You're good at your work. Your clients trust you. The business is busy.

Then Friday afternoon hits, and you're digging through receipts, wondering whether that software charge belongs in office expense, contractor cost, or something else entirely. A customer still hasn't paid. Payroll is due. Your bank balance looks decent, but you still don't know whether the month was profitable. You tell yourself you'll clean everything up later, usually at night, usually tired, usually while trying to remember what happened three weeks ago.

That's where many service business owners get stuck. They know how to deliver great work, manage clients, and solve problems. They don't always have a clean financial system that turns daily activity into useful decisions.

Professional accounting support changes that. It doesn't just help you file taxes or save a few admin hours. It creates the financial layer your business needs to operate with confidence. It gives you timely books, clear reports, and reliable cash flow visibility. Once that foundation is in place, higher-level guidance becomes possible. A fractional CFO can only plan from accurate numbers. A lender can only evaluate clean statements. You can only make smart hiring or pricing decisions if the underlying data is trustworthy.

That matters because small businesses make up 99.9% of all companies in the United States, and without professional accounting partners, 65% fail, while businesses with dedicated accounting support show stronger survival and financial health, according to Escalon's roundup of small business accounting statistics.

Introduction From Financial Fog to Strategic Clarity

A lot of owners think accounting support starts when tax season gets painful. In practice, it usually starts earlier, with smaller signs.

You send invoices late because you're busy serving clients. You pay bills from memory instead of a schedule. You glance at your checking account to decide whether you can hire, spend, or wait. That feels manageable for a while. Then one surprise expense or one slow-paying client throws everything off.

The problem usually isn't effort. It's structure.

What financial fog looks like

Financial fog shows up in ordinary ways:

- Unclear profitability: You know revenue came in, but you can't tell which services made money.

- Cash confusion: You see cash in the bank, but some of it already belongs to payroll, taxes, or vendors.

- Messy records: Receipts live in email, paper folders, and your memory.

- Delayed decisions: You wait to hire, invest, or market because you don't trust the numbers enough.

A good accounting partner clears that fog by building a repeatable system. Transactions get categorized correctly. Accounts get reconciled. Payroll gets processed on time. Reports come out consistently. Instead of guessing, you review.

Clean books don't make your business grow by themselves. They make good decisions possible.

Why this matters beyond bookkeeping

Many owners think of accounting support as back-office maintenance. That's incomplete. Bookkeeping is the floor, not the ceiling.

Once your financial data is accurate and current, you can start asking better questions. Should you raise prices? Can you afford another employee? Are collections slowing down? Is one service line carrying the rest of the business? Those are strategy questions, but they depend on accounting discipline.

That's the shift. Small business accounting support starts with order. It ends with decision-making.

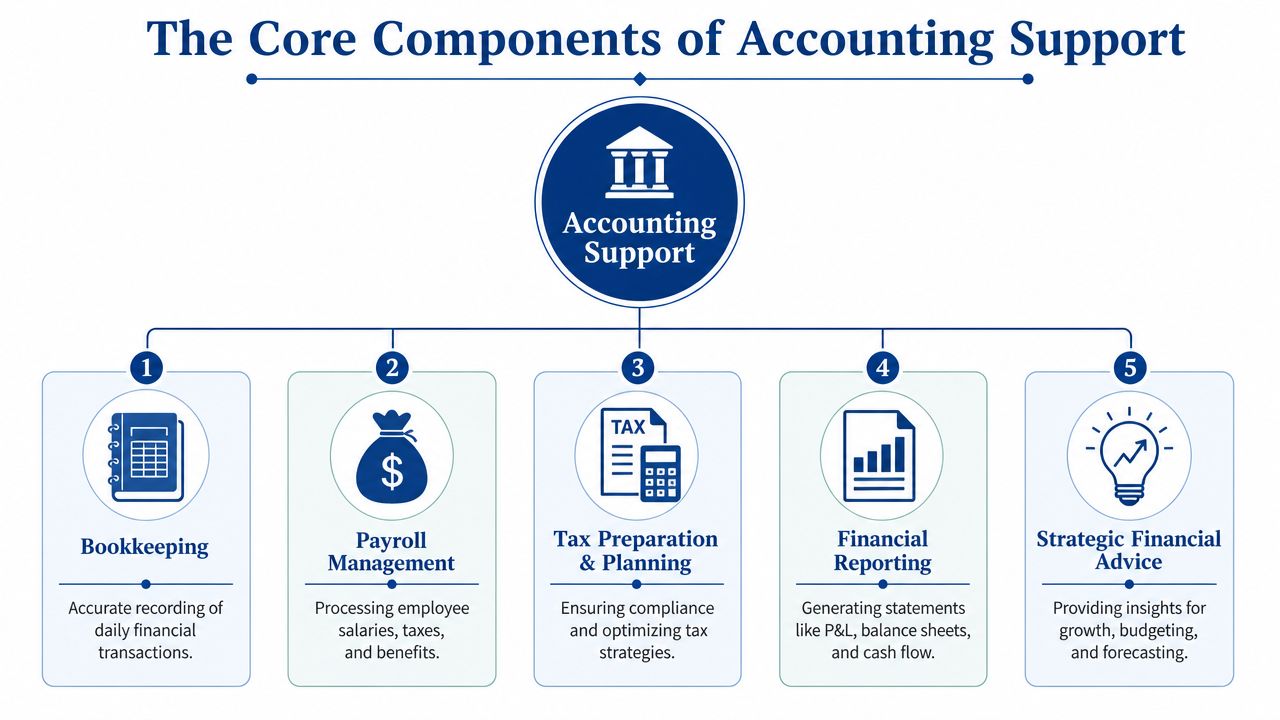

The Core Components of Accounting Support

If your business were a vehicle, accounting support would be both the engine room and the dashboard. One part keeps the machine running. The other tells you whether you're headed in the right direction.

Most owners see only the dashboard at first. They want reports. They want answers. But the reports are only as good as the work underneath them.

Bookkeeping is the base layer

Every transaction gets recorded and assigned to the right account. That sounds simple until you've tried to untangle owner draws, software subscriptions, merchant fees, loan payments, reimbursable expenses, and payroll entries in one general ledger.

Effective support uses double-entry bookkeeping, where every transaction is mirrored as a debit and credit. That structure keeps the ledger balanced and improves cash flow visibility. It also supports better advisory work later. Forbes notes that 62% of small business owners want talent management insights from their accounting providers, which shows how disciplined bookkeeping often becomes the base for broader business guidance in Forbes Advisor's bookkeeping overview.

Here's where owners often get confused: categorizing a transaction isn't clerical busywork. It determines what your reports say. If advertising expense lands in the wrong place, your service line profitability can look better or worse than it really is.

The practical pieces most businesses need

A complete support function usually includes several moving parts:

- Accounts receivable: Creating invoices, tracking due dates, and following up on unpaid balances.

- Accounts payable: Recording vendor bills, scheduling payments, and avoiding both late fees and duplicate payments.

- Payroll administration: Processing wages, tax withholdings, and related filings through tools like Gusto or QuickBooks Payroll.

- Bank and credit card reconciliation: Matching your books to actual statements so errors and missing items get caught.

- Chart of accounts design: Building the list of categories your business uses to sort financial activity.

Think of the chart of accounts as your business's filing cabinet. If the drawers are labeled badly, everything that gets filed later becomes harder to find and harder to trust.

For owners who want a straightforward picture of what ongoing bookkeeping usually includes, this overview of bookkeeping services for small businesses is a useful reference point.

Practical rule: If your reports don't match how you actually run the business, the chart of accounts probably needs work.

Reporting turns records into decisions

At month-end and year-end, accounting support should produce reliable financial statements, not just raw exports from software. At minimum, that means a profit and loss statement, a balance sheet, and a cash flow view that someone can explain in plain English.

This is also where strategic support starts to appear. Once the numbers are clean, outside advisors can use them. If you're evaluating funding options, lender expectations matter, and GoSBA Loans' broker insights can help owners understand how financing conversations often depend on organized financial records and clear documentation.

That's why small business accounting support isn't just “keeping up the books.” It's building the information system that strategy depends on.

Five Signs Your Business Needs an Accounting Partner

Some businesses don't need a push. They need a diagnosis.

If one of the situations below feels familiar, you're probably past the point where DIY finance is harmless. You don't need more discipline. You need a better system and someone responsible for maintaining it.

You're behind on invoicing and bills

When invoicing slips, cash slips with it. When vendor bills pile up, you lose control of timing.

The fix is simple in concept, but hard to do consistently without support. An accounting partner creates a cadence. Invoices go out on time. Receivables get tracked. Bills are recorded and scheduled. You stop relying on memory.

You don't have a current view of cash flow

Many owners check the bank account and assume that number equals available cash. It doesn't.

Some of that cash is already spoken for. Payroll may be coming. Sales tax may be due. Credit card autopay may hit next week. An accounting partner helps separate “cash in the account” from “cash available to use.”

Tax season keeps bringing surprises

If every tax deadline feels like a fire drill, your books probably aren't giving your tax preparer what they need in a clean format. That usually means rushed clean-up, avoidable confusion, and stress you could have prevented months earlier.

The best tax season is boring. The work was already done during the year.

Your books are messy from prior DIY work or a weak provider

This happens often. Categories are inconsistent. Reconciliations were skipped. Loans were posted incorrectly. Payroll entries don't tie out. The software technically has data, but the data can't support decisions.

Cleanup is one reason owners seek outside help. Once the historical mess is fixed, reporting becomes usable again.

You spend too much time on finance and not enough on clients

This is the sign owners notice first. Every hour spent sorting receipts, correcting transactions, or chasing payroll issues is an hour not spent selling, delivering work, or managing the team.

If you want a good example of how better reporting support changes operations, this write-up on Helpwithmetrics agentic BI service is worth reviewing. It highlights a common reality: when reporting becomes dependable, leadership stops wasting time arguing about the numbers and starts using them.

A quick self-check

| Sign | What it usually means |

|---|---|

| Invoices go out late | Revenue collection is too manual |

| Reports feel unreliable | Categorization or reconciliation issues exist |

| Tax prep is chaotic | Books aren't being maintained throughout the year |

| You avoid looking at the numbers | The reporting system feels confusing or unhelpful |

| You're doing finance at night | The business has outgrown owner-managed accounting |

A partner doesn't just remove tasks. They restore order to the financial side of the business.

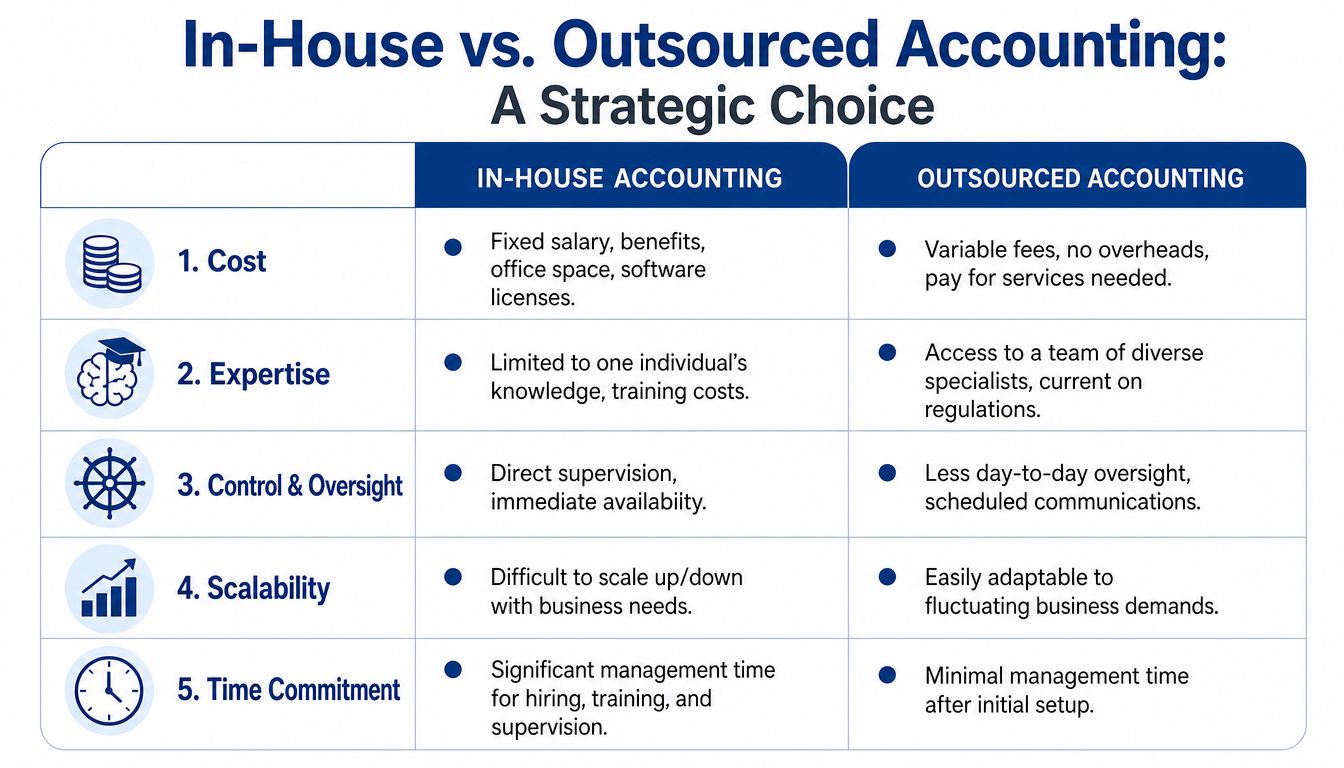

Comparing Accounting Support Models In House vs Outsourced

Once you know you need help, the next question is how to structure it. Most service businesses end up choosing between three models: in-house support, outsourced accounting, or a fractional setup that combines bookkeeping with higher-level finance guidance.

The right answer depends less on ideology and more on stage, complexity, and management capacity.

In-house support

An in-house bookkeeper or accountant offers proximity. They're available during the day, they know your team, and you can supervise the work directly.

That can be useful, especially if your operation is large enough to keep someone fully occupied. But in-house support also means hiring, training, oversight, software management, and the risk of relying too heavily on one person's knowledge.

Outsourced support

Outsourced accounting gives you a service model instead of a single employee. That often means access to multiple skill sets, better process consistency, and easier scaling as your business changes.

For many small businesses, this is also the more practical cost structure. Slateridge Finance notes that 31% of small businesses spend between $1,000 and $5,000 annually for basic accounting services, and that monthly packages for ongoing support typically range from $500 to $2,500, as outlined in this small business accounting cost guide.

If you want to see what that model looks like in practice, this page on outsourced accounting for small business shows the general scope owners often look for: recurring bookkeeping, payroll support, reconciliations, and reporting.

Here's a short visual explanation of the tradeoff many owners consider:

Fractional support

A fractional model sits above day-to-day bookkeeping. It usually makes sense after the accounting foundation is already stable.

A fractional CFO can help with budgeting, hiring plans, scenario analysis, lender conversations, and performance review. But that strategic work only works if the bookkeeping layer is timely and accurate. Otherwise, the advice is built on unstable numbers.

Side-by-side decision criteria

| Model | Best fit | Main strength | Main limitation |

|---|---|---|---|

| In-house | Businesses with enough volume for a full-time role | Direct supervision | More overhead and single-person dependency |

| Outsourced | Small and growing businesses that need flexibility | Scalable access to process and expertise | Less day-to-day physical presence |

| Fractional | Businesses ready for planning and financial leadership | Strategic guidance | Depends on strong books underneath |

Risk, systems, and oversight

One overlooked point is professional risk management. If you work with an outside firm, it's reasonable to ask how they handle professional liability and internal controls. Business owners who want context on that side of the profession can review Select Insurance for accounting firms to better understand why errors and omissions coverage matters in accounting relationships.

The best model is the one that gives you reliable execution today and enough financial depth for tomorrow. For many service businesses, outsourced support handles the operational layer, and fractional leadership gets added once the reporting is solid.

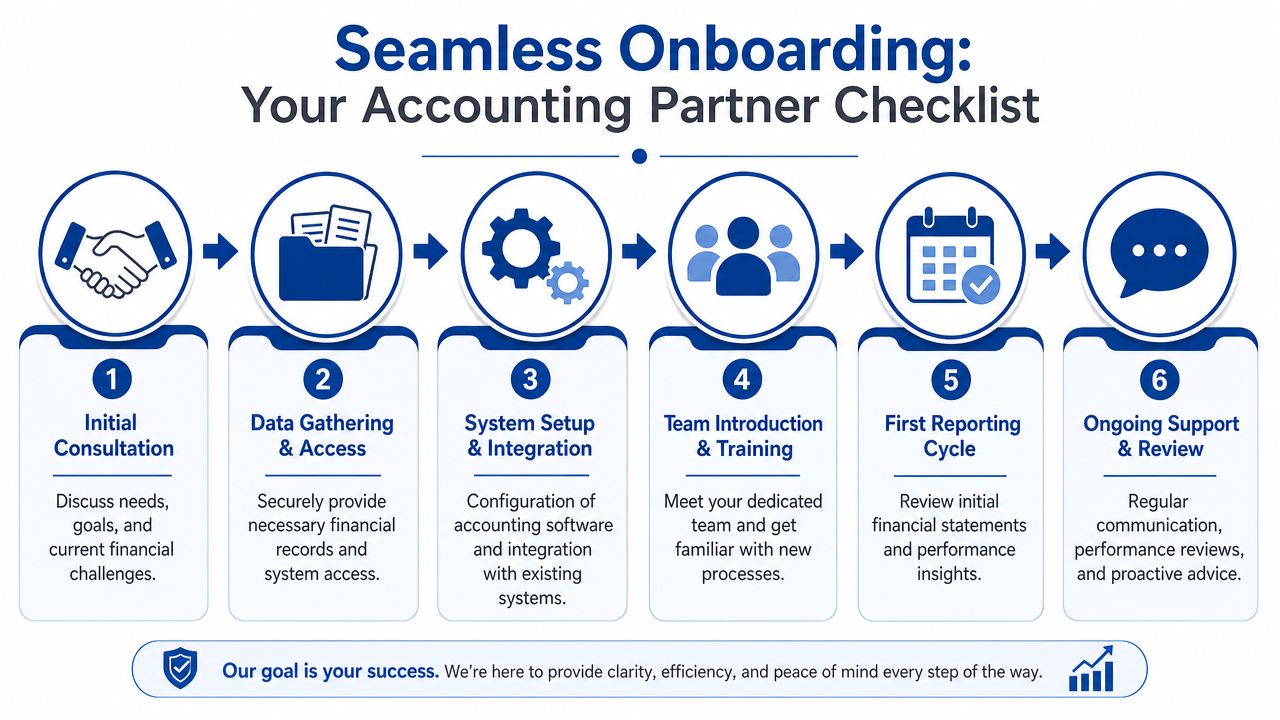

Your Onboarding Checklist for a Seamless Transition

Owners often delay getting help because they expect onboarding to be painful. It doesn't need to be. A good transition is structured, secure, and surprisingly practical.

The key is to treat onboarding as building your financial back office, not just handing someone your logins.

What to gather before the first working session

Start with the records that let your new partner understand the current state of the business.

- Bank and credit card statements: Recent statements help identify missing transactions and reconciliation gaps.

- Prior tax returns: These give context for entity structure, payroll setup, and historical reporting.

- Loan documents: Notes, balances, and payment terms matter because loan entries are often posted incorrectly.

- Payroll access: If you use Gusto or QuickBooks Payroll, your provider needs visibility into wage and tax setup.

- Old financial reports: Even imperfect reports can reveal how the prior system was organized.

If anything is missing, don't panic. Incomplete records are common. The point is to start with what exists.

Clarify the systems and the workflow

Accounting support works best when the tech stack is simple and connected. For many service businesses, that means QuickBooks Online paired with a payroll platform like Gusto.

At this stage, a good partner should help answer practical questions such as:

- Which bank and card feeds should connect directly?

- Who approves bills before payment?

- How should owner draws be handled?

- Which reports need to be reviewed weekly, and which belong in the monthly close?

- Who on your team needs access, and at what level?

Owner note: Don't outsource decisions you haven't made. Even a strong accounting team needs your input on approval rules, service categories, and management priorities.

Build the chart of accounts for how you actually operate

A generic chart of accounts rarely helps a service business owner make decisions. You need categories that match reality.

If you run an agency, contractor labor, software subscriptions, ad spend, and client reimbursements may need separate treatment. If you run a consulting firm, revenue may need to be split by service line. If you manage payroll for a growing team, compensation and benefits categories should support review, not just compliance.

This is also the right moment to discuss cleanup. Historical books may need corrections before reporting becomes meaningful. That's normal.

Set communication rules early

The smoothest accounting relationships usually define communication before problems arise.

A simple setup often includes:

- A weekly touchpoint: For urgent questions, cash issues, and approvals

- A monthly review meeting: For financial statements and trend discussion

- A document process: One shared system for receipts, notices, and requests

- Clear deadlines: When reports will be ready and when owner input is required

When these expectations are clear, the business stops lurching from deadline to deadline.

Using Financial Reports to Drive Growth

Good reports don't just describe the past. They shape the next move.

That's the key payoff of small business accounting support. Once the books are clean and current, reporting becomes a tool for action. You stop reading statements like paperwork and start reading them like operating signals.

The three reports owners should actually use

Most service businesses rely on three core statements.

The profit and loss statement shows whether your service delivery model is producing profit. The balance sheet shows what the business owns, owes, and retains. The cash flow view helps explain why profit and cash aren't always the same thing.

Owners usually understand the profit and loss statement first. The balance sheet is where confusion starts. That's because it tracks timing and obligations, not just activity. Loan balances, unpaid bills, retained earnings, and owner distributions all live there. If that report is wrong, strategy gets distorted fast.

For a practical framework on keeping reports useful and consistent, these financial reporting best practices are a solid reference.

What to watch in a service business

A report only becomes strategic when you connect it to operating questions.

Here are examples of useful review points:

- Gross profit margin: Are your direct labor and delivery costs in line with how you price work?

- Days sales outstanding: How long does it take customers to pay after invoicing?

- Customer acquisition cost: Are you spending sensibly to win new business?

- Payroll as a management issue: Is hiring keeping pace with revenue, or getting ahead of it?

- Cash runway: If collections slow, how much room do you have?

Different businesses will track different measures. The point is to choose a small set that links directly to action.

Reports should answer decisions, not just display totals.

Reporting cadence matters as much as report quality

A clean monthly close is important. But many owners also need a lighter, faster cash view during the month.

A practical rhythm often looks like this:

| Cadence | What to review | Why it matters |

|---|---|---|

| Weekly | Cash position, major receivables, upcoming payables | Prevents short-term surprises |

| Monthly | P&L, balance sheet, trend changes, owner questions | Supports management decisions |

| Periodically for planning | Forecasts, scenarios, hiring timing, funding readiness | Supports strategic growth |

The main idea is consistency. Reports help only when they arrive often enough to influence choices.

Why strategy depends on accounting depth

The conversation progresses beyond compliance. Advanced accounting support can pull historical transaction data into forecasting and dashboard tools that help owners see what's coming, not just what already happened.

According to Datamatics CPA's overview of small business accounting needs, providers using cloud platforms like QuickBooks can reduce data entry errors by 35% and create unified financial views, while AI-driven analytics can turn historical data into real-time cash flow forecasting that supports planning and lender readiness.

That matters for strategic growth. A fractional CFO can build hiring scenarios, pricing models, and cash forecasts. But none of that works if revenue is miscoded, reconciliations are late, or liabilities are missing. Strategic advice is only as reliable as the accounting underneath it.

In other words, bookkeeping records the business. Reporting explains the business. Strategic finance helps you change the business.

Frequently Asked Questions

| Question | Short answer | What it means in practice |

|---|---|---|

| Do I need accounting support if I'm still small? | Probably yes, if transactions, payroll, or invoicing are already inconsistent. | Small doesn't mean simple. Even a lean service business needs reliable categorization, reconciliations, and reporting. |

| What's the difference between a bookkeeper and a fractional CFO? | A bookkeeper maintains the records. A fractional CFO uses those records for planning and decision support. | If the books are messy, start there first. Strategic finance comes after the data is dependable. |

| Can accounting support help if my books are already behind? | Yes. Cleanup is a common starting point. | Historical corrections often come before ongoing monthly work. Once the old periods are repaired, current reporting becomes useful again. |

| What if my team isn't comfortable with accounting terms? | A good provider should explain things in plain language. | Owners shouldn't need to speak in debits and credits to understand cash flow, payroll impact, or profitability. |

| I use QuickBooks and Gusto already. Is that enough? | The software helps, but software doesn't create process. | Tools are only effective when someone sets up categories correctly, reviews exceptions, reconciles accounts, and explains the output. |

| How do fractional CFOs benefit from a bookkeeping partner? | They get cleaner inputs for forecasting, budgeting, and board or lender reporting. | When the bookkeeping layer is stable, the CFO can spend time on analysis instead of cleanup. |

| What if I'm a non-English-speaking owner or not comfortable with digital onboarding? | You may need a provider that offers more human guidance and less jargon. | Some owners need onboarding and explanations that are bilingual, non-technical, and accessible without assuming advanced software comfort. |

| Are there options for very small or underserved businesses that can't afford full support yet? | Sometimes, but access is uneven. | Some community-based programs offer coaching or software support, but many owners still struggle to find no-strings accounting help without credit-based requirements. |

If your business needs cleaner books, better payroll support, or reporting that a founder or fractional CFO can use, Steingard Financial is one option to consider. The firm works with service businesses that need transaction categorization, reconciliations, payroll support, month-end reporting, and a more dependable financial back office built around tools like QuickBooks and Gusto.