You've got money in the business account, payroll is run, clients are paying, and now the obvious question shows up. How do you take money out correctly?

For service business owners, this usually starts as a cash question and quickly becomes a tax and bookkeeping problem. The words distribution and dividend sound interchangeable. They aren't. If you code the payment the wrong way in QuickBooks, skip payroll when payroll was required, or pull cash without tracking basis or equity, you can end up with bad financials, tax surprises, and cleanup work later.

Owners often get tripped up. A profitable S corporation owner may call every owner payment a dividend. A C corporation shareholder may assume a cash transfer is just a draw. An LLC owner may mix personal spending with business expenses and expect the books to sort themselves out. They won't.

The right treatment depends first on your entity type, then on how you process the payment, then on whether your books support it. QuickBooks and Gusto can make this easier, but only if the setup matches the legal reality of the business.

Distribution vs Dividend What Business Owners Must Know

If you own a service business, the first rule is simple. You don't get to pick a payout label based on preference. Your entity type picks most of the rules for you.

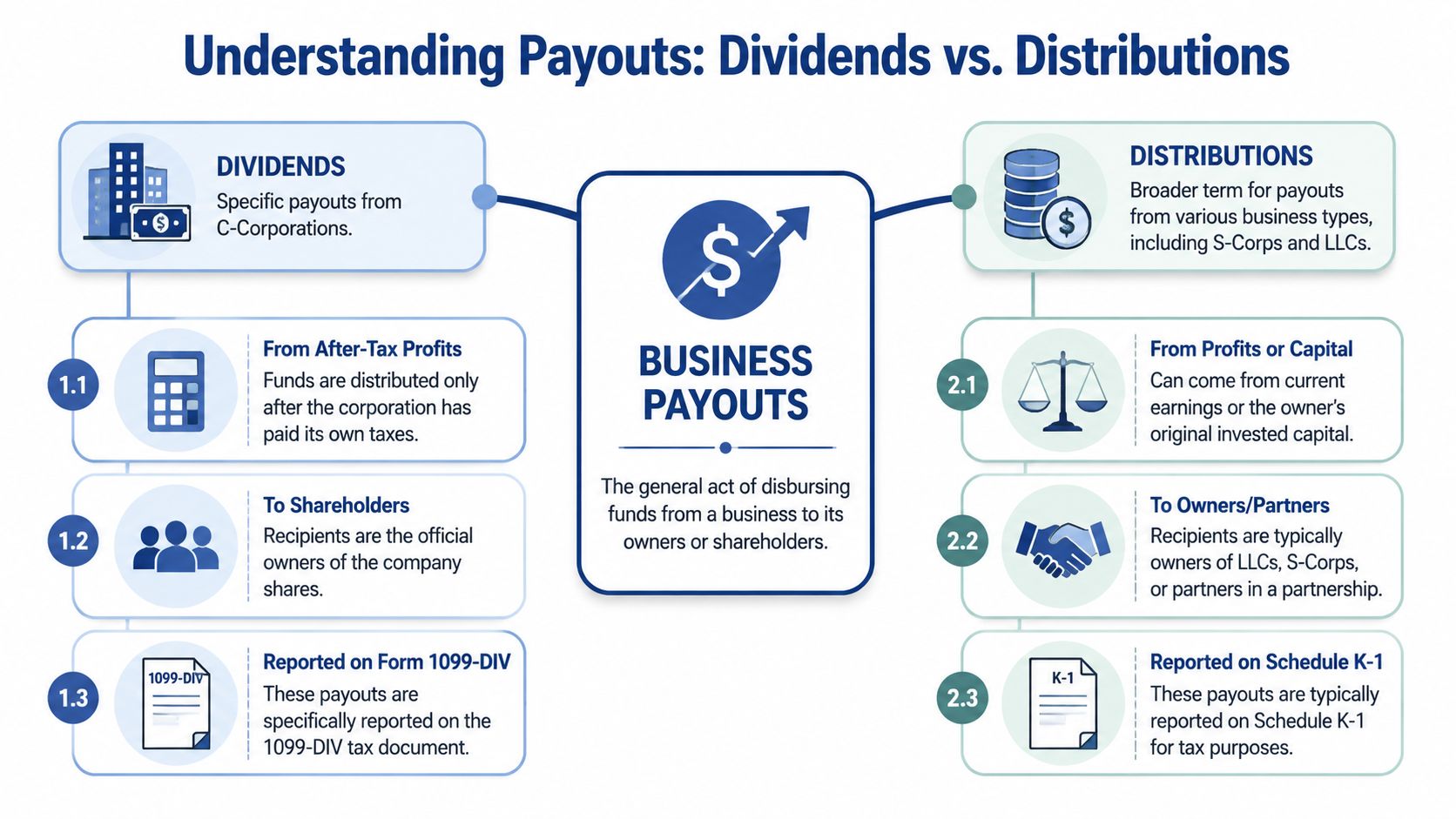

A dividend is a payment a corporation makes to shareholders from profits, and it's usually paid quarterly or annually. A distribution is a broader payout term used for entities and vehicles where payments may include more than corporate profit, such as S corporations and funds. That distinction matters because the tax treatment can change depending on how the payment is classified and what kind of entity is making it.

Here's the practical version for business owners:

| Issue | Dividend | Distribution |

|---|---|---|

| Typical business using it | C corporation | S corporation, LLC taxed as partnership, LLC taxed as S corp |

| Who receives it | Shareholders | Owners, members, partners, S corp shareholders |

| Where it comes from | Corporate profits | Owner equity, pass-through income, sometimes capital |

| Tax reporting | Often tied to Form 1099-DIV for corporate dividends | Often tied to owner-level reporting such as Schedule K-1, depending on entity |

| Bookkeeping treatment | Equity payout, not payroll expense | Equity payout, not payroll expense |

| Main risk | Double-tax style confusion and bad retained earnings tracking | Reasonable compensation failures, basis issues, messy owner draw coding |

Practical rule: If the payment is compensating you for work, start by asking whether it belongs in payroll, not whether it belongs in distributions.

Owners usually focus on how to get cash out. The better question is how to get cash out without breaking payroll compliance or your books. That means separating three things that are often blended together in small businesses:

- Salary or wages through payroll

- Owner distributions or draws through equity

- Dividends if the business is a C corporation

When those are mixed, your P&L gets distorted, bank reconciliations get harder, and year-end tax prep turns into reconstruction work.

The Fundamental Payouts Dividends and Distributions

At the simplest level, a dividend is one kind of distribution, but not every distribution is a dividend.

A dividend belongs to the corporate world. Citizens explains that a dividend is a payment a corporation makes to shareholders from profits, while a distribution is a broader payout term used for vehicles such as mutual funds, ETFs, and S corporations, where the payment can include dividends, interest, and capital gains rather than just corporate profit. It also notes that C-corporation dividends are generally paid from after-tax corporate earnings and can be taxed again at the investor level, while S-corporation distributions are typically pass-through payments that avoid corporate-level tax, as described in Citizens' explanation of dividends and distributions.

Dividends are a corporate profit payout

Think of a dividend like serving slices of pie after the company has already paid for the ingredients, the kitchen, and the staff. In a C corporation, the company earns profit, pays its own tax, and may then issue a dividend to shareholders.

From a bookkeeping angle, that means you don't run a dividend through payroll and you don't book it as an operating expense. It belongs in equity. If you want a refresher on how retained earnings interacts with owner payouts, this retained earnings sample is a useful reference.

Distributions are broader and more flexible

A distribution is the wider umbrella. In a pass-through business, it's often the cash owners take out apart from wages. The tax logic is different because the entity itself may not be paying tax in the same way a C corporation does.

That's why service business owners in LLCs and S corporations need to be careful with language. Calling an S corp owner payment a “dividend” may sound harmless in conversation, but it creates confusion in accounting records, tax prep, and shareholder reporting.

If you've seen distributions discussed in a real estate context, that's a good comparison point because the term is used more broadly there too. Homebase has a clear primer on how real estate distributions work, and it helps illustrate why “distribution” is a broader concept than “dividend.”

In practice, the label matters because the label tells your bookkeeper what equity account to hit, tells your payroll team what not to run through wages, and tells your tax preparer what trail to follow at year-end.

How Your Business Structure Dictates the Rules

The biggest mistake owners make in the distribution vs dividend conversation is treating it like a preference. It's not. Your legal and tax structure controls the vocabulary, the compliance rules, and the bookkeeping workflow.

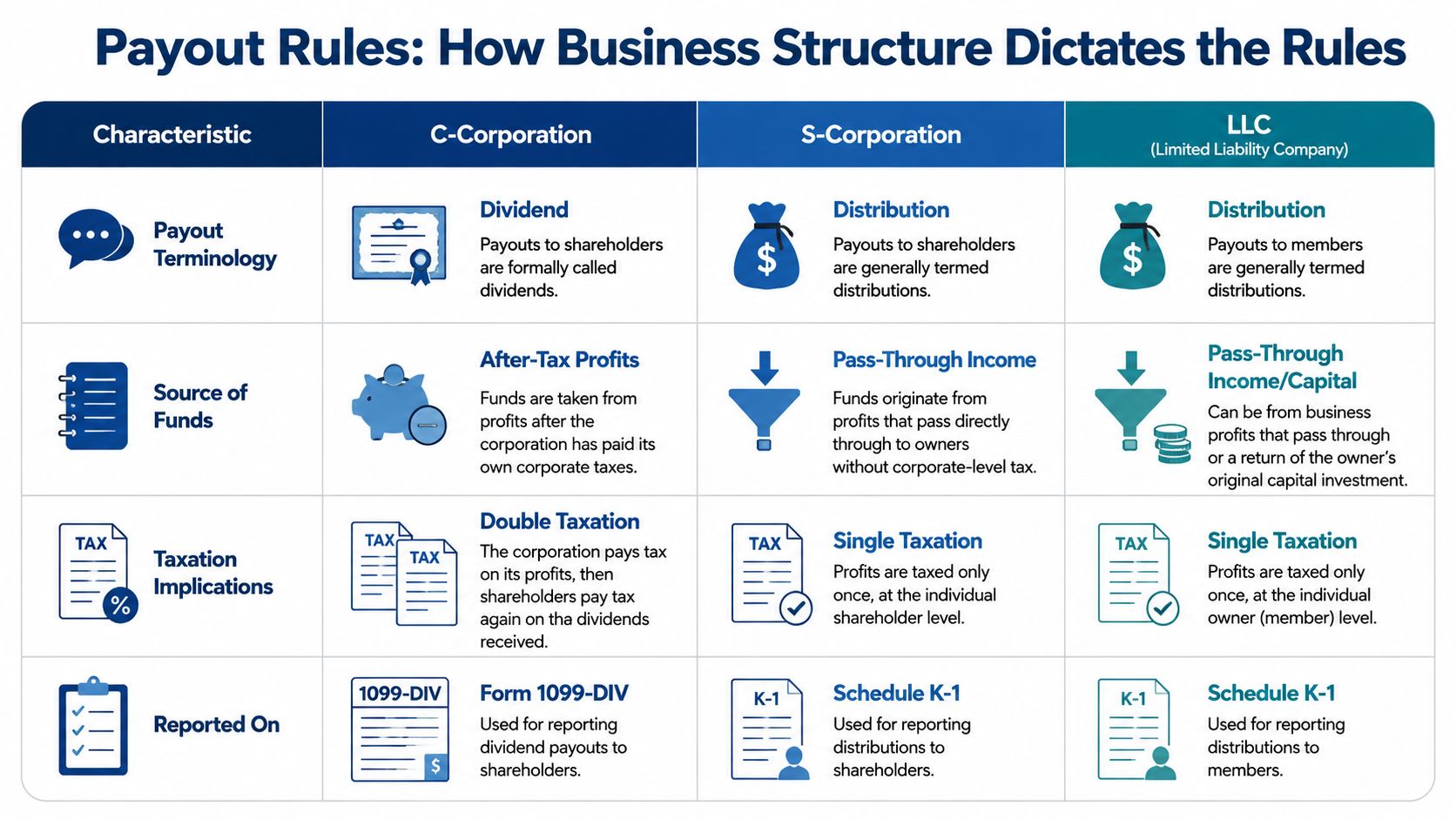

C corporations

C corporations deal with dividends. The IRS notes that dividends are a subset of corporate distributions paid out of a corporation's earnings and profits, and corporations report them on Form 1099-DIV. The IRS also distinguishes dividends from return of capital, which is not a dividend because it reduces the shareholder's adjusted cost basis, as outlined in IRS Topic No. 404 on dividends.

For a service business owner, that means a few practical things:

- Corporate tax comes first: The company is its own taxpayer.

- Dividend decisions are formal: Board approvals, shareholder records, and equity tracking matter.

- The books must show capacity: If retained earnings and shareholder equity don't support the payment, your records won't tell a clean story.

A lot of smaller service firms never need C corp dividends in routine operations because owners are typically taking salary, bonus, or reinvesting cash. But if you are operating as a C corp, “owner draw” is not the right mental model.

S corporations

S corporations deal with distributions, not dividends in the usual operating sense. The business is generally a pass-through entity, so profits move to the shareholder's tax world differently than they do in a C corp.

This is the classic setup for owner-operators in consulting firms, agencies, practices, and other service businesses. The opportunity is clear. The compliance trap is also clear. You can't skip payroll and just take distributions if you're actively working in the business.

That's why owners who are considering or already using this setup should understand both compensation design and state-level rules. If you want a practical overview that includes state considerations, this guide to understanding California entity taxes is useful background, especially for owners comparing structures. For a more direct look at owner pay mechanics, this article on how to pay yourself from an LLC is a good companion.

What usually works in an S corp

A clean S corp back office usually follows this pattern:

- The owner is set up in payroll if they provide services to the business.

- Gusto or another payroll system runs regular wages.

- Separate bank transfers move owner distributions out of the business.

- QuickBooks codes those transfers to a dedicated equity account such as Shareholder Distributions.

What usually fails

The opposite pattern creates problems fast:

- No payroll at all: The owner takes cash whenever needed.

- Personal charges on the business card: Meals, mortgage, travel, and family spending get mixed into expenses.

- No equity account structure: Every payment lands in “Ask My Accountant” or gets posted to an expense line.

That setup produces inaccurate profit reports and unnecessary tax risk.

LLCs

LLCs are where the confusion gets worst because the legal form is flexible. An LLC can be taxed in different ways, and the tax election determines whether owner payments behave more like draws, S corp distributions, or C corp dividends.

If the LLC is taxed as a partnership or disregarded entity, owners usually take draws or distributions rather than dividends. If the LLC elected S corporation taxation, the S corp rules control the payout process. If it elected C corporation taxation, then dividend rules can come into play.

The LLC label on your state filing doesn't answer the payout question by itself. Your tax classification does.

So when someone says, “I have an LLC, can I take dividends,” the right answer is usually another question. How is the LLC taxed?

Tax and Compliance A Deep Dive for Owners

Once the entity type is clear, the substantive work starts. Payouts are easy to move in the bank. They're harder to defend on the tax return if the setup is sloppy.

C corp owners need to separate compensation from shareholder return

If you work in your C corporation, money can leave the business in more than one way. Some of it may be compensation. Some may be a shareholder return. Those are not interchangeable in the books.

The practical control here is documentation. If the payment is for services, run it through payroll. If it's a dividend, support it as a shareholder payout and keep it out of operating expenses.

There's another point many owners miss. Fidelity explains that when a company pays a dividend, the stock price should adjust downward because cash leaves the company's asset base. A special dividend causes an immediate price reduction, which shows that a dividend isn't free cash. It's a transfer of value from corporate assets to shareholders, as described in Fidelity's explanation of why dividends matter.

S corp owners need reasonable compensation discipline

For service businesses, this is often the most important compliance issue in the entire article. If you own an S corp and actively work in it, you generally need to pay yourself a reasonable salary before relying on distributions.

That means:

- W-2 pay belongs in payroll: Use Gusto, not ad hoc bank transfers.

- Distributions come after that system is running: They're not a replacement for wages.

- Support matters: Job role, duties, and consistency in payroll all matter more than what you call the transfer in the memo line.

If you skip this and pull cash only as distributions, you create a problem that software can't solve after the fact.

A bad owner-pay system usually leaves fingerprints in three places at once: payroll, the general ledger, and the owner's personal tax return.

Fund-style distributions show why labels can mislead

A useful parallel comes from investment reporting. Scotia fund materials note that distributions can be taxable even when reinvested and can reduce NAV by the distribution amount, which means headline yield can overstate usable cash flow. The same materials note that distributions may include return of capital, capital gains, and foreign income, which makes them more variable and harder to model than regular dividends, as explained in Scotia's discussion of fund distributions.

That same mindset helps business owners. The cash movement alone doesn't tell you the tax result. You need to know what the payment is.

For owners operating internationally or comparing how compliance pressure shows up in different systems, this article on cash flow and compliance for Australian businesses is a good reminder that clean records and timely processing matter everywhere.

Recording Payments in QuickBooks and Gusto

Here, theory turns into process. If the books are clean, owner payouts are easy to follow. If the chart of accounts is vague, every payout turns into cleanup.

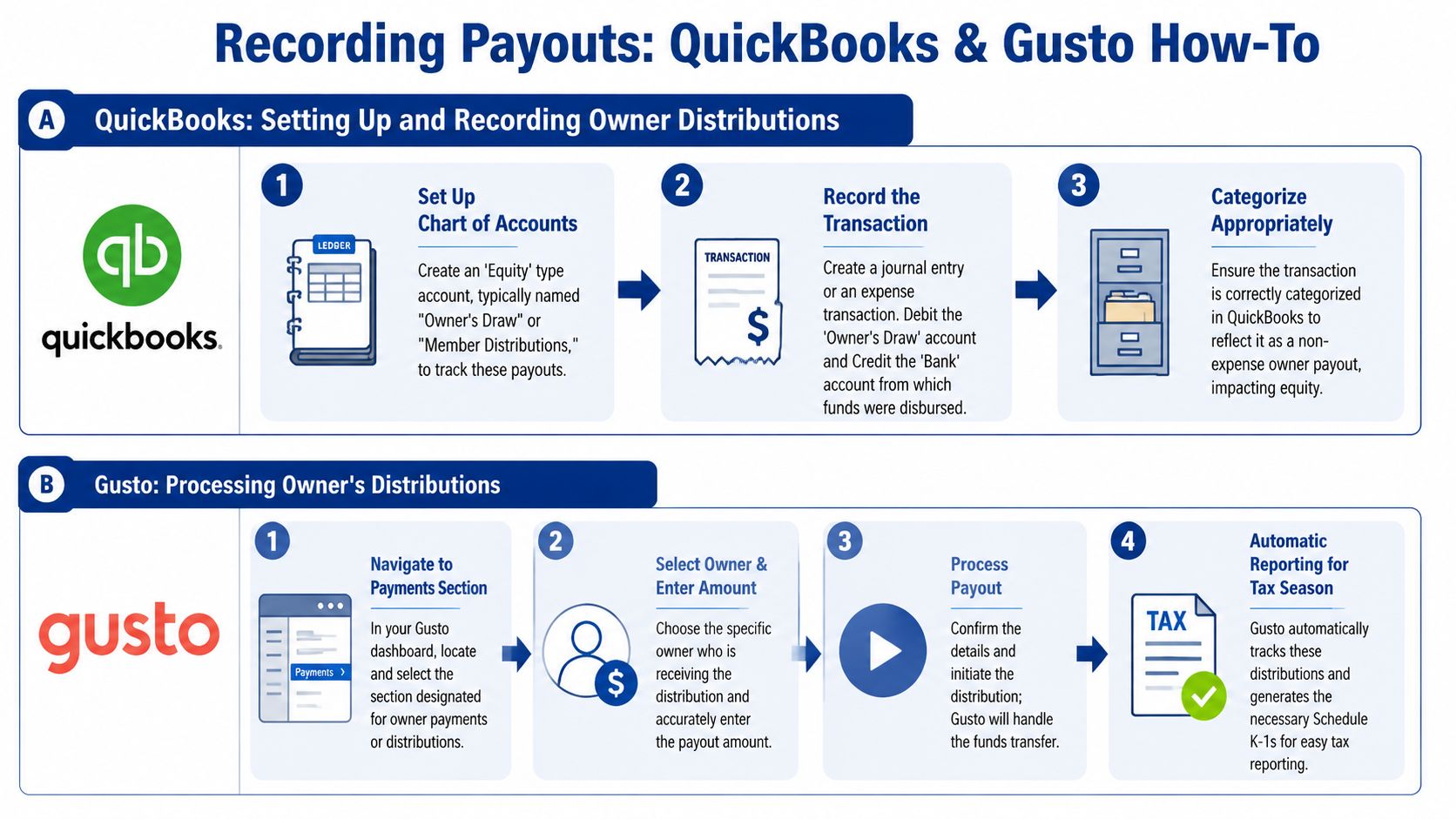

Set up the chart of accounts first

Before recording a single payout, create the right equity accounts in QuickBooks Online. If you need a starting point, this walkthrough on how to create a chart of accounts is a good baseline.

For most service businesses, I'd use accounts like these:

| Entity type | Suggested QuickBooks equity account |

|---|---|

| Single-member LLC or partnership-style LLC | Owner Draw or Member Distribution |

| S corporation | Shareholder Distributions |

| C corporation | Dividends Paid or Shareholder Dividends |

| Any entity with owner payroll | Keep wages in payroll accounts, not equity |

The naming matters because it keeps reports readable for the owner, the bookkeeper, and the tax preparer.

How to record an S corp or LLC distribution

For a straightforward owner distribution paid by bank transfer:

- Open the bank transaction in QuickBooks.

- Categorize it to the appropriate equity account, not an expense account.

- Add the owner name in the memo if there are multiple owners.

- Reconcile the bank account so the transfer clears cleanly.

If you're entering it manually rather than through bank feed, the accounting logic is simple:

- Debit Shareholder Distributions or Owner Draw

- Credit Bank

That reduces cash and records the payout in equity. It does not hit the profit and loss statement.

What not to do

- Don't post owner distributions to Meals, Travel, or Miscellaneous Expense

- Don't let personal spending sit in uncategorized expense accounts

- Don't run a distribution through accounts payable

- Don't treat a shareholder distribution as contractor pay

Those shortcuts create distorted margins and bad tax prep data.

How to handle owner salary in Gusto

Gusto is primarily a payroll platform, which means it's built for compensation, not for every type of owner cash movement. If an S corp owner or C corp owner is on payroll, set them up as an employee and run regular wages through Gusto.

That means using Gusto for:

- Salary

- Payroll tax withholding

- Year-end wage reporting

- Consistent pay cadence

It does not mean every owner withdrawal belongs in Gusto.

Here's a practical way to think about it. Use Gusto for labor pay. Use bank transfers plus QuickBooks equity coding for owner distributions.

To see the workflow in action, this short video is a helpful overview:

A repeatable monthly process

The cleanest owner-pay systems are boring. That's a good thing.

Use a monthly checklist:

- Run payroll first: If the owner is an employee, process wages in Gusto on schedule.

- Transfer distributions separately: Use a dedicated bank transfer, not random debit card spending.

- Review equity balances: Make sure each owner's activity is posted where it belongs.

- Close the month: Reconcile bank and credit card accounts before making more owner payouts.

If you can't tell from the QuickBooks balance sheet how much was wages, how much was reimbursement, and how much was owner distribution, the process isn't finished.

Actionable Payout Strategies for Your Business

Most payout problems don't start with tax law. They start with inconsistent habits. The fix is a repeatable payout policy that matches your entity type and your software workflow.

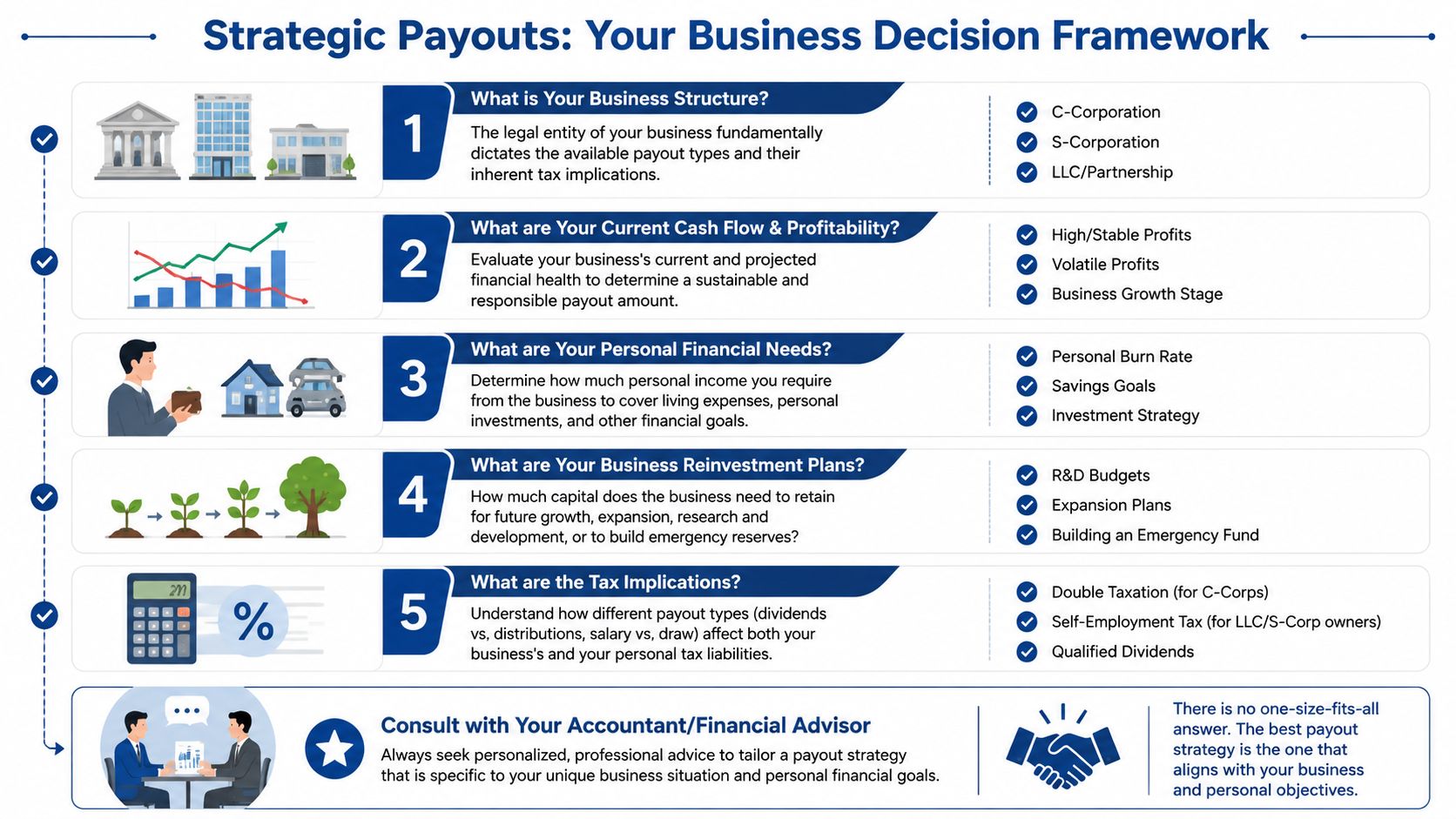

Use this decision framework

Start with the structure, then move to process.

Identify the tax entity

If you're a C corporation, think in terms of dividends and shareholder formalities. If you're an S corporation or partnership-style LLC, think in terms of distributions and owner equity. If you're an LLC, confirm the tax election before doing anything else.

Separate pay for work from pay for ownership

Owners who perform services often need payroll in the mix. Don't use owner distributions to replace wages where wages belong.

Protect the books

Route owner payments through named equity accounts. Don't swipe the business card for personal spending and hope to “true it up later.”

Review before paying out

Check cash needs, open liabilities, payroll timing, and how the distribution will appear in the books. A cash transfer affects more than the bank balance.

Keep the transfer of value in mind

Fidelity's point matters here too. When cash leaves a company as a dividend, that value is leaving the business. It isn't free money appearing from nowhere. It's a movement from company assets to the owner.

What works in real service businesses

The owners who stay out of trouble usually follow a few habits:

- Scheduled payroll: Especially for S corp owner-operators

- Separate distribution transfers: Clean bank trail, easy reconciliation

- Quarterly reviews: Equity, profitability, and tax posture checked before larger owner payouts

- No personal spending on the business card: Reimburse properly or transfer funds out cleanly

What to discuss with your CPA or bookkeeper

Bring these questions to the conversation:

- Am I taking money out in a way that matches my entity type?

- Should any part of this be payroll instead of distribution?

- Are my QuickBooks equity accounts set up correctly?

- Can someone read my balance sheet and immediately understand owner activity?

A good payout strategy isn't fancy. It's clear, documented, and easy to repeat.

If your owner pay is running through a mix of bank transfers, personal card charges, QuickBooks shortcuts, and payroll workarounds, it's time to clean it up. Steingard Financial helps service businesses build accurate books, clear chart of accounts structures, and practical payroll workflows in QuickBooks and Gusto so distributions, dividends, and owner compensation are recorded the right way from the start.