget ticking off items on a spreadsheet. Instead, you see two neat columns: one with transactions pulled from your bank feed, and the other with the transactions you’ve already recorded in your books.

Your main job becomes confirming the matches that QuickBooks suggests. The software is smart—it uses dates, amounts, and vendor names to propose likely pairs, which you can often approve with a single click.

Here’s what that reconciliation screen looks like in QuickBooks Online, where you’re comparing your books to the bank statement. The real magic is the “Difference” amount at the top right. QuickBooks updates this number in real-time as you check off items, guiding you toward that perfect zero balance.

For any transactions the software can’t automatically match, you can quickly find and link them yourself. You can also handle new items right from this screen. For example, if a monthly bank fee shows up in your feed but isn’t in your books yet, you can add and categorize it as an expense on the spot. No need to jump to another part of the program.

Using a tool like QuickBooks doesn’t just make reconciliation faster; it makes it a continuous process. By reviewing and categorizing transactions from your bank feed weekly, your month-end reconciliation can take minutes instead of hours.

Streamlining the Workflow Step by Step

Even though the software does the heavy lifting, your expertise is still needed. You’re the one reviewing its work, making sure everything is categorized correctly based on your knowledge of the business.

Here’s how the automated process generally plays out:

- Connect Your Accounts: First, you’ll securely link your bank and credit card accounts to QuickBooks using the bank feeds feature.

- Enter Statement Info: When you’re ready to reconcile, you’ll kick things off by entering the ending date and ending balance directly from your bank statement.

- Review Matches: Go through the transaction list. QuickBooks will have pre-matched most of them for you. Your job is to give them a quick once-over for accuracy.

- Handle Unmatched Items: For anything left over, you can manually match them or create new entries. This is where you’ll typically account for things like bank fees or interest earned.

- Identify Discrepancies: The software keeps a running total. If the difference isn’t zero, QuickBooks helps you pinpoint the problem so you can track it down more easily.

- Finalize and Report: Once you hit a zero difference, you finalize the reconciliation. QuickBooks then saves a detailed report, which becomes a permanent and crucial part of your financial records and audit trail.

This structured workflow takes the guesswork out of the equation and creates a system that ensures no transaction gets missed. By leaning on technology, you turn reconciliation from a backward-looking chore into a proactive, real-time financial habit that gives you the confidence to run your business on accurate, timely data.

Solving Common Reconciliation Headaches

Even with the slickest system, you’re going to hit a snag during reconciliation sooner or later. It happens to everyone. The secret isn’t avoiding problems, but knowing exactly how to troubleshoot them when they pop up.

Think of yourself as a detective. You’re hunting for that one clue—the one missing transaction or incorrect number—that’s throwing everything off balance. Most of the time, the culprit is something small and simple to fix once you know where to look.

Let’s walk through the most frequent reconciliation headaches and give you a clear plan of attack for each. This will help turn those moments of frustration into opportunities to sharpen your bookkeeping skills.

When Your Opening Balance Is Off

This is one of the most jarring issues. You sit down to start reconciling, and the opening balance in your books doesn’t match the opening balance on your bank statement. It stops you dead in your tracks.

Whatever you do, don’t start matching transactions until this is fixed. An incorrect opening balance is a guarantee that your reconciliation will fail. This error almost always points back to a problem with the previous month’s reconciliation.

Here’s how to hunt down the problem:

- Pull last month’s report: Find the reconciliation report from the prior period. First, confirm it was actually finalized with a zero difference.

- Look for forced adjustments: Check to see if anyone made a “plague entry” or forced an adjustment just to make the last reconciliation balance. This shortcut is a ticking time bomb for future reconciliations.

- Hunt for edited transactions: The most likely culprit is a transaction from a previous, already-reconciled period that was changed or deleted after the fact. Someone might have voided a check or changed an invoice date, which retroactively messes up that month’s closing balance.

Most good accounting software has a report that shows transactions changed after a reconciliation was completed. This is your best tool for finding the specific entry that was altered so you can correct it.

The Transposed or “Fat Finger” Error

This is an incredibly common—and often maddening—human error. You meant to enter $82.50 for office supplies, but your fingers typed $28.50. Or maybe you keyed in $500 when it should have been $50.00.

These “fat finger” mistakes create a discrepancy that can be surprisingly hard to spot. Luckily, there’s a neat math trick to help you out.

If your reconciliation difference is perfectly divisible by 9, you almost certainly have a transposed number somewhere. For example, the difference between $82.50 and $28.50 is $54, and $54 divided by 9 is 6. This is a huge clue that you should be looking for a typo.

To find it, scan your transactions for amounts that look similar to your discrepancy. Another tip: if the difference is exactly half of a specific transaction amount, you might have entered a debit as a credit (or vice versa). Fixing these issues is a fundamental part of keeping your books clean, which is essential for creating an accurate trial balance format for your financial reports.

Finding Transactions in the Wrong Month

Another classic mix-up is a transaction recorded in the wrong accounting period. For instance, you get a vendor invoice dated May 31st, but the payment doesn’t actually clear your bank account until June 2nd.

If you recorded that payment in your books in May, but the bank shows it clearing in June, your May reconciliation will never balance. This isn’t really an “error” but a timing difference that needs to be handled the right way.

- For expenses: A check you wrote in May that doesn’t clear until June should be listed as an outstanding check on your May reconciliation report.

- For income: A deposit you recorded on May 31st that doesn’t post until June 1st is called a deposit in transit.

Both are legitimate reconciling items that explain why your books don’t perfectly match the bank statement on a specific day. The key is to make sure you aren’t missing them or double-counting them. The transaction should only be marked as “cleared” in the month it actually shows up on the bank statement.

The Dreaded Duplicate Entry

Finally, a duplicate entry can throw a big wrench in the works. This happens when the same transaction gets recorded twice in your accounting software by mistake. For example, you might manually enter an expense and completely forget that your bank feed is also set to import it automatically.

This creates an extra transaction in your books that simply doesn’t exist at the bank. The fix here is thankfully simple: once you’ve confirmed it’s a true duplicate, just delete one of the entries. Your books will snap back into alignment with the bank statement, and you can get back to your reconciliation.

Knowing When to Call in a Professional

For a lot of business owners, doing the books yourself starts as a point of pride. But as your business grows, that once-manageable task can turn into a serious time sink. Recognizing when DIY bookkeeping just isn’t cutting it anymore is a smart business move, not a sign you’ve failed.

If you’re spending more hours chasing down tiny discrepancies than you are serving your clients, that’s a pretty clear signal. Other red flags? Maybe your transactions are getting more complex with multiple currencies or payment gateways. Or maybe you just feel like you’re constantly a month behind on reconciliations. This isn’t just about getting a few hours back; it’s about stopping costly mistakes and avoiding burnout.

Gaining a Strategic Financial Partner

Outsourcing your bookkeeping isn’t about losing control. It’s about bringing on an expert who can deliver a level of accuracy and insight that’s tough to achieve on your own. Professional bookkeepers live and breathe the details, making sure every transaction is categorized correctly and your financial reports are flawless.

This kind of expertise is critical as finance gets more complex. The banking industry, for example, is a leader in using reconciliation software to improve accuracy and catch fraud. These automated systems can reduce manual reconciliation time by up to 80% and boost fraud detection by 60%—a testament to what specialized knowledge and tools can do. You can read the full market analysis on reconciliation software to see just how powerful these systems are.

A professional bookkeeper does a lot more than just reconcile your bank statements. They give you the confidence that comes from knowing your financial data is accurate, compliant, and ready to back up your next big business decision.

Ultimately, making the switch is an investment in your company’s future. It frees you up to concentrate on growth, innovation, and your customers—the things that really move the needle. To see what this looks like in the real world, check out our guide on how to outsource bookkeeping for your small business.

Answering Common Bank Reconciliation Questions

Even with a clear process, a few questions always seem to pop up. Here are some quick answers to the most common things business owners ask when they’re getting the hang of reconciliation.

How Often Should I Reconcile My Bank Accounts?

For just about every business out there, reconciling monthly is the gold standard. This timing lines up perfectly with your monthly bank statements.

Doing it once a month creates a consistent, manageable rhythm for your financial check-ins. It’s frequent enough to catch errors or potential fraud quickly but not so often that it becomes overwhelming.

Can I Reconcile My Business Credit Cards Too?

Absolutely. In fact, you really should. The great news is that the process is nearly identical to reconciling a bank account.

You’ll just be comparing your credit card statement against the expenses you’ve logged in your books. This is a critical step for accurately tracking all your business expenses, managing what you owe, and making sure every single charge is legitimate.

What if My Reconciliation Difference Is Not Zero?

A perfect reconciliation always ends with a zero difference. If yours doesn’t, that’s a clear signal that something is off and needs a second look.

Whatever you do, don’t force it to balance. The best move is to backtrack and hunt for the usual suspects: transposed numbers, a bank fee you forgot to record, or maybe some outstanding checks that haven’t cleared yet.

Feeling overwhelmed by the details? The expert team at Steingard Financial can handle your bank reconciliations, payroll, and bookkeeping with precision, giving you back your time and providing the financial clarity you need to grow. Get in touch with us today at https://www.steingardfinancial.com.