You buy a new server rack, replace half the office computers, and sign for a software license your team will use for years. The cash leaves your bank account today, but the value doesn’t disappear today. That mismatch is where a lot of service business owners get tripped up.

If you expense everything at once, your profit drops hard in one month and looks artificially better in the months after. If you ignore the cost entirely, your books overstate profit and make decisions look safer than they are. Depreciation and amortisation solve that problem by spreading long-term asset costs over the period those assets help you earn revenue.

For a busy owner, this isn’t just accounting vocabulary. It affects your tax timing, your month-end reporting in QuickBooks, your loan conversations, and your confidence in the numbers you use to hire, price, and invest.

Beyond Simple Expenses Understanding Asset Value Over Time

A box of printer paper is a simple expense. You buy it, use it, and move on.

A server, office buildout, company vehicle, or purchased patent is different. Those items keep helping your business long after the day you pay for them. Accounting treats them as assets first, then recognizes their cost over time.

Why timing matters

If your consulting firm buys equipment in one month and records the full cost as a regular expense, that month can look far worse than the months that follow. But the equipment may support client work for years. Good bookkeeping tries to match cost with use.

That idea is often called the matching principle. You recognize the cost across the same general period the asset helps produce revenue. The result is a profit and loss statement that reflects business activity more fairly, instead of bouncing around because of one large purchase.

Practical rule: If the item benefits the business over multiple periods, don’t think of it like rent, coffee, or utilities. Think about whether it belongs on the balance sheet and needs to be depreciated or amortised.

What owners usually confuse

Most confusion starts with one reasonable question: “I already paid for it, so why can’t I just expense it?”

Because cash movement and profit measurement are not the same thing. Your bank account tracks when money moved. Your financial statements try to show what that spending means over time.

That distinction matters when you’re:

- Reviewing profitability: A cleaner P&L helps you judge whether a service line is working.

- Planning cash: Non-cash expenses still matter, even though they don’t create a second cash outflow later.

- Preparing taxes: Book treatment and tax treatment may differ, which creates planning opportunities and reconciliation work.

- Using QuickBooks reports: Your reports are only useful if asset purchases are categorized correctly from the start.

A good mental model is this. Buying a long-term asset is like paying upfront for years of business use. Depreciation and amortisation are the process of recognizing that prepaid value gradually instead of pretending it vanished on day one.

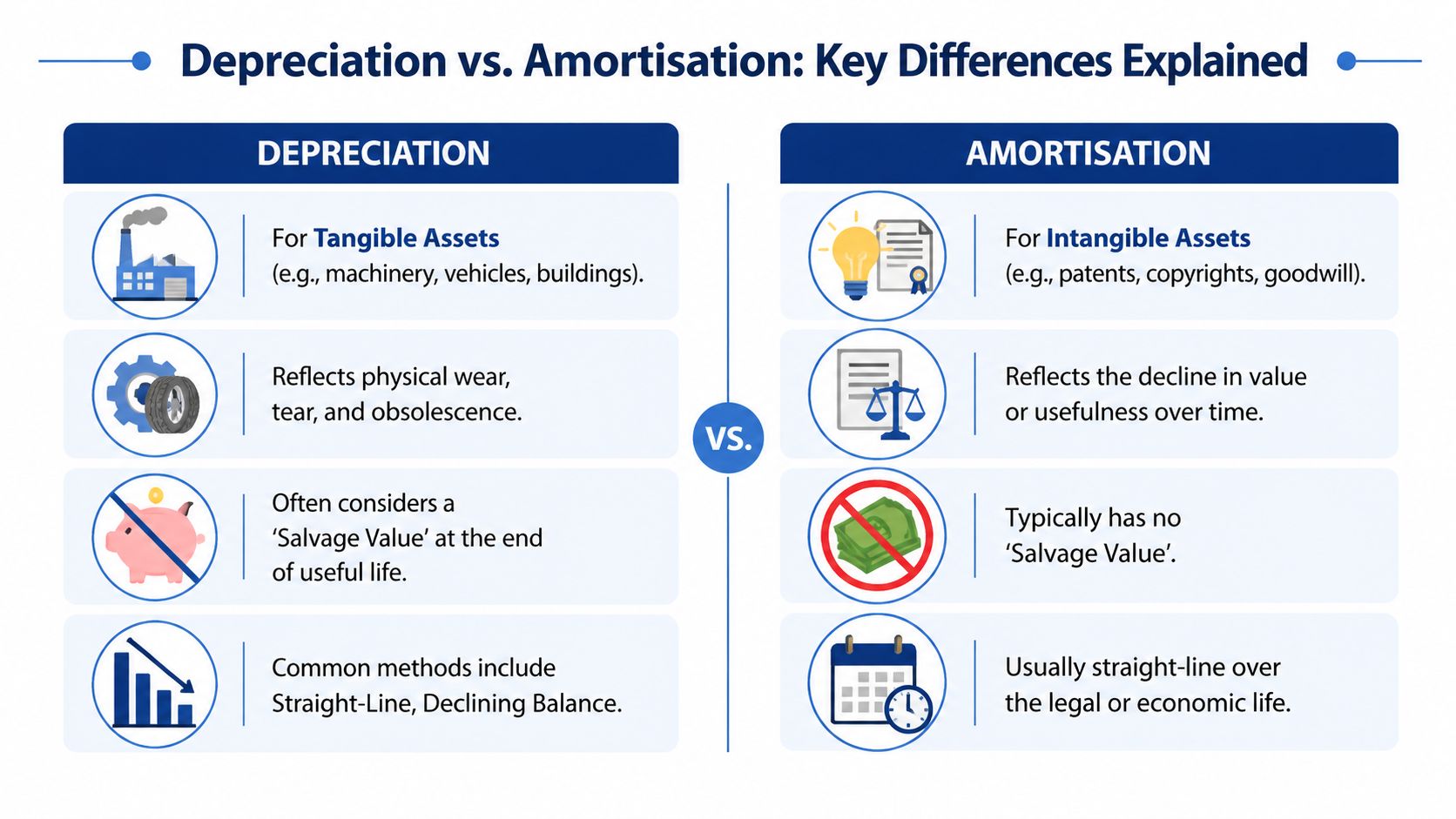

Depreciation vs Amortisation Key Differences Explained

These terms are related, but they’re not interchangeable.

Depreciation applies to tangible assets. Things you can touch. Think office furniture, computers, vehicles, or machinery.

Amortisation applies to intangible assets. Things you can’t physically hold but that still have value. Think patents, certain software-related rights, copyrights, goodwill from an acquisition, or purchased customer-related intangibles in some cases.

A simple way to separate them

A company van loses value because it wears out, becomes outdated, and eventually reaches the end of its useful life. That’s depreciation.

A patent loses value because its legal or economic usefulness runs down over time. That’s amortisation.

They serve the same big purpose. Both spread cost over time. The difference is the kind of asset they apply to.

Depreciation vs Amortisation at a Glance

| Attribute | Depreciation | Amortisation |

|---|---|---|

| Asset type | Tangible assets | Intangible assets |

| Common examples | Machinery, vehicles, furniture, computers | Patents, copyrights, goodwill, certain licenses |

| Why value declines | Wear and tear, obsolescence, use | Passage of time, legal life, declining usefulness |

| Residual or salvage value | Often considered | Typically none |

| Common methods | Straight-line, accelerated methods | Usually straight-line |

One of the clearest examples comes from SimFin’s explanation of depreciation and amortisation. The most common approach is the straight-line method. For a $100,000 machine with a 10-year useful life and $10,000 residual value, annual depreciation is $9,000. For a $50,000 patent with a 5-year life, annual amortisation is $10,000.

Where service businesses run into trouble

The errors usually aren’t complicated. They’re classification errors.

A few common ones:

- Software confusion: Teams often treat every software payment the same, even when one payment is a routine subscription and another is tied to a longer-term intangible asset.

- Furniture and equipment mix-ups: Office chairs, server equipment, and specialized devices can get buried in ordinary operating expense accounts.

- Acquisition-related intangibles: If you buy part of a business, the intangible piece often needs very different treatment from the desks, laptops, or vehicles that came with it.

If you can touch it, start by asking whether it’s depreciated. If you can’t, start by asking whether it’s amortised.

That won’t answer every edge case, but it gets most owners pointed in the right direction fast.

How to Calculate Depreciation and Amortisation

Once the asset is classified correctly, the math gets easier.

The key inputs are usually the asset’s cost, its useful life, and, for many tangible assets, any residual or salvage value. From there, you apply the method your books or tax rules require.

Straight-line method

The straight-line method is the one most owners should understand first because it’s simple and widely used.

For depreciation, the formula is:

(Cost − Residual value) ÷ Useful life

Using the machine example already noted earlier, the annual depreciation is ($100,000 − $10,000) ÷ 10 = $9,000. That means the business records the same expense each year until the asset reaches its residual value.

For amortisation, the formula is usually even simpler:

Cost ÷ Useful life

For the patent example, $50,000 ÷ 5 = $10,000 per year.

Why straight-line is so popular

Straight-line is predictable. It makes monthly and yearly reporting easier to review. It also works well when an asset provides fairly even value over time, which is common for many service business assets.

A depreciation or amortisation schedule built on straight-line usually includes:

- Original cost

- Useful life

- Residual value, if any

- Annual expense

- Accumulated depreciation or amortisation

- Remaining book value

If you want to see how schedules are structured in practice, this guide on how to calculate an amortization schedule is a useful companion because it trains your eye to follow period-by-period reductions clearly.

Accelerated depreciation methods

Book accounting often uses straight-line, but tax and planning discussions frequently involve faster methods for tangible assets.

A good example is double-declining balance, often shortened to DDB. According to Thomson Reuters’ discussion of amortization vs. depreciation, for a $21,000 asset with a 5-year life, the DDB rate is 40%, producing a Year 1 expense of $8,000, compared with $4,000 under straight-line if you assume $1,000 salvage value.

That tells you something important without needing to memorize every formula. Accelerated methods push more expense into earlier years. Straight-line spreads it evenly.

Faster depreciation doesn’t mean the asset is “used up” faster in real life. It means the accounting method recognizes more of the cost earlier.

Here’s the practical effect:

- Straight-line: smoother reporting

- DDB: higher early expense, lower later expense

- Tax planning angle: earlier deductions can matter for cash flow

Schedule thinking matters more than formula memorization

Owners often focus on one year’s expense and miss the bigger picture. The better habit is to think in schedules, not isolated entries.

A schedule helps you answer questions like these:

- What’s left on the books?

- When does the expense stop?

- Why does this year’s tax depreciation differ from book depreciation?

- What happens if we dispose of the asset early?

If you’re still deciding whether a purchase belongs in an asset account at all, a plain-English explanation of what counts as capital outlay can help clarify the boundary between routine expense and long-term investment.

A clean schedule turns depreciation and amortisation from a year-end scramble into a normal part of month-end reporting.

Here’s a helpful visual walkthrough of the concepts and calculations:

Recording Depreciation and Amortisation in Your Books

Calculation is only half the job. The other half is recording it correctly so your income statement and balance sheet both make sense.

Most accounting systems, including QuickBooks, rely on double-entry bookkeeping. That means each depreciation or amortisation entry affects at least two accounts.

The core journal entry

For depreciation, the standard entry is usually:

- Debit Depreciation Expense

- Credit Accumulated Depreciation

For amortisation, it’s similar:

- Debit Amortisation Expense

- Credit Accumulated Amortisation

The expense account appears on the income statement and reduces profit. The accumulated account sits on the balance sheet as a contra-asset account, which means it reduces the asset’s carrying value without changing the original cost line.

What this looks like in practice

Suppose your business owns equipment recorded in a fixed asset account. The original cost stays visible. Each month or year, accumulated depreciation grows. That lets you see both what you paid and how much of that cost has already been recognized.

That structure is more useful than reducing the asset account directly. It preserves history.

A simplified view looks like this:

| Account | What it does | Statement |

|---|---|---|

| Depreciation Expense | Records current-period cost allocation | Income Statement |

| Accumulated Depreciation | Offsets the asset’s book value | Balance Sheet |

| Amortisation Expense | Records current-period intangible cost allocation | Income Statement |

| Accumulated Amortisation | Offsets the intangible asset’s book value | Balance Sheet |

Why setup matters in QuickBooks

If your chart of accounts is messy, depreciation and amortisation become messy too. Owners often post long-term assets into generic expense accounts, then try to fix everything at year-end. That’s where reporting starts to drift.

A stronger process usually includes:

- Separate asset accounts: Keep furniture, equipment, vehicles, and intangibles organized.

- Dedicated accumulated accounts: Don’t bury contra-asset activity inside the asset itself.

- Recurring month-end entries: Record the expense consistently so reports don’t swing unexpectedly.

- Supporting schedules: Your books should tie back to an asset list, not just a journal entry.

Clean adjusting entries make your reports believable. Sloppy ones make every P&L discussion longer than it needs to be.

If you want a straightforward reference for how these entries work, this walkthrough of an adjusting entries example is useful because depreciation and amortisation are classic adjusting entries at month-end and year-end.

Tax Implications and Strategic Reporting

Tax rules often don’t mirror your internal books. That’s why owners get confused when their CPA says one depreciation number goes on the tax return while QuickBooks shows another for management reporting.

For book purposes, the goal is often clarity and consistency. For tax purposes, the goal is following tax law while making smart choices about deduction timing.

Book depreciation and tax depreciation are not the same thing

Book depreciation usually focuses on useful life and matching cost to operations. Tax depreciation in the U.S. often follows MACRS, which can accelerate deductions for tangible assets.

That matters because accelerated deductions can reduce taxable income earlier, which can preserve cash when a growing firm needs it most.

OnPay’s overview of amortization vs. depreciation gives a clean illustration. For a $50,000 coffee machine with a 10-year useful life and no salvage value, straight-line gives $5,000 per year, while double-declining at 20% produces $10,000 in Year 1, $8,000 in Year 2, $6,400 in Year 3, and $5,120 in Year 4. At a 21% corporate tax rate, that Year 1 DDB approach saves about $1,050 compared with straight-line.

The point isn’t that every service business should rush into accelerated methods. The point is that timing affects cash.

Section 197 intangibles create a separate set of rules

Intangible assets can be even more counterintuitive.

According to Wall Street Prep’s explanation of depreciation vs. amortization, Section 197 intangibles such as goodwill and certain acquired patents are amortized over 15 years on a straight-line basis for tax purposes, with no salvage value. The same source gives an example where a $15,000 patent would be $1,500 per year over 10 years economically, but $1,000 per year when forced into the 15-year tax treatment.

That slower deduction pattern can raise near-term taxable income even when the asset may lose practical value sooner.

The bonus depreciation phase-down changed planning

Many owners got used to more generous immediate write-offs. That environment has shifted.

A Commerce Bank article on understanding depreciation and amortization notes that bonus depreciation drops to 40% in 2025 from 60% in 2024. For businesses that invest in equipment, that changes purchase timing decisions and can reduce the tax cushion owners expected from a major buy.

That doesn’t automatically mean “buy now” or “wait.” It means you should model the tax effect before signing the purchase order.

Strategic reporting questions to ask before year-end

A useful tax conversation usually starts with a short list:

- Are book and tax asset schedules reconciled? If not, your reporting can become hard to trust.

- Did we classify every purchase correctly? Misclassification can cost deductions or create cleanup work later.

- Do our current-year purchases still make sense after the phase-down? Timing matters.

- Do we have acquired intangibles that fall under special rules? These often surprise owners.

- Will financing change the deduction strategy? If you financed equipment or expansion, it also helps to understand business loan parts you can deduct so interest and asset-related deductions are viewed together.

Tax depreciation is a cash planning tool, not just a compliance exercise.

When depreciation and amortisation are handled well, you don’t just file a more accurate return. You make better timing decisions about equipment, software, acquisitions, and financing.

How D&A Impacts Your Business Financial Health

Depreciation and amortisation are often called non-cash expenses. That phrase confuses owners because they did spend cash at some point.

The better way to say it is this: the cash usually moved when you bought the asset, but the accounting expense shows up later over time. So the expense reduces accounting profit in the current period without creating a fresh current-period cash payment.

Why lenders and operators care

Because these expenses lower net income, but they don’t work like payroll or rent in the month they’re recorded. On the statement of cash flows, they’re commonly added back under operating activities.

That’s one reason metrics like EBITDA get attention. EBITDA removes interest, taxes, depreciation, and amortisation to give a rougher view of operating performance before those items. It’s not the same as cash, and it’s not a substitute for real analysis, but it can help owners compare operations across periods.

A useful red-flag ratio

One metric that deserves more attention is the D&A/Sales ratio.

According to GMT Research’s note on the depreciation and amortisation to sales ratio, the D&A/Sales ratio is a critical KPI for assessing capital intensity and accounting integrity. The same source notes that asset-light service firms often have ratios below 2%, but a significant unexplained drop relative to peers can be a red flag for under-depreciation, which can artificially inflate profits.

That matters because many service businesses are asset-light by nature. A low ratio alone doesn’t prove anything. But if your ratio suddenly falls while your asset base hasn’t meaningfully changed, that deserves a second look.

A healthy ratio isn’t just about how “light” your business is. It’s about whether your books reflect reality consistently.

How to use this insight without overcomplicating it

You don’t need a forensic accounting project every month. You do need pattern awareness.

A practical review process looks like this:

- Compare trend to your own history: If D&A drops sharply, ask why.

- Check new assets against recorded schedules: Did everything get added properly?

- Review disposed assets: If old assets were removed, did the schedule and books both get updated?

- Look at profit quality: If margins improved, was it operational, or did accounting treatment change?

For owners who want cleaner reporting context around those relationships, a guide on how to prepare financial statements can help tie the income statement, balance sheet, and cash flow statement together.

The core value here is judgment. Depreciation and amortisation don’t just satisfy accounting rules. They help you tell whether your profits are durable, whether your asset spending is keeping pace with reality, and whether your reports deserve your trust.

When to Outsource D&A to a Bookkeeping Pro

A solo consultant with one laptop and one phone plan can usually keep things simple.

A growing service business can’t. Once you have office equipment, leasehold improvements, specialized devices, software-related assets, acquisitions, or multiple locations, depreciation and amortisation stop being a side task and start becoming a system.

Signs DIY has become risky

The issue usually isn’t that owners can’t understand the basics. It’s that the volume of moving parts grows faster than expected.

A few common triggers:

- Multiple asset categories: Furniture, equipment, vehicles, and intangibles all need different treatment.

- Book and tax differences: Your QuickBooks books may not match your tax depreciation schedules.

- Financing or lender scrutiny: Banks care whether financial statements are clean and consistent.

- Messy historical records: Once assets were expensed incorrectly for a year or two, cleanup gets harder.

- Acquisition activity: Purchased goodwill and other intangibles create rules many internal teams don’t see often.

What a specialist actually improves

A bookkeeping professional or CPA doesn’t just post journal entries. They build a repeatable process.

That usually means:

- A cleaner chart of accounts.

- A fixed asset register that ties to the balance sheet.

- Recurring adjusting entries that don’t get skipped.

- Reconciliations between book records and tax support.

- Reporting that lets the owner understand what changed and why.

That’s especially useful if your current reporting feels accurate only after someone “explains away” the odd parts every month.

If your depreciation only gets attention at tax time, your monthly financial statements are probably missing part of the story.

If you’re comparing outsourced support models, this review of Jumpstart Partners' services review gives a broader look at how firms structure outsourced accounting support, what they tend to handle, and where specialized bookkeeping becomes valuable.

Outsourcing makes sense when the cost of errors, delays, or weak reporting is higher than the cost of getting the system right.

Frequently Asked Questions About Depreciation and Amortisation

A few questions come up almost every time owners start using these concepts in practice.

Common D&A Questions

| Question | Answer |

|---|---|

| Is depreciation the same as a cash expense? | No. The cash usually went out when you bought the asset. Depreciation records that cost over time for accounting purposes. |

| Do all assets get depreciated or amortised? | No. Routine short-term purchases are usually expensed directly. Long-term assets are the ones that usually need this treatment. |

| Can the tax method differ from the book method? | Yes. That’s common. Book treatment often aims for clear reporting, while tax rules may allow or require different timing. |

| What happens when an asset is fully depreciated or amortised? | Once it’s fully written down under the chosen method, no further expense is recorded. The asset may still be in use, but the scheduled expense has ended. |

Should I record depreciation monthly or yearly

Monthly is usually better for internal reporting if you review financials regularly. It keeps your P&L from looking overstated during the year and then suddenly shifting at year-end.

Yearly may be acceptable in very simple situations, but it gives you weaker month-to-month insight.

What if I bought something and put it in the wrong account

That’s common. The fix depends on timing and materiality, but the first step is to stop letting the error roll forward.

Review the purchase, determine whether it should have been capitalized, and then make the correcting entry with supporting documentation. If more than one period is affected, you may also need to adjust prior reports internally so your trend analysis stays useful.

Does amortisation always mean intangible assets have no value left

Not necessarily in a business sense. It means the accounting schedule has recognized the recorded cost according to the applicable method.

An intangible asset may still help operations after the amortisation period, but if the rules say the cost has been fully amortised, the expense stops. Accounting value and practical usefulness aren’t always the same thing.

Why do owners get tripped up by D&A so often

Because three different ideas get blended together:

- Cash paid

- Book expense

- Tax deduction

Those are related, but they aren’t identical. Once you separate those three, most confusion starts to clear up.

If you want your books to reflect asset purchases accurately, your month-end reports to stay reliable, and your tax planning to line up with how your business operates, Steingard Financial can help you build a cleaner system around depreciation, amortisation, payroll, and ongoing reporting.