You're doing the work. Your team is busy. Clients are getting billed. Money is coming in.

But when you ask simple management questions, the answers are fuzzy.

Which projects are profitable? Are you hiring too early or too late? Is cash tight because the business is weak, or because invoices lag behind delivery? Why does the P&L look strong while the bank balance says something else?

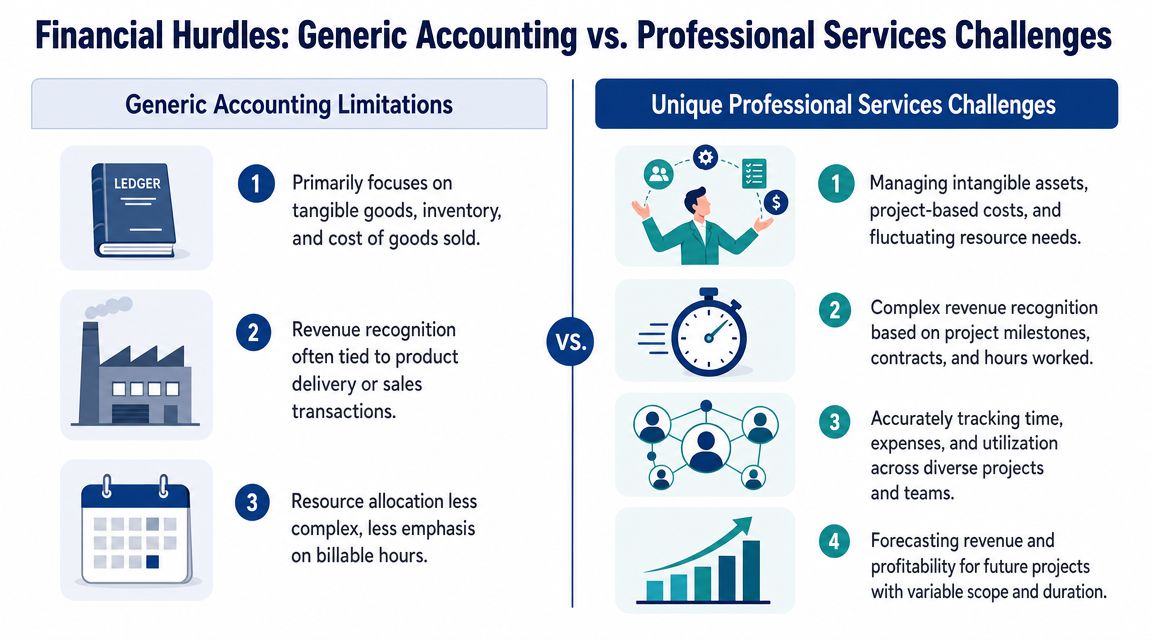

That's where many service businesses hit the limits of generic accounting. A system built around products, inventory, and one-time sales won't give you clean visibility when your real product is time, expertise, and delivery across projects. For a consulting firm, agency, law practice, design studio, IT services company, or outsourced operations team, the accounting model has to reflect how value is created.

Why Your Service Business Needs More Than Generic Accounting

A product business asks accounting questions like these: What did we sell? What did it cost to produce? What's left in inventory?

A service business asks different ones. Which client work consumed the most senior time? How much revenue have we earned on an ongoing engagement? Are we over-servicing retainers? Is the team stretched, underused, or assigned to the wrong mix of work?

That difference matters because professional services accounting is designed around labor, projects, contracts, and timing gaps between work performed, invoices sent, and cash collected. It's not a cosmetic variation on standard bookkeeping. It's a different lens for running the business.

The scale of the market makes that clear. IBISWorld projects the U.S. accounting services industry at $158.4 billion in 2026, with 85,412 businesses in the industry, after 1.4% CAGR growth over the prior five years, which shows how central accounting infrastructure has become across the service economy (IBISWorld accounting services industry data).

Practical rule: If your product is expertise, your accounting system should answer operational questions, not just tax questions.

Generic accounting often gives owners a backward-looking record of activity. Professional services accounting should give you something more useful: a way to connect financial statements to staffing, pricing, delivery, and growth decisions.

That means your books need to do more than stay clean for year-end. They need to tell you, in near real time, whether:

- Work is earning well against the labor going into it

- Billing is aligned with how services are delivered

- Cash timing is manageable even when projects run ahead of invoices

- Team capacity supports growth without creating margin leakage

If those answers aren't clear today, the issue usually isn't effort. It's that the accounting setup wasn't built for a service business in the first place.

Defining Professional Services Accounting

Think of a retail store. It buys goods, holds inventory, sells units, and records revenue at the point of sale. The accounting system follows the movement of products.

Now think of a service firm. It sells judgment, time, deliverables, and access to skilled people. There's no shelf of inventory to count. Instead, the business has to coordinate contracts, hours, project costs, milestones, expenses, billing events, and team assignments. That looks less like a store and more like a production schedule.

The core difference

At its simplest, professional services accounting is the financial management of businesses that deliver work through people and projects.

NetSuite notes that modern professional-services accounting supports project-based and time-based delivery models, where revenue may be recognized over time or tied to milestones. The same market overview says U.S. accounting services revenue reached $145.7 billion in 2023 from $144 billion in 2022 (NetSuite on accounting for professional services).

That shift matters because the system has to track economic reality before cash changes hands. If your team has already done half the work on a client engagement, management needs visibility into that progress whether the invoice has been issued yet or not.

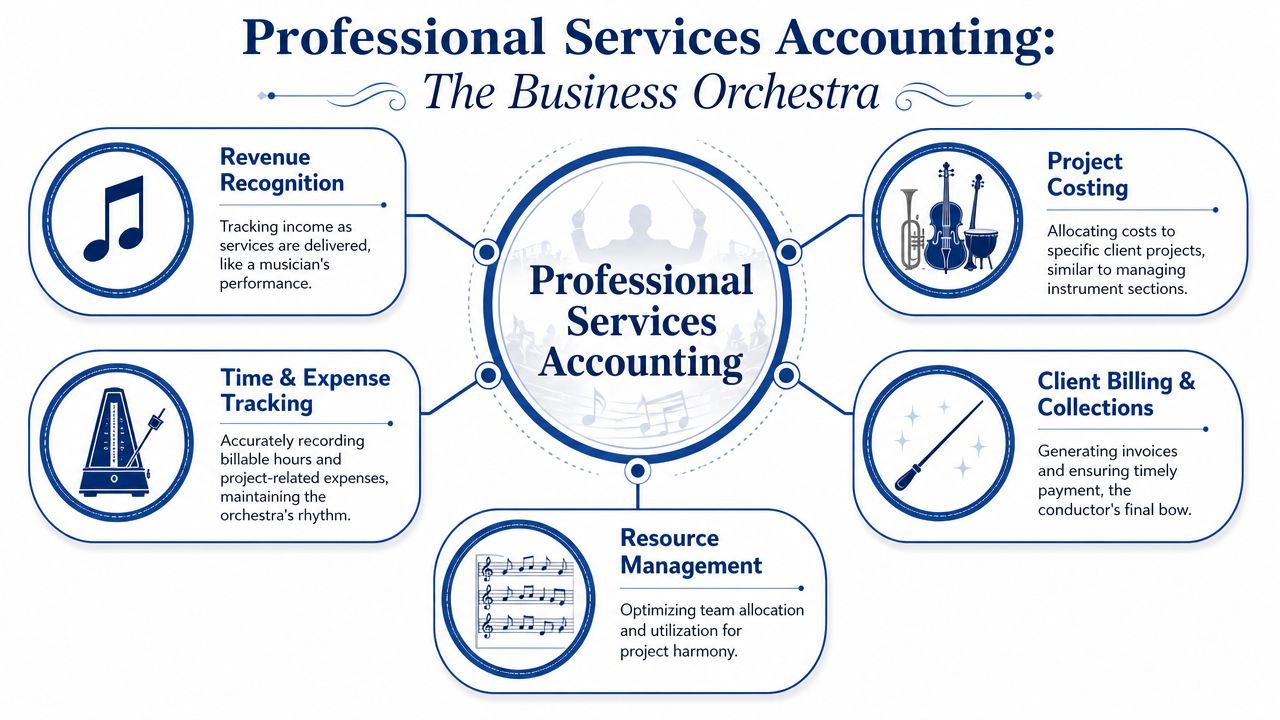

The three pillars owners should understand

Most confusion disappears once you break the model into three working parts.

Project accounting

Every engagement needs its own financial story. You want to know what was budgeted, what was delivered, what it cost, what's been invoiced, and what margin remains. Looking only at company-wide totals hides weak projects behind strong ones.Time and expense tracking

In many service firms, time is the raw material. Hours logged by employees or contractors shape billing, revenue recognition, utilization, and project profitability. Expenses tied to client work need the same discipline, or margins get distorted.Resource management

People drive delivery, so staffing decisions are financial decisions. When the wrong level of talent is assigned, when senior people do junior work, or when the bench grows faster than demand, the accounting impact shows up quickly.

A healthy service business doesn't just record what happened. It links delivery data to financial outcomes so leaders can act sooner.

What owners usually get wrong

The most common mistake is treating accounting, operations, and staffing as separate systems. In a service business, they overlap every day.

A cleaner way to think about it is this:

| Business question | Accounting answer needed |

|---|---|

| Are we making money on this client? | Project-level revenue and cost visibility |

| Can we afford to hire now? | Capacity, payroll impact, and cash outlook |

| Why is cash behind profit? | Timing differences between delivery, billing, and collection |

| Which work should we sell more of? | Margin by service line, client, or team mix |

That's the purpose of professional services accounting. It gives owners a financial operating system for a business built on people rather than products.

Navigating the Unique Financial Challenges of Service Firms

Most service firms don't struggle because they ignore accounting. They struggle because the hard parts sit in the spaces between systems.

Work starts before billing. Billing happens before cash collection. Team costs hit payroll on a fixed schedule even when client payments are uneven. And when an engagement changes shape midway through, the accounting has to keep up.

Revenue recognition is harder than invoicing

This is one of the biggest blind spots.

A client invoice tells you what you billed. It doesn't always tell you what you've earned. That gap becomes especially important on retainers, milestone contracts, long projects, and engagements with multiple deliverables.

NetSuite highlights an underserved issue in professional services accounting: firms need practical help recognizing revenue when work is performed over time, on retainers, or with milestone-based billing. It also points to common pain points such as contract decomposition, variable consideration, and aligning invoices with the actual transfer of services (NetSuite on revenue recognition for professional services).

Here's where owners often get confused:

- Invoice sent does not always equal revenue earned

- Cash received does not always equal project completed

- Project progress may create earned revenue before the billing event

If those ideas aren't separated, monthly results swing for accounting reasons rather than business reasons.

Project profitability often looks better than it is

A firm may look busy and still have weak margins.

That usually happens when teams price based on expected effort, then fail to capture the actual labor mix, rework, write-offs, or unbilled over-servicing. The client may seem profitable at a glance because revenue is visible. The hidden cost is buried in payroll and overhead.

A better approach is to review profitability through multiple lenses:

- By project to catch scope drift

- By client to identify accounts that consume too much attention

- By service line to see which offerings deserve more sales focus

- By staffing mix to see whether senior labor is being deployed correctly

If you can't explain why a project made money, you probably can't repeat that success intentionally.

Cash flow pressure comes from timing, not just performance

Owners sometimes assume cash strain means the firm is underperforming. In service businesses, timing is often the primary issue.

Work may be delivered this month. Payroll is paid on schedule. The invoice goes out later. Payment arrives later still. That delay creates stress even when the client relationship is healthy.

This is why a firm can post profit on paper and still feel squeezed operationally. The accounting system needs to show not only profitability, but also the lag between delivery, billing, and collections.

Utilization affects margin more than many owners realize

In a people-heavy business, capacity decisions shape profit quickly.

If billable staff spend too much time on internal work, low-value admin, or poorly scoped client requests, revenue per team member drops. But very high utilization can create a different problem. Teams get overextended, delivery quality slips, and leaders lose room for business development or process improvement.

That's why service firms need accounting that reflects operational reality, not just compliance categories.

Best Practices for Bookkeeping Billing and Payroll

The fix usually starts with discipline, not complexity. Most service firms don't need a giant finance stack. They need a clean structure, consistent rules, and tools that map to how the business earns money.

Use accrual accounting if projects span time

For most service firms, accrual accounting is the better foundation because project work, invoicing, and resource consumption rarely happen at the same moment. Fyle explains that accrual-based reporting records revenue and expenses when they occur, which smooths income volatility and gives a more accurate view of profitability across projects (Fyle on professional services accounting).

Cash-basis books can be useful for simple tax conversations. They're much less useful for managing a business where work and payment timing diverge.

If you're trying to decide whether to hire, adjust pricing, or cut a service line, you need a view that reflects earned work and incurred cost, not just bank activity.

Build the books around projects, not just categories

A standard chart of accounts isn't enough on its own. You also need a consistent way to tag work by client, project, service line, or class in QuickBooks so management reports can answer real questions.

A practical setup often includes:

- Revenue separation by service type, such as recurring retainers, project fees, or reimbursable income

- Direct labor clarity so payroll tied to delivery can be reviewed against revenue

- Expense tagging for software, contractors, travel, and other items that affect project margin

- Project coding rules so time, bills, and invoices land in the same reporting lane

If your current books don't support that level of visibility, this guide to how to do bookkeeping is a useful baseline for cleaning up the structure before you add more reporting layers.

Match billing model to delivery reality

Billing problems often start in sales, not finance. If the contract doesn't reflect how work will unfold, accounting gets messy later.

Common models include:

- Time and materials when scope is flexible and tracking hours matters

- Fixed-fee when deliverables are well defined and change control is strong

- Retainers when clients buy ongoing access, recurring support, or a standing allocation of capacity

- Value-based pricing when the engagement outcome matters more than hours, though internal cost tracking still matters

The key is consistency. Revenue treatment, invoice timing, and internal project tracking should all match the structure of the agreement.

Treat payroll as an operating system

In service firms, payroll isn't just an HR function. It's one of the main drivers of margin, utilization, and capacity planning.

That's why owners should pay attention to role definitions, compensation logic, contractor treatment, onboarding timing, and payroll software integration. If your team includes remote or international complexity, comparing top UK payroll solutions for small businesses can help you think through feature gaps before they become reporting problems.

For U.S.-based firms using QuickBooks and Gusto, some owners also work with providers such as Steingard Financial to align bookkeeping, payroll entries, reconciliations, and reporting inside one service-business workflow.

Working rule: Every payroll decision becomes an accounting decision once you need to understand margin by team, client, or service line.

The KPIs That Drive Profitability and Growth

Good reporting doesn't drown you in metrics. It gives you a short list that helps you decide what to do next.

For service firms, that usually means measuring team output, project economics, and the relationship between labor capacity and revenue. Sikich identifies utilization rate as a core operating metric in professional services and defines it as billable hours divided by total available hours. It also notes that utilization should be read alongside related measures to determine whether margin pressure comes from underused staff or excessive non-labor overhead (Sikich on professional services KPIs).

Start with the few that explain the business

Here are the metrics that tend to matter most in owner conversations.

| KPI | Formula | What It Measures |

|---|---|---|

| Utilization rate | Billable hours / Total available hours | How much of paid team capacity is being turned into client work |

| Project margin | Project revenue minus direct project costs | Whether an engagement is financially worth doing |

| Revenue per billable team member | Total revenue / Number of billable team members | How effectively your revenue model converts talent into output |

| Overhead per billable employee | Total non-labor overhead / Number of billable employees | Whether support costs are too heavy for the delivery team |

| Accounts receivable aging | Open invoices grouped by how long they remain unpaid | How much collections timing may strain cash flow |

What these KPIs actually tell you

Utilization rate is the headline metric, but it's easy to misuse. Low utilization may mean weak demand, poor scheduling, overstaffing, or too much non-billable admin. High utilization may look healthy while signaling burnout or delivery bottlenecks.

Project margin tells you whether the work itself is sound. If margins are weak, the problem may be pricing, scope control, staffing mix, or delivery inefficiency.

Revenue per billable team member helps owners judge scaling quality. If headcount rises but this number stalls, the firm may be adding labor faster than it is adding effective demand.

Use KPI trends, not isolated snapshots

One month rarely tells the full story. Owners should review these metrics in sequence and in combination.

A useful management rhythm looks like this:

- Weekly review for time capture, billing readiness, and collections follow-up

- Monthly review for utilization, project margin, and overhead pressure

- Quarterly review for hiring plans, pricing changes, and service line focus

If you want cleaner commercial visibility around demand and client activity, tools built for sales reports for service businesses can complement your accounting data. And if you're refining how you read margins, these notes on what are profitability ratios are a helpful companion to your KPI review process.

A Sample Workflow from Quote to Cash

A strong professional services accounting process should feel orderly from the first proposal through final reporting. Not flashy. Just clear, connected, and hard to break.

Step one through step three

A client requests support for a defined project. The firm prepares a quote in QuickBooks or a connected proposal system, using a pricing model that matches the expected delivery. If the work will be billed in phases, the estimate should already reflect milestones or retainer logic.

Once approved, the team sets up the engagement as a trackable project. Time entries, contractor bills, software costs, and reimbursable expenses are coded to that project from day one. That's what makes later reporting trustworthy.

During delivery, project managers and finance need shared visibility. The delivery team watches progress and scope. Finance watches time capture, cost accumulation, billing triggers, and whether the work being performed still matches the original agreement.

Step four through step six

When a milestone is reached or the billing period closes, the firm issues the invoice based on contract terms rather than guesswork. If your process still involves copying values manually across tools, resources that show how to eliminate manual data entry for invoices can help tighten the handoff between quoting and billing.

Collections follow next. That includes payment reminders, client communication, and cash application once payment arrives. This stage is where many owners discover that slow cash isn't always a sales problem. Sometimes it's an invoicing delay, approval bottleneck, or inconsistent follow-up process.

After payment, the project shouldn't disappear into the archive. Finance should close the loop by comparing estimate to actuals, reviewing profitability, and identifying where time leaked beyond scope. A practical reference for tightening that back-office movement is the invoice to pay process, especially if your team wants fewer handoff errors.

The workflow matters because every weak handoff between quote, delivery, invoicing, and reporting creates noise in the numbers.

What a clean workflow gives you

When quote-to-cash is well designed, owners gain three things:

- Less administrative friction because project, billing, and accounting data stay aligned

- Better cash visibility because invoice timing and collections are easier to monitor

- Stronger decision support because actual project economics are visible after the work ends

That's the point of the whole system. Not perfect bookkeeping for its own sake, but cleaner decisions about pricing, staffing, and growth.

When to Partner with an Accounting Specialist

Some firms can manage with a basic setup for a while. Then growth changes the math.

A few more employees. More overlapping projects. A mix of retainers and one-off engagements. Contractors in the workflow. Payroll complexity. Books that take too long to close. Reporting that sparks debate instead of confidence.

That's usually the point where DIY accounting stops being frugal and starts becoming expensive.

The clearest signs you've outgrown a basic setup

A specialist becomes useful when your team is facing problems like these:

- You don't trust the numbers enough to make hiring or pricing decisions

- Month-end closes drag on because reconciliations and project adjustments are manual

- Revenue timing is unclear on retainers, milestone work, or mixed-scope engagements

- Payroll and staffing decisions feel disconnected from project demand

- Cash keeps surprising you even when revenue appears solid

These aren't just bookkeeping issues. They affect how confidently you can run the business.

Thomson Reuters highlights a major need in advisory-led, people-heavy service models: owners want practical frameworks for turning accounting data into hiring and capacity decisions, especially around capacity planning and cash preservation during growth (Thomson Reuters on advisory obstacles and owner needs).

What a specialist should actually help you do

A good accounting partner for a service business should help you:

- Clean up the financial foundation with reconciled books, a useful chart of accounts, and consistent project coding

- Build reporting for decisions such as utilization, receivables, project margins, and staffing needs

- Align systems so QuickBooks, payroll, AP, and client billing don't contradict each other

- Support growth choices with better visibility into when to hire, when to delay, and where margins are leaking

A short explainer can help if you want a visual sense of how firms approach these decisions in practice.

Outsourcing isn't giving up control

Owners sometimes resist outside help because they think it means handing off visibility. In a healthy setup, the opposite happens.

You gain faster closes, clearer dashboards, better payroll coordination, and more confidence in the operational meaning behind the financials. That makes it easier to decide whether a problem is pricing, staffing, utilization, collections, or scope management.

Professional services accounting's value isn't that it keeps you compliant. It's that it turns finance into a management tool.

If your service business needs cleaner books, sharper reporting, and accounting that supports hiring, payroll, and profitability decisions, Steingard Financial works with service businesses across the United States to build and maintain that financial foundation.