You formed the LLC. The bank account is open. Clients are finally paying. Then the question hits fast: how do you take money out without creating a tax mess or wrecking your bookkeeping?

That’s where a lot of new owners get stuck. They know the business has money, but they’re unsure whether to transfer cash to a personal account, run payroll, call it a draw, or wait for year-end. For service businesses using QuickBooks and Gusto, the right answer depends less on preference and more on how the LLC is taxed and how disciplined the back office is.

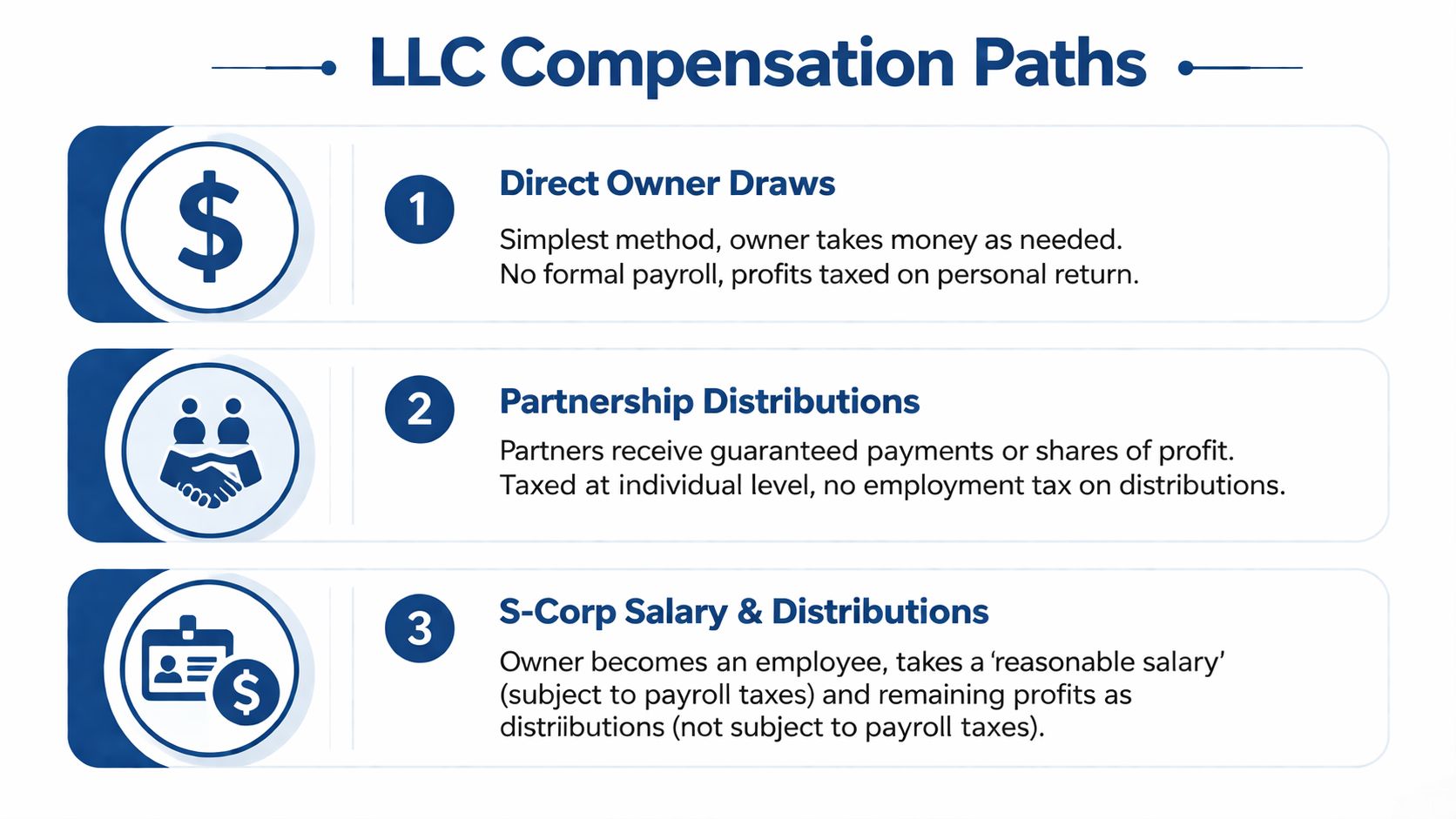

If you want to pay yourself llc the right way, there are really three lanes: owner’s draws, partnership distributions or guaranteed payments, and salary plus distributions for an LLC taxed as an S corporation. Each works. Each creates different tax, payroll, and recordkeeping obligations. The trick is matching the method to the entity setup you have, not the one you assumed you had.

Your LLC is Official Now How Do You Get Paid

A familiar version of this happens all the time. A consultant forms a single-member LLC on Monday, lands a client on Friday, gets paid the next week, and then hesitates before moving any money. They don’t want to “do payroll wrong.” They also don’t want to treat the business account like a personal checking account.

That hesitation is healthy. The mistake isn’t asking the question. The mistake is guessing and hoping the books can be cleaned up later. In practice, the cleanest compensation method depends on whether you’re a solo owner taxed by default as a sole proprietorship, a multi-member LLC taxed as a partnership, or an LLC that elected S corporation treatment.

Most LLC pay problems start as bookkeeping problems. The owner took money correctly in substance, but recorded it incorrectly, mixed accounts, or skipped the tax planning that should have happened first.

The good news is that this isn’t mysterious once you separate the legal entity from the tax treatment. A draw, a distribution, and a salary all move money from the business to the owner. But they aren’t interchangeable, and QuickBooks should not treat them the same way.

Choosing Your Compensation Path

The right compensation path starts with one question: how is your LLC taxed right now? The legal label “LLC” doesn’t answer that by itself.

The three paths in plain English

A single-member LLC usually defaults to sole proprietorship tax treatment. In that setup, the owner typically pays themselves with an owner’s draw. There’s no owner payroll just because the business exists. The money comes out of the business account and reduces owner’s equity in the books.

A multi-member LLC usually defaults to partnership taxation. Owners don’t usually go on payroll just because they’re active in the business. Instead, compensation is commonly handled through guaranteed payments, profit distributions, or both, based on the operating agreement and tax reporting structure.

An LLC taxed as an S corporation is different. Once that election is in place, the owner who works in the business generally needs to be paid a reasonable salary through payroll, and then may take additional distributions. That’s where tax planning gets more involved, and where tools like Gusto matter because payroll compliance stops being optional.

Side by side comparison

| Compensation path | Best fit | Admin burden | Core tax treatment |

|---|---|---|---|

| Owner’s draw | Solo owners who want simplicity | Lower | Profit passes through to the owner’s return |

| Partnership payments | Businesses with multiple members | Moderate | Income is allocated to members and reported through K-1s |

| S-corp salary and distributions | Established profitable service businesses that can support payroll compliance | Higher | Salary runs through payroll, distributions are handled separately |

Core trade-off: the simpler the method, the easier the administration. The more tax optimization you pursue, the more documentation, payroll discipline, and scrutiny you should expect.

What works well and what usually doesn’t

Owner’s draw works well when the business is new, cash flow is uneven, and the main priority is keeping the books clean. This is often the right starting point for solo service providers.

Partnership-style payments work well when the owners agree in writing how compensation should happen. They work badly when one partner assumes effort should drive pay and another assumes ownership percentage should drive everything.

S-corp treatment works well for businesses with steady profit, enough maturity to support payroll, and good documentation for compensation decisions. It works badly when the owner wants the tax benefit but doesn’t want the payroll process, quarter-end filings, or salary support.

A practical decision lens

Ask these questions before changing anything:

Are you the only owner

If yes, owner’s draw may be the default unless you elected S-corp taxation.Do you have a signed operating agreement that addresses owner pay

If not, a multi-member LLC is exposed to avoidable confusion.Can your current systems support payroll

If QuickBooks isn’t reconciled and no one is reviewing payroll liabilities, an S-corp setup will create more problems than savings.Is the business consistently profitable

Tax strategy should follow stable operations, not substitute for them.

The mistake many owners make is choosing based on what sounds cheapest in taxes without asking whether the books, cash flow, and compliance process can support that choice.

The Owner's Draw Method for Single-Member LLCs

If you run a single-member LLC taxed as a sole proprietorship, the clean method is usually an owner’s draw. That means you move money from the business account to your personal account and record it as an equity transaction, not payroll and not a business expense.

The practical steps are straightforward. Open a dedicated business bank account, transfer money from that account to yourself when appropriate, record each draw in the books as a reduction to owner’s equity, and set aside 25% to 35% of draws for quarterly estimated taxes, because profits pass through to your personal return on Schedule C and are subject to self-employment tax and income tax according to this single-member LLC owner draw walkthrough.

How to move the money correctly

A lot of owners overcomplicate the banking side. You don’t need a fancy mechanism. You need a clean one.

Use a business check, ACH transfer, or bank transfer from the LLC account to your personal account. In the memo or transaction note, label it consistently as Owner’s Draw. If you use the business debit card for personal spending, the same economic result may exist, but the bookkeeping gets uglier fast and the audit trail gets weaker.

The separate bank account matters for more than convenience. It supports the liability shield by avoiding commingling. It also makes reconciliation easier inside QuickBooks, because transfers out to the owner can be identified and categorized consistently.

If the transfer leaves the business account and benefits the owner personally, QuickBooks should usually point that transaction to an equity account, not to meals, office expense, subcontractors, or some catch-all bucket.

How to record it in QuickBooks

In QuickBooks Online, create an equity account such as Owner’s Equity or Owner’s Draw. When the transfer happens, categorize the outflow there.

If you’re thinking in journal-entry form, the entry is:

| Account | Debit | Credit |

|---|---|---|

| Owner’s Equity / Owner’s Draw | amount of draw | |

| Cash | amount of draw |

That entry is important because it answers a common misconception. The draw does not reduce business profit on the profit and loss statement. It reduces owner equity on the balance sheet. If you book it as an expense, you distort margins, understate net income, and create confusion at tax time.

What taxes catch owners off guard

A single-member LLC owner often assumes tax is tied to how much cash they withdrew. It isn’t. Tax is generally tied to business profit, not the timing of draws.

That’s why a profitable month can create tax exposure even if you leave most of the money in the business. It’s also why a low-draw month doesn’t guarantee a low tax bill. Good books matter because the tax estimate should come from actual results, not from what felt affordable to transfer.

For owners trying to keep the accounting tight, a good foundation is disciplined categorization, monthly reconciliation, and documentation of each owner transfer. This is also where strong record keeping for small business saves a lot of cleanup later.

What works in practice

For a solo consultant, designer, agency owner, or therapist, the clean rhythm usually looks like this:

- Pay business bills first so operating cash stays visible.

- Transfer owner pay intentionally on a regular cadence instead of random swipes.

- Record every draw to equity in QuickBooks immediately.

- Hold tax money separately so estimated payments don’t compete with rent or payroll.

What doesn’t work is treating the business account like a shared household wallet. The draw method is simple, but only if the records are disciplined.

Compensating Owners in a Multi-Member LLC

A multi-member LLC adds a layer of complexity because the payment question is no longer just tax-related. It’s also about governance. Owners can agree to many compensation structures, but if they don’t put the rules in writing, routine payments turn into arguments.

By default, a multi-member LLC is generally taxed as a partnership. Payments can be handled through guaranteed payments, distributions from capital accounts, or a combination, and the operating agreement should spell out draw schedules and profit splits according to this multi-member LLC payment overview. That same guidance notes that members should typically set aside 25% to 35% for quarterly estimated taxes, and that unequal draws without an agreement cause disputes in an estimated 40% of multi-member LLCs.

Guaranteed payments versus distributions

These two items often get blurred together, but they solve different problems.

Guaranteed payments are fixed payments to a member for services or use of capital, regardless of whether the LLC is profitable for the period. They’re useful when one owner is doing substantially more of the day-to-day work and needs predictable compensation.

Distributions are allocations of profit or capital based on the operating agreement. They’re not the same thing as “who worked hardest this month.” They follow the ownership and agreement framework.

Here’s the practical distinction:

| Payment type | Best use | Bookkeeping focus |

|---|---|---|

| Guaranteed payment | One member needs regular compensation for active work | Record consistently and reflect partnership treatment correctly |

| Distribution | Owners share profits based on agreed terms | Track by member equity or capital account |

A service business example

Take a two-owner marketing firm. One member manages delivery and client communication every day. The other member focuses on sales and strategy and is less involved in weekly operations. If they split all cash evenly whenever there’s money in the bank, resentment tends to build.

A better structure is to decide, in writing, whether one member receives a guaranteed payment for operational work and whether remaining profits are distributed by ownership percentage. That approach separates compensation for labor from return on ownership. It also gives the bookkeeper clear rules for coding transactions in QuickBooks.

What QuickBooks should show

The books need to reflect each member separately. In practice, that usually means separate equity accounts or capital accounts for each owner so distributions don’t get blended together.

If the LLC issues a distribution to one member, the bookkeeping should reduce that member’s equity balance rather than posting the payment to an operating expense account. If the payment is a guaranteed payment, it should be tracked distinctly so year-end reporting is accurate.

In a multi-member LLC, vague bookkeeping usually mirrors vague agreements. When owners don’t define the payment method, the accounting team ends up guessing what the transaction was supposed to mean.

Tax reporting and owner expectations

Another point that catches owners by surprise is the mismatch between cash received and taxable income. A member may owe tax based on the K-1 allocation even if the LLC retained cash for operations or expansion. That’s why partnership compensation decisions should include both cash policy and tax reserve policy, not just profit split language.

For service businesses, this is where monthly review matters. If one owner is taking ad hoc draws and another is waiting for a formal distribution, you don’t just have a tax issue. You have a governance issue with a bookkeeping symptom.

Unlocking Tax Savings with an S-Corp Election

For the right service business, an S-corp election can be the most valuable move in the pay yourself llc conversation. It’s not the simplest route, but it can materially change the tax profile of owner compensation when profits are strong enough to support a reasonable salary and formal payroll.

According to Homebase’s LLC owner compensation guide, an LLC generating $200,000 in annual profits could owe about $30,600 in self-employment taxes under traditional LLC treatment. In the same profit scenario, an S-corp election can reduce FICA taxes to about $6,885, producing potential annual tax savings of over $16,000. The reason is structural. The owner pays themselves a reasonable salary subject to payroll taxes and takes the remaining profit as distributions that avoid self-employment tax. The same guidance also notes that the IRS heavily scrutinizes whether that salary is reasonable.

Why this works for some service businesses

This setup often fits established firms with predictable profit and clean books. Think agencies, consultancies, accounting firms, design studios, and similar service businesses where the owner’s role can be described, benchmarked, and documented.

It’s a poor fit if cash flow is erratic, payroll feels premature, or the books are behind. An S-corp election is not just a tax checkbox. It creates an operational requirement to run payroll correctly, withhold and remit payroll taxes, and handle the employment tax side of the business.

That’s where Gusto can be useful. Once the owner must be paid through payroll, a payroll platform helps manage wages, filings, and recurring runs. But software only works if the compensation logic behind it is sound.

The reasonable salary issue

The biggest mistake in this area is chasing distributions and minimizing salary so aggressively that the setup stops looking credible.

The IRS standard for reasonable compensation is qualitative in practice. Similar work, similar businesses, similar circumstances. If the owner is the revenue engine, account manager, and operator, a token salary won’t hold up well.

A sensible process usually includes:

- Defining the owner’s actual role so the salary reflects real duties.

- Looking at comparable market pay for similar work in similar businesses.

- Documenting the rationale in case the salary decision is ever questioned.

- Reviewing the number periodically as the business grows or the role changes.

Tax savings are real, but they only hold if the salary side of the structure is defensible.

A strong payroll setup also needs coordination between payroll and bookkeeping. Gusto can process the payroll. QuickBooks should receive or mirror the accounting accurately so wages, employer taxes, and owner distributions don’t get blended together.

What the workflow looks like

Once an S-corp election is active, the owner should generally stop treating every cash transfer as a casual draw. Compensation needs a cleaner split.

The recurring sequence usually looks like this:

- Run owner payroll through Gusto on a defined schedule.

- Record payroll and payroll taxes correctly in QuickBooks.

- Take separate owner distributions only after reviewing cash flow and retained obligations.

- Keep documentation supporting the salary decision with the tax file.

For businesses trying to tighten that process before year-end, a practical checkpoint is stronger planning around books, payroll, and documentation before filings start. A useful preparation step is building a clean close process and tax packet using guidance like this how to prepare for tax season resource.

A short walkthrough can also help make the structure easier to visualize:

When owners should slow down

Not every profitable LLC should elect S-corp treatment immediately. If the owner hasn’t separated personal and business spending, doesn’t reconcile QuickBooks monthly, or doesn’t have confidence in payroll compliance, then complexity may arrive before discipline does.

In practice, the best candidates are businesses that can support both the tax strategy and the process that makes the strategy defensible.

Common LLC Payroll Pitfalls and How to Avoid Them

Most LLC compensation problems don’t start with bad intent. They start with shortcuts. A transfer gets miscoded. A personal expense hits the business card. Payroll gets delayed because cash was tight. Then tax season exposes everything at once.

The first recurring issue is commingling. If the owner uses the business account for personal life and tries to sort it out later, the books lose clarity fast. Even when the right answer is “that was a draw,” the accounting team now has to reconstruct intent from bank activity instead of following a clean compensation policy.

The second issue is misclassification inside QuickBooks. Distributions and draws often get posted to expense accounts because someone wanted the bank feed cleared quickly. That distorts the profit and loss statement and creates confusion around what the business spent versus what the owner withdrew.

The salary trap in S-corp setups

The most serious problem is usually the unreasonably low S-corp salary. According to Bench’s discussion of paying yourself from an LLC, the IRS defines reasonable compensation as what similar enterprises would pay for similar services. The same source notes that a salary of $1,000 paired with $90,000 in distributions is a major audit trigger, and reports a 25% increase in S-corp owner compensation audits. It also notes that many audits target salaries below the 50th percentile of industry norms, and that service industry managers may see a median range of $80K to $120K in BLS data.

That matters because owners often hear “pay yourself a reasonable salary” but never operationalize it. In practice, that means documenting duties, time spent, market comparisons, and why the salary makes sense for the business. A low number without support is not strategy. It’s exposure.

If you’re weighing entity structure more broadly, a legal overview like this S Corp vs C Corp guide from Coto & Waddington can help frame the election decision before you layer payroll into it.

Other mistakes that create preventable pain

Skipping quarterly tax planning

LLC owners who aren’t on standard payroll withholding often under-save for taxes and then scramble when estimates are due.Running payroll without reviewing liabilities

Payroll isn’t just net pay. It creates tax liabilities that need to be tracked, remitted, and reconciled. A clean primer on that side is this explanation of what are payroll liabilities.Using distributions to solve cash management

If the business account is used as a pressure valve whenever personal cash is tight, there’s usually no compensation policy at all. There’s just drift.

Good compliance is boring on purpose. The cleaner the routine, the less likely you are to create a year-end surprise.

LLC Owner Pay Compliance Checklist

| Area | Check | Why It Matters |

|---|---|---|

| Banking | Separate business and personal accounts are maintained consistently | Supports liability protection and clean reconciliations |

| Owner pay method | The LLC uses the compensation method that matches its tax treatment | Prevents payroll and tax mismatches |

| QuickBooks coding | Draws, distributions, and payroll are each posted to the right accounts | Keeps P&L and balance sheet accurate |

| Tax reserves | Money is being set aside for owner tax obligations | Reduces underpayment surprises |

| Operating agreement | Multi-member payment rules are written and current | Prevents disputes over timing and allocation |

| Payroll process | S-corp owner payroll runs on a defined schedule | Supports filing compliance |

| Salary support | Reasonable compensation is documented for owner-employees | Helps defend the compensation structure |

| Reconciliation | Bank, credit card, and payroll accounts are reviewed regularly | Catches coding errors before they compound |

What actually works

For most service businesses, the safest answer is consistency. Pick the proper compensation structure, run it the same way each month, and let the books tell the truth. Owners get into trouble when they mix methods, override the system for convenience, or let tax goals outrun documentation.

A Recommended Workflow for Service Businesses

The cleanest pay yourself llc workflow for a modern service business usually combines QuickBooks Online for accounting and Gusto for payroll. Not because software solves judgment, but because it supports a repeatable process once the compensation method is set correctly.

A monthly rhythm that scales

For a single-member LLC using owner’s draws, the workflow is simple. Revenue lands in the business account. Bills get paid from that account. The owner transfers a planned amount to personal, and QuickBooks codes it to owner’s equity. The books get reconciled monthly so every owner transfer is captured correctly.

For a multi-member LLC, the workflow needs more structure. Owner payments follow the operating agreement, not whoever asked first. QuickBooks tracks separate member equity accounts or capital balances, and the team reviews whether each payment was a guaranteed payment or a distribution before closing the month.

For an S-corp taxed LLC, Gusto becomes central. Payroll runs on schedule, taxes are withheld and remitted through the payroll system, and any owner distributions are recorded separately in QuickBooks after cash review.

Journal entries that keep the books clean

For an owner’s draw, the entry is straightforward:

| Entry | Debit | Credit |

|---|---|---|

| Owner’s Draw / Owner’s Equity | draw amount | |

| Cash | draw amount |

For payroll, the exact detail can vary by chart of accounts and payroll mapping, but the concept should stay clean:

- Debit wage expense for gross payroll

- Debit payroll tax expense for employer taxes

- Credit cash or payroll clearing for the amount funded

- Credit payroll liabilities for taxes and withholdings until remitted

That’s where service businesses often benefit from letting Gusto handle payroll mechanics while QuickBooks remains the general ledger of record. The key is making sure the mapping is reviewed, not assumed.

The operating discipline that matters most

Three habits tend to make this system work:

- Close the books monthly so compensation errors don’t linger.

- Review owner pay against cash flow before money leaves the business.

- Keep documentation with the file for distributions, guaranteed payments, and S-corp salary support.

A compensation method should reduce stress, not create cleanup work every quarter. If your current process depends on memory, manual fixes, or recategorizing transactions months later, it’s time to tighten the workflow.

If you want help building a clean QuickBooks and Gusto process for owner compensation, Steingard Financial helps service businesses across the U.S. set up bookkeeping, payroll, reconciliations, and reporting systems that make paying yourself accurate, compliant, and manageable.