You've formed your LLC. The state filing is done, clients may already be asking for invoices, and you're trying to keep momentum without getting buried in admin. Then the bank asks for an EIN, formation papers, ownership details, maybe an Operating Agreement, and if you run a remote business, even your address can suddenly become a problem.

That's where many owners get stuck. Opening a llc bank account sounds simple, but it's really one of the first tests of whether your financial systems are going to be clean or messy. If you get it right now, bookkeeping gets easier, tax prep gets easier, and your records tell a clear story. If you get it wrong, every deposit, transfer, and reimbursement becomes harder to classify later.

This guide walks through the process the way a patient CPA or bookkeeper would. You'll see what the bank wants, why they want it, where new 2026 BOI issues fit in, and how remote-first service businesses can avoid common roadblocks.

Why Your LLC Needs Its Own Bank Account

If you're a consultant, agency owner, coach, designer, developer, or other service business operator, you may be tempted to use your personal account for a little while. It feels faster. You're already busy. You just want to get paid.

That shortcut creates problems almost immediately. Your software subscription, lunch, client payment, owner transfer, and home utility bill all start living in the same feed. Then tax season arrives, and you or your bookkeeper have to untangle every line.

The strongest reason to open a separate account isn't just convenience. According to research summarized by Business Rocket, businesses using multiple financial services accounts show 30% higher long-term success rates, and 80% of small business owners with a dedicated business checking account report better financial organization. That's a practical result, not just a bookkeeping preference.

Separation protects both records and the business

A business bank account creates a clean starting point. Every client payment goes in. Every legitimate business expense comes out. That clean trail supports reconciliations, monthly reports, and tax filings.

It also helps preserve the legal separation between you and the LLC. If you want a plain-language overview of avoiding piercing the corporate veil, that resource explains why commingling personal and business funds can weaken the protection LLC owners expect.

Practical rule: If a transaction belongs to the business, it should move through the business account. If it belongs to you personally, keep it out.

A business account makes the next decisions easier

Once the account exists, other pieces fall into place. Payment processors like Stripe or PayPal can connect to the right place. Payroll systems can draft from the correct account. QuickBooks can import transactions without forcing you to sort through personal spending.

That matters later when you decide how to pay yourself and document owner transfers properly. If you need help thinking through that side of the setup, this guide on how to pay yourself from an LLC is a useful next read.

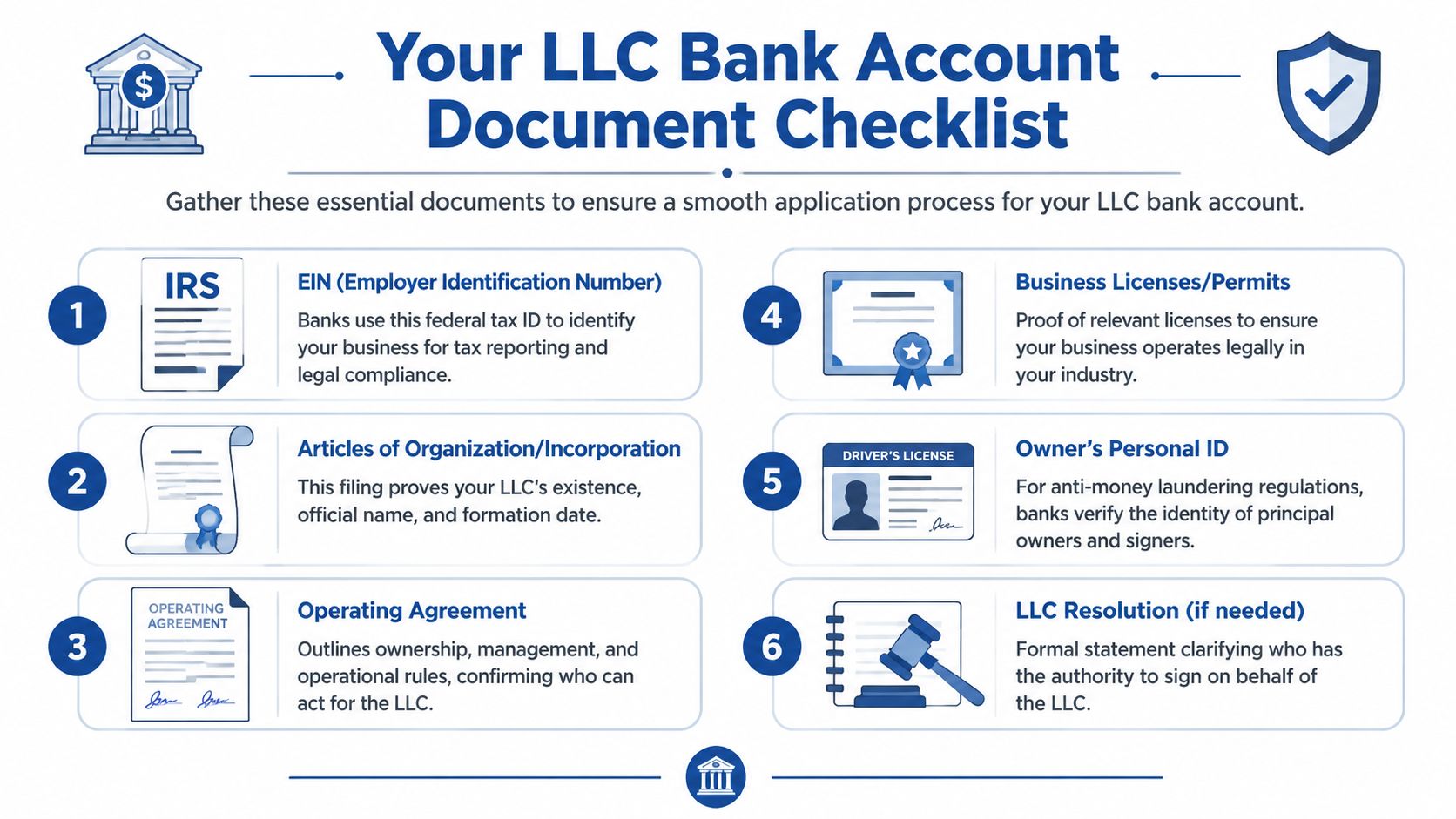

Your Document Checklist Before You Apply

Banks don't ask for paperwork just to be difficult. They're trying to answer a few basic questions. Does this LLC legally exist? Who owns it? Who has authority to act for it? Can the bank verify the people involved?

If you understand those questions, the checklist starts to feel logical.

Must-have documents for most LLC bank applications

EIN for federal tax identification

Articles of Organization to prove the LLC was formed

Operating Agreement to show ownership and authority

Government-issued ID for owners and signers

Business licenses or permits if your industry requires them

LLC resolution if the bank wants formal authorization for who can open and manage the account

Your EIN is the business tax ID

An EIN, or Employer Identification Number, works like the business's federal tax ID. Even if you don't have employees yet, banks commonly want it because they use it for tax reporting and compliance.

The online EIN process through the IRS is fast, but you should have your information ready before you begin. If you stop for too long, the session can time out. Once you have the EIN confirmation, save it in a secure folder with your other formation records.

Your Articles of Organization prove the LLC exists

Think of the Articles of Organization as the LLC's birth certificate. This is the state filing that shows the business name, formation status, and formation date.

Banks need this because they can't open an account for an entity that hasn't been formally created. If your LLC name on the bank application doesn't match the formation document exactly, that can trigger delays. Check spelling, punctuation, and any designator such as “LLC.”

Your Operating Agreement shows who can act for the business

Many new owners get confused here, especially single-member owners who assume they don't need one. The bank often wants an Operating Agreement because it helps confirm ownership, management structure, and authority.

For a single-member LLC, this document shows you are the owner and manager. For a multi-member LLC, it becomes even more important because the bank needs to know who can sign, who can transact, and who must be identified during account opening.

Personal ID is about verification, not suspicion

Banks must verify the identity of the people opening and using the account. That's why they ask for a driver's license, passport, or similar government-issued ID.

This requirement can feel personal, but it's standard. The bank is matching real people to a real legal entity.

Licenses and permits may matter depending on your work

Not every bank asks for business licenses in every case, but some do. This tends to come up more when the business operates in a regulated field or local licensing is common.

If you're unsure whether your business needs one, resolve that before the appointment. It's easier to delay the application by a day than to scramble after the banker asks for something you didn't know existed.

An LLC resolution may be required

Some banks want a separate LLC resolution stating who has authority to open and manage the account. This is especially common when the ownership or management structure is more complex.

A simple way to think about it is this:

| Document | What it tells the bank |

|---|---|

| EIN | The federal tax identity of the business |

| Articles of Organization | The LLC legally exists |

| Operating Agreement | Who owns and manages the LLC |

| Personal ID | The signer is a real, verified person |

| Business license | The business is authorized to operate where required |

| LLC resolution | The signer has authority to act for the LLC |

For recordkeeping, keep digital copies of every document in one folder, and name them clearly. A messy desktop becomes a messy application. If you want a broader system for storing these records, this article on small business record keeping is worth bookmarking.

How to Choose the Right Banking Partner

Choosing a bank isn't just about opening the first account you qualify for. It affects how easily you collect client payments, run payroll, reconcile transactions, and expand later.

For many service businesses, the first big question is whether to use a traditional bank, an online-only bank, or a fintech platform.

According to Airwallex's summary of current business banking trends, more than 80% of small businesses would consider switching to an online-only banking provider. The same source notes that initial deposit requirements typically range from $100 to $1,000, while monthly maintenance fees generally fall between $10 and $15, though some options have no monthly fee.

Online bank or traditional bank

The right answer depends on how your business operates.

| Banking option | Often a better fit when | Watch for |

|---|---|---|

| Traditional bank | You want branch access, in-person problem solving, or future lending relationships | Monthly fees, minimum balances, slower account changes |

| Online-only bank | You work remotely, rarely handle cash, and want faster digital tools | Cash deposit limitations, support quality, document rules |

| Fintech platform | You want simple remote onboarding and modern dashboards | Limits on services, transfer rules, and support escalation paths |

A remote marketing agency that invoices clients and pays contractors electronically may love an online-first setup. A local service company that handles checks, cash, or frequent branch needs may still prefer a traditional bank.

Look beyond the headline fee

A “free” account isn't always the cheapest account. Sometimes the monthly fee is low, but other costs show up later through transaction limits, wire fees, overdraft rules, or charges for treasury features.

Review these items before you apply:

- Monthly maintenance fee. Know whether you can waive it, or whether the account has no monthly fee.

- Minimum opening deposit. Make sure the required amount fits your startup cash plan.

- Payment processing support. If you use Stripe, Square, or PayPal, ask how smoothly those tools connect.

- ACH and wire capability. Service firms often pay contractors, software vendors, or overseas tools electronically.

- User permissions. If a bookkeeper or operations lead needs limited access, check whether the bank supports role-based permissions.

A bank account should fit your workflow, not force your workflow to fit the bank.

Software integration matters more than many owners expect

The account you choose will feed your books. That means transaction quality matters. If the bank sends clean transaction descriptions and stable feeds into QuickBooks, your books become easier to maintain. If the feed is messy, duplicated, or unreliable, every month-end close takes longer.

Ask practical questions:

- Does the bank connect directly to QuickBooks Online?

- Can you export transactions cleanly if the feed breaks?

- Does it work well with Gusto if you'll run payroll?

- Can you create separate debit cards for different team members or expense categories?

If your business is growing, also think a year ahead. You may want a business credit card, a savings account for tax reserves, or stronger cash management tools. Opening a llc bank account is a setup task, but selecting the right partner is a systems decision.

A short overview may help if you're weighing digital options against branch-based accounts:

A simple decision filter

If you're stuck between two options, score each bank on these five questions:

- Can I qualify without friction?

- Will it connect cleanly to my accounting and payroll tools?

- Will the fee structure still make sense six months from now?

- Can this account support how I get paid and pay others?

- If something breaks, can I reach a human who can fix it?

That short list usually cuts through the marketing.

The Application Process Decoded

You submit what looks like a simple application. Then the bank asks who owns the LLC, who can sign, whether the business address is acceptable, and whether your ownership records match what the government has on file. That surprises many first-time owners, especially remote-first service businesses that do not operate from a traditional office.

Opening a llc bank account is really a verification process. The bank is building a file that ties together four things: the legal business, the people behind it, the person with authority to act, and the tax identity used to report activity correctly. If one piece does not match the others, the application can pause even when the business itself is legitimate.

A helpful way to view the process is this: your formation documents prove the LLC exists, your EIN connects the business to the IRS, your ID proves you are who you say you are, and your operating documents show who has permission to control the account. Banks check all four because they are required to know their customer and monitor business accounts for fraud, money laundering, and tax reporting accuracy.

Online application versus in-person appointment

Online applications work well when the file is simple and complete. That usually means one owner, clean documents, a standard business address, and no confusion about signer authority.

An in-person appointment helps when the business has more than one owner, a manager-managed structure, a virtual address, or BOI details that may trigger follow-up questions. For a remote-first agency, consultancy, or freelance studio, this matters. A banker can tell you right away whether the bank will accept your address setup and what extra proof of business activity they want.

Here's a practical comparison:

| Approach | Best for | Main tradeoff |

|---|---|---|

| Online | Simple ownership, clean documents, comfort with uploads | Harder to solve document questions in real time |

| In person | Multi-member LLCs, authority questions, address complications | Requires scheduling and showing up prepared |

Single-member LLC path

A single-member LLC usually has the shortest path because the bank is matching one owner to one business record.

You will usually provide:

- your EIN

- your Articles of Organization

- your Operating Agreement

- your personal ID

- any required business license or permit

The bank reviews the documents to answer a few basic questions. Does the LLC legally exist? Does the EIN belong to that business? Does the owner's name match across the file? Is this person allowed to open the account?

If your business is remote-first, be ready for one extra layer. Some banks want a physical business address, while others accept a home address, registered agent address for formation only, or separate mailing address plus proof of where the business physically operates. A website, client invoices, signed service contracts, or a utility bill tied to the owner can help show the business is real and active.

Bring digital copies and printed copies if you are going to a branch. Banks do not always use the same system for uploaded documents and branch review.

Multi-member and manager-managed LLC path

Multi-owner LLCs take longer because the bank has to verify authority, not just existence.

That distinction matters. An LLC can be legally formed and still leave the bank with an open question: who is allowed to control the money? For bookkeeping and internal controls, that answer should be clear before the application starts. If it is vague, you risk delays now and account disputes later.

According to NCH's guidance on LLC banking practices, banking resolutions are commonly missed during account setup. That gap creates avoidable follow-up because the bank needs written proof of who can act for the company.

What a banking resolution does

A banking resolution is a document that tells the bank who can open, manage, and sign on the account for the LLC.

It works like a permission slip backed by the company's own records. For a member-managed LLC, it can confirm which members may act. For a manager-managed LLC, it can show that day-to-day authority sits with a manager rather than every owner.

A useful banking resolution should state:

- Authorized signers

- Any limits on signer authority

- Whether the LLC is member-managed or manager-managed

- How signer authority changes will be approved later

That may feel formal for a small business. It prevents messy bookkeeping and governance problems. If one co-owner believes everyone can spend freely and another believes only one person can approve payments, the bank account becomes the first place that conflict shows up.

What beneficial ownership means

Beneficial ownership means the actual people who own or control the company, even if only one person will use the account day to day.

Banks ask for this because they are required to identify who stands behind the business. Starting in 2026, many owners will run into this issue earlier because FinCEN BOI reporting is now part of the account-opening conversation, not just a separate compliance task. If the ownership details on your BOI filing, Operating Agreement, and bank application do not match, the bank may stop and ask for clarification.

For practical purposes, treat these three records as one set:

- your Operating Agreement

- your BOI filing or BOI confirmation details

- your bank application ownership section

If one says 50/50 ownership and another says 60/40, the bank sees a risk issue. Your bookkeeper sees a capital-account problem. The IRS can eventually see a tax-reporting problem. Clean records start here.

A clean application sequence for multi-owner LLCs

For partnerships, agencies with co-founders, and manager-managed service firms, this order usually keeps the process orderly:

- Confirm the Operating Agreement matches the actual ownership and management structure.

- Prepare the banking resolution before the application starts.

- Gather ID and contact information for each required owner and signer.

- Check that BOI ownership details match the same names and percentages.

- Ask the bank in advance whether all owners must appear or whether one authorized signer can handle the appointment.

The reason for this sequence is simple. A single-member LLC mostly proves identity and existence. A multi-member LLC must also prove decision-making authority, ownership transparency, and internal consistency across several records.

Avoiding Common Account Opening Pitfalls

Most problems don't come from the bank rejecting a legitimate business. They come from owners assuming old rules still apply or assuming a remote business should be handled the same way as a local office-based company.

The two issues causing the most confusion today are BOI reporting and business address requirements.

Don't treat BOI as a later task

Many owners still think Beneficial Ownership Information reporting is something to handle after the account is open. That assumption can backfire.

According to Tailor Brands' 2026 overview of LLC bank account issues, BOI reporting has been a key part of bank openings since January 1, 2024, and 12% of account applications are rejected because the BOI is incomplete. If your ownership details are missing or inconsistent, the bank may pause or deny the application.

A simple approach works best:

- File BOI early. Don't wait until the bank asks whether it's been handled.

- Make sure ownership details match your Operating Agreement and bank application.

- Save the confirmation receipt so you can produce it quickly if requested.

- Check changes promptly if ownership shifts after formation.

If your LLC has more than one owner, assume the bank will look closely at who owns what and whether your BOI details are complete.

Remote businesses need an address plan

Many banking guides assume you have a traditional office. Many modern service businesses don't. Consultants, agencies, SaaS teams, and virtual firms often run fully remote.

That same Tailor Brands source notes that 28% of new businesses are remote startups, that banks such as Chase now accept virtual mailboxes or registered agent addresses if EIN-verified, and that 65% of fintechs like Wise offer EIN-only remote openings.

For remote-first owners, that changes the strategy.

What to do if you don't have a physical office

Use an address approach that the bank can work with. Depending on the institution, that may mean:

- A registered agent address tied to your LLC records

- A virtual mailbox that the bank accepts when paired with EIN verification

- A fintech platform built for remote onboarding

The important part is consistency. Your address on bank records, formation records, and supporting documents should align closely enough that the compliance team doesn't have to guess what's going on.

Where remote owners often go wrong

Remote businesses usually hit trouble in three places:

- They apply before deciding which address they'll use consistently.

- They choose a bank with rigid branch-era policies when a fintech would fit better.

- They submit ownership paperwork that doesn't match the BOI filing.

That combination can make a healthy business look disorganized on paper. Banks don't see your good intentions. They see the file you submit.

Your Account Is Open What Now

A new LLC bank account is like a clean ledger page. It only stays clean if every dollar starts using the right path from day one.

Your first job is to make the account the home base for the business. Deposit startup funds there. Send client payments there. Pay business bills from there. If money first lands in your personal account and then gets transferred over, your records become harder to read, and that creates extra bookkeeping work at tax time.

Set up your systems early, while the account is still simple and easy to review. For a remote-first service business, this step matters even more because your bank account often becomes the main paper trail that shows how the company operates.

- Connect payment processors right away. Link Stripe, Square, PayPal, QuickBooks Payments, or other tools directly to the business account.

- Limit access carefully. Order debit cards and checks only for people who need them, and set permissions based on their role.

- Turn on account alerts. Alerts help you catch fraud, duplicate charges, and failed deposits before they turn into larger cleanup projects.

- Connect your bookkeeping software. Sync the account with QuickBooks or your accounting system, then review the first few imported transactions to make sure they are coding correctly.

- Add payroll and bill pay after you verify the basics. One wrong account number can delay payroll or vendor payments.

- Label owner money clearly. Owner contributions, draws, and reimbursements should each be recorded separately so they do not get mixed together.

Do one more housekeeping step now. Save a copy of the account approval email, signature card, account numbers, online banking access details, and any bank compliance messages in the same secure folder as your LLC formation documents, EIN letter, and BOI records. If the bank requests an update later, which can happen when ownership information changes or FinCEN rules require fresh reporting, you will not have to rebuild the file from scratch.

Then build a monthly review habit. Reconciling means matching your bank activity to your bookkeeping records so every deposit, payment, fee, and transfer is accounted for. If you want a step-by-step example, this guide on how to reconcile bank accounts walks through the process.

A separate account helps only if you treat it as the center of your financial system. That is what gives you cleaner books, clearer tax records, and reports you can trust when deciding how much to spend, save, or pay yourself.

If you want help turning a new bank account into a clean bookkeeping system, Steingard Financial can help you set up accurate records, connect QuickBooks and payroll tools, and keep your books organized from the start.