You open the credit card statement at month end and already know what's coming. A software subscription. A client lunch. A family dinner. A recurring Zoom charge. A pharmacy purchase. An airline ticket that might be for business, except you booked personal travel that same week. Now your QuickBooks feed is full of transactions that need judgment calls, receipt chasing, and owner follow-up.

That's the problem in the business vs personal credit cards decision. It isn't just rewards points or annual fees. It's whether your books stay clean enough to trust, whether your tax preparer gets a defensible set of records, and whether your business operates like a company instead of an extension of your wallet.

A lot of owners fall into this pattern because it's convenient. In a 2022 survey summarized by Hello Alice's small business credit stats, 73% of small business owners reported having a personal credit card, and 61% said they use that personal card for business-related purchases. Those numbers match what bookkeeping teams see every week. Mixed spending creates avoidable cleanup work, and cleanup work gets expensive.

Why the Right Card Matters for Your Service Business

Service businesses usually don't have warehouses or heavy equipment. That makes owners think card choice is a minor issue. It isn't. If you run an agency, law firm, design studio, consulting practice, therapy group, home services company, or professional office, your business lives on recurring transactions. Software, travel, subcontractors, meals, supplies, training, dues, advertising, and employee reimbursements all flow through your cards.

When those charges hit a personal card, the bookkeeping gets harder immediately. Your bookkeeper has to separate owner draws from legitimate business expenses. Your reconciliations slow down. Your QuickBooks rules become less reliable because the same statement includes both deductible and nondeductible spending. If you run payroll in Gusto, the mess spreads there too. Reimbursements become harder to verify, and owner-paid expenses often sit in suspense accounts until someone explains them.

What this looks like in practice

The issue rarely shows up as one dramatic mistake. It shows up as friction.

- Month-end drags on: The bank feed imports quickly, but review takes longer because someone has to identify personal charges.

- Receipts go missing: Business purchases made on a personal card often don't get documented the same way team purchases do.

- Reporting gets less useful: Profit and loss statements lose credibility when expenses are posted late or reclassed after the fact.

- Tax prep becomes forensic work: Instead of handing over organized business records, you hand over a story that needs reconstruction.

Practical rule: If a transaction requires a conversation to determine whether it belongs to the business, the workflow is already broken.

Using a dedicated business card won't solve every accounting issue. But it fixes one foundational problem. It creates a cleaner source record. That matters because good reporting starts with how transactions enter the system, not with heroic cleanup later.

For a service business owner, the right card is part of operating discipline. It supports better categorization, faster closes, and more reliable financial statements. That's what lets you make decisions from your numbers instead of arguing with them.

Understanding the Fundamental Design Differences

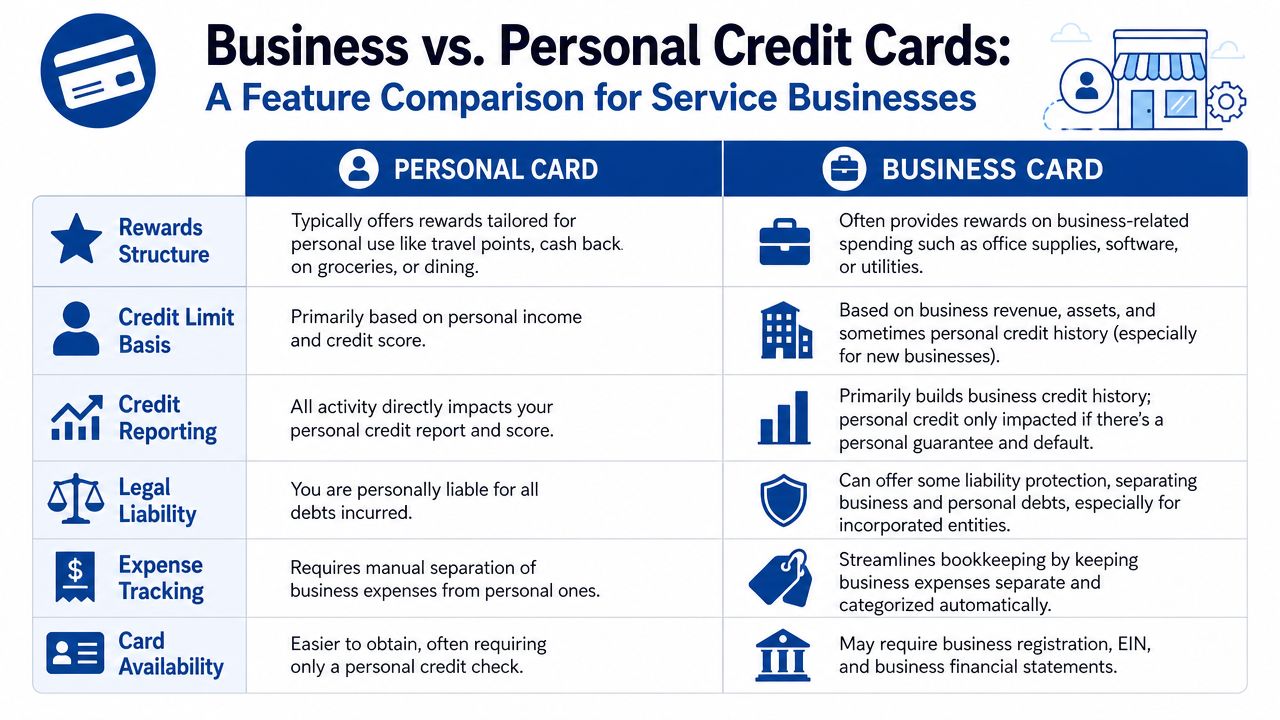

A personal credit card and a business credit card may look similar in your wallet, but they're built for different jobs.

A personal card is designed around individual spending. It assumes the user is buying household goods, travel, gas, dining, and daily consumer purchases. The account is tied to your personal financial life, and the card issuer evaluates you as a consumer.

A business card is designed as an operating tool. It's meant to support company purchases, create cleaner expense records, and give the business its own financial identity over time. That's the key distinction. One card is built for a person. The other is built for an entity, even when the owner still signs a personal guarantee.

The design difference affects daily operations

This isn't just branding. It changes how the card works in your back office.

Business cards commonly include features that fit a company workflow, such as employee cards, expense reporting, and accounting integrations. Personal cards generally center on consumer use and household spending patterns. If you want a broader primer on that split, this overview of understanding business and personal credit is a useful companion read.

For service businesses, that design difference matters most in four places:

Expense ownership

A business card signals that the charge belongs to the business first. That reduces ambiguity when transactions hit QuickBooks.Delegation

If an office manager, project lead, or technician needs purchasing authority, a business card structure handles that far better than sharing one owner card or asking for reimbursements.Workflow consistency

The best bookkeeping systems rely on repeatable rules. Business cards fit repeatable rules. Personal cards create exceptions.

Why owners still use personal cards

Usually, it's speed. The owner already has the card, already knows the login, and doesn't want another application process. That can feel harmless early on, especially for a solo operator.

But convenience at the point of purchase often creates cost later. Someone still has to classify the expense, attach support, reconcile the statement, and explain mixed charges. In a service business, those tasks don't disappear. They just move downstream to your books, your tax return, and your reporting.

Comparing Card Features Rewards and Costs

A plumbing owner pays for Google Ads, QuickBooks, job materials from a supply house, and two Gusto payroll tax debits in the same month. If those charges run through the wrong card setup, the problem is not just weaker rewards. The problem shows up later in categorization, reconciliation, and owner draw cleanup.

| Feature | Personal Credit Card | Business Credit Card |

|---|---|---|

| Rewards structure | Usually geared toward household categories like dining, groceries, gas, or general travel | Often geared toward business spending categories such as software, utilities, office purchases, or travel |

| Credit limit basis | Primarily tied to personal income and personal credit profile | Often underwritten using both the owner's profile and the business operating profile |

| Expense tracking | Business transactions must be separated manually from personal spending | Better fit for dedicated business-only feeds and cleaner bookkeeping |

| Employee use | Not designed for team purchasing controls | Commonly supports employee cards and business spending oversight |

| Credit reporting path | Tied to consumer credit reporting | Typically tied to business credit reporting, though personal guarantee risk may still apply |

| Primary operational use | Personal spending with occasional business crossover | Company spending, entity-level tracking, and finance workflow support |

Rewards should match your chart of accounts

For a service business, rewards only matter if they fit actual spend. Many owners use cards for software, fuel, small tools, travel, online advertising, education, and client meals. Household bonus categories rarely line up cleanly with that mix.

Cash back is often easier to manage than points if clean accounting is the goal. It posts clearly, creates fewer valuation questions, and is easier to explain when reviewing owner activity or month-end reports. Travel rewards can still make sense, but only if the business spends enough in those categories to justify the annual fee and the extra tracking.

The practical test is simple. Review the last three months of expenses in QuickBooks. If the biggest card categories are software subscriptions, digital ads, contractor payments, and travel, a business card usually fits the ledger better than a consumer rewards card.

Credit limits affect operations, not just purchasing power

Capacity matters in service businesses with uneven cash flow. A firm may front ad spend, book flights for a crew, pay annual insurance, or cover project costs before the client pays the invoice. A card that tops out too early can force awkward owner transfers, delayed purchases, or multiple partial payments that complicate the books.

Personal cards are often tied more closely to the owner's household income and consumer profile. Business cards may consider business revenue and operating history alongside the owner's guarantee. In practice, that can produce a limit that better matches the company's real cash needs.

That matters in bookkeeping. If one card can reliably carry normal monthly operating spend, the QuickBooks feed stays cleaner and reconciliation stays predictable.

Fees are easier to judge when you price the admin time

Owners often focus on annual fees and miss the actual cost. A no-fee personal card can create monthly sorting problems if business and personal charges hit the same statement. Then someone has to identify owner draws, code reimbursable items, request missing receipts, and explain exceptions at tax time.

I usually tell clients to compare the fee to the labor it saves. If a business card gives employee cards, spending limits, better merchant detail, and cleaner exports into QuickBooks, the fee may be cheaper than an extra hour or two of cleanup every month. For teams running payroll through Gusto, that cleaner separation also makes it easier to keep wage expenses, reimbursements, and owner spending from getting mixed together.

Some businesses need tighter controls than a standard credit line provides. For limited-use purchasing, vendor-specific funding, or team spending caps, it can help to compare a card program with a prepaid debit card for business.

Terms and reporting details deserve a close read

Read the agreement before choosing based on rewards alone. Pay attention to who is liable for employee cards, whether the issuer offers downloadable transaction data that works well with your bookkeeping process, and how disputes are handled. If your company operates in Washington, rules tied to fair credit reporting for WA businesses are also worth understanding before you rely on any credit product for day-to-day operations.

The best card produces decent rewards, enough capacity, and fewer bookkeeping exceptions. That combination usually beats the highest sign-up bonus.

How Each Card Type Impacts Your Credit Score

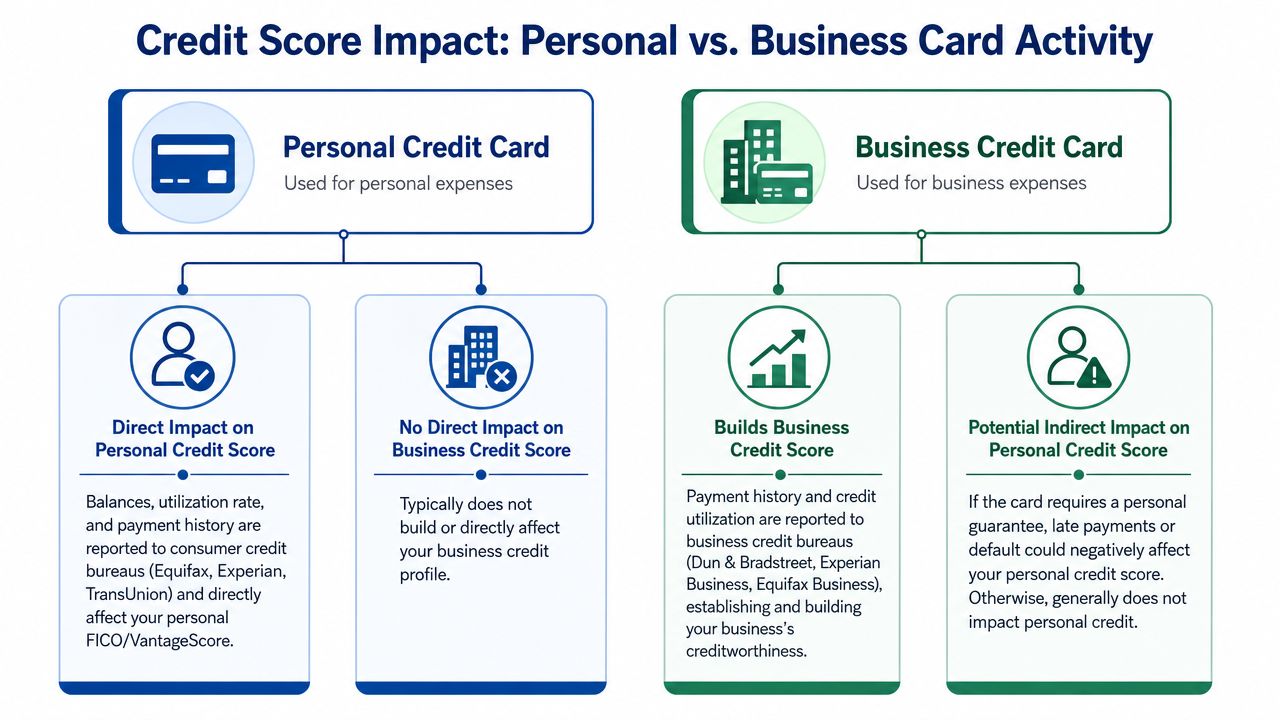

The credit side of the business vs personal credit cards decision is where many owners make assumptions that turn out to be wrong.

A personal card reports to the major consumer bureaus, which means balances and payment history affect your personal credit file. A business card typically reports to business credit bureaus such as Dun & Bradstreet, Experian Business, and Equifax Business, helping the company establish a separate business credit profile, as explained in Brex's comparison of business and personal credit cards.

Why this matters beyond the card itself

If you put business spending on a personal card, your company's operating expenses can shape your personal credit profile. Even if every charge is legitimate and every payment is on time, you're still routing business activity through your consumer file.

A business card changes that structure. The company begins building a record in its own name. Over time, that's useful for financing conversations, vendor relationships, and the broader effort to operate as a real business rather than as an owner-funded side account.

Business cards also often come with higher credit limits because businesses can face larger expenses. That's another reason reporting separation matters. You want business spending power tied to business operations where possible, not constantly leaning on your household credit profile.

The personal guarantee is the caveat

Owners sometimes hear “separate business credit” and assume that means no personal risk. That's not how most small-business cards work.

Many business cards still require a personal guarantee. That means the owner remains liable for the debt if the business can't pay. So the account may help establish business credit, but it doesn't automatically remove personal exposure.

That distinction matters. Separate reporting and separate liability are not the same thing.

- Separate reporting helps the company build its own credit identity.

- Personal guarantee means the owner may still be responsible if the account goes bad.

- Operational benefit remains strong because the card still supports cleaner entity-level tracking.

A compliance point owners shouldn't ignore

If you're dealing with credit file issues, adverse reporting, or disputes around what appears on a report, the legal framework matters too. For Washington businesses and owners, this explainer on fair credit reporting for WA businesses gives helpful context on how credit reporting rules can affect business-related situations.

A business card should be viewed as part of your credit architecture. Not just as a payment method.

The Critical Role in Bookkeeping and Tax Compliance

The card decision transitions from theoretical to practical.

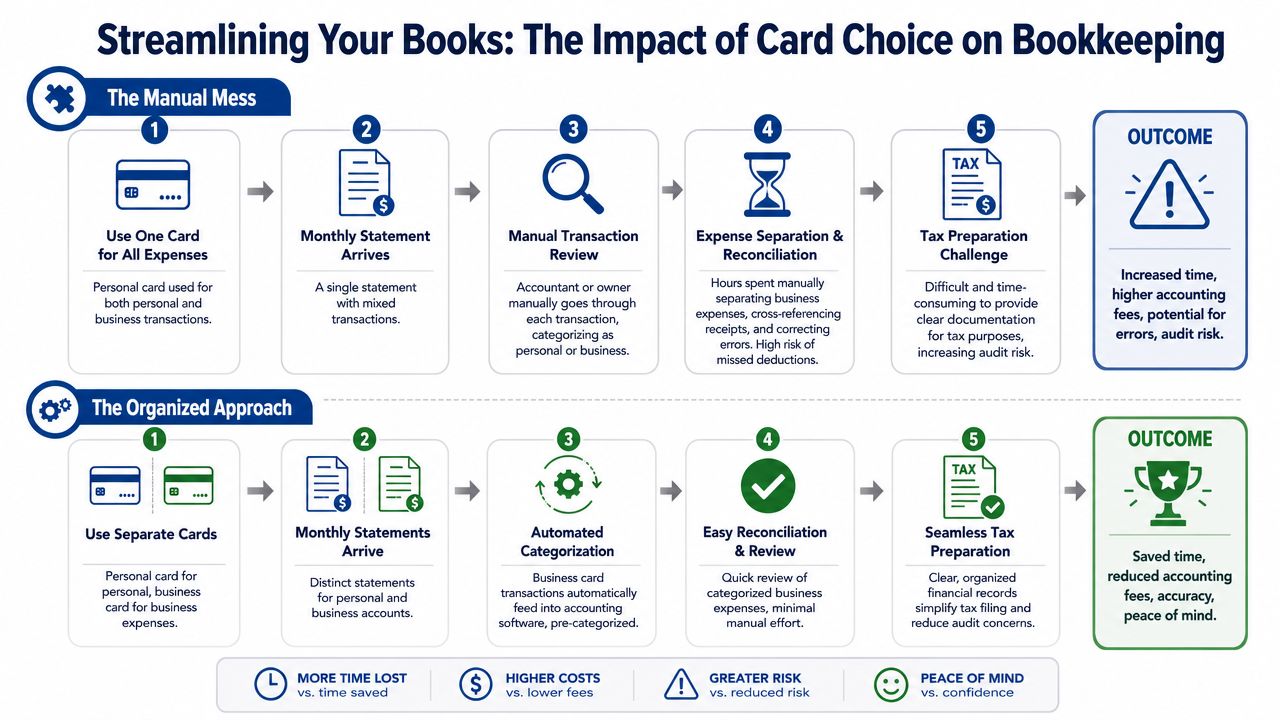

When a dedicated business card feeds into QuickBooks Online, the bookkeeping process becomes more structured. Rules work better. Expense categories are more consistent. Reconciliation gets faster because the account is supposed to contain business activity only. Review still matters, but review is very different from reconstruction.

What clean card feeds do for QuickBooks

QuickBooks works best when the source accounts are logically separate. If your business card is used only for business purchases, the bank feed can support reliable automation.

That means you can:

- Create smarter bank rules: Recurring software charges can route to software subscriptions. Merchant processors can route to fees. Travel vendors can land in the right travel category for review.

- Reconcile faster: The statement total should tie to business transactions, not a mixed list that needs owner interpretation.

- Review exceptions only: Your bookkeeper spends time on unusual items instead of every single charge.

This is one reason month-end close quality improves when owners stop using personal cards for company expenses. The accounting team can focus on judgment, not cleanup.

How this affects Gusto and payroll workflows

The card decision also shows up in payroll and reimbursement systems. If employees use personal funds and submit reimbursement through Gusto, you need support, approval, and accurate coding. That's manageable when it's occasional. It becomes messy when it's the default because no one has a business purchasing method.

Business cards let you move expenses closer to the business itself. Instead of reimbursing every recurring purchase, you can assign spending responsibility more cleanly. The expense lands in the right account from the start, and payroll doesn't become a backdoor expense clearing system.

Tax compliance gets easier when records start clean

Tax rules require clear support for business deductions. A dedicated business card doesn't prove every charge is deductible by itself, but it creates a far better audit trail.

The practical advantages are straightforward:

The account purpose is clear

A business-only card statement starts from the presumption that charges belong to the business ledger.Documentation is easier to maintain

Receipts can be collected against one stream of business purchases instead of scattered across owner accounts.Year-end adjustments drop

Fewer personal transactions need to be carved out of expense accounts.

If you're trying to tighten your documentation process, this guide for automating financial documents is useful for thinking through how statements and records can be made more workable in digital workflows.

Owners who still have mixed spending can improve things immediately by standardizing receipt capture and account review. A practical starting point is building a repeatable system for records retention. This checklist on how to organize business receipts pairs well with a business-card-first workflow.

What works: one business bank account, one business credit card feed, documented receipts, and monthly reconciliation in QuickBooks.

What doesn't: one owner card carrying software charges, airfare, household purchases, and “I'll sort it out later” notes.

Navigating Legal Liability and Asset Protection

A common fact pattern looks harmless at first. The LLC is formed, the client invoices run through the business, but the owner still puts software, travel, and emergency purchases on a personal card because it is faster. Six months later, QuickBooks is full of owner-paid expenses, reimbursements are inconsistent, and the line between company activity and personal spending is harder to defend than it should be.

That matters for more than neat records. If you operate through an LLC or corporation, the business should act like a separate business in its banking, card use, and accounting records. Regularly paying company expenses from a personal card weakens that separation. In a dispute, messy financial behavior gives the other side more room to argue that the entity was not treated as distinct.

Separation has to show up in the records

Owners usually hear this described as protecting the corporate veil. In practice, the issue is simpler. Do the books, statements, and workflows show a real boundary between the owner and the company?

A dedicated business card helps answer yes. The card feed goes into QuickBooks under the business, recurring charges post to the right accounts, and reimbursements can be limited to true exceptions instead of becoming part of the normal process. For service businesses, that operating discipline matters. If payroll runs through Gusto, vendor bills are paid from the business bank account, and card spending still sits on the owner's personal statement, the financial process is split across two systems. That creates avoidable noise in monthly reporting and year-end cleanup.

A personal guarantee and legal separation are different issues

Many business cards require the owner to personally guarantee the debt. Owners often hear that and assume there is no legal or practical upside to using a business card.

There is. A personal guarantee means the owner may still be responsible for the balance if the business does not pay. It does not erase the benefit of keeping business transactions inside business accounts and business accounting records. From a CPA's perspective, those are separate questions. One is who owes the card issuer. The other is whether the company has been run with clean financial boundaries.

The setup that holds up best is straightforward:

- Business bank account only for company activity

- Business credit card only for company purchases

- Owner draws or distributions recorded clearly

- Personal payments for business expenses treated as documented reimbursements or owner contributions

- Monthly reconciliation in QuickBooks so mixed charges do not sit unresolved

If the banking side is still informal, start there. Steingard Financial's guide to opening an LLC bank account properly is a practical next step.

A business card does not eliminate liability. It does reduce commingling, improve the audit trail, and make it easier to show that the company operates as its own entity. For a small service business, that is the primary protection.

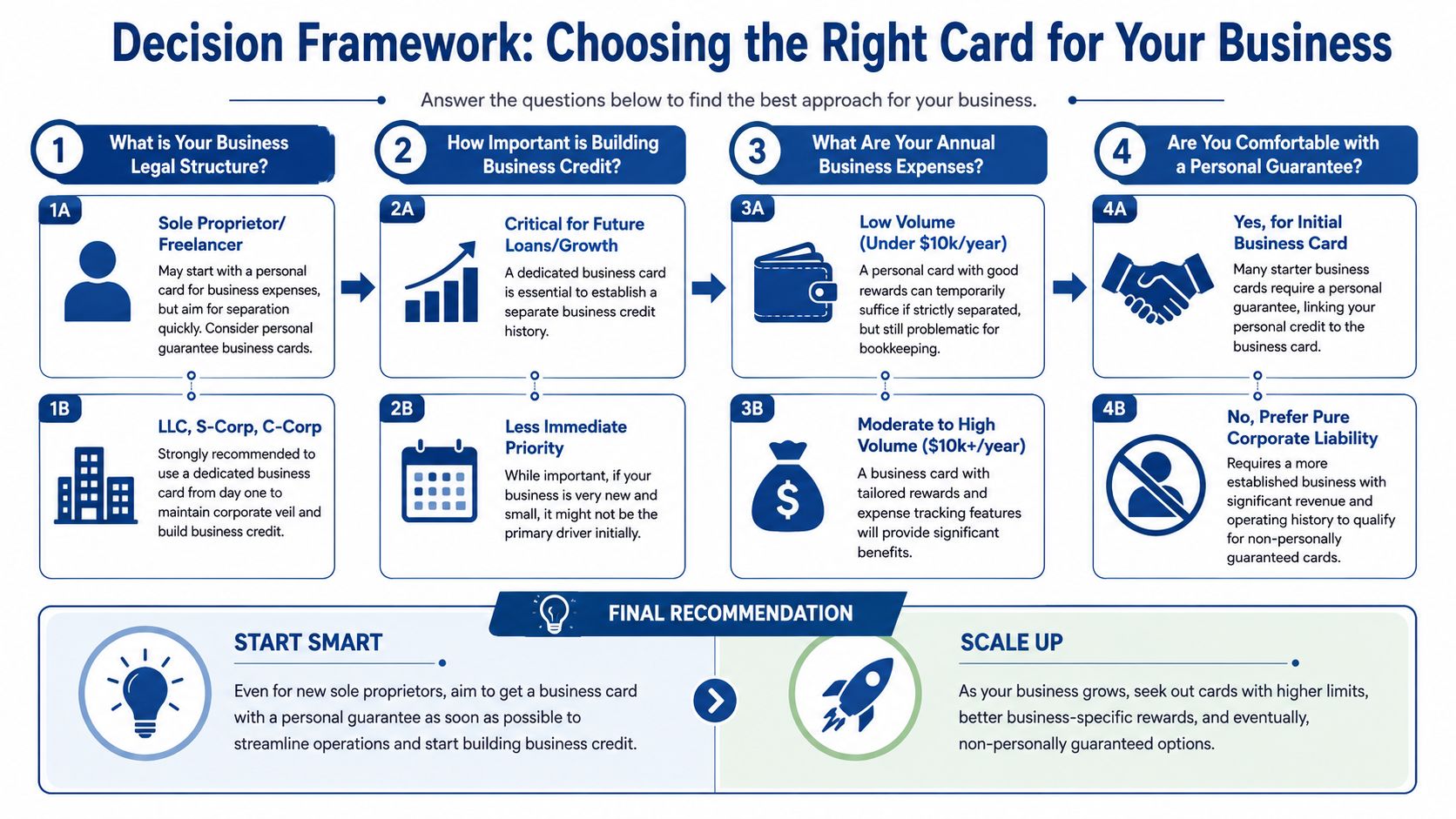

A Decision Framework for Your Business

The right answer depends on how your business operates today, not on what card gives the nicest perk.

If you're a brand-new sole proprietor with minimal activity, no employees, and very few business purchases, a personal card can function as a temporary bridge. But “temporary” needs to mean temporary. Once the business has recurring expenses, client travel, software subscriptions, contractors, or a formal entity structure, the case for a dedicated business card becomes strong very quickly.

Use this short test.

Choose a business card if these are true

- You have an LLC or corporation: Separation should start at the transaction level.

- You use QuickBooks and want clean monthly reporting: Dedicated feeds make categorization and reconciliation far more reliable.

- You run payroll or reimbursements through Gusto: Business purchases should go through business systems, not owner cards.

- You expect growth: Employee cards, cleaner records, and business credit development support scale.

A personal card is only a narrow short-term option

A personal card is tolerable only when the business is very small, very early, and tightly controlled. Even then, strict separation inside your records matters. The moment the business becomes a real operating company, the personal-card workaround starts costing more than it saves.

The better habit is simple. Open the business bank account. Get the business card. Route all company purchases through it. Keep owner spending out of the business ledger unless it's intentionally recorded as a contribution, draw, or reimbursable expense.

That decision pays off in cleaner books, fewer tax headaches, and a more defensible operating structure.

If you want help cleaning up mixed transactions, setting up QuickBooks correctly, or building a bookkeeping and payroll workflow that scales, Steingard Financial can help you put the right structure in place. They work with service businesses across the U.S. to untangle historical messes, tighten month-end close, and create cleaner reporting through QuickBooks and Gusto.