You hire someone to help with marketing, bookkeeping, design, IT, or client delivery. They want to start next week. You need the work done now, and the easiest path looks obvious: pay them as a contractor and move on.

That's where many businesses get into trouble.

Employee classification isn't a paperwork preference. It's a legal decision that affects payroll taxes, overtime, benefits eligibility, recordkeeping, and audit exposure. And it's easy to get wrong because the day-to-day working relationship often drifts away from what the contract says.

Why Employee Classification Is a Critical Decision

A business owner brings in a bookkeeper for “a few months” and pays them as a contractor. Six months later, that person works set hours, uses the company login, follows the office process, and reports to a manager every week. On paper, nothing changed. In practice, the relationship did.

That gap is why classification deserves close attention. Employee classification decides how you run payroll, withhold and pay taxes, handle overtime, issue year-end forms, and document the relationship if a state agency or the IRS asks questions. It also affects workers' compensation, unemployment insurance, benefit plan eligibility, and wage-and-hour compliance.

The key point is simple. Classification is not a label you choose once and file away. It works more like coding a worker into the right lane of your payroll and HR system. If the setup is wrong, every process connected to that worker can be wrong too.

Business owners usually get tripped up for practical reasons, not careless ones. Hiring happens fast. A contractor arrangement can look cheaper at first glance. A signed agreement feels final. But agencies and courts usually focus on what happens in day-to-day operations, not just what the contract says.

Here's where confusion shows up inside the business:

- Operations drift: The role starts as project work, then becomes part of your regular workflow.

- System mismatch: Accounts payable treats the worker like a vendor while managers treat them like staff.

- Documentation gaps: There is no clear file showing why the classification decision was made.

- Year-end surprises: The team has to sort out invoices, payroll records, and 1099 filing steps for contractors after the fact.

A practical way to view this is as an audit trail problem. If your real-world management of the worker says “employee,” but your payment process says “contractor,” you have built a contradiction into your records. That contradiction is often what creates trouble during an audit, a payroll review, or a worker complaint.

Good classification work connects legal analysis to daily execution. You need a repeatable workflow: review the role, document the facts, make an informed choice on employee or contractor status, then set the person up correctly in payroll, accounts payable, onboarding, time tracking, and manager instructions. That is how businesses keep compliance from turning into a cleanup project later.

If the foundation is wrong, the rest of the system starts to wobble.

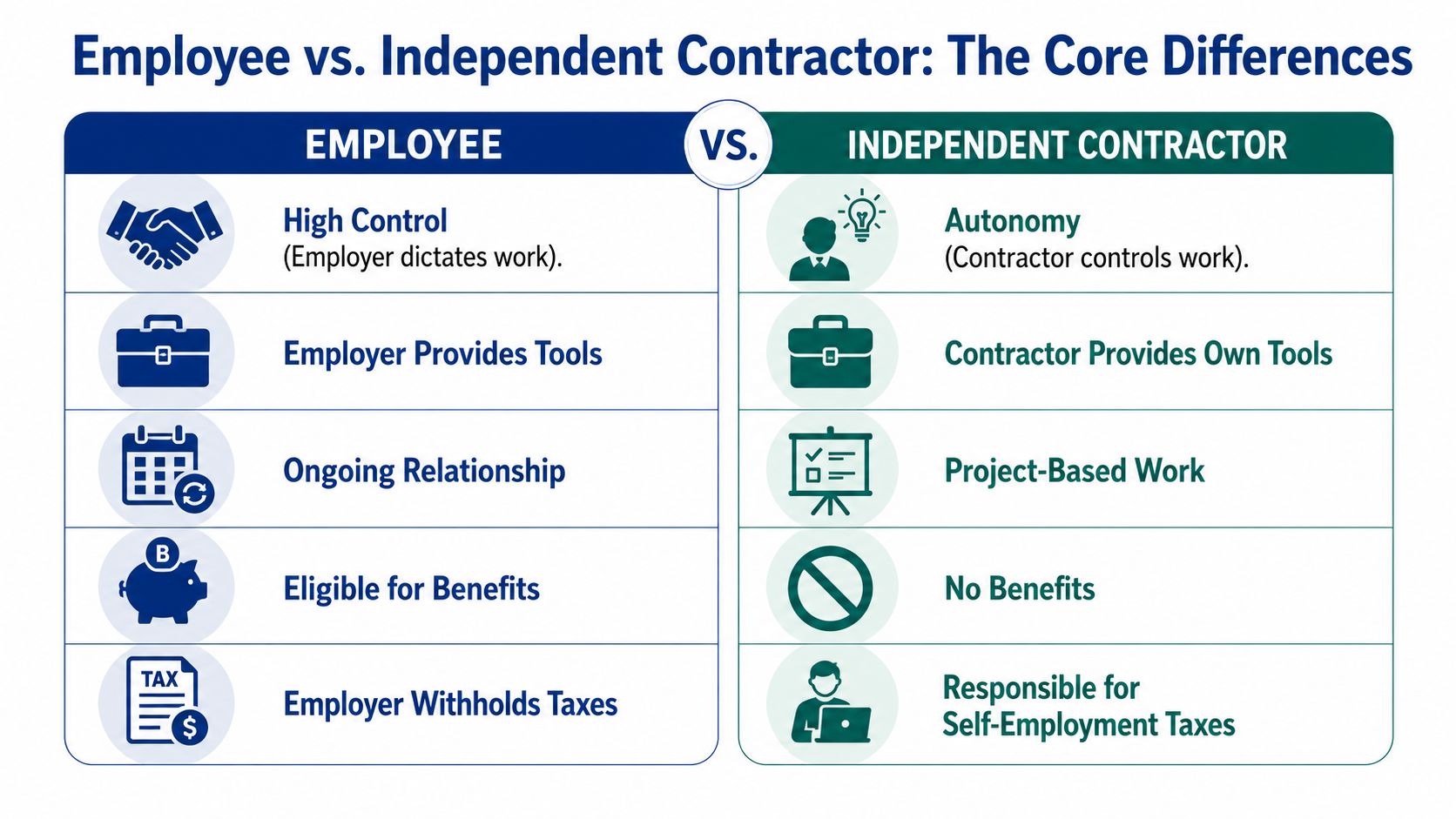

Employee vs Independent Contractor The Core Differences

A simple way to think about this is chauffeur versus car rental.

If you hire a chauffeur, you're paying for a person who works within your instructions, schedule, and standards. That's closer to an employee relationship.

If you rent a car, you're buying access to a resource for a defined purpose. The rental company controls how it runs its business. That's closer to an independent contractor relationship.

What usually separates the two

The biggest difference is control. Employees typically work inside your business. Contractors typically run their own business and deliver a result.

Here's the practical comparison:

| Area | Employee | Independent contractor |

|---|---|---|

| Work control | You direct how, when, and often where work happens | They control how the work gets done |

| Payment | Paid through payroll | Usually paid against invoices |

| Taxes | Employer withholds taxes | Worker handles self-employment taxes |

| Tools and systems | Employer often provides tools, software, and access | Contractor usually provides their own |

| Relationship | Ongoing and integrated into operations | Often project-based or limited-scope |

| Benefits | May be eligible for benefits | Typically not eligible |

If you're weighing the basics before making a decision, this guide to an informed choice on employee or contractor status is useful because it frames the business tradeoffs in plain language.

Payroll treatment changes everything

The classification decision flows directly into payroll operations.

An employee goes into your payroll system. You track wages, withholding, possibly paid time off, and benefit deductions. A contractor usually goes through accounts payable or contractor payment workflows, then receives year-end tax reporting if required. If you need to clean up that reporting process, this walkthrough on how to generate 1099s for contractors is a good operational reference.

A good test is this: are you buying labor inside your business, or are you buying a service from an outside business?

Don't mix this up with exempt and non-exempt

At this point, owners often blend two separate decisions.

First, you decide whether the worker is an employee or independent contractor. If the person is an employee, then you may also need to decide whether they are exempt or non-exempt under the Fair Labor Standards Act.

According to Foothold America's FLSA classification guide, exempt versus non-exempt status requires meeting both a salary threshold of at least $684 per week as of 2020, subject to 2024 updates, and strict duties tests for executive, administrative, or professional roles. Non-exempt employees are entitled to overtime pay for hours worked beyond 40 in a week.

That means a person can be correctly classified as an employee and still be incorrectly treated for overtime.

Titles don't decide status

Calling someone a “consultant,” “specialist,” or “fractional” worker doesn't settle anything. A remote bookkeeper on Slack every day, using your systems, attending your team meetings, and following your deadlines may still look much more like an employee than a contractor.

This is why employee classification has to connect to daily operations, not just HR forms.

Decoding the Legal Tests for Classification

A worker starts as a part-time contractor. Six months later, they have a company email, attend weekly team meetings, use your software stack, and ask a manager for approval before taking time off. Nothing felt dramatic as those changes happened. From a compliance standpoint, though, the relationship may have crossed a line.

That is why the legal tests matter in day-to-day operations. They are not academic checklists for lawyers. They are decision tools that should match how work is assigned, supervised, paid, and recorded in your payroll and HR systems.

Regulators are trying to answer a practical question: Is this worker running their own business, or are they working inside yours?

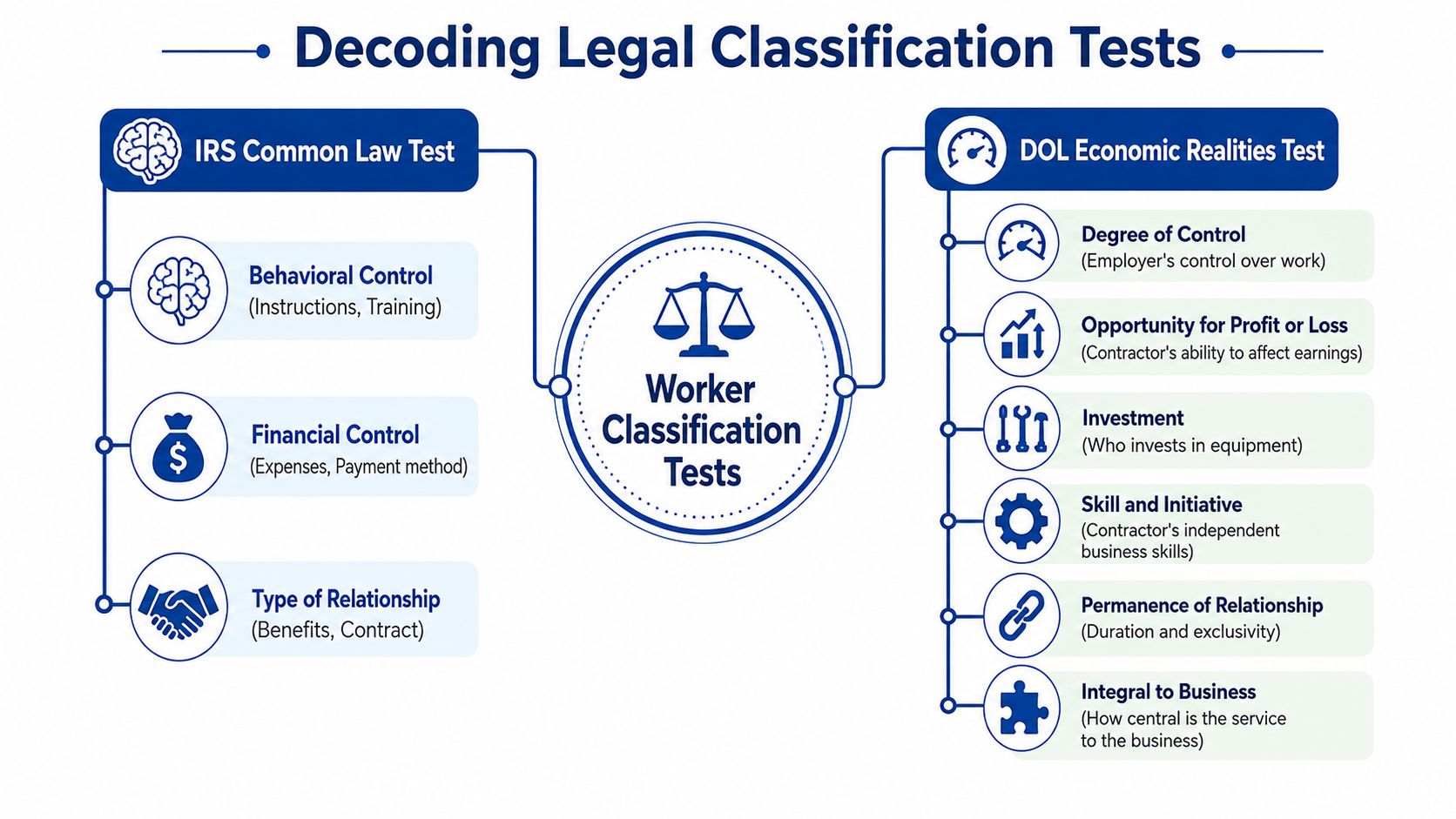

The IRS view of the relationship

The IRS groups its analysis into three buckets: behavioral control, financial control, and the relationship of the parties.

For an owner, those buckets work like an audit lens. One looks at how the work gets done. One looks at who carries business risk. One looks at how the relationship functions in real life.

Behavioral control

Start here: who decides how the work gets done?

If you train the worker on your process, require your scripts, set their schedule, monitor how tasks are performed, and correct their methods, you are showing a level of control that often points to employee status. If the worker chooses the process, tools, and sequence of work and you mainly judge the final result, that leans more toward contractor status.

This part trips owners up because deadlines are normal in both relationships. A contractor can have a due date. The key question is whether you control the route, not just the destination.

Financial control

Next, ask who is taking business risk.

A true contractor usually operates like a small business. They may buy their own equipment, pay for software, set prices, market to other clients, absorb overruns, and increase profit through better decisions. An employee usually does not face that kind of upside or downside. They are paid for their labor, not for running a separate business line.

If the worker depends on your systems, your budget, and your payment structure to earn income, that should get your attention.

Relationship of the parties

Then look at the setup as a whole.

Is the work open-ended? Does the person fill a standing role in the company? Do they appear in org charts, attend regular staff meetings, or receive benefits tied to employment? A written agreement helps, but it is only one piece of evidence. Daily practice carries more weight than labels on paper.

Contracts document the relationship. They do not redefine the facts.

The DOL economic reality test

For wage and hour questions under the FLSA, the Department of Labor applies a broader analysis. According to A&O Shearman's summary of the 2024 DOL rule, the rule uses a six-factor economic reality test and weighs the full picture:

- Opportunity for profit or loss

- Investments by the worker and employer

- Permanence of the relationship

- Nature and degree of control

- Whether the work is integral to the employer's business

- Skill and initiative

This is a multi-factor test. No single fact decides the outcome by itself.

That is why classification work should connect to your actual processes, not just a contract file. A sound review ties these factors to onboarding, time tracking, invoice handling, manager permissions, and payroll compliance controls so the legal conclusion matches the way the worker is treated every week.

How these factors show up in real operations

Here is the practical translation.

- Opportunity for profit or loss: A contractor who can price projects, control costs, subcontract parts of the work, and improve margin through business decisions looks more independent than a worker paid the same recurring amount regardless of results.

- Investment: A web designer using their own laptop, paid tools, business insurance, and client management process looks different from one using your device, your software licenses, and your internal workflow.

- Permanence: A defined project with a clear end date usually looks different from an indefinite arrangement that keeps renewing and becomes the worker's primary source of income.

- Control: Fixed working hours, required attendance at internal meetings, approval chains, and close supervision point toward employee status.

- Integral work: If the worker performs services at the center of what your company sells, they may look less like an outside vendor and more like part of the business.

- Skill and initiative: Specialized skill alone is not enough. The worker also needs to use that skill in an independent business way, such as finding clients, setting terms, and managing delivery.

Where owners get this wrong

Two facts get too much weight in practice. The contract. The worker's preference.

A worker can ask to be paid as a contractor. You can sign an agreement calling them one. If the person works like a supervised member of your team, those facts will not carry the day.

The safer approach is closer to an internal audit than a one-time form choice. Review the facts, document the reasoning, map the decision into payroll and HR workflows, and revisit the classification when the relationship changes. That is how you move from a legal theory to an operating process that holds up.

The High Cost of Misclassification Risks and Penalties

Misclassification usually doesn't show up as one neat problem. It spreads.

A worker files a complaint. Payroll records get reviewed. Overtime treatment gets questioned. Tax handling gets pulled in. Then someone asks why a long-term “contractor” had a company email, fixed schedule, manager approval process, and no real outside business.

That chain reaction matters because classification touches a huge portion of the workforce. In 2023, over 93 million professionals in the U.S. were classified in the “management, professional, and related occupations” group, representing 57.8% of the total workforce, according to workforce data summarized from the U.S. Bureau of Labor Statistics.

What the fallout looks like

When a business gets classification wrong, the consequences can stack up fast:

- Tax exposure: Employers may need to address payroll tax issues tied to workers who should have been on payroll.

- Wage claims: If a worker should have been a non-exempt employee, unpaid overtime can become a major issue.

- Benefits disputes: A worker who was treated as outside the employee group may challenge that exclusion.

- Audit disruption: Management time gets pulled into document gathering, interviews, and response work.

- Operational confusion: Finance, HR, and managers may all be using different assumptions about the same worker.

For many owners, the hidden cost is distraction. A classification problem rarely arrives alone. It often lands during growth, a funding process, a sale review, or a staffing transition, when leadership attention is already thin.

A common small business scenario

A service firm brings on a “contract” operations lead. The person works full time, uses the company's QuickBooks and Gusto environment, joins recurring management meetings, and reports to the owner. After a dispute, the company has to reconstruct payment history, time expectations, and role duties.

That's when the administrative shortcut stops being a shortcut.

If you want a broader operational lens on how classification connects to wage rules, filings, and documentation, this explainer on payroll compliance for business owners is worth reviewing.

A short overview can help frame the risk before you begin your own review:

Bottom line: Misclassification is rarely just an HR issue. It becomes a payroll, tax, legal, and management issue all at once.

How to Conduct an Employee Classification Audit

An employee classification audit is like a financial cleanup. You don't start by arguing about labels. You start by gathering facts.

Start with a complete worker roster

List every person performing work for the business, not just payroll employees. Include freelancers, consultants, virtual assistants, remote specialists, seasonal help, and anyone paid outside standard payroll.

Then collect the records that show how the relationship works:

- Contracts and amendments: Review the written terms, but don't stop there.

- Invoices and payment records: Check whether billing reflects project work or recurring payroll-like compensation.

- Job descriptions and scopes: Compare stated duties with actual duties.

- System access: Look at company email, Slack, project tools, time tracking, and software permissions.

- Manager practices: Ask who approves the work, who sets priorities, and who controls the schedule.

Apply the facts, not the title

Once you have the file, test each worker against the practical factors discussed earlier. A simple review works well:

- Who controls the workday? If your manager sets hours, meetings, and methods, that's a warning sign.

- Who supplies the tools? Company laptop, software licenses, and standardized workflows can matter.

- Is the relationship indefinite? Long-running, exclusive arrangements deserve a closer look.

- Is the work central to the business? Core service delivery often raises risk.

- Does the worker operate an independent business? Look for multiple clients, separate branding, and business autonomy.

Pay special attention to remote workers

Remote work confuses a lot of employers because distance can make a worker feel independent when the facts say otherwise.

A key point from Woods Rogers' discussion of the DOL's 2024 economic realities approach is that remote IT and specialized workers can still be employees. Set hours, company-provided equipment, and managerial oversight matter more than physical location.

If a remote worker logs into your systems on your schedule under your supervision, don't assume distance makes them a contractor.

Build a repeatable review process

A one-time cleanup helps, but ongoing review is what protects you as the business grows.

Use a checklist at these trigger points:

- Before onboarding a contractor

- When a project expands into ongoing work

- When a contractor becomes exclusive to your business

- When a manager starts supervising the person like staff

- Before year-end tax reporting

If you want an outside benchmark for audit thinking, Beacon Recruitment's compliance and audit consulting shows the kind of structured review framework businesses often need when documentation and worker status drift apart.

For the payment side of the process, this guide on how to pay contractors correctly can help align classification decisions with accounts payable and tax reporting procedures.

From Audit to Action Remediation and Integration

A classification audit is like finding bad wiring behind a wall. The report matters, but the repair work is what keeps the building from failing inspection later.

Start by turning each audit finding into a case file. For each worker, decide four things: the correct status, the date the change starts, the pay impact, and the systems that need updating. That keeps the legal decision tied to payroll, onboarding, and accounting instead of leaving it as a memo no one operationalizes.

A practical remediation workflow looks like this. After reclassifying a freelance designer to W-2 employee status, the payroll team updates the worker's profile in Gusto, sets tax withholding, and assigns the person to the correct pay schedule. HR sends the employee offer letter and I-9 instructions, then opens benefit eligibility if the plan rules apply. Accounting closes the designer's vendor record in QuickBooks so future payments do not keep going through accounts payable. The manager gets a short note explaining the new rules on timekeeping, overtime approval, and supervision.

That sequence matters. If payroll changes the worker but AP keeps paying old invoices, or if HR enrolls the person but managers still treat them like an outside contractor, you have fixed the file and missed the process.

Reclassification also affects money already paid. Review whether prior payments need to be corrected through payroll, whether unpaid overtime may be owed, and whether tax filings need amendment. If the issue is exempt versus non-exempt status, confirm the salary basis and actual job duties before coding the role in payroll. Job titles are labels. Pay rules follow the work being done.

Use a short control workflow that forces the right handoffs:

- Open a remediation ticket with the worker's name, current status, corrected status, and effective date

- Assign owners across HR, payroll, AP, and the worker's manager

- Update every record tied to the worker, including payroll profile, vendor status, onboarding documents, and manager instructions

- Run a first-paycheck check to confirm taxes, earnings codes, overtime treatment, and benefit deductions are correct

- Store the reasoning and approvals with the worker record so the next reviewer can see why the classification changed

Many businesses lose control when the legal review sits in one folder, payroll setup happens in another system, and AP never gets the message. A good process connects those steps so one classification decision flows into every place the worker appears.

If your stack includes QuickBooks, Gusto, and a separate bill-pay process, treat classification like a master setting, not a one-time opinion. Once a worker is coded correctly, that status should drive how they are onboarded, how they are paid, which forms they receive, and who can approve changes later. An outside advisor adds value here by translating the legal conclusion into payroll codes, approval checkpoints, and recurring review rules your team can follow.

If you want help turning classification decisions into clean payroll setup, documented workflows, and ongoing compliance support, Steingard Financial can help build the back-office process around your hiring reality, not just your year-end forms.