Decoding Your Profits: Non Operating Costs Guide

Revenue is up. Clients are paying. Your team is busy. Then you open QuickBooks, glance at your profit and loss statement, and wonder why the bottom line looks thinner than expected.

That gap often comes from costs that aren't part of delivering your service, but still hit your profit hard. Loan interest. A legal bill. A write-down on equipment you sold at a loss. These aren't day-to-day operating costs, yet they can change how healthy your business looks on paper and how much cash you keep.

A lot of owners miss them because they focus on sales, payroll, software, and rent. That's reasonable. Those are the obvious drivers of operating performance. But non operating costs tell a different story. They show what financing choices, one-time events, and non-core decisions are doing to your final earnings.

That category can be bigger than many people assume. In one hospital study, non-patient-related expenses, a form of non-operating costs, represented a median 14.6% of operating expenses in 2024 and ranged from 0.2% to 51.1% across hospitals, according to Trilliant Health's hospital margin analysis. Different industry, same lesson. “Non-core” doesn't always mean “small.”

The Hidden Story Your Financials Are Telling

A service business can look strong in the work it performs and still disappoint at the bottom line.

Take a common situation. A consulting firm grows billings, keeps utilization high, and controls payroll. On the surface, the operation is working. But net income drops because the owner took on debt, paid interest each month, and settled an old dispute. Nothing in that list says the delivery team did a worse job. Yet the final profit number still falls.

That's why non operating costs matter. They explain why good operations and weak net income can exist at the same time.

Why owners get tripped up

Profit is often interpreted as one clean verdict. Profitable or not profitable. Healthy or unhealthy. The problem is that a profit and loss statement blends multiple stories together unless the accounts are set up clearly.

One story is about your core engine. Did your pricing, labor mix, and overhead support profitable service delivery?

The second story is about everything around that engine. Did debt, legal issues, asset decisions, or one-time events pull earnings down?

Practical rule: If a cost didn't help your team deliver the service you sell this month, stop and ask whether it belongs outside operating expenses.

For owners using QuickBooks, this matters because messy categorization creates false signals. Interest expense buried in general overhead makes operations look less efficient than they are. A one-time legal charge mixed into administrative expenses can make a normal month look broken.

When you separate these items correctly, your reports become decision tools instead of compliance documents. You can see whether the business model is working, whether financing is too expensive, and whether an unusual event is temporary or a sign of deeper trouble.

Core Concepts Operating vs Non-Operating Costs

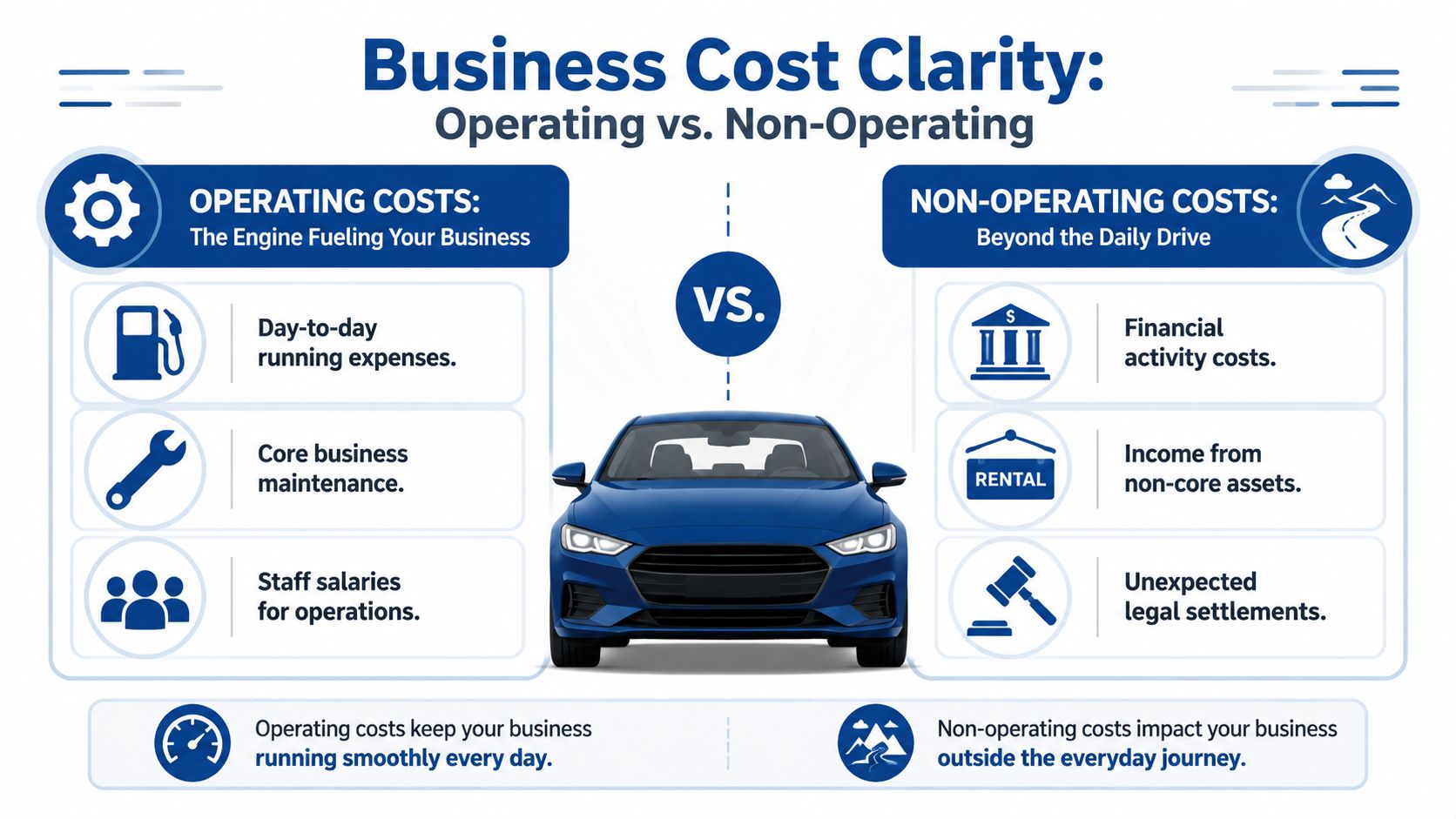

The easiest way to think about this is a car.

Your operating costs are the fuel, maintenance, and routine parts that keep the car moving every day. Your non-operating costs are the financing cost on the car loan, the loss from selling an old vehicle, or a legal issue from an accident. Both affect your wallet. Only one group tells you what it takes to run the vehicle day to day.

The core test

Ask one question first.

Does this cost directly support delivering the service you sell?

If yes, it usually belongs in operating expenses. If no, and it relates to financing, asset sales, legal events, or unusual losses, it may belong in non-operating costs.

For many service businesses, the largest recurring non-operating cost is interest expense from loans or lines of credit, while less frequent but still material items can include losses on disposal of old equipment or one-time legal fees, as noted in Alaan's overview of operating and non-operating expenses.

Operating vs Non-Operating Costs at a Glance

| Category | Operating Costs (Core Business Activities) | Non-Operating Costs (Incidental Activities) |

|---|---|---|

| Purpose | Supports service delivery and day-to-day business activity | Comes from financing, asset events, or unusual matters outside core delivery |

| Common service business examples | Wages for service staff, payroll taxes, software subscriptions, rent, internet, insurance tied to operations, marketing, training | Interest expense, loss on disposal of equipment, legal settlement costs, impairment losses, foreign-currency losses |

| How often they occur | Usually recurring and expected | Often irregular, event-driven, or tied to financing structure |

| What they tell you | Whether your service model is efficient | Whether debt, one-time events, or non-core decisions are affecting earnings |

| QuickBooks concern | Need detailed expense accounts for accurate job and overhead tracking | Need separate “Other Expense” or similar accounts so they don't muddy operating KPIs |

Examples owners commonly misclassify

A few edge cases cause confusion.

- Interest on a working capital line is not the cost of delivering bookkeeping, legal work, consulting, marketing services, or IT support. It's a financing cost.

- Payroll for your delivery team is operating. It belongs with the cost of running the business.

- A loss on selling an old office server or computer isn't an ordinary monthly operating expense.

- Routine legal fees tied to contracts or compliance may need judgment. Some firms treat recurring legal support as operating because it's part of normal administration. A lawsuit settlement usually belongs outside core operations.

A useful habit in QuickBooks is to ask, “Would I expect this account balance every month if I had no debt, no asset sale, and no unusual event?” If the answer is no, review the classification.

The goal isn't perfection on the first pass. It's consistency and a chart of accounts that makes your financial story readable.

How Non-Operating Costs Appear on Financial Statements

On a standard income statement, non-operating costs appear below operating income. That placement is intentional. It gives anyone reading the report a cleaner view of core performance before financing activity and one-time events are layered in, as described in NetSuite's explanation of non-operating expenses.

What the income statement is trying to show

Think of the profit and loss statement as a sequence.

First, it shows revenue. Then it subtracts the costs of running the business. That produces operating income. After that, it includes items outside normal operations, such as interest expense or a loss on an asset disposal. The result moves closer to net income.

A simple reading flow looks like this:

- Revenue

- Operating expenses

- Operating income

- Non-operating income and expenses

- Net income

That middle subtotal matters. If operating income is healthy, your service model may be solid even if net income is under pressure.

Why the placement matters to lenders and owners

Banks, investors, and owners don't all ask the same question.

A lender may care whether debt payments strain earnings. An owner may care whether pricing and staffing are working. A manager may care whether overhead is under control. Keeping non-operating costs below operating income helps each person isolate the part of the business they're evaluating.

If you're still getting comfortable reading your reports, this guide to understanding profit and loss statements gives helpful context on how the pieces fit together.

Clean financials don't just answer “Did we make money?” They answer “What kind of money did we make, and what pulled it down?”

QuickBooks reporting implications

In QuickBooks Online, the placement on the report depends on the account type and report mapping. If you post interest expense into a regular overhead account, your operating section gets distorted. If you create separate accounts under other expense categories, the report is far easier to read.

That also improves internal analysis. If you're reviewing pricing or labor efficiency, you want operating costs separated before you calculate margin. If you're refining internal cost tracking, clear classifications also make related tools like overhead rate formulas more useful because the overhead base isn't cluttered with financing or one-off items.

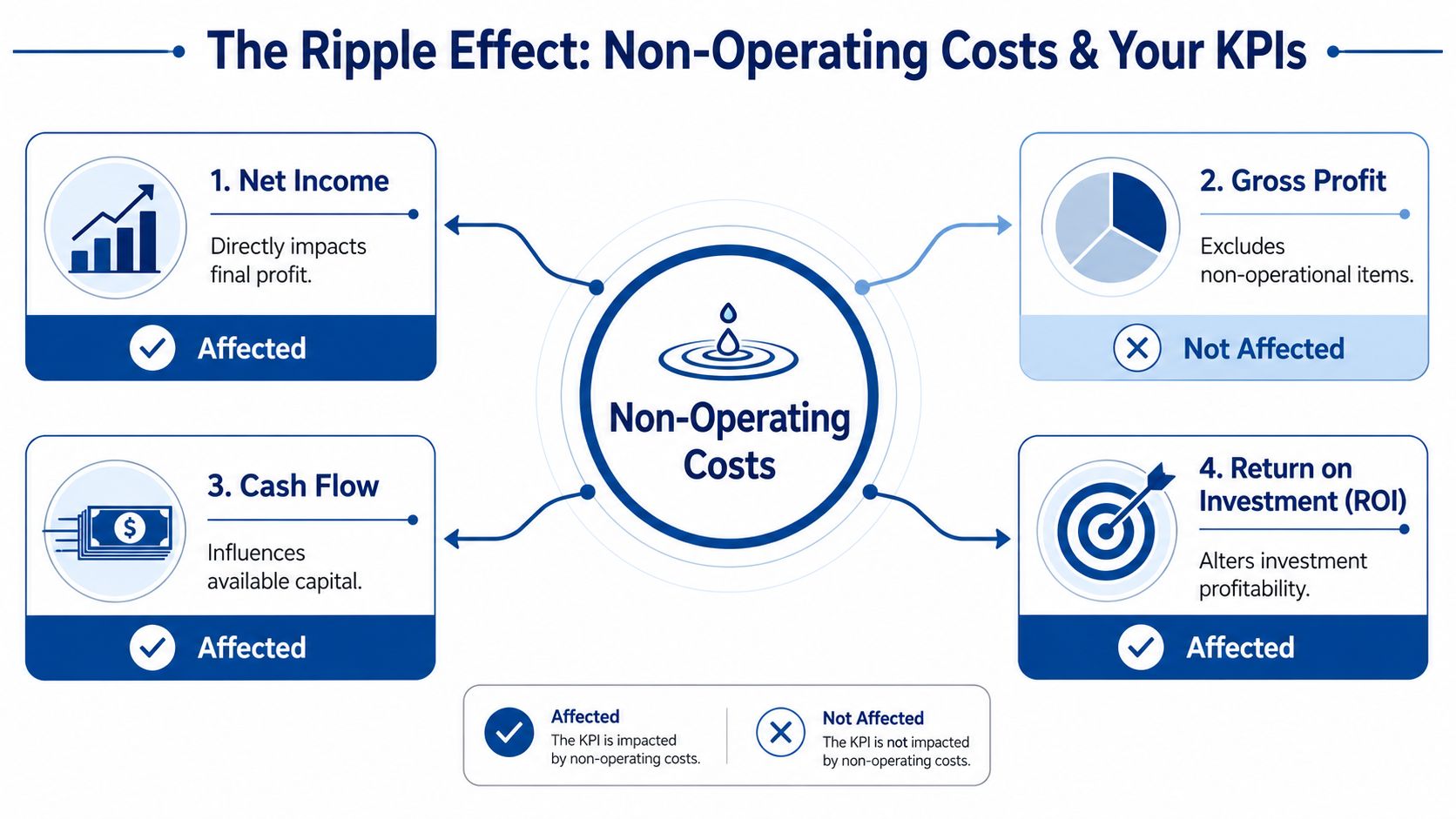

The Real Impact on Your Business KPIs

Non operating costs don't hit every metric the same way. That's where many owners get confused.

They see net income drop and assume the service model weakened. Sometimes it did. Sometimes it didn't. Sometimes debt, a settlement, or a disposal loss pushed down final profit while core operations stayed steady.

Which KPIs change and which don't

Here's the practical view most service owners need.

| KPI | Effect of non operating costs | Why it matters |

|---|---|---|

| Gross profit | Not affected directly | Gross profit focuses on revenue minus direct service delivery costs |

| Operating margin | Not affected directly when classified correctly | It measures performance from core business operations |

| EBITDA | Generally excludes financing costs such as interest | Useful for comparing operational performance apart from capital structure |

| Net income | Affected directly | It includes the full impact of non-operating costs |

| Cash flow | Often affected | Even if a cost is “non-operating,” it can still reduce cash available to run the business |

Why operating margin can look healthy while net income looks weak

This is normal, not contradictory.

A firm can price well, control payroll, and maintain a strong operating margin. Then interest expense lowers the final profit. Or a legal settlement lands in one month and hits net income without saying much about the quality of current service delivery.

That distinction matters in owner meetings. If you respond to a financing problem by cutting delivery payroll, you may solve the wrong problem.

EBITDA helps, but only if the books are clean

Many advisors use EBITDA because it strips out some items that can obscure operating performance. That can be useful when comparing periods or discussing the business with lenders or buyers.

But EBITDA only works if the underlying accounts are mapped correctly. If loan interest is buried inside office expense or admin overhead, the metric loses credibility. QuickBooks won't fix that automatically. Someone has to build the chart of accounts and review transactions with intent.

Owner takeaway: Use operating margin to judge how the business runs. Use net income to judge what the whole structure of the business, including debt and unusual events, is producing.

A practical monthly review might include all three questions:

- Are core operations profitable?

- Did non-operating items change the final result?

- Was the impact temporary, recurring, or financing-driven?

That approach keeps you from overreacting to the wrong number.

Best Practices for Your Chart of Accounts and Tools

Most non operating cost problems start in the chart of accounts, not in the profit and loss report.

If the account structure is too broad, QuickBooks has nowhere sensible to place interest expense, legal settlements, or asset disposal losses. Everything gets dumped into overhead. Then your reports stop helping.

A simple QuickBooks structure that works

For most service businesses, keep your operating accounts clean and your non-core items separate.

Consider a structure like this:

- Operating expense accounts for payroll, payroll taxes, software, rent, marketing, contractor costs, insurance, utilities, travel, and training

- Other expense accounts for interest expense, loss on disposal of assets, legal settlement expense, impairment or write-down expense

- Other income accounts if you also need to track non-operating gains separately

You don't need dozens of tiny accounts. You need enough separation to protect decision-making.

Suggested account names

These names are plain, readable, and easy to manage inside QuickBooks Online:

| Account type | Suggested account name | Use case |

|---|---|---|

| Expense | Salaries and Wages | Core team payroll |

| Expense | Payroll Taxes | Employer payroll taxes |

| Expense | Software and Subscriptions | Day-to-day tools |

| Expense | Rent and Occupancy | Office or workspace cost |

| Other Expense | Interest Expense | Loans, lines of credit, financing charges |

| Other Expense | Loss on Asset Disposal | Equipment or furniture sold below book value |

| Other Expense | Legal Settlement Expense | Non-routine lawsuit or settlement costs |

| Other Expense | Write-Downs and Impairments | Non-core value reductions |

If you're building this from scratch, this article on how to create a chart of accounts is a practical companion.

Tool setup matters as much as account setup

A clean chart of accounts only helps if connected tools feed it correctly.

If you run payroll through Gusto or QuickBooks Payroll, map wages, employer taxes, benefits, and reimbursements to operating accounts. Don't let payroll software post labor into vague buckets that later require cleanup. The same goes for loan payments. Split principal and interest correctly so only the interest hits the profit and loss statement.

For businesses that want outside help with setup and cleanup, Steingard Financial works with QuickBooks and payroll platforms to structure accounts, categorize transactions, and produce KPI-focused reporting. That's one option. Some owners handle setup internally, and others use a CPA or outsourced bookkeeping team.

A monthly review checklist

Use this at month-end:

- Scan for interest expense and confirm it didn't land in bank fees or general admin.

- Review legal and professional fees to separate normal recurring counsel from unusual matters.

- Check fixed asset activity if you sold or retired equipment during the month.

- Look for one-time entries that shouldn't stay in routine overhead accounts.

Small classification errors create big interpretation errors.

Strategies for Managing and Reducing Non-Operating Costs

You can't eliminate every non-operating cost. You can manage many of them before they turn into profit surprises.

Start with the recurring items

For many service businesses, interest expense is the biggest recurring non-operating cost. That means debt structure deserves regular attention.

Ask practical questions. Is the loan still the right fit? Is the rate competitive? Does the business still need that balance level? If refinancing, restructuring, or faster payoff lowers interest burden, that improvement goes straight to the bottom line.

Reduce surprises from asset and legal events

Some non-operating costs aren't monthly, but they are still manageable.

- Plan asset disposals early. If old equipment has little value left or needs replacement, review timing and expected proceeds before the sale.

- Maintain documentation. Good records reduce confusion when unusual transactions hit QuickBooks.

- Review insurance coverage. A gap in coverage can turn a dispute or incident into an expensive out-of-pocket event.

- Use approval controls. Require review before major write-offs, settlements, or disposal decisions.

Non-operating doesn't mean uncontrollable. It often means the decision happened earlier, outside daily delivery work.

A short educational walkthrough can help frame the issue from a business owner's perspective:

Build a review habit, not a rescue project

The best time to manage non operating costs is before year-end.

A monthly finance review should include a short section for non-core items. Look at interest. Check unusual legal or professional fees. Ask whether any write-down, settlement, or disposal loss needs explanation. If the same “one-time” account appears over and over, it isn't one-time anymore.

That discipline improves more than reporting. It sharpens owner decisions about borrowing, insurance, contracts, and asset purchases.

How an Outsourced Partner Creates Financial Clarity

Most owners don't struggle because the concept is too advanced. They struggle because they don't have time to police every account, every bank rule, and every month-end classification detail.

That's where an outsourced accounting partner earns its keep. The value isn't just bookkeeping. It's turning a noisy profit and loss statement into a report you can put to use.

What clarity looks like in practice

A good partner separates operating and non-operating items at the account level, reviews unusual transactions before month-end closes, and helps you interpret what the numbers mean for pricing, staffing, debt, and cash.

That matters if you're growing, borrowing, or presenting results to lenders or investors. Some companies also pair bookkeeping support with broader finance leadership. If you're weighing that route, this perspective on hiring fractional finance experts is useful for understanding when strategic finance support makes sense.

Why owners outsource this piece

The hard part isn't knowing that interest expense belongs below operating income. The hard part is doing the work consistently.

That means:

- Designing the chart of accounts so the reports separate cleanly

- Reviewing transactions monthly for unusual items and misposts

- Protecting KPIs so operating margin and related metrics reflect the business accurately

- Explaining the story behind the numbers in plain English

If you're considering outside support, this overview of outsourced accounting for small business outlines what that model typically includes.

When non operating costs are tracked correctly, you stop guessing why profit changed. You can tell whether the issue came from operations, financing, or a one-off event. That's the kind of clarity that supports better decisions.

If your QuickBooks file doesn't clearly separate operating results from non-core costs, Steingard Financial can help you clean up the chart of accounts, improve reporting, and make your month-end numbers easier to trust.