You buy a new service van, a set of specialized diagnostic tools, or upgraded workstations for your team. The cash leaves your bank account today, but the equipment will help you earn revenue for years. That gap is where many owners get tripped up.

If you record the whole purchase as a regular expense right away, your profit can look unusually low in the month you bought it and oddly high later. That can distort pricing decisions, technician productivity reviews, and even how confident you feel about hiring or replacing equipment.

Depreciation for equipment solves that problem. It spreads the cost of a long-term asset over the period you expect to use it, so your books tell a more realistic story about what it takes to run the business.

Your New Equipment Is an Asset Not Just an Expense

A lot of service business owners see a major purchase and think in cash terms first. That makes sense. You wrote the check, financed the asset, or put it on a card. But accounting asks a different question: Will this item help the business for more than one year?

If the answer is yes, the equipment is usually treated as a capital asset rather than an immediate expense. In the United States, equipment is typically recovered through depreciation instead of being deducted all at once, according to IRS depreciation guidance.

That matters because a fleet vehicle, a dental imaging device, a contractor's testing instrument, or a bank of design computers doesn't just support one month of revenue. It supports many future months.

Why owners misread this at first

The confusion usually starts with a simple thought: “I paid for it now, so I should expense it now.”

That's a cash mindset, not an accrual accounting mindset. For decision-making, you want your profit and loss statement to reflect the cost of using the asset over time, not just the day you purchased it. If you're trying to sharpen your process around accounting for fixed assets, it helps to think of equipment as part of a long-term asset system rather than a one-time bill.

A related concept is capital spending itself. If you want a clean primer on what belongs in that category, this overview of capital outlay gives useful context.

Practical rule: If an item will serve the business beyond the current year, don't treat the bookkeeping casually. The purchase decision and the accounting treatment need to line up.

Why this matters in a service business

Manufacturers often think about depreciation in terms of plant machinery. Service businesses need a more practical lens.

Your equipment might include:

- Client-facing technology like high-end computers for architects, engineers, designers, or media teams

- Mobile operations assets such as vans, trucks, and other service fleet vehicles

- Field tools like diagnostic devices, calibration tools, scanners, and specialized repair equipment

- Office and support equipment that helps your team deliver work consistently

When those purchases are handled correctly, your monthly margins look more stable, replacement planning gets easier, and your tax reporting has a stronger foundation.

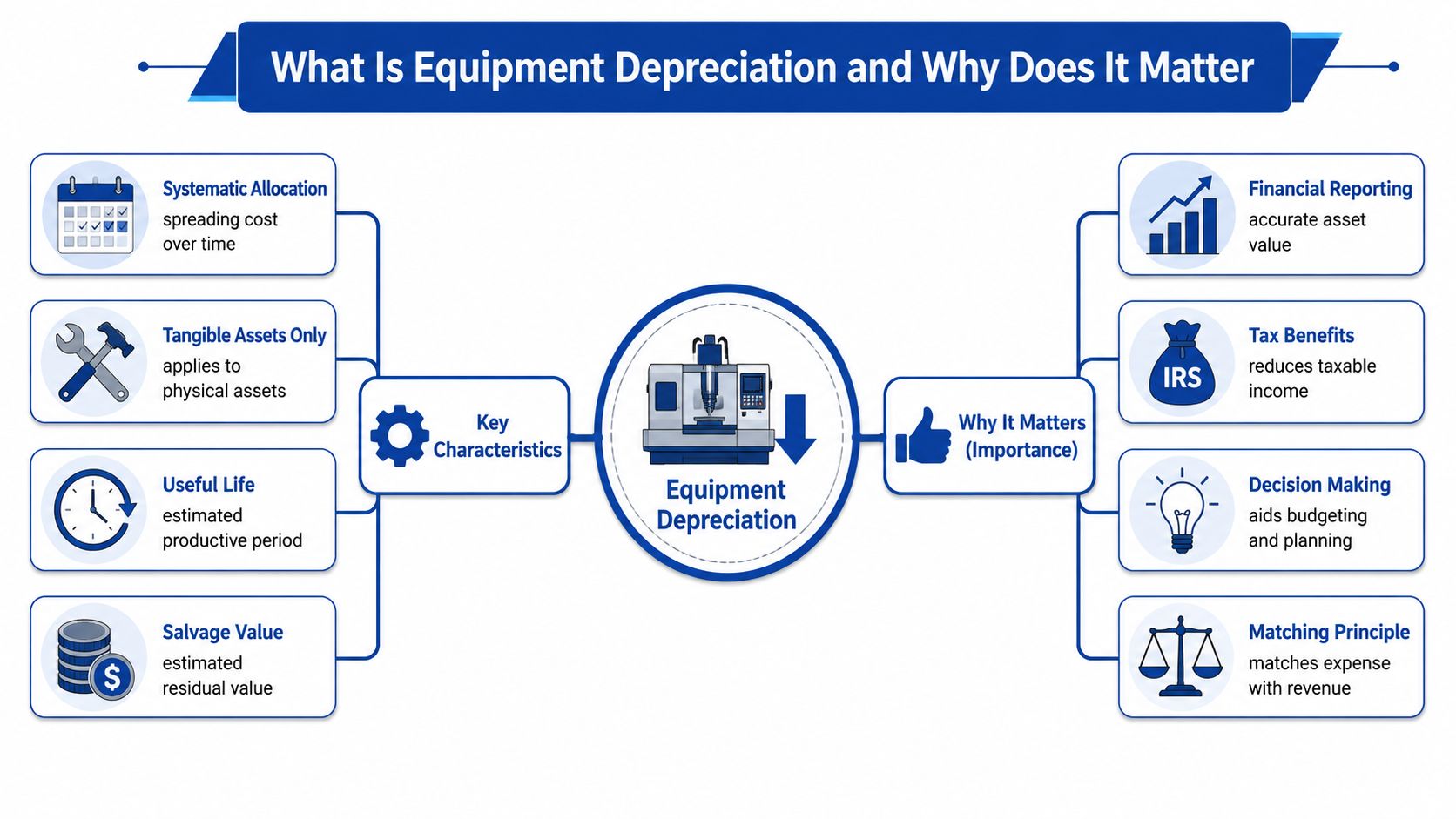

What Is Equipment Depreciation and Why Does It Matter

Think about a new car. The day you drive it off the lot, it hasn't stopped working, but part of its value has already been used up. Equipment works in a similar way. Depreciation is the accounting process of allocating an asset's cost over its useful life.

For tax and bookkeeping purposes, equipment depreciation is generally only allowed when the asset is owned by the business, used in an income-producing activity, has a determinable useful life, and is expected to last more than one year, as explained in this tax depreciation overview.

The three building blocks owners should know

You don't need to become a tax technician to understand depreciation. But you do need to know the inputs that drive it.

- Cost or basis means what the asset cost the business to put into service.

- Useful life is the period over which the asset is expected to provide value.

- Salvage value is what you expect the asset to be worth at the end of that useful life.

If you skip one of those ideas, the whole topic gets fuzzy fast.

A simple example

Under the straight-line method, annual depreciation equals (initial cost minus salvage value) divided by useful life. One example shows a $10,000 asset with a $3,000 salvage value and a 5-year life depreciating by $1,400 per year, or 14% of original cost annually, based on this equipment depreciation method example.

That example is simple, but the lesson is bigger. You're not saying the market would buy the asset for exactly that amount each year. You're creating a rational schedule for recognizing cost.

Depreciation doesn't track cash leaving the bank. It tracks the cost of using long-term equipment to generate revenue over time.

Why business owners should care

Depreciation affects more than compliance. It affects how you interpret your numbers.

Here's where it shows up in real life:

- Profit reporting: Your income statement includes depreciation expense, which lowers reported profit for the period.

- Balance sheet accuracy: The asset stays on the books, while accumulated depreciation reduces its book value over time.

- Replacement planning: If your tools, computers, or fleet age faster than you expected, your depreciation schedule highlights that issue.

- Cash planning: Profit and cash are not the same thing. If that distinction gets blurry, these profit vs cash flow insights are worth reviewing.

Service businesses often focus on utilization, labor efficiency, and job profitability. That's good. But if equipment costs aren't recognized properly, those KPIs can look cleaner than they really are.

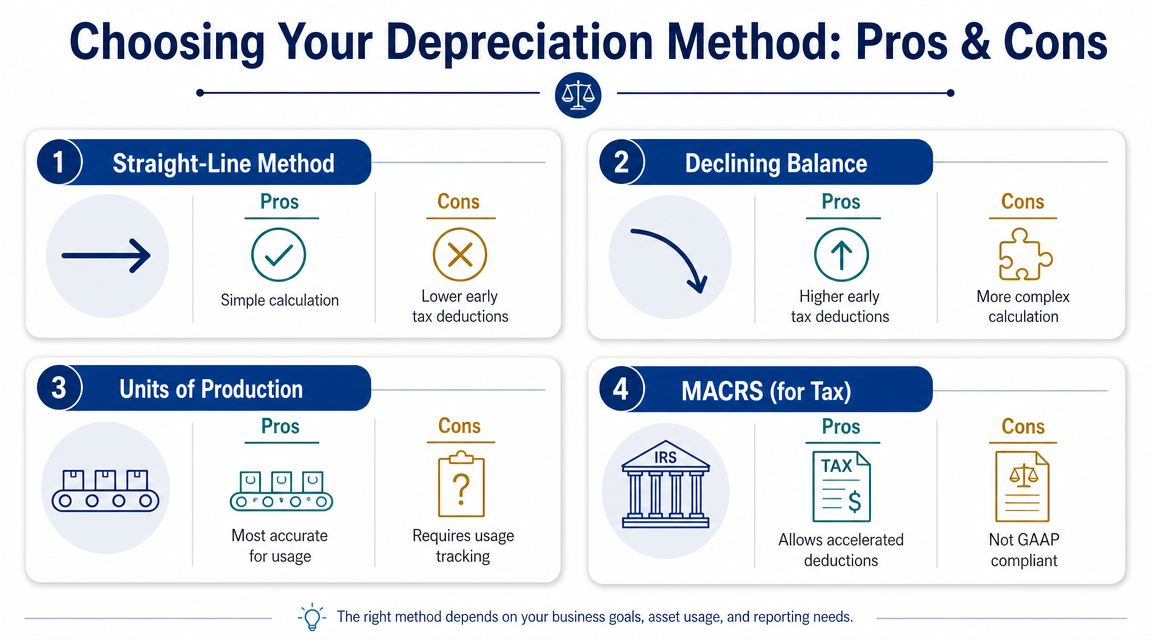

Comparing Common Depreciation Methods

A plumbing company buys three assets in the same quarter: a service van, a set of drain inspection cameras, and new laptops for dispatch and estimating. Putting all three on one depreciation method may be simple, but it can blur what is happening in the business. Each asset loses usefulness in a different way, and the method you choose changes the timing of expense on your books.

That matters because service businesses usually watch monthly profit, job margins, utilization, and replacement timing. If depreciation does not match how equipment is used, those KPIs can give you the wrong signal.

Side by side comparison

| Method | Expense Pattern | Best For |

|---|---|---|

| Straight-Line | Even expense over the asset's useful life | Assets with steady value consumption, like office equipment or general-purpose tools |

| Double-Declining Balance | Higher expense earlier, lower expense later | Assets that lose usefulness faster in the early years, like some technology |

| Units of Production | Expense rises and falls with output or usage | Usage-sensitive equipment, such as tools tied closely to jobs completed or hours used |

Straight-line gives you a steady baseline

Straight-line works like dividing the cost of an asset into equal slices over its useful life. The IRS describes straight-line as a method that deducts the same amount each year over the recovery period in Publication 946.

That consistency is useful for service businesses that want cleaner month-to-month reporting. If your admin team, estimators, or field managers rely on monthly P&Ls, straight-line keeps depreciation from swinging just because the method is front-loaded.

It often fits assets such as:

- Back-office computers used steadily across scheduling, billing, and customer communication

- Office furniture and fixtures that support operations over time

- General-purpose tools that do not lose most of their value early

For decision-making, the benefit is simple. Your reported margins are easier to compare across periods.

Double-declining balance recognizes heavier early-year loss

Some equipment gives you the most value up front. High-end laptops, tablets used by field teams, and certain diagnostic electronics can become outdated well before they stop working. In those cases, an accelerated method can match economic reality better than an even annual charge.

The Financial Accounting Standards Board defines declining-balance methods as accelerated approaches that produce higher depreciation in earlier years and lower amounts later, as described in the FASB Master Glossary entry for depreciation methods.

A car is a useful comparison here. It usually loses more value in the first years than in the last years. Technology often behaves the same way in a service business. A four-year-old workstation may still turn on every morning, but if it slows estimating, dispatch, design work, or reporting, its business value has dropped faster than a straight-line schedule suggests.

This method can be helpful when you want your books to reflect that front-loaded loss of usefulness. It can also make early-period job or department profitability look lower, which is not bad if it is more accurate.

Units of production ties expense to actual use

Some assets wear out because your team uses them, not because the calendar changed. A sewer camera pushed through hundreds of inspections or a floor-cleaning machine used on nonstop commercial jobs does not age the same way as a desk in the office.

Units of production addresses that problem by linking depreciation to output, mileage, hours, or another usage measure. The Corporate Finance Institute explains that this method is based on actual use rather than time in its overview of units of production depreciation.

For service businesses, that can make job costing more meaningful. If a piece of equipment is heavily used during peak months, more of its cost shows up in those periods. If usage drops, depreciation drops too.

The catch is recordkeeping.

You need dependable usage data, such as machine hours, miles driven, or jobs completed. Without that discipline, the method can create noise instead of clarity.

The best method depends on how the asset helps you earn revenue

Here is the practical test a busy owner can use:

- Choose straight-line when the asset supports the business evenly over time.

- Choose double-declining balance when the asset delivers more value in the early years or becomes obsolete quickly.

- Choose units of production when wear closely follows usage, not time.

The goal is not to find the fanciest method. The goal is to match expense recognition to how the asset contributes to revenue, so your financials support better pricing, replacement, and profitability decisions.

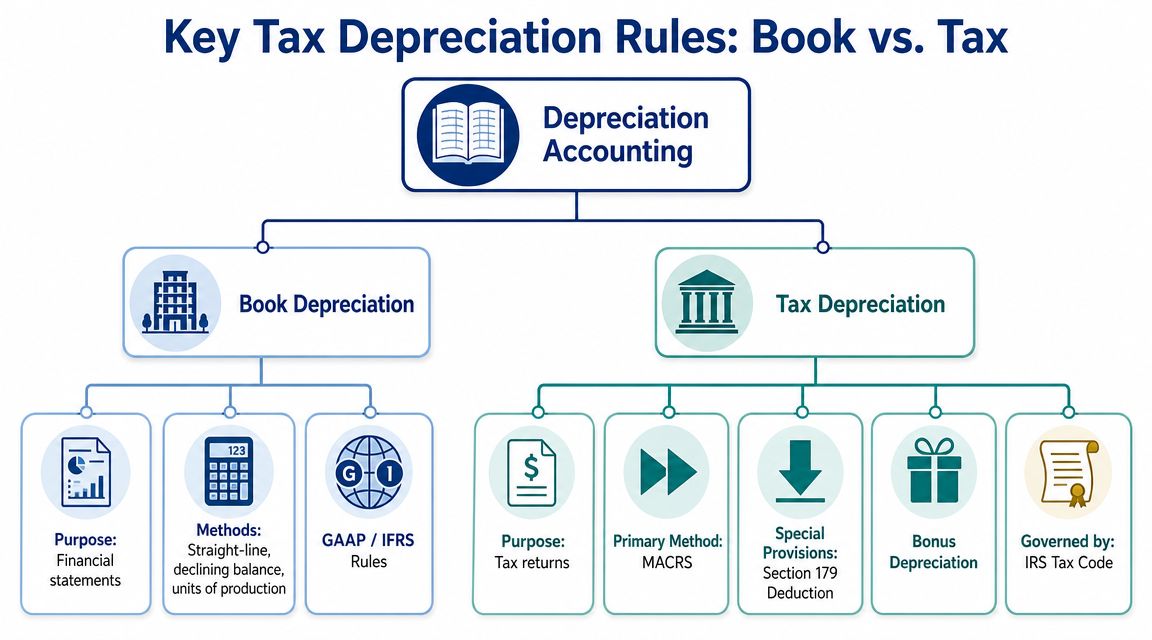

Understanding Key Tax Depreciation Rules

You buy six new laptops for your field team in December, add a diagnostic scanner for faster service calls, and put two vehicles into the fleet before year-end. The cash is gone immediately, but the tax deduction may not show up the way you expect. That surprise usually comes from one fact: book depreciation and tax depreciation follow different rules.

For your books, the goal is a useful picture of business performance. For taxes, the goal is to apply IRS rules correctly so your deduction timing is accurate. A service business needs both. If you rely only on the tax return, your profit trends, job pricing, and replacement planning can get distorted.

The four inputs tax depreciation needs

Tax depreciation starts with four basic pieces of information: basis, class life, placed-in-service date, and depreciation method.

Those terms sound technical, but each one answers a simple business question:

- Basis: How much cost are you recovering?

- Class life: Over how many years do tax rules say you recover it?

- Placed-in-service date: When was the asset ready and available for business use?

- Depreciation method: How is the deduction spread across those years?

A mistake in any one of those can throw off the full tax schedule.

For a service business, this is more than compliance. If your CPA is given the wrong in-service date for a service van, or the wrong cost basis for a high-end computer setup that included installation and required software, your first-year deduction can change. So can your estimated tax payments.

Why timing can change the first-year deduction

Timing rules often catch owners off guard. Tax depreciation does not always begin on the day you paid the invoice. It begins when the asset is ready and available for use in the business.

That matters in real life.

A vehicle delivered on December 28 may count in the current year if it is placed in service right away. A diagnostic tool sitting unopened in a box may not. The same logic applies to computers for new hires, routing tablets for technicians, or equipment waiting on setup before it can be used on customer jobs.

The IRS also uses timing conventions that can reduce or shift the first-year deduction. One of the most important is the mid-quarter convention, which can apply if a business places a large share of its equipment in service late in the year. For service companies that do year-end buying sprees, that rule can change projections materially.

Watch the calendar: Purchase date and placed-in-service date are not always the same. For tax purposes, ready for use is what counts.

Where MACRS, Section 179, and bonus depreciation fit

Owners often hear MACRS, Section 179, and bonus depreciation in the same conversation and treat them like interchangeable options. They are related, but they do different jobs.

- MACRS is the standard federal tax depreciation system used for many business assets.

- Section 179 can let you deduct some or all of the cost of qualifying equipment in the year you place it in service, subject to limits.

- Bonus depreciation can also allow a larger upfront deduction when the tax law permits it.

A simple way to view this is to compare it to driving routes. Your destination is recovering the cost of the asset. MACRS is the standard route. Section 179 and bonus depreciation may let you take more of that deduction earlier. The right route depends on taxable income, purchase timing, and what kind of financial picture you want your books to show.

That difference matters for service business decision-making. A managed IT firm may want smoother book expense on workstations and servers so gross margin trends are easier to read. The same firm may still choose faster tax write-offs to lower taxable income. A repair company with a growing vehicle fleet may do the same thing to keep operating KPIs useful while still taking available tax deductions.

Tax depreciation affects your tax bill. Book depreciation affects the numbers you use to run the business. You need both sets of rules working correctly.

How to Choose the Right Depreciation Method

You buy ten new laptops for your consulting team, a van for field calls, and a diagnostic device your technicians use all day. All three are equipment. They should not automatically use the same depreciation method.

The right method depends on how each asset loses value and how you use your financial statements. If you choose a method just because it is familiar, your books can become less helpful for pricing, margin analysis, lender reporting, and year-end tax planning.

Match the method to the asset

A service business usually owns equipment that wears out in different ways. A computer often loses value because it becomes outdated. A service vehicle loses value through time, mileage, and heavy use. A specialized tool may hold up well physically but generate more wear during busy months than slow ones.

That is why straight-line is often the default starting point for book depreciation. It spreads cost evenly and keeps monthly results easier to read. The IRS overview of depreciation methods and conventions also helps clarify that tax depreciation rules may follow a different schedule than your book method.

Here is the practical fit for common service business assets:

- High-end computers and office tech: Straight-line often works well for books if you want stable overhead by month or by employee. If the equipment becomes obsolete quickly, you may still use faster tax write-offs separately.

- Fleet vehicles: If vehicles are replaced on a planned cycle and used fairly consistently, straight-line often gives management cleaner trend lines for repair, utilization, and operating margin.

- Diagnostic tools and field equipment: If usage clearly rises and falls with jobs performed, a usage-based method can better match expense to revenue, but only if you track that usage reliably.

A simple comparison helps. A car used for the same commute every week usually loses value in a fairly predictable pattern. A vehicle driven hard for service calls across multiple territories wears out faster. Your depreciation method should reflect that difference, or your reports will smooth over something your operations team is feeling.

Start with the decision you need to make

Owners usually get better answers when they start with the business question, not the accounting label.

If you want cleaner monthly reporting, straight-line is often the better choice. If you want the expense pattern to follow actual use, a usage-based method may fit better. If your main goal is lowering current taxes, the answer may sit in your tax elections rather than in your book depreciation method.

That distinction matters for service businesses because many of the KPIs you watch are sensitive to timing. Front-loading expense can pressure net income early in an asset's life. Spreading expense evenly can make gross margin, EBITDA trends, and job profitability easier to compare from month to month.

Use a simple filter before you choose

Run through these four questions:

- How does this asset lose value in real life? Through time, usage, obsolescence, or a mix?

- Which number matters most right now? Internal management reporting, lender-facing statements, or taxable income?

- Can you track usage consistently? If not, a usage-based method may create more noise than insight.

- What decision will this number support? Pricing, hiring, fleet replacement, equipment budgeting, or tax planning?

For many service businesses, the answer is not one method for everything. It is a policy that fits each major asset class.

Keep book reporting and tax strategy separate in your mind

Owners often get tripped up. They hear that a faster tax deduction is available and assume book depreciation should match it. Often, it should not.

Your tax return is designed to apply tax law. Your books are designed to help you run the business. A managed IT firm may prefer straight-line on workstations to keep monthly overhead predictable, while still taking accelerated tax depreciation where allowed. A field service company may use one book approach for vans and another for specialized tools if that gives a truer picture of job costs.

Once you choose a method, apply it consistently and document why it fits the asset. That makes reviews easier for your CPA, helps your team post adjusting entries correctly, and gives you financial statements you can use to make decisions.

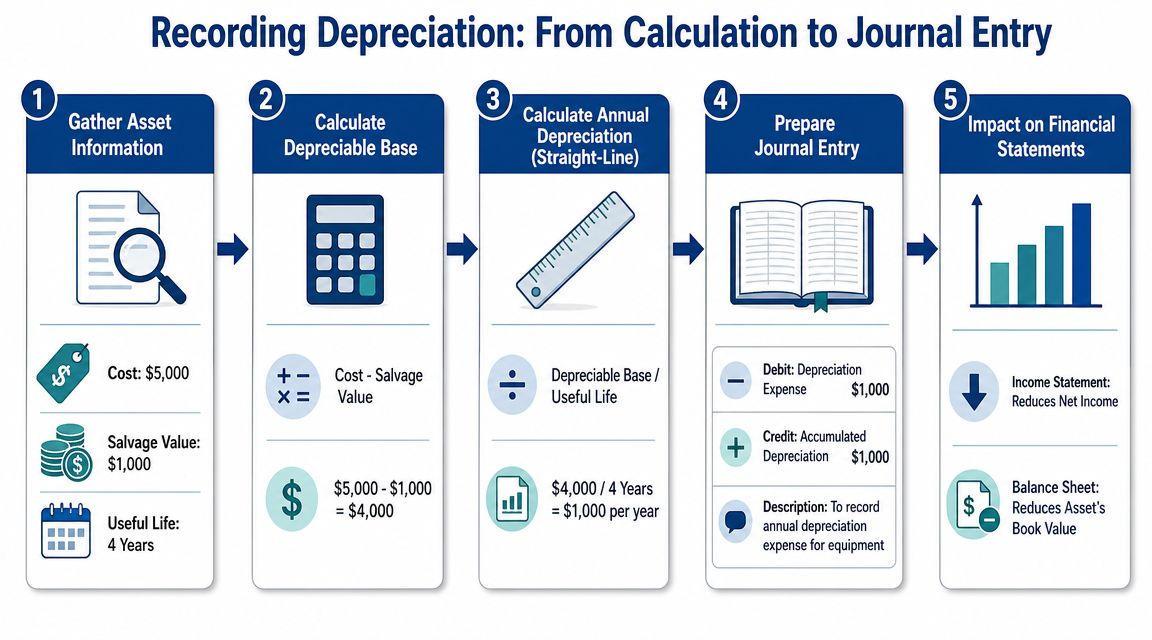

Recording Depreciation with Calculations and Journal Entries

Depreciation shifts from conceptual understanding to a monthly accounting task. The mechanics aren't difficult once the setup is right.

Use this example as a model.

Start with a simple straight-line calculation

Suppose you buy a piece of diagnostic equipment for $5,000, expect a $1,000 salvage value, and estimate a 4-year useful life.

The straight-line calculation is:

($5,000 – $1,000) / 4 = $1,000 annual depreciation

That means the depreciable base is $4,000, and you recognize $1,000 of depreciation expense each year until the asset reaches its expected salvage value.

If you record depreciation monthly, divide the annual amount by the number of months in the year and post the recurring entry consistently. The principle is the same. You're just recognizing smaller portions more frequently.

The journal entry

To record annual depreciation, the journal entry is:

| Account | Debit | Credit |

|---|---|---|

| Depreciation Expense | $1,000 | |

| Accumulated Depreciation | $1,000 |

This entry matters because it affects two statements at once.

- Income statement: Depreciation Expense reduces net income.

- Balance sheet: Accumulated Depreciation reduces the asset's carrying value without changing the original cost recorded in the fixed asset account.

If you want a refresher on the broader logic behind this type of period-end bookkeeping, these examples of adjusting entries are helpful.

How this usually looks in QuickBooks Online

In QuickBooks Online, many owners create the fixed asset account correctly but forget the related accumulated depreciation account. That leads to messy reporting.

A cleaner setup usually includes:

- Fixed Asset account: The original equipment cost

- Accumulated Depreciation account: A contra-asset account that offsets the asset on the balance sheet

- Depreciation Expense account: The recurring expense on the P&L

Then you can post recurring journal entries monthly or work with your bookkeeper to record them at month-end.

This walkthrough gives a visual explanation of the flow:

What trips owners up

The math is rarely the hardest part. The setup is.

Common problems include:

- Wrong start date: The asset should begin depreciating when it's placed in service, not when it was merely ordered.

- Missing salvage value logic: Some owners ignore it without thinking through whether that makes sense.

- No fixed asset register: Without a list of equipment, dates, methods, and balances, month-end gets sloppy.

- Mixing tax and book entries: That creates confusion when management reviews profitability.

A well-maintained fixed asset schedule keeps those issues under control and makes year-end much easier.

How Depreciation Impacts Your Service Business KPIs

Depreciation changes how your business looks on paper, and that affects the KPIs owners watch most closely.

On the profit and loss statement, depreciation lowers net income. On the balance sheet, accumulated depreciation lowers the book value of your assets. That means metrics based on earnings or assets can shift even when cash didn't move during the month.

The KPI effects owners actually feel

For service businesses, depreciation often shows up in:

- Net income: Lower because depreciation is an expense

- Return on assets: Affected because both earnings and asset carrying values are involved

- Job or department profitability: More realistic when equipment-heavy work carries part of the equipment cost

- EBITDA: This metric excludes depreciation, which is why owners should understand both EBITDA and net income, not just one of them

Idle equipment creates another common point of confusion. Authoritative accounting guidance generally says depreciation reflects the expected consumption of future economic benefits, not whether the asset is actively generating revenue. That means idle equipment should still be depreciated, as noted in this equipment depreciation discussion for financed equipment.

A spare service van sitting in the lot or a backup diagnostic tool on the shelf may not be producing revenue this month, but it can still be losing useful life from an accounting perspective.

That's why depreciation belongs in your broader operating review alongside utilization and cash flow calculation guidance. If you ignore it, you may underprice work, postpone replacements too long, or overestimate the return you're getting from older assets.

If your books need cleaner fixed asset tracking, stronger month-end reporting, or a better system for translating equipment purchases into useful management numbers, Steingard Financial helps service businesses build dependable bookkeeping around the decisions owners have to make.