You’re probably living some version of this right now. Revenue is coming in. Payroll is going out. Clients are active. Your team is busy. But when you look at your financial reports, they feel like a foreign language.

Maybe your bookkeeper sends a profit and loss statement each month, and you glance at the bottom line without knowing what to do next. Maybe your operations lead is asking whether you can afford to add headcount, while HR is trying to fix retention and you’re not sure which numbers should guide the decision. Maybe cash in the bank looks fine this week, yet you still feel uneasy.

That discomfort usually doesn’t come from a lack of intelligence. It comes from a lack of translation.

Business owners often hear that accounting is the language of business. That’s true, but it’s incomplete. A language only helps if people can use it. Raw reports don’t make decisions. People do. And in most service businesses, the people making daily decisions aren’t accountants. They’re owners, operators, HR leaders, and department heads.

That’s why financial fluency matters. You don’t need to become a CPA. You do need to understand what the numbers are saying, what they’re not saying, and how to turn them into actions your team can follow. Good systems matter here. If you’re trying to tighten the basics before you interpret the story, these Practical bookkeeping workflows give a helpful overview of how disciplined recordkeeping supports clearer reporting.

When the numbers stay trapped inside accounting reports, you’re a passenger. When you can read them, question them, and translate them into pricing, staffing, and operating choices, you’re in the pilot’s seat.

Introduction Are You a Passenger or the Pilot of Your Business

A lot of owners run successful companies while feeling strangely disconnected from the finances. They know sales activity. They know client satisfaction. They know who their best employees are. But when someone asks about margins, liquidity, or whether labor costs are drifting too high, confidence drops fast.

That gap creates a real leadership problem.

If you can’t interpret the numbers behind your business, you end up managing by instinct alone. Instinct matters, but it shouldn’t carry the full weight. Service businesses are especially vulnerable because labor, timing, utilization, payroll, collections, and client delivery all interact. A small reporting error can lead to a bad hiring call, an underpriced engagement, or a delayed response to cash pressure.

What feeling like a passenger looks like

You may be in that position if any of this sounds familiar:

- You review reports after the month is over: By the time you see a problem, the team has already repeated it for weeks.

- You rely on your bank balance: Cash in the account feels reassuring, but it doesn’t tell you what bills are due, what work is profitable, or whether receivables are slipping.

- You hear accounting terms without context: Words like accruals, liabilities, equity, and reconciliations sound technical because no one has translated them into business decisions.

- Your department leaders use different numbers: Operations tracks staffing one way, HR tracks compensation another way, and finance reports something else entirely.

You don’t need more jargon. You need a clearer connection between financial facts and business choices.

What being the pilot looks like

A financially fluent owner asks better questions. Which clients create healthy margins? Is hiring ahead of demand realistic? Are rising payroll costs tied to growth, inefficiency, or retention pressure? Should pricing change before profit gets squeezed further?

That’s what this topic is really about. Not accounting for accounting’s sake. It’s about leadership, control, and calm.

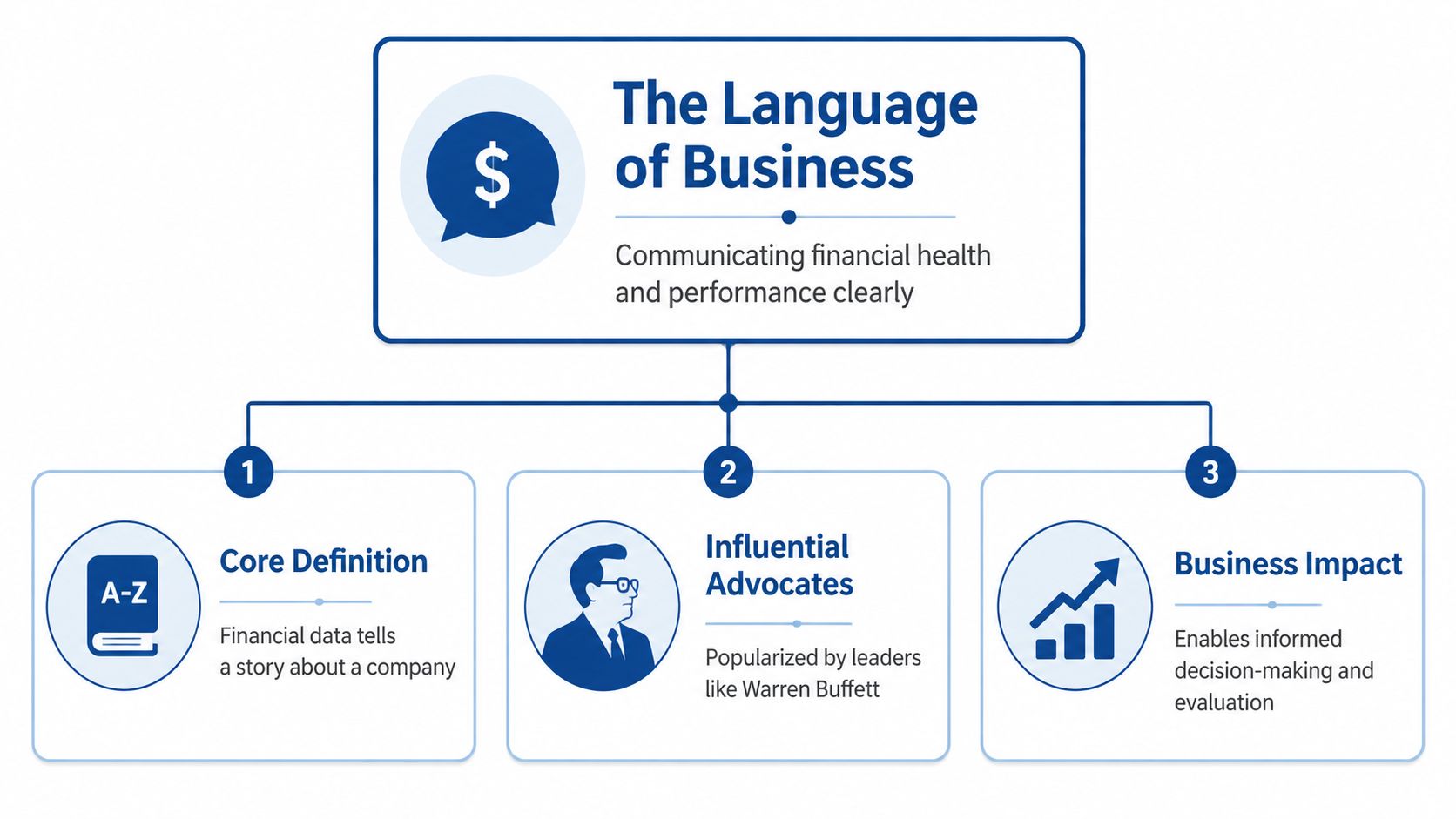

What the Language of Business Really Means

The phrase has been repeated for years because it captures something important. Accounting gives businesses a structured way to describe reality. It translates daily activity into a consistent set of records and reports that other people can understand.

Core idea: Accounting is the system businesses use to record, organize, and communicate what’s happening financially.

The phrase “accounting is the language of business” is widely tied to Warren Buffett’s modern popularization of the idea, building on much earlier foundations including Luca Pacioli’s 1494 work on double-entry bookkeeping. That framework later supported standards such as GAAP and IFRS, and 94% of Fortune 500 companies use those frameworks to present a “true and fair view” of financial health, as described in this overview of accounting’s role in business communication.

Why a business needs a common grammar

Think about what would happen if every department used its own rules for the same event.

Sales counts a contract when it’s signed. Operations counts it when work starts. Payroll reflects staffing costs every pay period. The owner looks at bank deposits. If nobody aligns those views, the company starts arguing about numbers instead of making decisions from them.

That’s why standards matter. GAAP and IFRS act like grammar rules. They help companies classify transactions consistently, present financial statements in a recognizable format, and create trust between the business and the people reading those statements.

Without that consistency, “profit” can mean one thing in one meeting and something else in the next.

Why double entry still matters

Double-entry bookkeeping sounds academic until you see what it protects you from. Every transaction affects at least two accounts. That keeps the accounting equation in balance and gives you a traceable record of cause and effect.

If you buy software, one account changes and another changes with it. If you invoice a client, you haven’t just “made money.” You’ve created revenue and an amount receivable. If payroll runs, wage expense increases and cash or liabilities change too.

That structure matters because it makes the numbers testable.

The point most articles miss

Accounting isn’t a rich human language. It doesn’t explain itself naturally. It records, classifies, and summarizes. Someone still has to interpret it.

That’s where many businesses get stuck. They have books. They have reports. They may even have accurate reports. But they don’t have translation from accounting language into operating language.

HR wants to know whether compensation changes are sustainable. Operations wants to know whether utilization supports another hire. Owners want to know whether growth is healthy or just expensive. The reports contain clues, but the business still needs a translator.

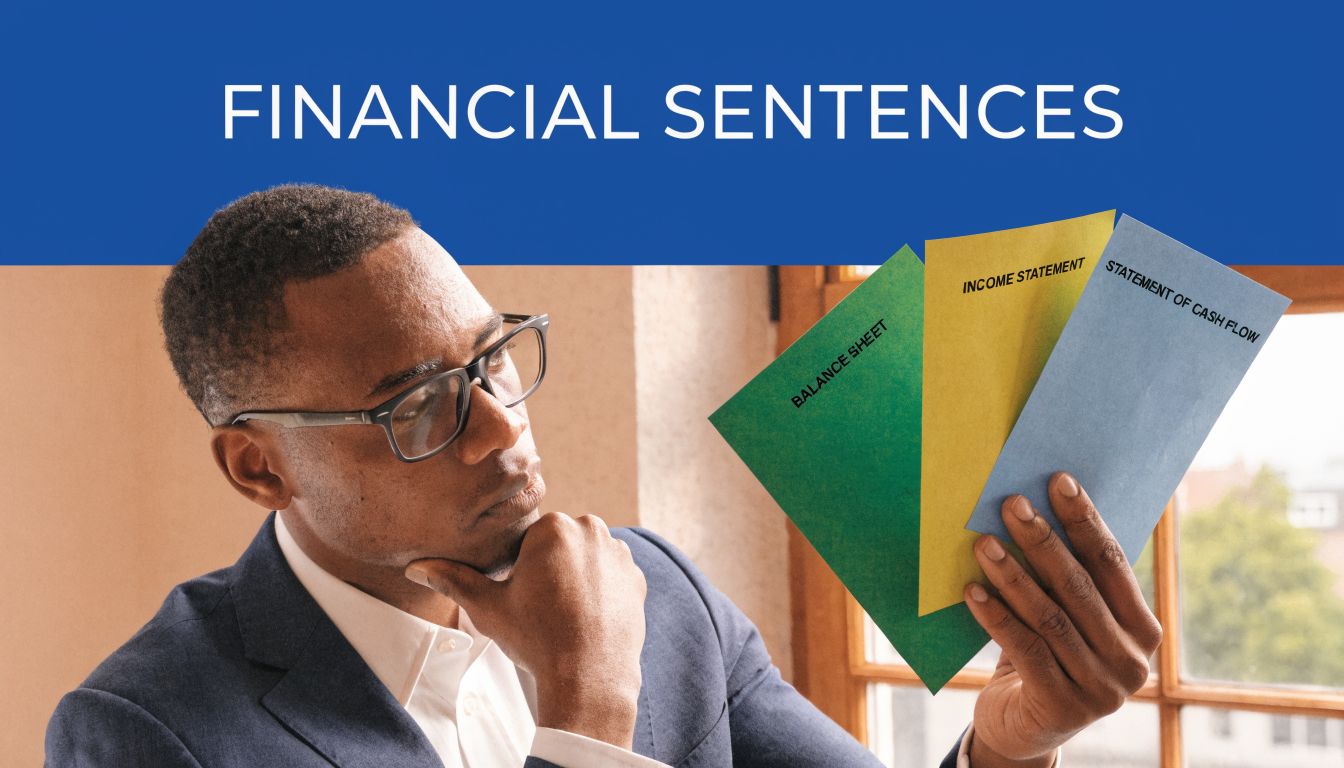

The Three Core Financial Sentences You Must Know

If accounting is the language of business, the financial statements are its core sentences. Most owners don’t need to memorize textbook definitions. They need a simple way to understand what each report is saying.

A practical way to think about them is this. One report shows where you stand. One shows how you performed. One shows what happened to cash.

The balance sheet says what you have and what you owe

The balance sheet is a snapshot on a specific date. It tells you what the business owns, what it owes, and what remains for the owner.

That sounds abstract until you use plain language:

- Assets are things the business has or controls, such as cash, receivables, or equipment.

- Liabilities are obligations, such as unpaid bills, payroll liabilities, or debt.

- Equity is the residual interest after liabilities are accounted for.

If your service business looks profitable on paper but receivables are piling up and liabilities are growing, the balance sheet will often reveal the tension before your bank account does.

A lot of confusion starts here because owners assume “doing well” means “having cash.” Those aren’t the same thing. A business can show strong sales and still carry stress in collections, debt, or timing.

The income statement says whether your work is profitable

The income statement, often called the profit and loss statement, covers a period of time. It shows revenue earned and expenses incurred during that period.

This is your performance report. It answers questions like:

- Are we charging enough?

- Is payroll rising faster than revenue?

- Are overhead costs eating into profit?

- Which months are stronger or weaker?

For a service business, this report often tells the clearest story about pricing discipline and labor efficiency. If revenue grows but profit doesn’t, something in delivery, staffing, or expense control needs attention.

If you want a broader explanation of how these reports fit together, this guide on the 4 financial statements is a useful companion.

The cash flow statement says where the money actually went

The statement of cash flows is the reality check. It explains how cash moved through the business.

This is the report owners often wish they had looked at sooner. You can show profit on the income statement and still feel cash pressure because cash timing follows different rules. Clients may pay late. Equipment may have been purchased. Debt may have been repaid. Payroll may have hit before receivables cleared.

Profit answers whether the business earned money. Cash flow answers whether the business had money available when it needed it.

That distinction is where many smart owners get tripped up.

This short video gives a straightforward visual explanation of how the statements relate to one another.

How to read them together

One report alone can mislead you. The balance sheet may show growing receivables. The income statement may show rising revenue. The cash flow statement may show tightening cash. Together, they tell a fuller story: sales are being booked, but collections aren’t keeping pace.

That’s why owners should stop asking, “Did we make money?” and start asking a better set of questions.

- What changed in our position

- What drove profitability

- What happened to cash

- What should we do differently next month

Those are leadership questions, not accounting questions.

From Financial Reports to Smart Business Moves

Financial statements matter because they support decisions. If they stay locked in monthly PDFs, they become historical paperwork. If you turn them into operating questions, they become management tools.

Standardized financial statements help businesses make decisions about pricing and expansion. They support analysis such as markup decisions that produce 25% to 40% gross margins, ROI forecasts with a greater than 15% hurdle rate, and can help audited, GAAP-compliant companies secure 15% lower borrowing costs on average, as described in this discussion of accounting precision and strategic growth.

The key shift from reporting to action

Most owners don’t need more reports. They need fewer, better metrics tied to real choices.

A useful KPI should answer a decision question. If it doesn’t guide a decision, it’s usually just trivia.

Practical rule: Every KPI should connect to one choice your team can actually make.

Here’s a working reference for service businesses.

| KPI | What It Measures | Why It Matters for Service Businesses |

|---|---|---|

| Gross Margin | The portion of revenue left after direct service delivery costs | Helps you judge whether your pricing and delivery model leave enough room to cover overhead and profit |

| Net Margin | What remains after all operating costs | Shows whether growth is healthy or whether the business is getting bigger without becoming stronger |

| Current Ratio | Current assets compared with current liabilities | Helps assess short-term financial stability and whether you can cover near-term obligations |

| Customer Acquisition Cost | What it costs to win a new client | Shows whether sales and marketing spending is sustainable relative to client value |

| Accounts Receivable Aging | How long client invoices remain unpaid | Helps you spot collection friction before cash stress becomes visible in the bank account |

| Payroll as a Share of Revenue | How much of revenue is consumed by labor | Critical in service businesses where people costs often shape profit more than almost anything else |

| Revenue per Employee | Revenue generated relative to team size | Helps owners evaluate staffing efficiency and hiring timing |

| Utilization or Billable Capacity | The share of team time spent on client-producing work | Useful for firms that need to balance workload, hiring, and pricing |

What these KPIs help you decide

A gross margin discussion isn’t just about percentages on a report. It’s about whether your projects are priced well enough to support account management, recruiting, software, admin time, and owner compensation.

A current ratio conversation isn’t just a finance exercise either. It can affect whether you delay a hire, renegotiate payment terms, or push harder on collections.

A payroll-to-revenue review becomes an HR and operations conversation quickly. If payroll rises while margin shrinks, the answer may be higher pricing, improved utilization, a different staffing mix, or better scope control. The metric doesn’t make the decision. It tells you where to investigate.

Questions to ask when a KPI moves

Instead of reacting emotionally, use a short diagnostic list:

- If margin drops: Did pricing slip, labor time expand, or client mix change?

- If cash tightens: Are receivables aging, expenses jumping, or liabilities bunching up?

- If payroll climbs: Is this growth investment, inefficiency, overtime pressure, or retention correction?

- If net profit weakens: Which expenses are fixed, and which are controllable in the next cycle?

The value of accounting isn’t in producing elegant reports. It’s in helping your team choose the next move with better evidence.

Common Bookkeeping and Payroll Mistakes to Avoid

Bad accounting data doesn’t just create messy books. It creates bad decisions.

When bookkeeping errors stack up, the language of business gets distorted. You think one service line is profitable when it isn’t. You believe cash is healthier than it is. You assume payroll is under control when liabilities are building behind the scenes.

Mistakes that corrupt the signal

Some of the most common problems in service businesses are surprisingly ordinary.

- Mislabeled transactions: If software, contractors, owner draws, reimbursements, or client-related costs are posted to the wrong accounts, your reports stop reflecting reality.

- Unreconciled bank and credit card accounts: If transactions in QuickBooks don’t match actual statements, you’re making decisions from incomplete records.

- Messy accounts receivable: Revenue may look strong while unpaid invoices stretch further out.

- Messy accounts payable: Expenses may be understated if bills are sitting outside the accounting system.

- Payroll coded inconsistently: Labor costs lose meaning if wages, taxes, benefits, and reimbursements aren’t categorized cleanly.

These are not minor clerical issues. They change the story your numbers are telling.

Payroll mistakes carry extra risk

Payroll problems deserve special attention because they affect both compliance and management visibility.

If payroll liabilities aren’t tracked correctly, the books may understate what the business owes. If employee-related costs are split across the wrong categories, leaders can’t tell what labor costs. If pay runs are posted late or inconsistently, month-end reports stop lining up with operational reality.

If you want a practical breakdown of what sits inside these obligations, this explanation of payroll liabilities helps clarify what business owners should be watching.

Clean books don’t exist to satisfy an accountant. They exist so the owner, HR lead, and operations manager can trust the same numbers.

The operational damage from inaccurate books

Once accounting data goes off course, every downstream conversation gets harder.

HR can’t evaluate compensation decisions clearly. Operations can’t see whether staffing is aligned with demand. Owners hesitate on pricing because they don’t trust margin. Strategic meetings turn into debates about whose spreadsheet is right.

The fix isn’t glamorous, but it’s powerful:

- Reconcile accounts consistently

- Keep the chart of accounts clean and usable

- Review AP and AR regularly

- Post payroll accurately and on time

- Close the month with the goal of decision usefulness, not just completion

Businesses don’t need perfect books for vanity. They need reliable books so they can act before problems harden.

Speaking Fluent Finance with Modern Tools and Partners

Software has made accounting faster. It hasn’t made it self-explanatory.

QuickBooks Online can record transactions, organize accounts, and produce reports. Gusto can run payroll and track people-related data. Dashboards can surface trends quickly. But tools don’t solve the hardest problem by themselves. They don’t translate accounting output into operational judgment.

That’s the gap many service businesses feel but struggle to name.

The challenge isn’t only whether the books are accurate. It’s whether different departments can use the information. As noted in this analysis of accounting’s limits as a metaphor, teams often speak different “accounting dialects,” and value sits in the translation layer that turns month-end statements into decisions HR and operations can act on.

What the translation layer actually does

A translation layer takes financial data and rewrites it in the language each team needs.

For example:

- For HR: Payroll data becomes compensation visibility, hiring affordability, and retention context.

- For Operations: Revenue and labor data become staffing plans, utilization decisions, and delivery efficiency insights.

- For Owners: Combined reporting becomes a clearer view of margin, cash timing, and growth quality.

The accounting file may say wages increased. That’s only the start. Someone still has to determine whether the increase came from planned hiring, overtime, retention adjustments, administrative bloat, or client delivery expansion.

Tools help when the setup is thoughtful

This is where system design matters. A messy chart of accounts, inconsistent class tracking, poor vendor naming, or payroll mapping that collapses everything into one generic labor line makes meaningful analysis much harder.

Even upstream data handling matters. If your team still receives statements in awkward formats during cleanup or historical review, tools that help convert bank statement PDFs to Excel can make early-stage organization easier before data is validated and entered properly.

The software choice matters too. Startups and growing firms often need a setup that fits both current complexity and future reporting needs. If you’re weighing systems, this guide to best accounting software for startups is a useful place to compare options.

Why non-financial teams need translated reporting

A service business doesn’t win because the general ledger is elegant. It wins because leaders make coordinated decisions.

When finance, HR, and operations use the same facts but hear them in their own business language, execution gets cleaner.

That could mean monthly reports being turned into questions such as:

- Which roles are driving delivery bottlenecks?

- Is compensation aligned with client economics?

- Are we hiring ahead of revenue or behind demand?

- Which client segments support healthier staffing plans?

Those are translation-layer questions. They sit between bookkeeping and strategy. And for many companies, that middle layer is where the core value gets created.

Becoming a Fluent Leader Your Partner for Growth

Financial fluency doesn’t mean you need to prepare journal entries or master every rule in the accounting literature. It means you can lead from the numbers instead of reacting to them after the fact.

A fluent leader knows how to read the core statements, spot when data quality is weak, and ask the questions that turn reports into action. More important, that leader makes sure finance doesn’t stay trapped inside the accounting function. The numbers need to reach HR, operations, and management in a form they can use.

That’s the deeper truth behind the phrase accounting is the language of business. It’s not just about compliance or reporting. It’s about communication. Clear books help people align. Accurate payroll data helps teams plan. Consistent financial statements help owners make steadier decisions under pressure.

You don’t have to do all of that alone. Smart owners often hand off the technical grammar of accounting so they can focus on leadership, clients, and growth. That isn’t a weakness. It’s usually a sign that the business is maturing.

If your numbers feel noisy, late, or hard to apply, the next step isn’t more spreadsheets. It’s better translation. Once the data becomes understandable and decision-ready, the business gets easier to steer.

If you want cleaner books, clearer payroll visibility, and reporting that helps leaders make decisions, Steingard Financial supports service businesses with bookkeeping, payroll, and people advisory built for real-world operations. Their team helps turn financial data into useful insight so you can lead with more confidence and less guesswork.