You sent the invoice weeks ago. The work is done, the client approved it, and the revenue is already in your books. But cash still hasn't arrived.

That gap is where many business owners get tripped up. Your profit and loss statement may show a sale, while your bank account tells a less reassuring story. Some invoices will get paid late. A few may need collection follow-up. Some won't be collected at all.

That's why the allowance for credit losses matters. It gives your financial statements a realistic filter. Instead of assuming every dollar in accounts receivable will turn into cash, you record an estimate of what probably won't. For service businesses, that estimate can feel awkward because you may not have years of clean write-off history, and your client mix may change quickly.

What Is an Allowance for Credit Losses

An allowance for credit losses is a valuation account that reduces receivables to the amount you expect to collect. Think of it as a built-in reality check for your balance sheet.

If your books show $200,000 of accounts receivable, that doesn't automatically mean $200,000 will land in the bank. Some customers may dispute invoices, run into cash problems, or disappear. The allowance records that expected shortfall before the loss becomes obvious.

Under current accounting rules, this isn't just a “wait and see” exercise. For small and mid-sized service businesses, the practical challenge is estimating lifetime expected losses when historical write-off data is limited or your customer base changes quickly. CECL requires that forecast, but it doesn't prescribe one single method, so choices like how you pool receivables by risk can materially change the result, as discussed in CohnReznick's CECL implementation roadmap.

What this means in plain English

You're not trying to predict the future with precision. You're trying to avoid overstating assets.

Here's a simple perspective:

- Accounts receivable shows what customers owe you.

- Allowance for credit losses shows what you don't expect to collect.

- Net receivables shows the amount that's realistically likely to convert to cash.

That distinction matters for owners, lenders, and anyone reviewing your financial statements.

Practical rule: If your receivables include old invoices, concentrated customer risk, or clients with changing payment habits, your books need more than optimism.

Why business owners get confused

Many owners learned the older phrase “allowance for doubtful accounts.” The concept is related, but the current framework is broader and more forward-looking. It asks management to consider not only past write-offs, but also current conditions and a reasonable view of what may happen next.

If you want a bank-oriented explanation of how this reserve functions as a credit-risk measure, Visbanking's allowance for credit losses is a useful reference point, even though service businesses apply the idea to receivables rather than loan portfolios.

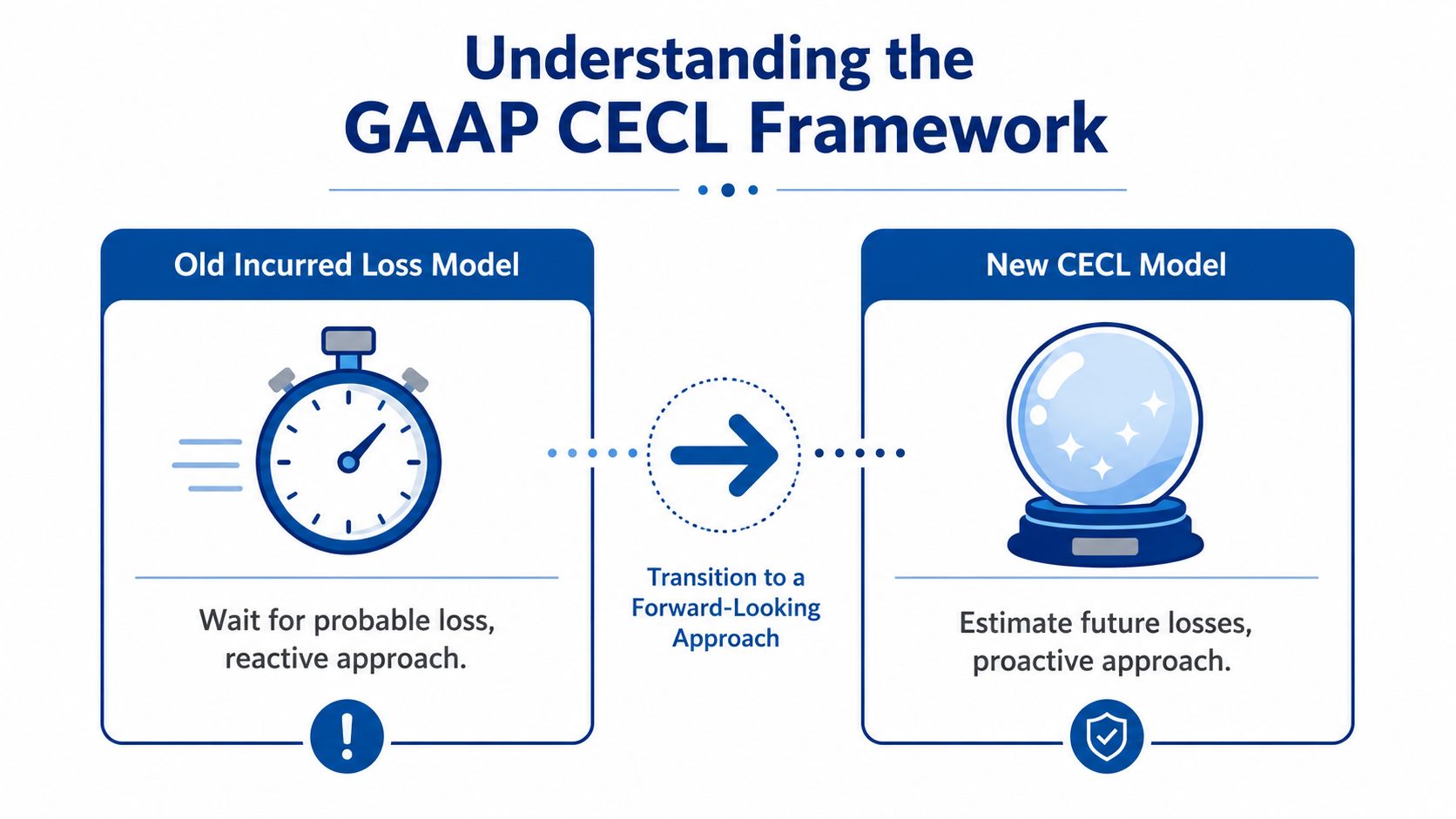

Understanding the GAAP CECL Framework

Older accounting guidance was closer to driving by looking in the rearview mirror. You waited until a loss looked probable, then recorded it. CECL is more like driving with navigation that also shows traffic ahead. You still use historical information, but you also consider present conditions and a supportable forecast.

The core change

Under CECL, the allowance isn't a reserve for “probable” losses. It's a valuation account measured as the difference between an asset's amortized cost basis and the net amount expected to be collected over the contractual term, using past events, current conditions, and reasonable and supportable forecasts, as outlined by the Texas Department of Banking's CECL examination guidance.

For a service business, that means trade receivables usually can't be evaluated with a once-a-year rough guess. Management needs a repeatable method that reflects the risk in the receivables on hand.

Why CECL was such a big deal

This wasn't a minor accounting tweak. In banking, CECL represented a major change in timing and reserve levels. The Federal Reserve found that adoption alone caused an immediate 37% increase in adopters' allowances on January 1, 2020, and excluding the adoption effect, allowances rose 76% in the first half of 2020 versus 2019:Q4 levels, compared with 32% for non-adopters, according to the Federal Reserve's analysis of CECL during the pandemic.

You may not run a bank, but the lesson applies. Once accounting moves from delayed recognition to expected-loss recognition, the allowance becomes more sensitive to your assumptions, customer risk, and reporting discipline.

Where owners usually stumble

Most confusion comes from three places:

| Issue | What owners often assume | What CECL expects |

|---|---|---|

| Timing | Record losses after a clear problem appears | Estimate expected losses earlier |

| Data | Past write-offs alone are enough | Use history, current conditions, and forecast inputs |

| Method | There must be one required formula | A supportable method is acceptable if applied consistently |

CECL doesn't require perfect forecasting. It requires a reasonable, documented estimate that you can explain.

That's a huge relief for service businesses. You don't need a giant model. You do need logic, consistency, and documentation.

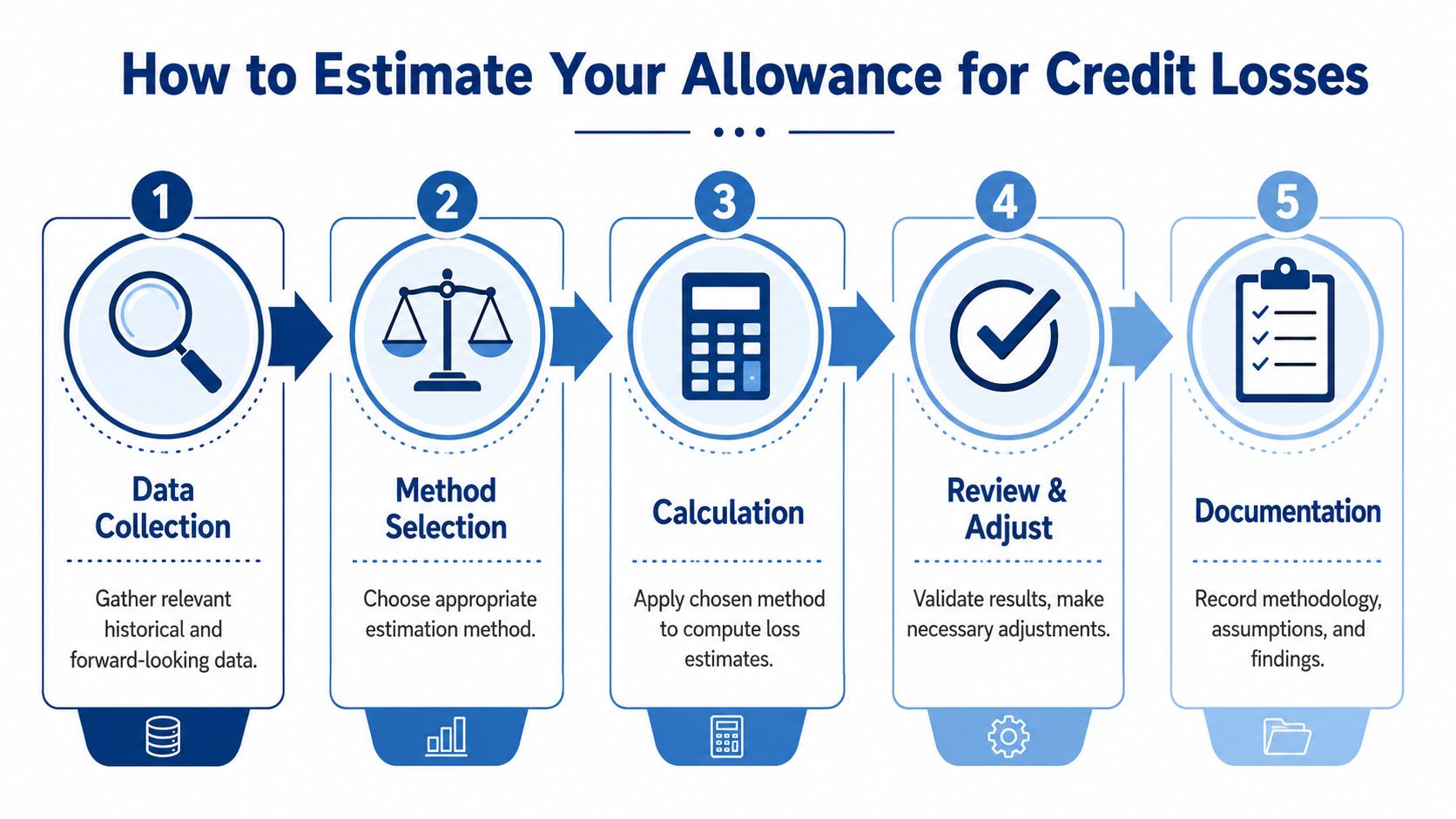

How to Estimate Your Allowance for Credit Losses

For most service businesses, the best starting point is not a complex model. It's a disciplined process.

The accounting literature gives flexibility. Accepted methods include discounted cash flow, loss-rate, roll-rate, probability-of-default, and aging-schedule approaches. What matters is that the method produces a supportable estimate and is updated at each reporting date, as summarized in Deloitte's CECL measurement guidance.

Start with the aging schedule

If you use QuickBooks Online or a similar system, your accounts receivable aging report is usually the most practical base. It groups invoices by how old they are. Older invoices generally carry more collection risk.

A common workflow looks like this:

- Pull the A/R aging report at month-end or quarter-end.

- Group invoices into aging buckets such as current, mildly overdue, and seriously overdue.

- Segment where needed by customer type, industry, geography, or invoice size if those differences affect collectibility.

- Apply estimated loss rates to each pool.

- Adjust for current conditions such as client concentration, billing disputes, or softness in a customer segment.

Other acceptable approaches

If your receivables behave differently, another method may fit better.

- Loss-rate method works well when you have a stable history and can estimate loss experience across a pool of receivables.

- Roll-rate method can help if you track how invoices move from one aging bucket to another before eventual collection or write-off.

- Probability-of-default thinking may be useful when a few large clients create most of the risk.

- Discounted cash flow is usually more effort than a small service business needs, but it's accepted in the framework.

Here's a practical explainer if you want a broader collection-risk perspective beyond GAAP mechanics: CFO's guide to bad debt.

What to do when your historical data is thin

This is the pain point for many firms. Maybe you cleaned up your books recently. Maybe you changed customer types. Maybe prior write-offs weren't tracked cleanly.

In that case, use a defensible blend:

- Your own history where it's usable

- Recent collection patterns, not just formal write-offs

- Qualitative adjustments for disputed invoices, customer concentration, or visible stress

- Reasonable pooling choices so unlike receivables aren't mixed together

A small company can have a strong allowance process without a big-company model. The standard is reasonableness, not mathematical glamour.

This short walkthrough may help if you want a visual explanation before building your process:

What makes an estimate defensible

Auditors and outside accountants usually care less about whether your estimate is “perfect” and more about whether it's consistent, documented, and tied to observable facts.

A workable file should show:

| Needed support | Example |

|---|---|

| Aging data | Month-end A/R aging report |

| Pooling logic | Separate rates for long-term clients and new clients |

| Loss assumptions | Internal history plus management judgment |

| Current condition adjustments | Notes on disputes, slow-paying sectors, or customer-specific risk |

| Review trail | Who prepared it, who reviewed it, and when |

That's often enough to move the process from informal guesswork to credible accounting.

A Practical Example with Journal Entries

Suppose you run a marketing agency. At month-end, your books show several unpaid client invoices. You want to estimate the allowance using an aging approach.

You review the receivables and sort them into broad pools based on age and risk. Some are current and from reliable clients. Others are old, disputed, or tied to clients who've started paying slowly.

Sample aging analysis

Here's a simple illustration:

| Receivable pool | Balance | Risk view |

|---|---|---|

| Current invoices | $80,000 | Mostly collectible |

| Moderately past due | $25,000 | Higher collection risk |

| Severely past due | $10,000 | Significant risk |

| Disputed invoice | $5,000 | Collection uncertain |

Management then applies reasonable estimated loss rates to each pool based on experience and current circumstances. The math might look like this:

| Receivable pool | Balance | Estimated loss rate | Estimated credit loss |

|---|---|---|---|

| Current invoices | $80,000 | 1% | $800 |

| Moderately past due | $25,000 | 8% | $2,000 |

| Severely past due | $10,000 | 25% | $2,500 |

| Disputed invoice | $5,000 | 60% | $3,000 |

| Total required allowance | $120,000 | $8,300 |

This means the balance sheet should not present the full $120,000 as if all of it will be collected. It should show receivables net of the estimated allowance.

The adjusting entry

If the allowance account currently has a zero balance, the month-end entry would be:

- Debit Bad Debt Expense $8,300

- Credit Allowance for Credit Losses $8,300

That entry records the expected loss in the same period as the related receivables remain on the books.

If you already had an allowance balance from a prior period, you wouldn't book the full amount again. You'd book only the adjustment needed to bring the allowance to the newly required balance.

The journal entry adjusts the allowance to the required ending balance. It doesn't automatically equal this month's write-offs.

Writing off a specific invoice later

Assume one of the old invoices, amounting to $3,000, is eventually deemed uncollectible. The write-off entry is:

- Debit Allowance for Credit Losses $3,000

- Credit Accounts Receivable $3,000

Notice what doesn't happen here. You don't hit bad debt expense again at the time of write-off, because you already recognized expected loss through the allowance estimate.

Why this matters for bookkeeping accuracy

This is one of the clearest examples of why adjusting entries matter. The estimate belongs in the period when risk becomes visible, not only when a collection failure becomes final. If you want a refresher on how adjusting entries work more broadly, this guide on examples of adjusting entries gives helpful context.

Common mistakes in the real world

Service businesses often slip in one of these ways:

- Booking write-offs only and skipping the allowance estimate entirely

- Using one flat rate for every customer, even when risk clearly differs

- Ignoring disputed invoices because they're still “open”

- Forgetting to true up the allowance each reporting period

A rough estimate with good logic is better than a polished spreadsheet built on weak assumptions.

Impact on Financial Statements and Business KPIs

The allowance for credit losses affects your statements in two places at once. It reduces asset value on the balance sheet, and the related expense reduces profit on the income statement.

The key accounting point is that the allowance is a valuation account deducted from the amortized cost basis of financial assets to present the net amount expected to be collected, as the OCC's allowance for credit losses guidance explains. It is not the same as directly writing down every receivable today.

Balance sheet effect

If gross accounts receivable is $120,000 and the allowance is $8,300, net receivables become $111,700.

That gives owners a cleaner picture of liquidity. It also keeps the balance sheet from overstating short-term assets.

Income statement effect

When you record or increase the allowance, you usually debit bad debt expense. That lowers net income for the period.

This can be uncomfortable for owners because it reduces profit before cash has been lost. But from an accounting standpoint, that's the point. The expense reflects expected credit cost while the receivable remains outstanding.

KPI effect

A stronger allowance process changes how several common metrics look:

- Working capital may decline because net receivables are lower.

- Current ratio may soften if current assets were previously inflated by doubtful invoices.

- Profit margin may decrease when bad debt expense is recorded on time.

- Days sales outstanding analysis becomes more meaningful when old, low-quality receivables aren't treated as fully collectible.

If you want a clearer grounding in how these accounts appear in practice, this primer on how to read a balance sheet is a useful companion.

Clean KPIs depend on clean receivables. If receivables are overstated, liquidity and profitability metrics can mislead you.

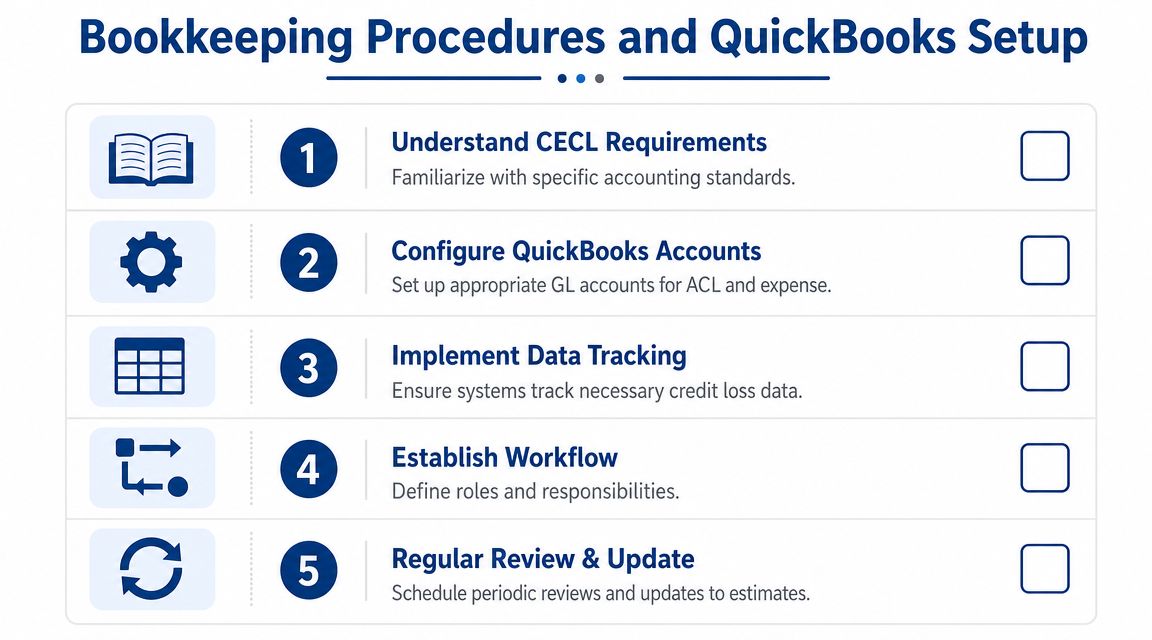

Bookkeeping Procedures and QuickBooks Setup

A good allowance process shouldn't live in one person's head or in a spreadsheet nobody revisits. It needs a repeatable bookkeeping routine.

Set up the accounts correctly

In QuickBooks Online, you'll usually want at least two general ledger accounts:

| Account | Type | Purpose |

|---|---|---|

| Allowance for Credit Losses | Contra asset tied to receivables presentation | Reduces A/R to expected collectible amount |

| Bad Debt Expense | Expense | Records the period's estimate adjustment |

Some businesses also create supporting schedules outside QuickBooks to document pooling, assumptions, and management adjustments.

A practical month-end workflow

A manageable process often looks like this:

- Run the A/R aging report as of month-end.

- Review unusual balances such as old invoices, disputes, credits, or customer concentrations.

- Update your estimate file using your chosen method.

- Compare required allowance to existing allowance balance.

- Post the adjusting journal entry for the difference.

- Save support such as reports, notes, and approvals.

How to keep it audit-friendly

You don't need a perfect dashboard. You do need discipline.

- Use one methodology consistently. If you change it, document why.

- Keep support with the entry. Save the aging report and your calculation in the same close folder.

- Separate preparation from review. Even in a small team, another person should look at the estimate.

- Flag customer-specific issues. One large disputed invoice can matter more than a dozen small current ones.

For firms building their accounting stack from scratch, this guide on how to set up QuickBooks Online for service businesses can help you organize the chart of accounts and close process in a cleaner way.

What not to automate blindly

Software can pull aging reports and memorize journal entries, but it can't replace judgment. If your client base shifts, a major account starts stretching payments, or a dispute turns serious, the allowance should change too.

That's why a monthly review matters. The process is part accounting, part credit judgment, and part documentation.

Audits Disclosures and When to Call an Expert

An allowance estimate becomes much more important once outside parties are reading your financials. Auditors, lenders, buyers, and investors usually want to know three things. How you built the estimate, whether the assumptions are reasonable, and whether you apply the method consistently.

A thin memo that says “management thinks this is enough” usually won't satisfy serious scrutiny. A short but clear file often will. It should tie the aging data to the estimate, explain any unusual adjustments, and show who reviewed it.

Signs the DIY approach is getting risky

Some situations deserve extra help:

- Rapid growth when your client mix is changing faster than your old history can explain

- Large customer concentration when one or two balances could swing the estimate

- Messy legacy books when write-offs and collections weren't tracked reliably

- Audit or financing pressure when someone external will challenge your assumptions

- Complex receivable pools when different industries, geographies, or contract types carry meaningfully different risk

If you can't explain your allowance in a few clear sentences and back it up with documentation, you're not ready for audit scrutiny.

The allowance for credit losses isn't just an accounting requirement. It's a discipline that forces your financial statements to match economic reality. For many service businesses, that's where better bookkeeping turns into better decision-making.

If your team needs help building a defensible allowance process, cleaning up receivables reporting, or setting up a month-end workflow that holds up under review, Steingard Financial can help you turn a confusing accounting requirement into a practical, repeatable system.