What Is Month End Close? a Guide for Business Owners

You're at the end of the month. Payroll went out, clients paid some invoices but not others, a few expenses are sitting in someone's inbox, and your bookkeeper says the numbers aren't final yet. Meanwhile, you still have to decide whether to hire, spend on marketing, or hold cash a little tighter.

That's where many service business owners get stuck. They have activity, but not clarity. They can see money moving, but they can't say with confidence what the business earned, owed, or spent last month.

That gap is what the month-end close is meant to fix. If you've ever wondered what is month end close, the short answer is this: it's the process that turns a messy month of transactions into a financial picture you can trust. And once that picture is reliable, strategy gets easier. You stop guessing. You start deciding.

More Than Just Numbers Why Your Month-End Close Matters

A lot of owners treat the close like brushing your teeth before a dental visit. Necessary, annoying, and easy to postpone. I get why. Close work usually shows up as reconciliations, journal entries, and review tasks that don't feel connected to winning new business.

But the connection is direct.

If your books aren't closed, your profit may be overstated because a large vendor bill hasn't been recorded yet. Your cash position may look stronger than it is because payroll taxes haven't hit correctly. Your revenue may look weaker than it is because customer invoices were posted late. In other words, unfinished books create false signals.

Flying blind costs more than owners think

Service businesses live on timing. You're managing payroll, utilization, client retention, collections, software costs, and often a growing team. A delayed or sloppy close makes all of those decisions harder.

Think about a consulting firm owner reviewing last month's results. If accounts receivable hasn't been cleaned up, they may assume a sales problem when the actual issue is collections. If accrued expenses aren't posted, they may greenlight hiring based on profit that doesn't really exist. If bank accounts haven't been reconciled, they may miss duplicate charges or unexplained withdrawals.

Good financial reporting doesn't just tell you what happened. It tells you whether you can trust what you're looking at.

A disciplined close gives you a repeatable monthly rhythm. Every month, your team gathers the same kinds of information, checks it, adjusts it, and turns it into reports that mean something. That rhythm matters because business owners don't just need data. They need dependable timing.

The real output is confidence

The point of month-end close isn't to “finish accounting.” It's to create a clean snapshot of the business at a specific point in time.

That snapshot helps you answer practical questions like:

- Are we profitable? Not just busy.

- Did cash improve for the right reasons? Or because bills are still sitting unpaid.

- Are labor costs in line? Especially important in service businesses where payroll drives margins.

- Can we invest this month? Or should we preserve cash.

That's why the close belongs in the same conversation as planning, pricing, and hiring. It isn't back-office housekeeping. It's the foundation for deciding what to do next.

Why business owners should care personally

Even if you have a bookkeeper or outsourced accounting team, this matters to you because you're the person making bets with the information. You don't need to post every journal entry yourself. You do need to know whether the numbers in front of you are final, reviewed, and usable.

When the close is working, you can sit down early in the month and review performance without second-guessing the data. When it isn't, every decision has an asterisk.

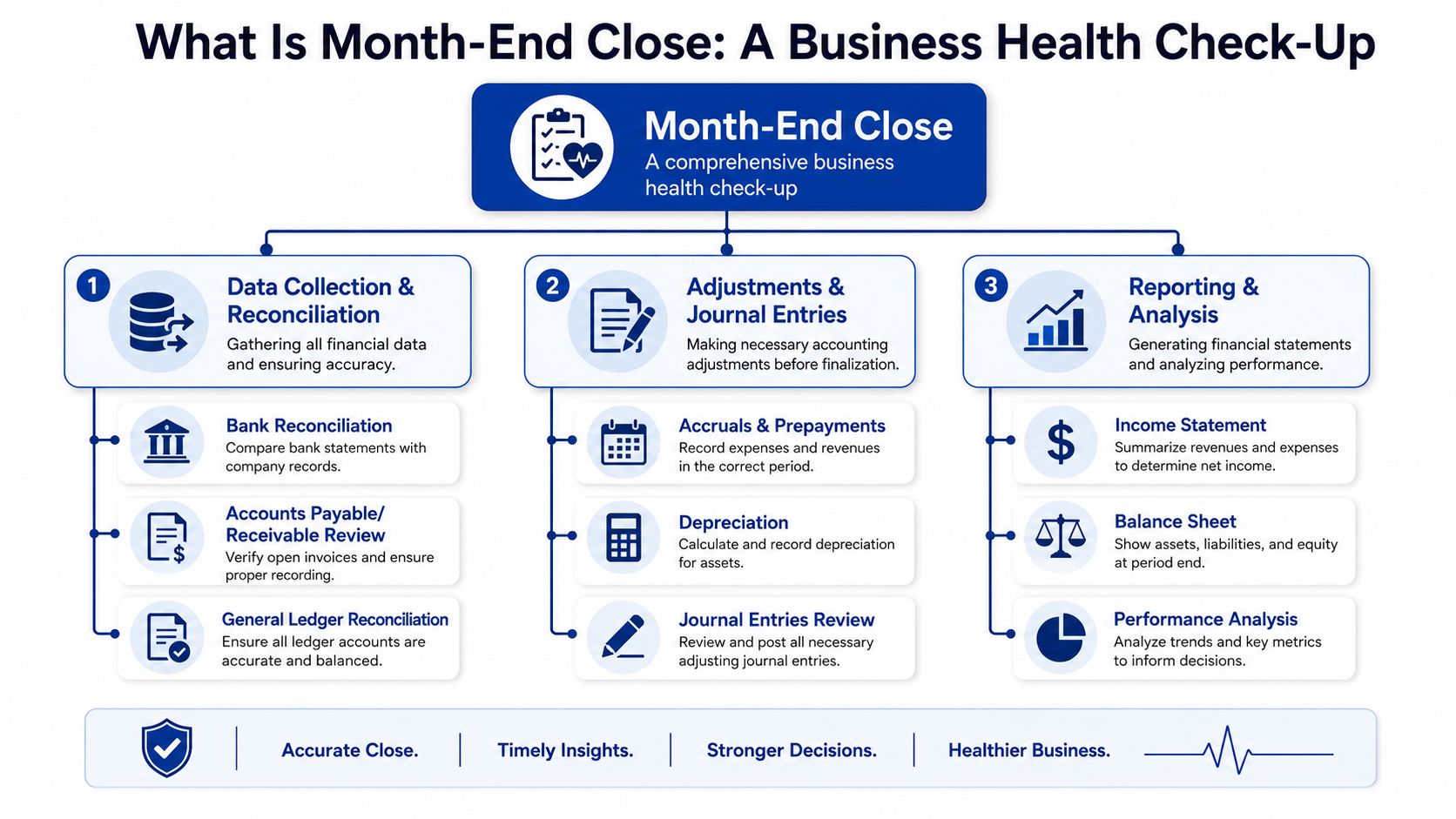

What Is Month End Close A Look Under the Hood

Think of month-end close as a financial health check-up. During a medical check-up, the doctor doesn't just ask how you feel. They measure, verify, compare, and look for anything unusual. Month-end close works the same way for your books.

According to Ramp's overview of the month-end close process, the median close takes 6.4 days, while a traditional manual process can take 8 to 10 business days and consume 120 to 150 manual hours. The point isn't speed alone. It's producing accurate, reliable financial data for decisions.

Definition: Month-end close is the recurring accounting process of verifying transactions, recording needed adjustments, and producing financial statements that accurately reflect the business for the month that just ended.

Pillar one is verification

First, the team confirms that the raw transaction data is complete and accurate. This means matching your internal records to outside evidence.

A simple example is bank reconciliation. Your accounting system says cash changed by a certain amount. Your bank statement shows what cleared. If those don't line up, someone has to find the reason. Maybe a transaction was duplicated. Maybe a deposit was recorded in the wrong month. Maybe a fee hit the bank and never made it into the books.

This same logic applies to credit cards, loans, accounts receivable, and accounts payable. Verification is about making sure the ledger reflects reality.

Pillar two is adjustment

Some important costs and revenues don't land neatly inside one month. That's why accountants post adjusting entries.

Common examples include:

- Accruals for expenses incurred this month but not billed yet

- Prepayments for costs paid in advance that belong to future periods

- Depreciation for long-term assets whose cost is recognized over time

- Payroll-related entries that need to reflect wages and benefits in the right period

This aspect often leads to confusion for owners. They'll say, “If no cash moved, why are we recording it?” Because accounting isn't just tracking the bank balance. It's matching income and expense to the period they belong to.

Pillar three is reporting

After verification and adjustment, the business can produce reports that are useful.

Those reports usually include:

| Report | What it tells you |

|---|---|

| Income statement | Whether the business earned a profit during the month |

| Balance sheet | What the business owns, owes, and has invested at month-end |

| Cash flow statement | How cash moved during the month |

A healthy close ends with reports that tie together. Profit should make sense next to cash movement. Balance sheet accounts should have support behind them. Unusual changes should be explainable.

That's the “under the hood” view. Not glamorous, but powerful. Once those three pillars are done well, the books stop being a record of transactions and become a tool for managing the company.

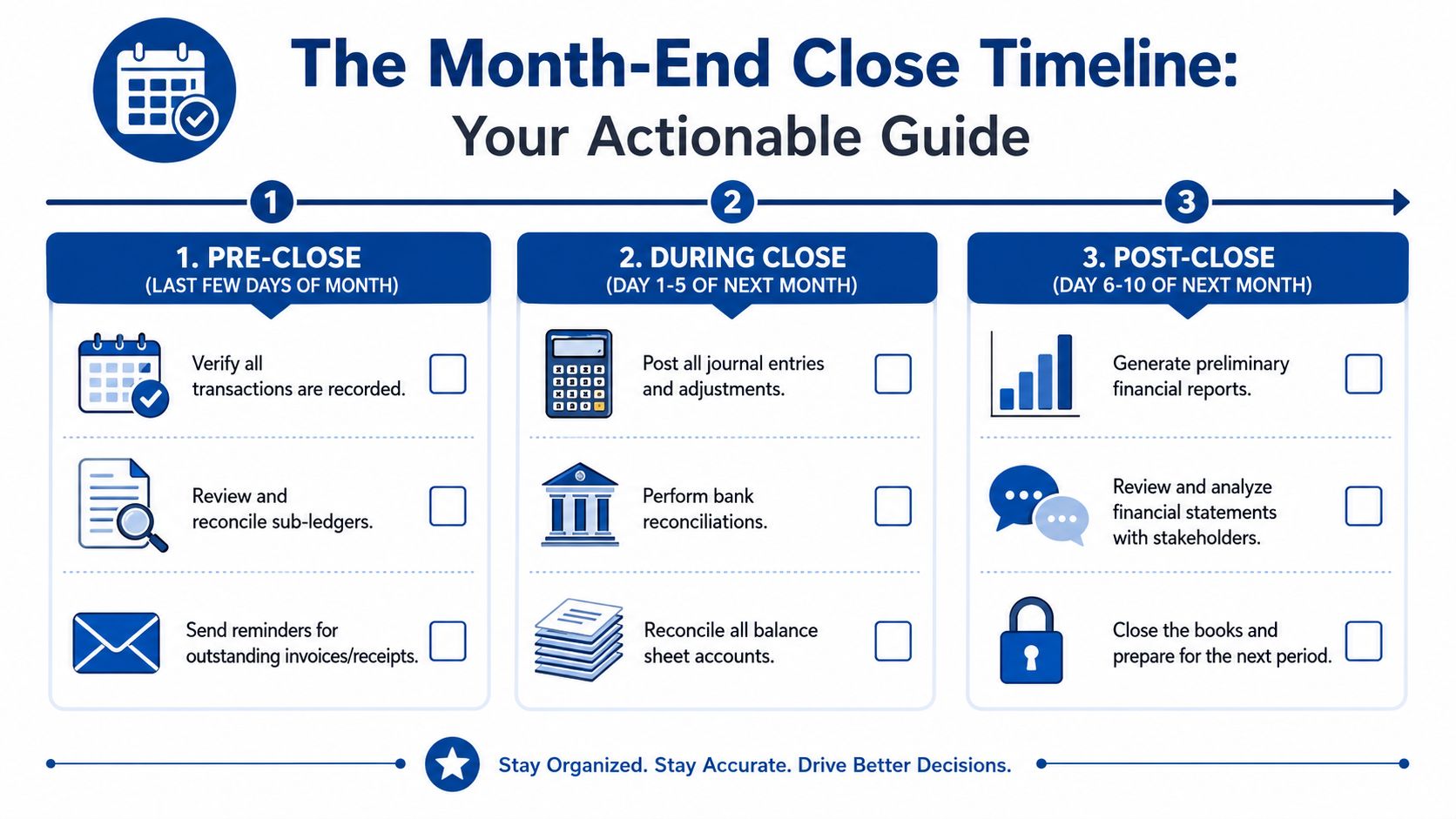

The Canonical Month-End Close Checklist and Timeline

Most owners don't need a more complicated close. They need a more consistent one. A strong close follows a predictable calendar, with work happening before, during, and after the month ends.

This visual lays out the rhythm.

Pre-close work in the last few days of the month

Good closes start before the month is over. If you wait until the first business day of the new month to gather everything, you're already behind.

Key pre-close tasks include:

- Record as much routine activity as possible. Enter customer invoices, vendor bills, payroll data, and recurring expenses before month-end so fewer items pile up afterward.

- Chase missing documents early. Ask team members for receipts, approvals, and expense support while the activity is still fresh.

- Review sub-ledgers. Check accounts receivable and accounts payable detail before close starts. This makes problems easier to spot.

- Confirm recurring entries are ready. Rent, software, loan payments, and payroll-related items often follow a pattern. Prep those in advance.

If your current process feels loose, a documented monthly bookkeeping checklist helps turn tribal knowledge into a repeatable routine.

Core close work in the first business days of the new month

The books move from “mostly there” to final. FloQast's explanation of the month-end close notes several critical steps, including closing revenue and expense accounts to an Income Summary, closing that summary to Retained Earnings, reconciling subsidiary ledgers against the general ledger, and having a Controller perform a final review.

In plain English, the core work usually looks like this:

Reconcile bank accounts and credit cards

This verifies cash activity and catches timing issues, duplicates, bank fees, and missing entries.Review accounts receivable

Confirm invoices were issued properly, payments were applied correctly, and old balances are real. This protects both revenue accuracy and collection planning.Review accounts payable

Make sure vendor bills are entered in the correct period. Otherwise, profit can look better than it really was.Post accruals and other adjustments

Record payroll accruals, benefits, prepaid expenses, and depreciation so the month reflects what was earned and incurred.Reconcile balance sheet accounts

Every meaningful asset and liability account should have support behind it, not just a number sitting in the ledger.Review unusual variances

If travel dropped sharply, software expense spiked, or gross margin shifted, someone should explain why before reports go out.

A walkthrough can help if you want to see the process in motion:

Post-close work after the books are finalized

Closing the books isn't the end. It's when the reports become useful.

After finalization, the team should:

- Generate management reports. Pull the income statement, balance sheet, and cash flow statement.

- Review performance against expectations. Compare actual results to budget, prior periods, or operating targets.

- Document issues from the close. If the same accounts caused delays again, fix the process before next month.

- Lock the period where appropriate. This reduces accidental backdating and keeps reports stable.

Practical rule: A close is only finished when the reports are reviewed, not when the reconciliations are uploaded.

Here's a sample close calendar you can adapt.

| Phase | Timing (Business Days) | Key Tasks |

|---|---|---|

| Pre-close | Last few days of the month | Enter routine transactions, request missing receipts, review AR and AP detail, prepare recurring entries |

| During close | Days 1 to 5 | Reconcile bank and credit card accounts, post accruals and adjustments, review balance sheet accounts, investigate variances |

| Post-close | Days 6 to 10 | Final review, issue reports, discuss results with leadership, document process improvements, lock period |

The exact timing varies by business. What matters is consistency, ownership, and making sure every task has a reason behind it.

Who Owns the Close Roles and Responsibilities

Month-end close breaks down when everyone assumes someone else is handling a key step. Clear ownership matters more than fancy software.

In a smaller service business, one person may wear several hats. In a larger company, the work is split. Either way, the same responsibilities exist.

The bookkeeper handles the foundation

The bookkeeper usually owns the daily flow of data. That includes transaction categorization, recording bills and invoices, posting routine entries, and doing initial reconciliations.

If the bookkeeper misses items or codes them inconsistently, the rest of the close gets slower and more expensive. Reviewers then spend their time cleaning up the base layer instead of analyzing results.

Typical bookkeeper responsibilities include:

- Recording transactions accurately

- Keeping AR and AP current

- Reconciling bank and credit card activity

- Collecting backup documentation

- Flagging unusual items for review

The accountant or controller owns judgment and review

The accountant or controller steps in where judgment matters more. They review reconciliations, post complex adjustments, assess unusual balances, and confirm the books are compliant and internally consistent.

This role is the quality-control function. If the bookkeeper is assembling the puzzle, the controller is checking whether all the pieces fit and whether the final picture makes sense.

A close without review is just organized data entry.

Typical controller or accountant responsibilities include:

| Role area | What this person usually owns |

|---|---|

| Adjustments | Accruals, depreciation, prepaid expense treatment, corrections |

| Review | Balance sheet support, variance analysis, unusual journal entries |

| Controls | Approval flow, documentation standards, final sign-off |

| Reporting | Preparing and reviewing final financial statements |

The owner still has a job

Many owners assume their role ends once the reports arrive. It doesn't.

The owner, operator, or fractional CFO should use the close to ask business questions. Why did margin shift? Why are receivables aging? Why did payroll rise faster than revenue? What changed operationally?

If no one on the leadership side reviews the story behind the numbers, the business misses the full value of the close. The accounting team can tell you what happened. Leadership has to decide what to do about it.

When one person wears every hat

If you're a solo owner with part-time support, don't worry about perfect org charts. Focus on separating tasks mentally. First record. Then reconcile. Then review. Then decide.

That sequence keeps you from making management decisions using unfinished accounting.

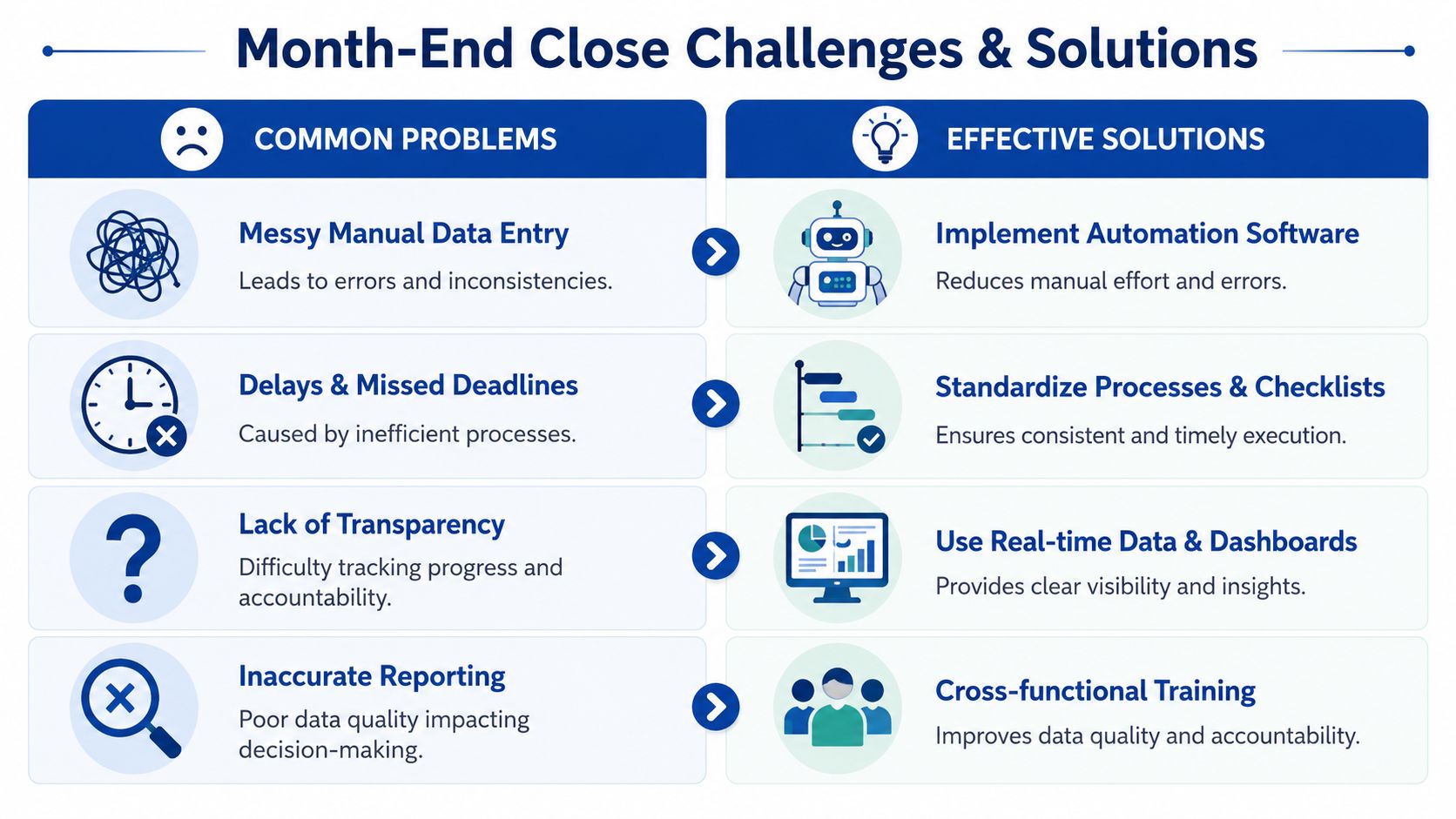

Common Month-End Close Problems and How to Fix Them

Most month-end close problems aren't accounting mysteries. They're process failures with financial consequences. The danger is that owners often normalize them. “We're always late.” “Payroll is always messy.” “We fix things after reports go out.” None of that is harmless.

InScope's discussion of close bottlenecks says 68% of small-to-midsize businesses take 7 to 10 days to close, with manual reconciliation as the main bottleneck. The same source says advanced automation can reduce close time by up to 40% while maintaining audit readiness.

Problem one is manual clutter

When transactions live across spreadsheets, inboxes, bank portals, and separate apps, the close becomes a scavenger hunt. People spend their time gathering information instead of reviewing it.

Fix: reduce handoffs and standardize inputs. Use connected systems where possible. Require receipts and coding support to arrive in one place. Set due dates before month-end, not after.

A close should feel like checking and confirming. If it feels like detective work every month, the intake process is broken.

Problem two is missing or late documentation

Owners often underestimate how much delay comes from waiting on simple items. A missing vendor bill, unsigned expense approval, or uncategorized charge can block review of an entire account.

Fix: create a close calendar with deadlines for non-accounting staff too. Operations, HR, and department heads all feed accounting. If they don't know their deadlines, Finance inherits the delay.

Problem three is weak reconciliations

Some businesses think “reconciled” means the bank feed imported. It doesn't. Reconciliation means the account balance is tied to supporting detail and unexplained differences are resolved.

If that's an area your team struggles with, this guide to reconciling bank accounts is a practical starting point.

Problem four is misunderstanding accruals

Cash basis thinking creates month-end confusion. Owners ask why an expense is recorded before the bill is paid, or why prepaid software isn't fully expensed the month cash leaves the bank.

Fix: decide whether you want reports that mirror cash movement or reports that show actual monthly performance. For management decisions, most growing service businesses need the second view. That requires accrual thinking, even if tax reporting follows a different basis.

Owner check: If your profit swings wildly from month to month because bills and payroll land unevenly, your close may be tracking payment timing instead of business performance.

Problem five is no measurement of close quality

Many teams measure whether they “got through it,” but not whether they did it well. That's like judging a sales process only by whether proposals were sent.

Track a few internal indicators consistently:

- Days to close to see whether the process is speeding up or stalling

- Reconciling items left unresolved to spot sloppy account cleanup

- Post-close adjustments to show how often you're changing numbers after reports were considered done

You don't need a complicated dashboard. You need visibility into whether the process is becoming more reliable month after month.

Streamlining Your Close with Software and Expert Help

A faster close usually comes from better design, not longer hours. If your team spends the first week of each month hunting for receipts, fixing payroll mappings, and matching bank transactions by hand, the problem is the workflow. Software and outside support help by removing routine friction so your team can spend its time reviewing what impacts decisions.

That distinction matters. The goal is not to produce reports a few days sooner for the sake of speed. The goal is to get numbers you can trust while there is still time to act on them. A close completed on the 20th tells you what happened. A close completed on the 5th helps you decide what to do next.

That is where the right tools earn their keep.

In many service businesses, QuickBooks Online handles bank feeds, recurring transactions, and basic account review well. Payroll systems like Gusto and QuickBooks Payroll simplify wage processing and payroll tax filings. Expense platforms collect receipts and approvals in one place. Reconciliation tools flag mismatches so your bookkeeper is not scanning every transaction line by line.

Software helps most when the close process is clear

Software works like a calculator for a math student. It speeds up the mechanics, but it does not decide which formula to use. Month-end close has the same limit. Tools capture transactions quickly, but someone still has to decide whether an item belongs in this month or next month, whether a payroll liability cleared correctly, and whether the final reports make business sense.

Payroll is a good example because it often looks finished before it is fully correct. HighRadius' write-up on month-end close issues explains why payroll-related accruals and prepayments often slow the close and why sync gaps between payroll systems and accounting platforms can create reconciliation problems. In plain English, a successful payroll run does not guarantee accurate month-end financials.

For an owner, the risk is simple. If payroll taxes, benefits, reimbursements, or wage accruals hit the wrong accounts or the wrong month, your profit for the period can be distorted. That can lead to bad decisions about hiring, owner draws, pricing, or cash reserves.

What a stronger close setup looks like

A well-run close combines automation with review rules your team follows every month:

- Bank feeds for transaction capture so cash activity enters the books quickly

- Recurring journal templates for standard monthly entries such as prepaid expenses or software amortization

- Payroll mapping reviews so wage expense, taxes, and benefits post to the correct accounts

- Exception-based reconciliation workflows so staff investigate mismatches instead of manually matching every line

- Period-close controls so finalized reports are not changed without review

For companies that want a tighter reconciliation process, automated reconciliation software can reduce manual matching and make monthly review more consistent.

If your business operates across markets, software selection may also depend on local filing and reporting requirements. In that case, Comfi's UAE accounting software recommendations offer practical context for evaluating tools in that region.

When expert help adds real value

There is also a point where adding one more app does not solve the actual problem. If the books need cleanup, the close depends on one overloaded employee, or the final numbers are still being questioned after reports go out, you need process ownership and review discipline.

That is where an outsourced accounting partner can help. A firm such as Steingard Financial can handle transaction coding, reconciliations, payroll coordination, month-end reporting, and close design around the systems you already use. For a service business owner, that means less time chasing accounting loose ends and more time using current financials to make decisions with confidence.

Good close support changes the value of your accounting function. Instead of producing historical reports after the moment has passed, it gives you a reliable monthly scorecard while choices about staffing, spending, and growth are still in front of you.