You're busy. Crews are working. Trucks are moving. Invoices are going out. Yet you open the bank app on Friday and wonder why cash feels tight again.

That disconnect is where most contractors get burned. The schedule looks full, but the books don't tell you which job is making money, which one is eating labor, and which invoice should have gone out three days ago. A standard bookkeeping setup can record deposits and expenses just fine. It usually can't tell you the financial truth of a project business.

That's why contractor accounting matters. Not as a tax-season exercise, and not as back-office paperwork. It's the operating system that ties field activity to profit. If you don't have that rhythm in place daily cost tracking, weekly billing discipline, monthly project review, your profits can vanish inside good-looking revenue.

Why Your Profits Disappear on Paper

A contractor can finish a strong month and still feel broke.

Take a common situation. You wrapped up one remodel, started two new jobs, approved extra material purchases, paid a subcontractor deposit, and ran payroll. On paper, sales look healthy. In reality, one job was underbilled, another carried labor overruns no one spotted early, and the biggest customer still hadn't approved the latest draw request.

The hidden problem isn't effort

Most owners don't have a work ethic problem. They have a visibility problem.

General bookkeeping looks backward. It tells you what hit the bank and what landed in the general ledger. Contractor accounting asks a different question: What happened on each job, and did billing keep pace with the work? That's the difference between being busy and being profitable.

Here's where confusion starts. If your office runs payroll in one system, tracks hours in texts or spreadsheets, and creates invoices later from memory, the numbers drift fast. That's why many contractors benefit from tighter field-to-office workflows, including tools like time tracking and invoicing software that connect labor capture to billing.

Cash stress often starts weeks before the bank account shows it.

Why the financial statements feel misleading

A company-level profit and loss statement can hide trouble. One profitable job can mask another job that's bleeding margin. A big customer payment can make cash look healthy even when future payroll is sitting on underbilled work.

That's also why contractors often get tripped up when switching reporting methods or reviewing how cash and accrual differ. If that's been a sticking point in your business, this overview of accrual to cash conversion helps clarify why the same business can appear to perform differently depending on the accounting lens.

The fix isn't more paperwork. It's better rhythm. Daily cost capture. Weekly billing review. Monthly job-level reporting. Once those pieces connect, the mystery starts to disappear.

Thinking in Projects Not Just P&Ls

The biggest mindset shift in contractor accounting is simple. Each job is its own financial unit.

That's not how most businesses think. A retailer can often look at company-wide sales, expenses, and margin. A contractor can't stop there. Every project has its own estimate, labor pattern, material usage, billing schedule, and risk.

Treat each job like a mini-business

A useful analogy is this: each project is a mini-business inside your business.

That mini-business has:

- Its own revenue plan tied to a contract

- Its own cost structure for labor, materials, equipment, and subs

- Its own timeline that affects when costs hit and when invoices go out

- Its own margin story that may be very different from the company average

If you only review the overall P&L, you're looking at the combined score after the game is over. Contractor accounting gives you the scoreboard for each field while the work is still happening.

Why contractor accounting is structurally different

Construction accounting differs from general business accounting because it treats each contract as an independent financial unit, not as part of one continuous stream of activity, as explained in this guide to construction accounting from Construction Executive.

That project-based structure changes how you organize your books. You need job-level revenue, job-level costs, and a system that can show whether a project is healthy before it ends. If you already think in terms of departments or service lines, this explanation of cost centers and profit centers is a helpful bridge. In contracting, each project often functions like both.

The report that clears up the confusion

The most misunderstood report in contractor accounting is the Work-in-Progress report, or WIP report.

At a practical level, the WIP compares three figures on each active job:

| Project question | What the WIP looks at |

|---|---|

| What have we spent so far? | Costs incurred to date |

| How much revenue have we earned based on progress? | Revenue recognized |

| How much have we billed the customer? | Amount billed |

That comparison tells you whether a job is overbilled or underbilled. That matters because billing and actual job progress rarely move in perfect sync.

A project can look cash-rich because you billed ahead. It can also look profitable while starving your bank account because you earned revenue you haven't billed yet.

What owners usually get wrong

Many owners assume this sequence: if the project is busy, and the invoices are out, the profit must be there.

Not always. Here's a more effective way to consider it:

- Job costing tells you where the money is going.

- Revenue recognition tells you how much you've earned.

- Billing status tells you whether cash collection is keeping up.

If one of those three is off, the whole picture gets distorted. That's why contractor accounting isn't just bookkeeping with different labels. It's a job-by-job control system.

Building Your Financial Framework

A good reporting process can't fix a bad accounting structure. If your chart of accounts is generic, your job reports will be generic too.

Most contractors using QuickBooks Online run into the same issue. The file was set up like a standard service business. Income is too broad. Direct costs are lumped together. Equipment, subcontractors, and burdened labor aren't separated clearly enough to support reliable job costing.

What your chart of accounts needs to do

Your chart of accounts should answer this question: Can I see where project margin is being made or lost without digging through transactions one by one?

For contractors, that usually means separating costs into buckets that reflect how jobs are managed.

A clean structure often includes:

- Direct labor accounts for field wages tied to jobs

- Material cost accounts that capture purchased job materials

- Subcontractor accounts separated from employee labor

- Equipment and tool cost accounts for owned or allocated usage

- Indirect overhead accounts for office payroll, rent, software, insurance, and admin costs

You don't want a single account called “Job Costs” swallowing everything. That makes review almost useless.

Build around job costing, not tax prep

Tax returns summarize. Contractor accounting needs to diagnose.

If your accounts are set up only to satisfy year-end filing, you'll miss the operating detail that matters during the year. The office should be able to assign transactions to the right customer, project, and cost category quickly. If not, reports become delayed and managers stop trusting them.

A practical setup approach in QuickBooks Online looks like this:

| Area | What to create |

|---|---|

| Income | Contract income, change order income, service income if applicable |

| Cost of goods sold | Direct labor, materials, subcontractors, equipment, permits, disposal, job supplies |

| Overhead | Office payroll, rent, admin software, insurance, marketing, professional fees |

| Balance sheet | Retainage receivable, customer deposits if used, fixed assets, loan accounts |

The detail level that actually helps

Too little detail is the common problem. Too much detail is the second one.

You don't need dozens of tiny accounts that no one uses consistently. You need a structure your office can maintain every week. The right level is the one that lets you compare estimate categories to actual categories in a way your project managers understand.

Practical rule: If your field team budgets labor, materials, equipment, and subs separately, your accounting should too.

If you're rebuilding your file or cleaning up a messy one, this guide on how to create a chart of accounts is a strong starting point. For contractors, the key is making that chart support job-level decisions, not just year-end totals.

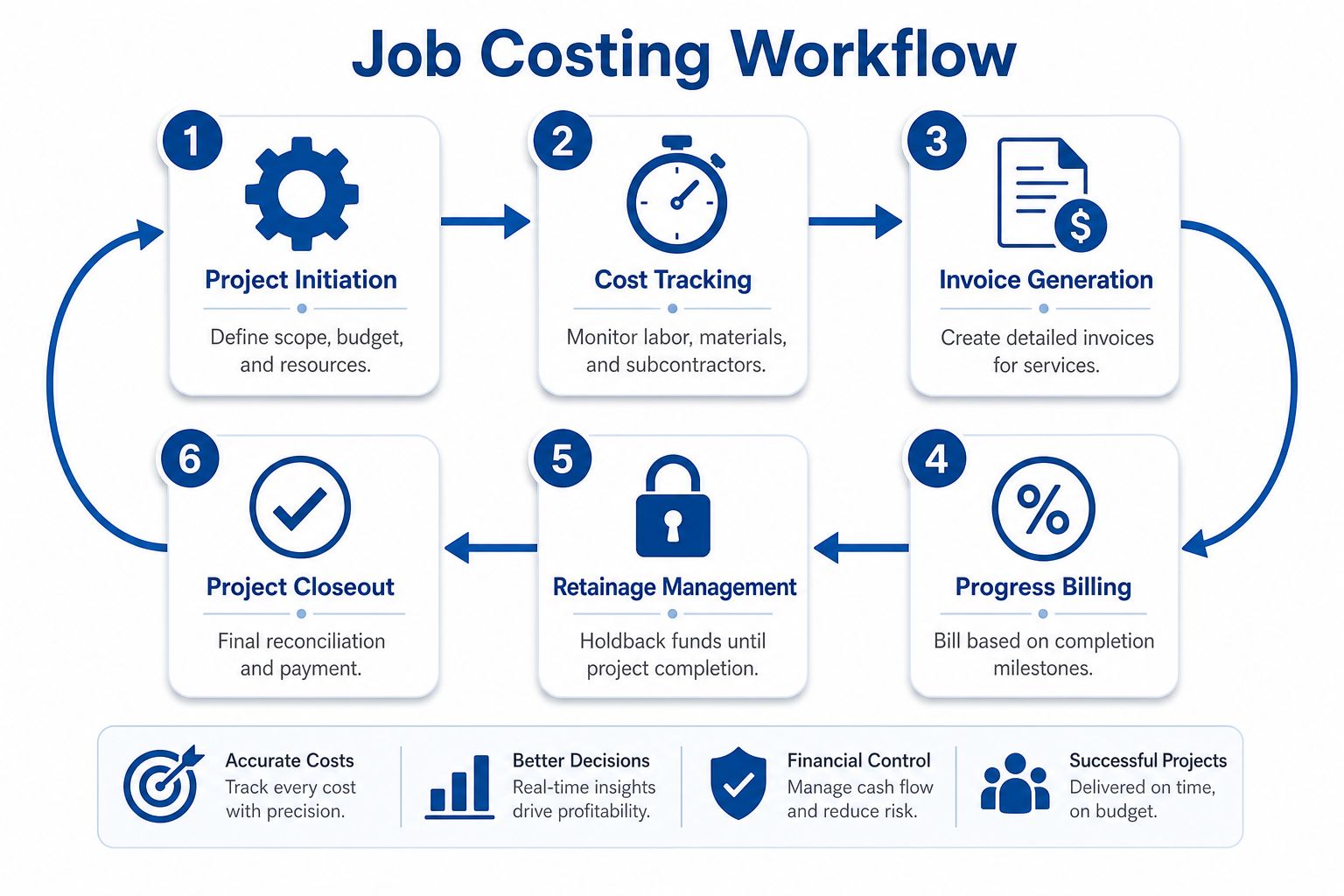

Mastering Job Costing Billing and Retainage

Contractor accounting becomes operational. The books stop being a record of the past and start becoming a control system for the current week.

The daily habit that matters most is job costing. Contractors need to allocate equipment, tool, and asset ownership costs to specific jobs, track committed subcontractor costs in real time, and run frequent WIP reports using actual job data rather than reacting after the fact, as outlined in Deltek's construction accounting best practices.

The daily workflow that protects margin

A healthy workflow is repetitive. That's a good thing. It means the office isn't reinventing the process every billing cycle.

Start with the field:

Capture labor daily

Hours need to be attached to the right job and, ideally, the right cost code. If time sits in notebooks or arrives late, profitability reporting falls apart.Enter material purchases quickly

Card charges, supplier invoices, and reimbursements should be coded to the job as they happen. Waiting until month-end guarantees missing detail.Track subcontract commitments before final bills arrive

A signed subcontract is already a financial commitment. If the office only records costs when invoices come in, job forecasts lag reality.Allocate equipment and owned asset usage

If a skid steer, trailer, or specialty tool is used across jobs, that cost needs a home. Otherwise one project carries too much burden and another looks cleaner than it is.

Why billing discipline matters as much as cost tracking

A well-costed project can still create cash pain if billing lags.

For progress billing jobs, the office should compare project status, approved change orders, prior billings, and current billable work before invoices go out. For time and materials jobs, labor entries, marked-up materials, equipment usage, and subcontractor pass-throughs need to feed the invoice without delay.

Here's a simple distinction:

- Progress billing follows contract milestones or percentage completion

- Time and materials billing follows actual labor, materials, and agreed markups

- Fixed fee billing still needs internal job costing, even though the client sees one price

A short visual can help align your team on the full cycle:

Retainage needs its own tracking

Retainage confuses a lot of owners because the invoice says one thing and the cash receipt says another.

Retainage is the portion withheld until a later project milestone or closeout. If you don't track it separately, accounts receivable becomes misleading. The office may think the customer is slow-paying when the holdback is contractual.

A practical way to handle it is to:

- Invoice the full earned amount according to the contract terms

- Record the retained portion separately from the collectible current receivable

- Review retainage by job so closeout billing doesn't get missed

- Bill final retainage promptly when punch list and documentation are complete

Billing is not just about getting paid. It's how contractor accounting keeps cash flow aligned with the work already performed.

What this looks like in the real week

A disciplined contractor accounting rhythm often looks like this:

| Timing | What should happen |

|---|---|

| Daily | Labor posted, purchases coded, subcontract commitments updated |

| Weekly | Open cost review, billing prep, missing receipts and time cleaned up |

| Monthly | WIP review, job profitability review, retainage and receivables follow-up |

If your office can do those three levels consistently, margin problems surface earlier, invoices go out cleaner, and project closeout becomes less chaotic.

Navigating Payroll and Tax Requirements

Payroll is one of the easiest places for contractors to create hidden risk.

The issue isn't just getting checks out on time. You also need clean classification, reliable job allocation, and payroll data that supports project reporting. If labor is your biggest moving cost, weak payroll controls can distort both compliance and profitability.

Employee or independent contractor

Owners often ask where to draw the line between a W-2 employee and a 1099 independent contractor. The answer depends on the actual working relationship, not what's most convenient.

If you control schedule, methods, tools, and day-to-day direction, that worker often looks more like an employee than an independent contractor. If you get this wrong, the fallout can include payroll tax issues, benefit questions, and insurance complications.

That's one reason payroll platform choice matters. Whether you use Gusto or QuickBooks Payroll, your system should support clear worker setup, tax filings, and job-linked labor reporting. It should also connect cleanly to your accounting file so payroll doesn't become a monthly cleanup project.

Insurance and payroll records are connected

Contractors sometimes think of payroll, workers' comp, and accounting as separate lanes. They aren't.

Payroll classifications affect workers' comp reporting. Claims history and payroll records can shape how the business is viewed by carriers. If you want a plain-English explanation of how claims history can influence cost, this resource on workers comp experience modification is useful context for owners managing both labor growth and insurance expense.

Revenue recognition still matters even when cash is tight

Many contractors look at the bank account first and book revenue based on what got paid. That's understandable. It isn't always sufficient.

The industry was standardized in 2014 by ASC 606, which introduced a five-step revenue recognition model governing when and how revenue is booked on construction contracts, as summarized in this review of construction accounting software and ASC 606.

Those five steps are:

- Identify the contract

- Identify performance obligations

- Determine the transaction price

- Allocate the transaction price

- Recognize revenue as obligations are satisfied

For a contractor, the practical takeaway is simple. Revenue should reflect the work earned under the contract, not just the timing of cash receipts.

If payroll runs weekly but revenue is recorded casually, your financial statements can tell two different stories at the same time.

For government contractors, the rules get tighter

Some contractors face another layer of compliance. Government contractors on contracts exceeding $50 million must comply with the 19 Cost Accounting Standards under 41 U.S.C. chapter 15, including a written DS-1 disclosure statement before award, according to the Federal Acquisition Regulation at FAR Part 30.

That doesn't apply to every contractor, but it reinforces the same principle. Cost accounting practices need to be consistent, documented, and defensible.

Key Financial Reports and KPIs for Contractors

A contractor doesn't need more reports. A contractor needs the right reports reviewed at the right time.

The standard profit and loss statement and balance sheet still matter. They just aren't enough on their own. To manage jobs well, you need reports that answer operational questions, not just tax or bookkeeping questions.

The reports that deserve regular attention

The most useful contractor reports usually include:

Job profitability report

Shows income and cost by project. This helps you see which jobs are carrying the business and which ones are eroding gross profit.WIP report

Shows whether earned revenue and billings are aligned. This report identifies overbilling and underbilling.Over and under billing summary

Gives leadership a quick read on where cash may be ahead of work or trailing work.Accounts receivable aging

Tells you which customer balances are current and which ones need action.

The questions each report should answer

A report is only useful if someone knows what to ask.

| Report | Key question |

|---|---|

| Job profitability | Did this job make the margin we expected? |

| WIP | Are we billing in line with actual progress? |

| Over and under billing | Which jobs are helping cash now, and which jobs are draining it? |

| AR aging | Who owes us money, and what needs follow-up this week? |

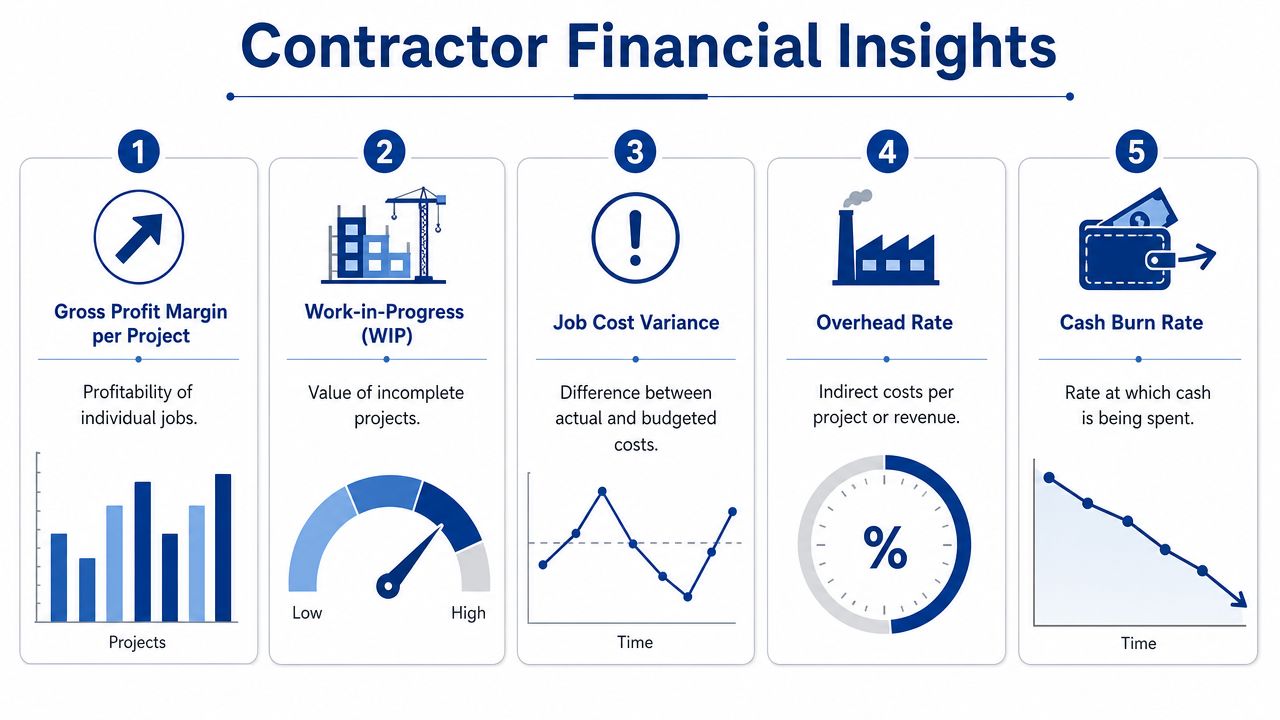

KPIs that actually help owners

Contractors often ask about KPIs as if they need a dashboard full of ratios. Most businesses don't. A short list reviewed consistently is more valuable.

Focus on indicators like:

- Gross margin per job to compare estimated margin against actual margin

- Budget versus actual costs to spot labor or material creep

- Days Sales Outstanding to understand how fast receivables convert into cash

- Cash burn rate to see whether current spending is outrunning collections

- Overhead rate to know how much indirect cost the company must support

The point isn't academic analysis. It's decision-making. If one project type repeatedly produces weak margins, you can reprice it, change how you staff it, or stop chasing that work. If underbilling keeps showing up, the problem may be billing cadence, documentation, or change order discipline rather than production itself.

Good contractor accounting turns reports into questions, and questions into action.

When to Partner With a Contractor Accounting Expert

Some owners can manage their books internally for a while. Then the business changes. More crews, more jobs, more billing complexity, more payroll volume. What used to be manageable starts creating blind spots.

Signs you've outgrown DIY bookkeeping

You don't need an accounting expert because the business is failing. You usually need one because the business is moving faster than the back office can handle.

Common warning signs include:

- Reports arrive late and no one trusts the numbers anyway

- Cash surprises keep happening even when sales look strong

- Job profitability is unclear until the project is almost done

- Retainage, change orders, or payroll allocations get messy

- A prior bookkeeper left cleanup work behind

Why outside help can be a strategic move

An experienced contractor-focused accountant doesn't just categorize transactions. They build structure. They tighten close processes. They make sure payroll, job costing, billing, and reporting feed each other.

That matters because owners should spend time pricing work, managing crews, and protecting customer relationships. They shouldn't spend nights trying to figure out why the receivable report doesn't match what the PM says was billed.

Outsourcing becomes valuable when it gives you timely numbers you can run the business with. That's not overhead for its own sake. It's a way to reduce financial guesswork and create a back office that can grow with the company.

If your contractor accounting still feels reactive, Steingard Financial can help you build a cleaner, more dependable system for bookkeeping, payroll, job-level reporting, and ongoing financial visibility. A discovery conversation is a practical next step if you want timely numbers, fewer surprises, and a back office that supports growth.