Financial Statement Preparation: Service Business Guide 2026

You're probably looking at a QuickBooks file, a bank feed, a payroll report, and a handful of invoices, thinking some version of the same thing every owner thinks the first time they try to do a real close: the numbers are here, but they don't feel trustworthy yet.

That's a frustrating place to be. Revenue might look healthy, yet cash feels tight. Payroll is posted, but you're not sure whether contractor costs hit the right month. The balance sheet has accounts you haven't reviewed in weeks, maybe months. Nothing is fully broken, but nothing feels clear either.

That's where proper financial statement preparation changes the game. Done well, it turns disconnected activity from your bank, payroll system, billing software, and expense tools into reports you can use. Not just to satisfy a lender, your tax preparer, or your board. To decide whether you can hire, whether pricing is working, whether a rough month was temporary, and whether the business is building real strength.

From Financial Fog to Strategic Clarity

A service business owner usually reaches this point after growth outpaces habit.

At first, the books are simple enough to manage by instinct. You know which clients paid late. You know payroll is your biggest cost. You can glance at the bank balance and make decisions. Then the business adds staff, recurring software subscriptions, contractors, prepaid retainers, equipment, and maybe a loan or line of credit. The same basic bookkeeping process that worked at a smaller size starts producing reports that are technically present but practically unhelpful.

I see this most often when the income statement gets treated as the whole story. An owner sees a profit and assumes the month went well, while accounts receivable stretched, deferred revenue piled up, or cash left the business faster than expected. The statements weren't prepared incorrectly on purpose. They just weren't prepared with enough discipline to answer real operating questions.

Financial statements should reduce uncertainty. If they create more of it, the close process needs work.

For a service business, the core package is straightforward. You need an income statement to show what you earned and spent over a period. You need a balance sheet to show what the business owns, owes, and has built in equity. You need a statement of cash flows to explain why profit and cash rarely move in perfect sync.

The mistake is thinking those reports begin when you click “Run Report” in QuickBooks.

They begin much earlier, with how transactions were coded, how payroll was posted, whether account balances were reconciled, and whether the numbers reflect what happened in operations. A strong close doesn't just assemble reports. It interprets them. If a major client delayed a project, if overtime increased to protect service delivery, or if you spent more on retention and staffing stability, that story belongs alongside the numbers.

That's when financial statement preparation stops feeling like compliance and starts becoming management.

Setting the Stage with Quality Inputs

Good statements start with boring discipline. There's no shortcut around it. If the inputs are messy, the output will be polished nonsense.

Gather the records before you touch the reports

For a proper month-end close, pull the full set of source records first. In a service business, that usually includes:

- Bank activity: Monthly statements for every operating, payroll, savings, and merchant account.

- Credit card records: Statements plus detail for any cards used by owners, managers, or team leads.

- Payroll summaries: Reports from Gusto or QuickBooks Payroll showing gross wages, taxes, benefits, reimbursements, and employer costs.

- Accounts receivable aging: Open invoices, unapplied payments, credits, and any disputed balances.

- Accounts payable or unpaid bills: Vendor bills, recurring subscriptions, contractor invoices, and accrued items not yet entered.

- Loan and debt statements: Term loans, equipment financing, lines of credit, and interest details.

- Fixed asset support: Purchases of computers, furniture, or equipment that may need capitalization rather than immediate expensing.

Owners often want to begin by “cleaning up the P&L.” That's usually backward. Start by proving the underlying accounts.

Use the four C's or expect bad reports

The most practical data quality test I know is the four C's: correct, current, complete, and consistent. Applied well, they help achieve 98% accuracy in financial reporting benchmarks for US service businesses according to Citrin Cooperman's discussion of financial reporting best practices. The same source notes that misclassified assets and liabilities, improper revenue recognition, and incorrect cash flow classification collectively cause 42% of misleading financial reports in growing companies.

That sounds technical, but in practice it means asking plain questions:

| Data check | What to ask |

|---|---|

| Correct | Was this coded to the right account and the right customer or vendor? |

| Current | Did it hit the right month, or is timing off? |

| Complete | Are all bank, card, payroll, and billing transactions included? |

| Consistent | Are similar items treated the same way every month? |

A single coding shortcut can distort a whole report package. Booking a loan payment entirely to expense instead of splitting principal and interest distorts both the income statement and the balance sheet. Treating a client prepayment as revenue too early makes one month look stronger than it was and the next month weaker.

Your chart of accounts is the blueprint

Many first-time closes go sideways because the chart of accounts was never designed for the business as it operates. If your file has vague buckets like “miscellaneous expense,” “owner draw,” “other income,” and duplicate software or payroll accounts, review becomes guesswork.

A service business needs a chart of accounts that mirrors how management thinks. Revenue categories should reflect real service lines if those distinctions matter. Payroll accounts should separate wages, taxes, benefits, and contractor labor if you want labor visibility. Liability accounts should clearly distinguish credit cards, loans, taxes payable, and deferred revenue.

If yours isn't structured that way, it's worth learning what a chart of accounts should do in practice, because nearly every reporting problem eventually traces back to account design.

Practical rule: If you can't explain what belongs in an account without hesitation, that account is too vague.

Payroll data needs extra skepticism

Payroll is one of the biggest expenses in most service businesses, and it's one of the easiest areas to trust too quickly. Don't rely on the cash leaving the bank as proof that payroll is posted correctly. Review wages, employer taxes, benefits, reimbursements, and payroll liabilities separately.

Control matters here too. If one person can change pay rates, add employees, approve hours, and process payroll, reporting risk rises along with fraud risk. Owners who want a practical overview of internal safeguards should review these strategies to prevent payroll fraud, especially if payroll has grown faster than finance oversight.

Executing the Month-End Close and Reconciliation

Reconciliation makes accounting practical, moving it beyond theory. It is the part that forces your books to match reality.

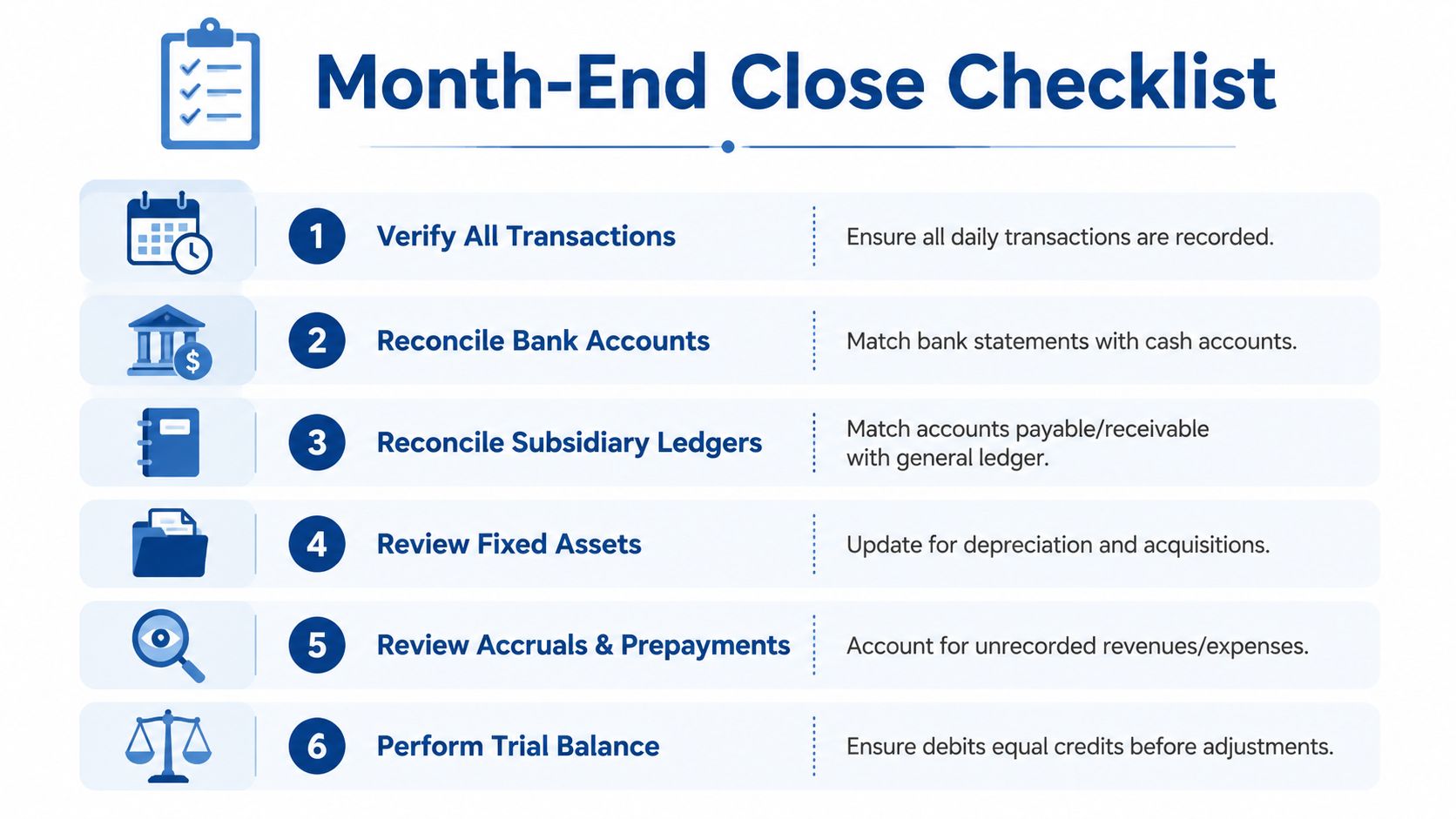

Start with cash, then move outward

The cleanest month-end close starts with the accounts that anchor everything else.

- Reconcile bank accounts first. Match every cleared transaction to the bank statement. Investigate anything old, duplicated, or uncategorized.

- Reconcile credit cards next. Don't stop at statement balance. Review whether each charge landed in the right expense, asset, or liability account.

- Tie receivables and payables to the general ledger. Open invoice and bill reports should agree to their control accounts.

- Review debt accounts. Loan balances should agree to lender statements, with principal and interest separated correctly.

- Inspect clearing and suspense accounts. These are often where old mistakes go to hide.

When owners skip directly to the profit and loss statement, unresolved balance sheet problems stay buried. Then they roll forward month after month and become “historical cleanup.”

A checklist is not administrative fluff

A formal close checklist matters because it controls sequence, ownership, and review. Used properly, a risk-prioritized close checklist can reduce month-end statement errors by 35% in lean finance teams according to Connor Group's guidance on accurate financial statements. The same methodology stresses separating preparation, review, and approval responsibilities, with compensating controls such as stronger post-close monitoring where full segregation of duties isn't possible.

That matters in small businesses because one person often handles too much.

If the same employee imports transactions, posts adjustments, reconciles accounts, and issues final statements with no second review, mistakes become final too easily. Full segregation isn't always realistic. A compensating control can be as simple as the owner or outside accountant reviewing reconciliations, unusual journal entries, and significant estimates before the package is finalized.

What a workable close sequence looks like

A useful checklist follows risk, not convenience.

- High-risk first: Cash, merchant accounts, payroll liabilities, sales tax, and debt should be reviewed before lower-risk expense accounts.

- Timing-sensitive next: Accrued expenses, deferred revenue, and unbilled or prepaid items need close attention because they affect the period presented.

- Judgment-heavy later: Estimates like depreciation, allowances, and reserves should be documented after the base balances are proven.

- Final review last: Someone should walk through the full reporting package from top to bottom, not just scan account balances.

If you want a practical model, this overview of month-end close best practices is the kind of discipline growing service firms benefit from.

Reconciliation work should leave a trail

A reconciliation isn't complete because the software says “difference = 0.00.” It's complete when another person can understand what was done and why.

That means keeping support for old outstanding checks, unusual deposits, loan balance changes, and reconciling items that didn't clear. It also means documenting why a transaction was reclassed or why an account was intentionally left unreconciled pending support.

For teams building this process for the first time, a visual walkthrough of step-by-step account reconciliation can help make the workflow less abstract.

If an account balance changed materially and nobody can explain the change in one or two sentences, the close isn't finished.

Common close failures

Connor Group's guidance highlights several recurring problems worth watching closely: failure to reconcile significant balance sheet accounts, inconsistent application of accounting policies across periods, and poor materiality judgment that either over-focuses on trivial items or misses important ones.

In plain English, that looks like this:

- Unreconciled balance sheet accounts: Payroll liabilities, old receivables, or merchant clearing balances sit untouched for months.

- Policy drift: Software subscriptions are expensed one month, prepaid the next, then split inconsistently after that.

- No materiality lens: The team spends time debating a tiny office supply charge while ignoring a major customer credit memo or revenue cutoff issue.

That's why the best close process feels a little repetitive. Repetition is what makes reports dependable.

Making Crucial Adjusting Journal Entries

Once the underlying accounts are reconciled, the next job is to capture what happened economically, not just what moved through the bank.

The entries owners usually miss

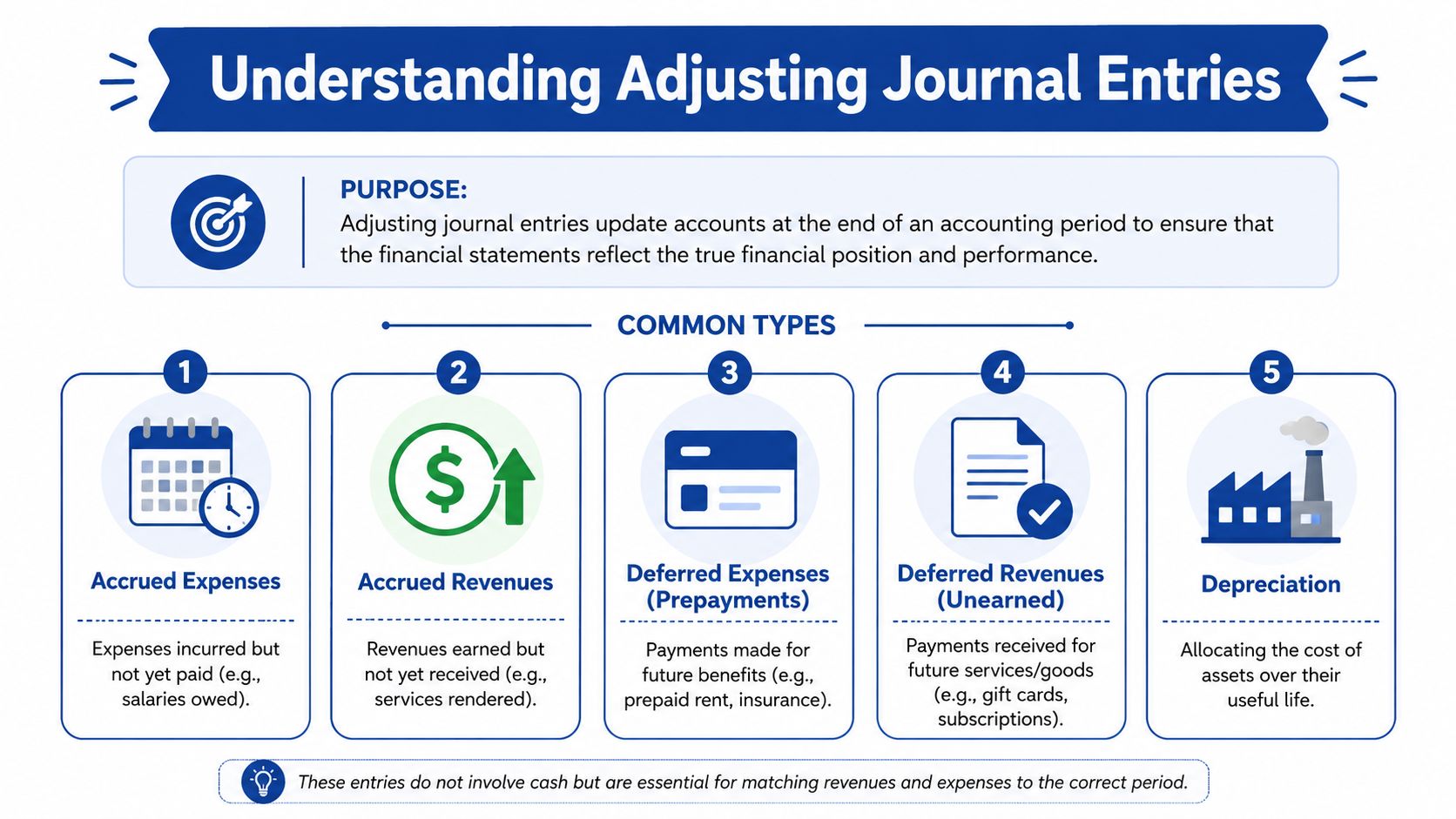

A service business can look current in the bank feed and still be wrong on the statements. That's because many real business events don't arrive as tidy same-month cash transactions.

Take a common example. A contractor finishes project work in the last week of January, but the invoice doesn't arrive until February. If January got the benefit of that labor, January should carry the cost. That's an accrued expense.

Another example is a prepaid client retainer. Cash may arrive upfront, but if the work will be delivered over future months, that amount shouldn't all hit revenue immediately. It starts as a liability and gets recognized as the services are performed.

Then there are fixed assets. If you buy new computers for your staff, that may not belong as a one-month office expense. Depending on the facts and your capitalization policy, the cost may need to be recorded as an asset and recognized over time through depreciation.

Here's a quick refresher before deeper review:

Estimates need support, not instinct

Some adjusting entries are mechanical. Others require judgment. The dangerous ones are the judgment calls that no one documents.

Connor Group's methodology for accurate statement preparation emphasizes validating estimates such as depreciation, allowances, and reserves each period by documenting the rationale and assessing sensitivity. That's the right standard for small service businesses too. If you change an estimate, write down why. If you continue an estimate from the prior month, confirm why it still makes sense.

A reviewer should be able to tell whether the entry reflects policy, evidence, and timing. Not just whether the math foots.

“Reasonable” is not enough support for an adjusting entry. You need a basis someone else can follow.

Resilience costs are real, and they need thoughtful treatment

This is the area most standard close guides barely touch.

Service firms increasingly spend money on operational resilience. That can mean retention initiatives, extra staffing capacity, cross-training, backup vendor arrangements, supply buffers, or systems put in place to avoid service disruption. These costs may not generate revenue directly in the current month, but they can be central to protecting delivery and client trust.

According to Insource Services' discussion of financial statement preparation pitfalls, a 2025 survey found that 42% of service firms now budget for “resilience buffers,” while 65% of organizations misallocate these costs as general expenses, which can distort margin analysis.

The practical issue isn't whether the business should incur those costs. It's how to present them without muddying core operating performance.

A practical way to handle resilience spending

There isn't one universal account title that solves this. The right answer depends on the nature of the spending and your reporting needs. But there is a good discipline to follow:

- Identify the underlying nature of the cost: Is it payroll, contractor labor, software, training, or outside services?

- Avoid dumping it into miscellaneous overhead: That hides both the amount and the business decision behind it.

- Track it separately for internal analysis: You may keep the GAAP presentation within its proper functional category while using subaccounts, classes, or memo tagging to isolate resilience-related spend.

- Discuss it in management reporting: If margins compressed because you intentionally funded staffing stability or backup capacity, that belongs in your narrative review.

For example, if you ran additional training to reduce turnover risk in a client-facing team, the cost may still belong in compensation or training expense. But management should also be able to identify that spend as a resilience investment rather than routine run-rate overhead.

That distinction matters. Without it, owners can overreact to a temporary margin dip and cut the very spending that protects service quality.

Standardize the support package

Every adjusting entry should have support attached. At minimum:

| Entry type | Support to keep |

|---|---|

| Accruals | Invoice, contract, work summary, or calculation |

| Deferrals | Billing schedule, service period, client agreement |

| Depreciation | Fixed asset detail, placed-in-service date, policy |

| Estimate changes | Written rationale and basis for revision |

If your team can't review the support quickly, the entry is too dependent on memory.

Compiling and Reviewing Your Financial Statements

Once reconciliations and adjustments are complete, you can generate the reports. This is the part most owners think of as financial statement preparation, but a CPA would treat report generation as the midpoint, not the finish line.

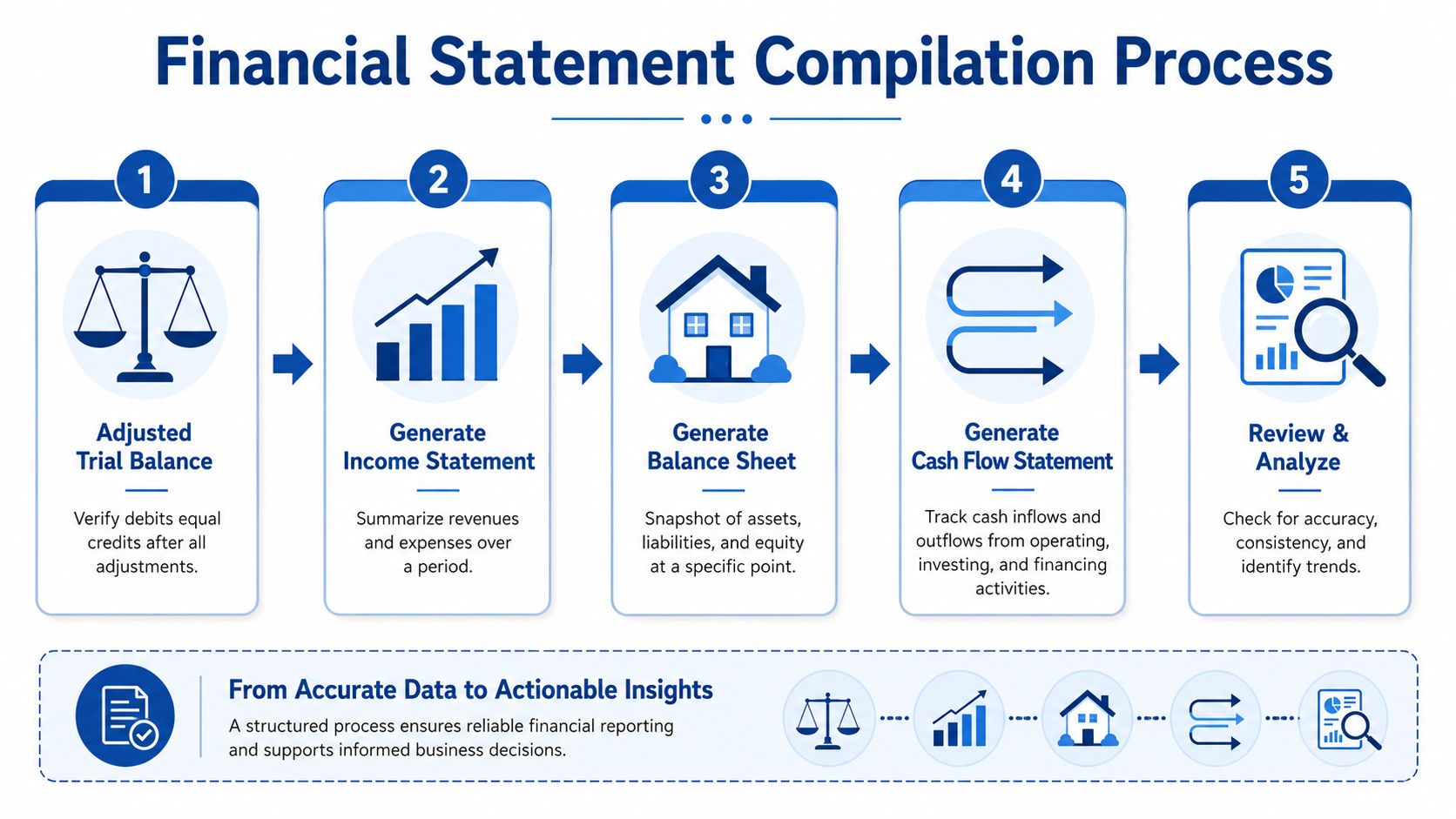

Build the package from the adjusted trial balance

The sequence matters.

First, confirm the adjusted trial balance is complete after all entries are posted. Then generate the income statement, balance sheet, and statement of cash flows for the period. If you use QuickBooks Online, don't just accept the default settings. Check period dates, accounting basis, comparative columns, and whether any unusual filters are active.

Then begin the review.

A good review asks whether the statements agree with each other and whether they agree with reality. The five-step reporting discipline outlined by Citrin Cooperman includes reconciling the trial balance to the general ledger, confirming beginning balances against prior-period close, validating that net income ties to retained earnings, confirming cash alignment between the balance sheet and cash flow statement, and requiring at least one reviewer to walk through the full package end-to-end. That's the standard to aim for in a serious month-end close, even in a smaller business.

Review logic before you review trends

The first review pass should focus on internal consistency.

- Net income tie-out: The current-period result should roll appropriately into equity.

- Cash agreement: Ending cash on the balance sheet should agree to the cash flow statement.

- Balance sheet reasonableness: Receivables, payables, debt, and deferred items should match what management knows to be true.

- Classification check: Large items should appear in the right sections and account groups.

Only after that should you shift to analytical review.

Variance review catches what account coding misses

A month can be technically closed and still misleading if nobody asks why the numbers changed.

Run a period-over-period comparison and investigate swings that don't make operational sense. Revenue up while receivables balloon? That may indicate collections pressure. Payroll down while service levels slipped? Staffing changes may be showing up before client retention does. Software expense doubled? Maybe annual renewals hit, or maybe duplicate subscriptions were booked.

A useful variance review doesn't require advanced software. It requires concise explanations. If revenue dropped because one project was delayed, say that. If gross margin tightened because senior staff covered turnover gaps, say that too.

Numbers without explanation force owners to guess. That's when bad decisions start.

Add the operating story to the financial story

Most reporting guides stop after accuracy checks. That leaves out one of the most valuable parts of the process: contextual narrative integration.

According to the SEC-linked summary in your provided research set, 78% of leaders struggle to connect financial metrics with operational context, and story-driven reporting is identified as an emerging trend for investor trust and internal decision-making in the SEC beginner-oriented financial statement guide reference.

For a service business, that means your close package should answer questions like:

- Why did revenue move?

- What changed in staffing, capacity, or utilization?

- Which costs were intentional investments versus ordinary drift?

- Were there operational disruptions, project delays, or collection issues?

- Did a change in client mix affect margins or cash timing?

This doesn't need to become corporate jargon or a lengthy memo. A short management narrative can be enough.

A simple management note format

Try attaching a one-page summary to the statements using a structure like this:

| Focus area | Example of useful narrative |

|---|---|

| Revenue | A major client project shifted into next month, delaying recognition. |

| Labor | Contractor usage rose to protect delivery during hiring gaps. |

| Cash | Collections slowed on two large invoices, despite stable profitability. |

| Resilience spending | Training and coverage costs increased intentionally to stabilize service levels. |

That small step changes how financial statement preparation functions inside the business. The statements stop being a historical archive and start becoming a decision tool.

Putting Your Financial Statements to Work

A clean month-end package earns its value after the close, not during it.

If you own a service business, the reports should help you answer practical questions. Is pricing keeping up with labor pressure? Are collections slowing? Are overhead costs creeping up because the business is growing, or because no one is watching subscriptions, contractors, and admin spend closely enough?

Start with a few usable measures

You don't need a dashboard with dozens of ratios. Start with a short list you'll review every month.

- Gross profit margin: Useful if your service model has direct labor or contractor costs that should be measured against revenue.

- Net profit margin: Shows what remains after all operating costs and other expenses.

- Days sales outstanding: Helps you see whether reported revenue is turning into cash on a reasonable timeline.

The exact formula setup depends on how your chart of accounts is organized. The important part is consistency. Once you define these measures, calculate them the same way every month so trend lines mean something.

If your marketing spend is material, pair financial statement review with channel-level evaluation. For owners trying to connect campaign spending to revenue quality, Rebus' expert marketing ROI advice is a practical complement to the finance side of the discussion.

Know when the process is costing too much owner time

There's a point where doing your own close becomes expensive even if it doesn't show up as a direct invoice. If you're spending late nights reviewing reconciliations, chasing payroll detail, fixing old coding errors, and trying to explain cash swings from memory, the business is already paying for the gap.

That's usually when financial statement preparation needs to move from owner-managed to professionally managed. Not because owners can't understand the numbers. They should. But because they shouldn't have to build and maintain the full accounting control process themselves.

If you want a clearer sense of what useful reporting analysis should look like after the statements are prepared, this explanation of financial statement analysis is a good next step.

Strong financials won't run the business for you. But they will remove a surprising amount of hesitation from hiring decisions, pricing conversations, cash planning, and growth bets. That clarity is usually what owners are looking for in the first place.

If your books are technically up to date but your month-end reports still don't feel decision-ready, Steingard Financial can help build a cleaner close process, organize your chart of accounts, manage reconciliations, and deliver financial statements that support growth.