Your office manager buys stamps. Your intern covers parking for a client meeting. Someone grabs printer paper on the way in because the team ran out right before a proposal deadline. None of these purchases is a big deal on its own. The headache starts later, when the receipt is missing, the reimbursement sits in limbo, and your bookkeeper has to guess where the expense belongs.

That's where a petty cash fund earns its keep.

Used well, it gives a service business a clean way to handle small, immediate purchases without turning every coffee run or office supply stop into an accounts payable event. Used poorly, it creates messy books, weak controls, and tax problems that show up long after the cash is gone.

For most service firms, the question isn't whether small incidental spending exists. It does. The question is whether you'll manage it with a real process or let it drift into ad hoc reimbursements, uncategorized transactions, and missing support. The difference shows up in your QuickBooks file, your month-end close, and your confidence in the numbers.

The Hidden Costs of Small Office Expenses

A new client is coming in at 10 a.m. Someone notices there's no coffee, no cups, and no pastries for the meeting. An employee runs out, pays personally, and comes back with a bag, a paper receipt, and the expectation of a quick repayment.

That seems harmless until the follow-up starts. The receipt gets folded into a pocket. The reimbursement request comes in days later. The expense lands in the wrong category, or doesn't get recorded at all. Then a second employee asks to be paid back for parking, and a third wants reimbursement for mailing documents.

Small expenses don't break a business. Unstructured handling of small expenses does.

A petty cash fund solves a very ordinary problem. It creates a pre-approved pool for minor business purchases, with a record attached to every dollar that leaves the box. That means fewer informal reimbursements, fewer loose receipts, and fewer judgment calls during bookkeeping.

Small operational leaks usually don't look dramatic. They look like five minor transactions no one documented correctly.

This is also an operations issue, not just an accounting issue. When owners and office managers spend time sorting out tiny purchases, they're losing time on work that moves the business forward. Teams that want cleaner back-office execution often pair financial discipline with process discipline elsewhere too, including automating recurring routines with Recurrr so small administrative tasks don't keep piling up.

Where the friction shows up

- Employee reimbursements drag on when there's no standard process for immediate purchases.

- Receipts disappear because people don't treat a one-off cash expense like a formal accounting event.

- Month-end gets harder when the bookkeeper has to reconstruct what happened from memory and fragments.

- Reporting gets weaker because small expenses end up miscoded, duplicated, or omitted.

A petty cash fund won't fix every spend-management problem. It will fix one specific one very well when you set it up with discipline.

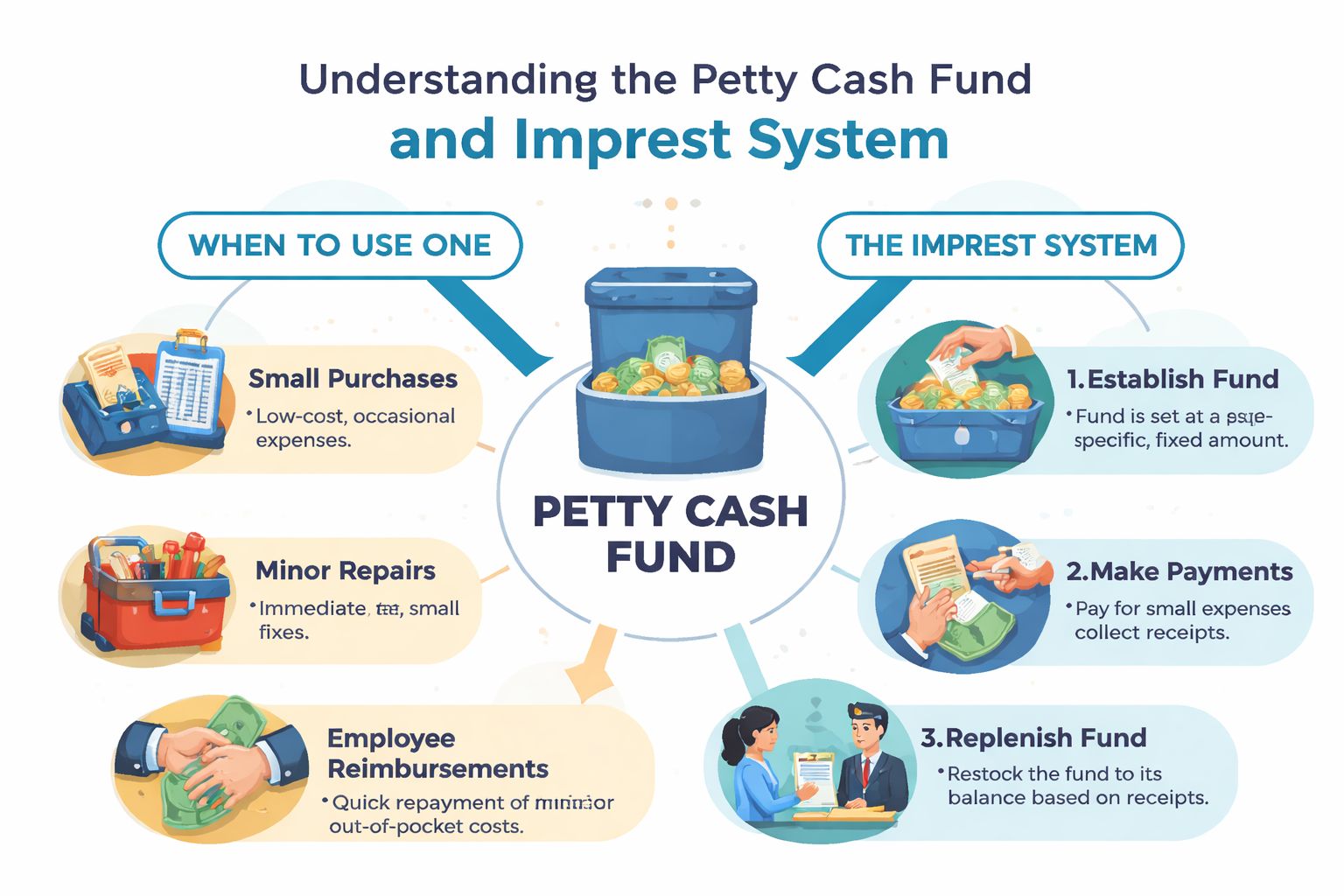

What Is a Petty Cash Fund and When to Use One

A petty cash fund is a small amount of company cash set aside for incidental business purchases that aren't worth putting through a full approval or reimbursement cycle. Think of it as an internal convenience tool with rules.

Most petty cash funds fall in the $50 to $500 range, depending on the business's needs, and the system most companies use is the imprest system, which was formalized in the early 20th century to manage small expenses efficiently while keeping them traceable for bookkeeping and tax purposes, as explained in Patriot Software's petty cash accounting overview.

The imprest idea in plain English

With an imprest fund, you set a fixed balance and keep it there. If your fund is set at a certain amount, the combination of cash remaining plus vouchers and receipts collected should always tie back to that total. You don't keep changing the size casually. You spend from it, document each use, and replenish it back to the approved amount.

That's why petty cash can work. It's simple, but it's not informal.

Good uses for a petty cash fund

For a service business, petty cash is appropriate when the expense is both small and immediate. Common examples include:

- Postage and courier drop-offs when someone needs to send documents right away

- Client parking or meter fees tied to a meeting

- Emergency office supplies like tape, batteries, or pens

- Minor refreshments for an in-office meeting

- Small out-of-pocket repayment when an employee had to cover a legitimate business purchase on the spot

These uses have one thing in common. They're low-dollar, occasional, and operationally inconvenient to process through a slower system.

Bad uses for a petty cash fund

Petty cash should not become a side channel for regular business spending.

Avoid using it for:

- Payroll or wages

- Contractor payments

- Inventory purchases

- Recurring bills

- Travel advances or major travel costs

- Personal items with a promise to repay later

Practical rule: If the expense is predictable, recurring, or large enough to deserve normal approval, it shouldn't go through petty cash.

For many firms, the right answer is a narrow petty cash policy, not a broad one. If nearly all your vendors accept cards and your team works well with digital reimbursements, you may only need a very small fund, or none at all. But if your office still runs into occasional cash-only or immediate purchases, a controlled petty cash fund remains useful.

How to Set Up and Fund Your Account

A petty cash fund works only when one person owns it and everyone else follows the same rules. Setup matters because during this stage you decide whether the fund will behave like a controlled asset or a loose drawer of money.

To formally establish a fund, a department head typically submits a memo to the controller specifying the amount, often capped at $500 without higher approval, the designated custodian, and the relevant chart of accounts. That approval creates the audit trail from the start, as outlined in Wentworth Institute's petty cash policy.

Pick the custodian first

Choose one custodian. Not two, not “whoever is at the front desk,” and not a rotating cast of employees.

That custodian should be responsible for:

- Holding the cash

- Releasing funds only for approved purposes

- Collecting receipts and vouchers

- Keeping the running balance current

- Requesting replenishment when needed

When multiple people informally control the fund, accountability disappears fast.

Decide on the right amount

Don't choose the fund size by instinct. Review the kind of minor purchases your office makes. If your team rarely uses cash, keep it small. If your office regularly handles mailing, parking, or walk-in supply purchases, size it to match real usage while staying conservative.

A smaller fund is easier to control. Idle cash creates risk without adding operational value.

Fund it correctly

Once approved, issue the cash through a recorded transaction, not an off-the-books withdrawal. In practice, that means creating the petty cash asset in your books and moving funds from the bank account into the cash box.

At this point, treat the physical setup as part of the accounting system.

- Use a locked box so the cash isn't sitting loose in a drawer.

- Store it in a limited-access location such as a locked cabinet or office.

- Keep blank vouchers nearby so every disbursement is documented immediately.

- Create a receipt habit from day one. If your team needs a process, this guide on how to organize business receipts is a practical place to start.

Write the ground rules before first use

A simple setup checklist beats a long memo no one reads. Before the first dollar goes out, define:

| Setup item | What to decide |

|---|---|

| Custodian | Who controls access and recordkeeping |

| Fund amount | How much cash the business will keep on hand |

| Storage | Where the cash box stays and who can access it |

| Allowed expenses | What qualifies for petty cash use |

| Documentation | What receipt or voucher is required |

| Replenishment | Who approves refill requests and how often |

The businesses that struggle with petty cash usually don't fail at accounting. They fail at setup.

Creating Ironclad Internal Controls and Policies

A petty cash fund without controls is a weak point in your financial process. It's cash, which means it moves quickly and leaves little room for sloppy habits. If your team treats it casually, your books will reflect that.

According to the ACFE, cash-related schemes, including petty cash fraud, account for 11% of all asset misappropriation cases, and key controls include appointing a single custodian, requiring dual signatures, and maintaining detailed vouchers, as summarized in Ramp's guide to petty cash funds.

That number matters because it reframes petty cash. This isn't just about convenience. It's about controlling a category of risk that businesses often underestimate because each individual transaction is small.

What strong petty cash control looks like

The best petty cash policies are boring. That's a compliment. They leave very little room for interpretation.

Start with these essential requirements:

- One custodian only. Everyone should know who holds the fund and who can release cash.

- A voucher for every disbursement. The voucher should capture the date, amount, business purpose, and signatures.

- Original receipts whenever available. A missing receipt should be an exception that gets documented, not routine practice.

- Manager approval for larger or unusual items. Don't let “small cash” become shorthand for “no approval needed.”

- No IOUs. Ever. An IOU is not support for a business expense.

- A running balance log. The custodian should know the fund position at all times.

If the money leaves the box before the paperwork exists, control has already weakened.

Essential Petty Cash Policy Components

| Policy Component | Description & Rationale |

|---|---|

| Fund purpose | Define that the fund is only for minor, incidental business expenses |

| Custodian responsibility | Assign one person to hold cash, issue disbursements, and maintain records |

| Approved expense types | List what's allowed so employees don't treat the fund like general reimbursement cash |

| Prohibited uses | Exclude personal purchases, wages, loans, advances, and recurring vendor payments |

| Documentation standard | Require receipts or vouchers with date, amount, purpose, and recipient signature |

| Approval process | Identify when supervisor approval is required before cash is released |

| Reconciliation frequency | State how often the fund is counted and reviewed |

| Shortage handling | Explain how overages and shortages are documented and escalated |

| Storage and access | Require a locked box and limited access to the physical cash |

| Audit rights | Reserve the right for spot checks by someone other than the custodian |

The policy has to match your team

A five-person office doesn't need the same petty cash procedure as a multi-location business. But every company needs clarity. If your office manager has to guess whether team lunch, client snacks, or parking is allowed, the policy is incomplete.

Many small businesses benefit from building petty cash into their broader control environment rather than treating it as an isolated office issue. A stronger framework for approvals, segregation of duties, and documentation makes the whole finance function better. If you're tightening processes more broadly, this overview of internal controls for small business is a useful companion.

What doesn't work

Weak petty cash systems usually fail in familiar ways:

- Shared access means no one owns discrepancies.

- Receipts collected later means details get forgotten.

- Unclear expense rules invite arguments and exceptions.

- Infrequent review lets problems sit too long.

A written policy is what turns petty cash from “cash in a box” into a manageable accounting process.

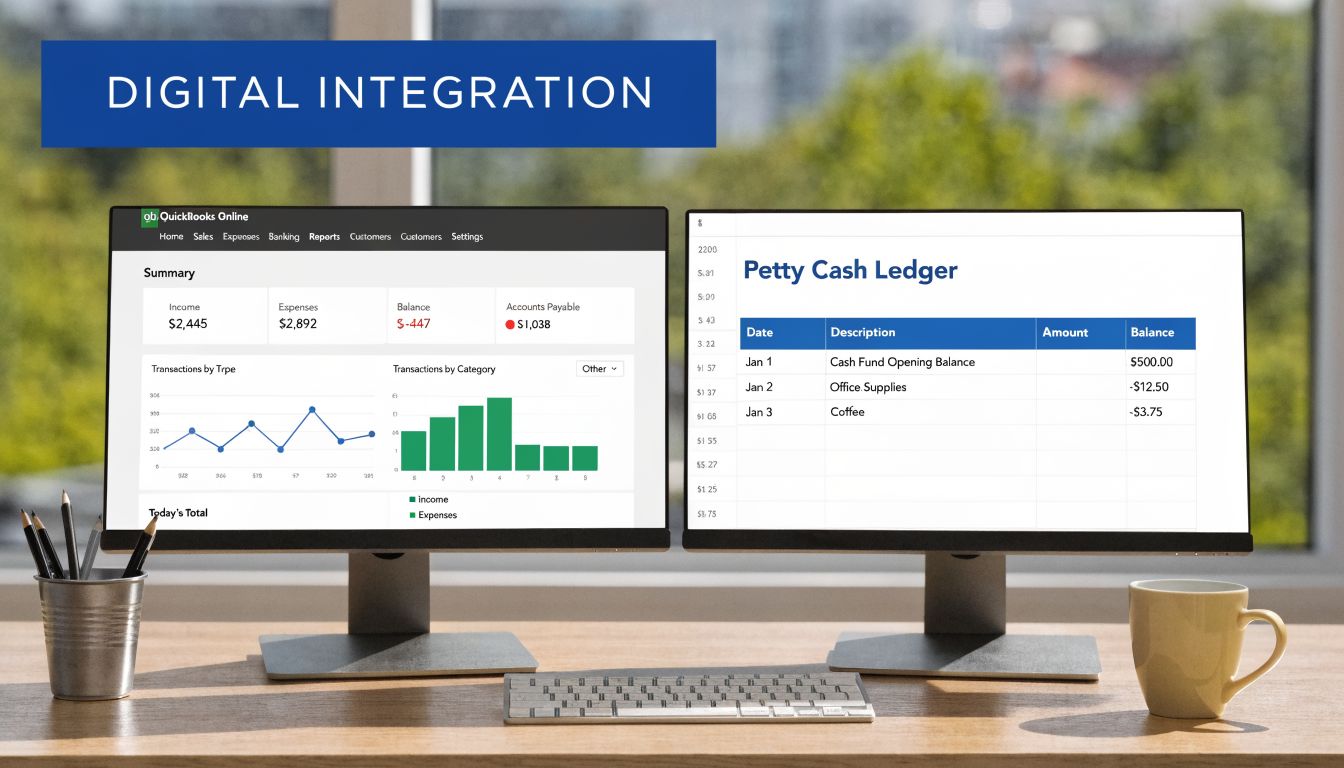

Petty Cash Accounting and QuickBooks Integration

The accounting side of a petty cash fund is where many businesses get off track. The physical box may be organized, but if the bookkeeping entry is wrong, your reports are still wrong.

Mishandling petty cash in QuickBooks is a common source of tax compliance issues. Businesses that fail to properly categorize reimbursements risk having legitimate deductions disallowed during an IRS audit, which is why proper setup and reconciliation matter, as noted in Kevin Harper CPA's discussion of petty cash and tax compliance.

How the accounting works

At setup, you create the petty cash fund as an asset account. In QuickBooks Online, that usually means an Other Current Asset account, often labeled something like Petty Cash.

The opening entry is straightforward. You debit Petty Cash and credit your bank account for the amount used to establish the fund.

After that, you typically don't book each small transaction one by one to the general ledger. Instead, the custodian keeps receipts and vouchers in the box, and the bookkeeper records expenses at replenishment.

What replenishment should look like

When the fund gets low, don't just refill it and move on. Review the support, group the spending by category, and record one replenishment entry tied to the receipts collected.

That entry generally does two things:

- Debits the relevant expense accounts based on what the cash was used for

- Credits the bank or operating cash account for the amount needed to restore the fund

That way, your financial statements reflect the actual nature of the spending, not just a vague “miscellaneous cash” bucket.

Bookkeeping rule: The petty cash asset shouldn't drift up and down every time someone buys tape or pays for parking. The expenses belong in the P&L when you replenish based on documentation.

A practical QuickBooks workflow

For a service business using QuickBooks Online, the cleanest workflow usually looks like this:

- Create the account under Other Current Assets.

- Fund the box from the operating bank account.

- Maintain a manual or spreadsheet ledger with receipts and running balance.

- Enter replenishment as an expense or check transaction, splitting lines by expense category.

- Attach support if you use digital receipt storage.

- Reconcile the petty cash balance against cash on hand plus vouchers before closing the month.

If you're building your file from scratch or cleaning up an older chart of accounts, this walkthrough on how to set up QuickBooks Online helps establish the structure before small cash activity starts cluttering the books.

Why categorization matters

The most common mistake isn't theft. It's laziness in coding.

When a replenishment is recorded in a single broad account, you lose visibility into where the money went. Office supplies, parking, postage, staff refreshments, and client-related costs do not belong in the same generic line if you want reliable reporting.

This short video gives a useful visual explanation of the workflow:

For many service businesses, petty cash is manageable inside QuickBooks if transaction volume is low and the process is disciplined. If the fund generates repeated cleanup work, it's often a sign that the business needs tighter coding standards or a different spend method for certain purchases.

Common Pitfalls and Outsourced Bookkeeping Solutions

Most petty cash problems don't start with fraud. They start with shortcuts. Someone borrows from the box and promises to bring the receipt later. Two people have the key. Replenishment happens only when someone notices the cash is almost gone. By then, nobody remembers what a few transactions were for.

A core principle of a secure petty cash fund is the imprest basis, where the fund is restored to its original fixed amount and the custodian must always have cash plus vouchers equaling that total. If the balance isn't reconciled daily or weekly, shortages can develop and must be written off as losses, according to Hartnell College's petty cash guidelines.

The mistakes that cause the most trouble

- Multiple users controlling the fund weakens accountability.

- IOUs instead of receipts turn business records into guesswork.

- Delayed reconciliation makes shortages harder to explain.

- Poor categorization in QuickBooks turns a simple cash process into a tax and reporting issue.

For some businesses, the right answer is to keep the fund but tighten the process. For others, the better answer is outside oversight. An outsourced bookkeeping team can review the receipts, record replenishment correctly, reconcile the fund as part of the monthly close, and flag patterns that suggest the fund is being used for the wrong kinds of spending. That's where a provider such as Steingard Financial fits into the workflow, particularly for service businesses already using QuickBooks and structured month-end reporting.

A petty cash fund should make life easier. If it's creating uncertainty in your books, the system needs attention.

If your team wants a petty cash process that doesn't turn into cleanup work at month-end, Steingard Financial can help you build the accounting structure around it. That includes QuickBooks setup, transaction categorization, reconciliations, and the reporting discipline that keeps even small cash expenses from becoming bigger compliance problems.