Boost Cash Flow: Working Capital Optimization 2026

You can be profitable, busy, and still feel short on cash every month.

That happens all the time in service businesses. Payroll hits on schedule. Contractors need to be paid. Software renewals stack up. Clients approve work, praise the results, and then take their time paying invoices. On paper, the business looks healthy. In the bank account, it feels tight.

That gap is where working capital optimization matters. Not as a finance buzzword. As a practical way to make sure the cash from your work shows up early enough to support the business you're already running.

Beyond the Buzzword What Working Capital Optimization Means for Your Service Business

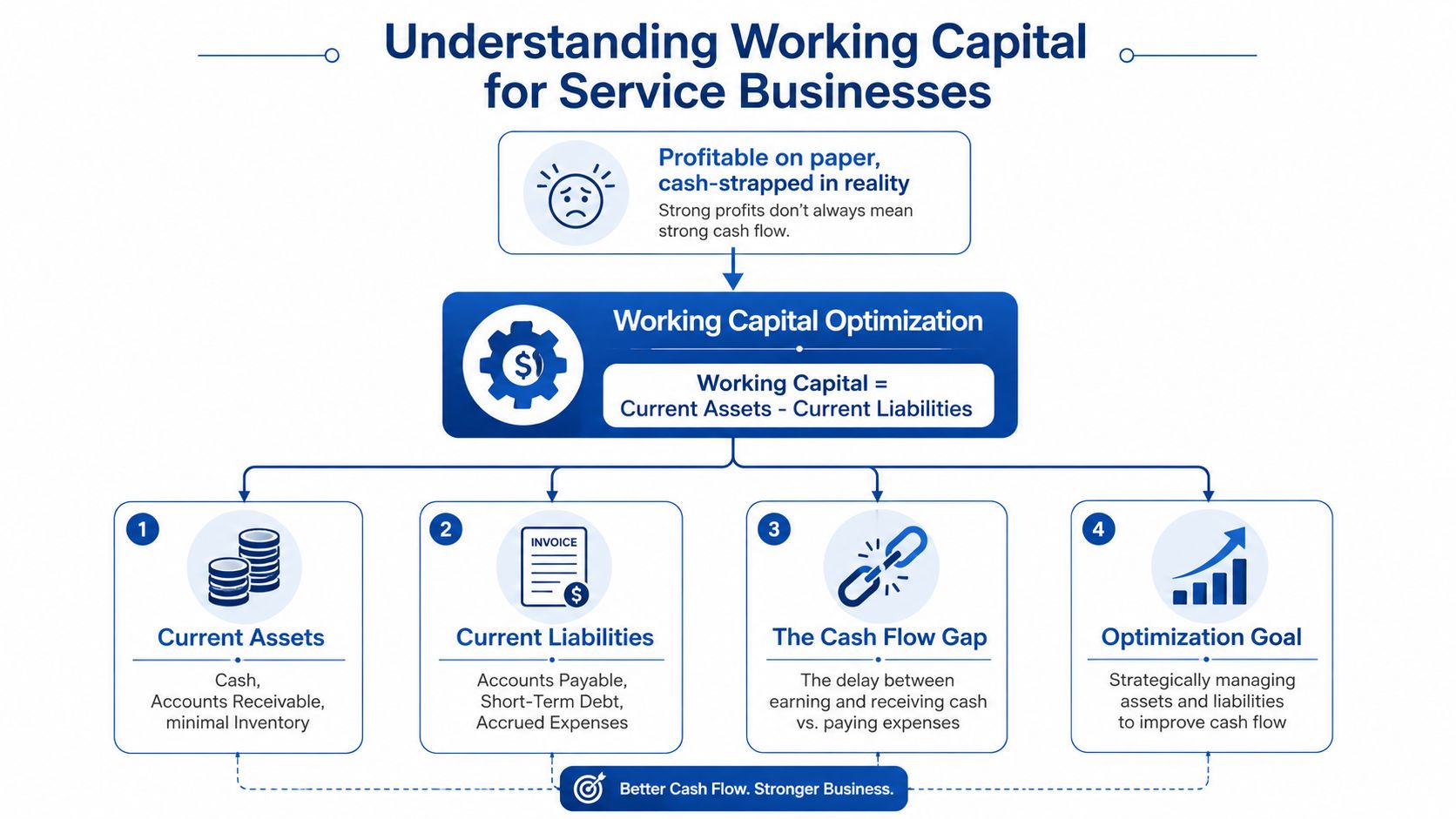

A service business can post a strong month on the P&L and still feel squeezed by Friday payroll.

For a service owner, working capital is not an abstract finance metric. It is the cash cushion between money going out now and money coming in later. The textbook formula is current assets minus current liabilities, but the practical question is simpler: can the business cover payroll, contractors, taxes, software, and vendor bills without waiting too long for clients to pay?

That question plays out differently in service firms than it does in inventory-heavy companies. Agencies, consultancies, law firms, IT providers, architecture firms, and other expertise-based businesses do not usually tie up cash in shelves of product. As HighRadius on working capital optimization strategies notes, service firms generally carry far less inventory than manufacturers, so the standard advice built around stock levels and warehouse turns only gets you part of the way.

In a service business, the primary pressure points are operational.

Your working capital is often trapped in work completed but not billed, invoices sent but not collected, and labor costs that hit before client cash arrives. That is why two firms with the same revenue can have very different cash positions. The one with cleaner billing habits, tighter approval steps, and better payment timing usually has more room to operate.

Where service firms really get stuck

The assets that matter most are usually invisible on a shop floor:

- Time already delivered that has not made it onto an invoice

- Invoices already sent that are sitting in accounts receivable

- Payroll and contractor costs due on a fixed schedule

- Vendor payment terms that may be shorter than client payment terms

I see this often in QuickBooks files. Revenue is recorded correctly. The problem is timing. A project wraps up on the 28th, the invoice goes out on the 10th, terms are net 30, and payroll keeps drafting every two weeks. Profit exists. Cash is late.

What optimization actually looks like

For a service business, working capital optimization means tightening the gap between doing the work and getting paid for it, while using vendor terms carefully enough to protect cash without creating strain with the people you rely on.

It usually shows up in a few practical moves:

| Focus area | What it means in a service business |

|---|---|

| Receivables | Send invoices as soon as milestones are reached, follow up consistently, and reduce billing disputes |

| Payables | Pay on terms, not on impulse, while protecting key vendor relationships |

| Forecasting | Review expected cash in and cash out before the month gets tight |

| Policies | Standardize deposits, due dates, retainers, and approval steps so billing does not stall |

There are trade-offs. Pushing too hard on collections can irritate good clients. Stretching every payable can damage vendor trust. Asking for larger upfront deposits can improve cash, but it may hurt close rates in some markets. Good optimization is not about squeezing every counterparty. It is about setting terms and routines that fit how service work is delivered.

If payroll is your largest fixed outflow, employer structure can affect timing, cash commitments, and administrative burden. This guide to PEO financial implications is a useful reference if you are weighing those choices.

For a broader foundation, Steingard's overview of what is working capital management adds helpful context. The main point for service owners is straightforward. Better cash flow often comes from faster billing, steadier collections, and clearer policies, not just from selling more.

The Diagnostic Phase How to Assess Your Current Cash Cycle

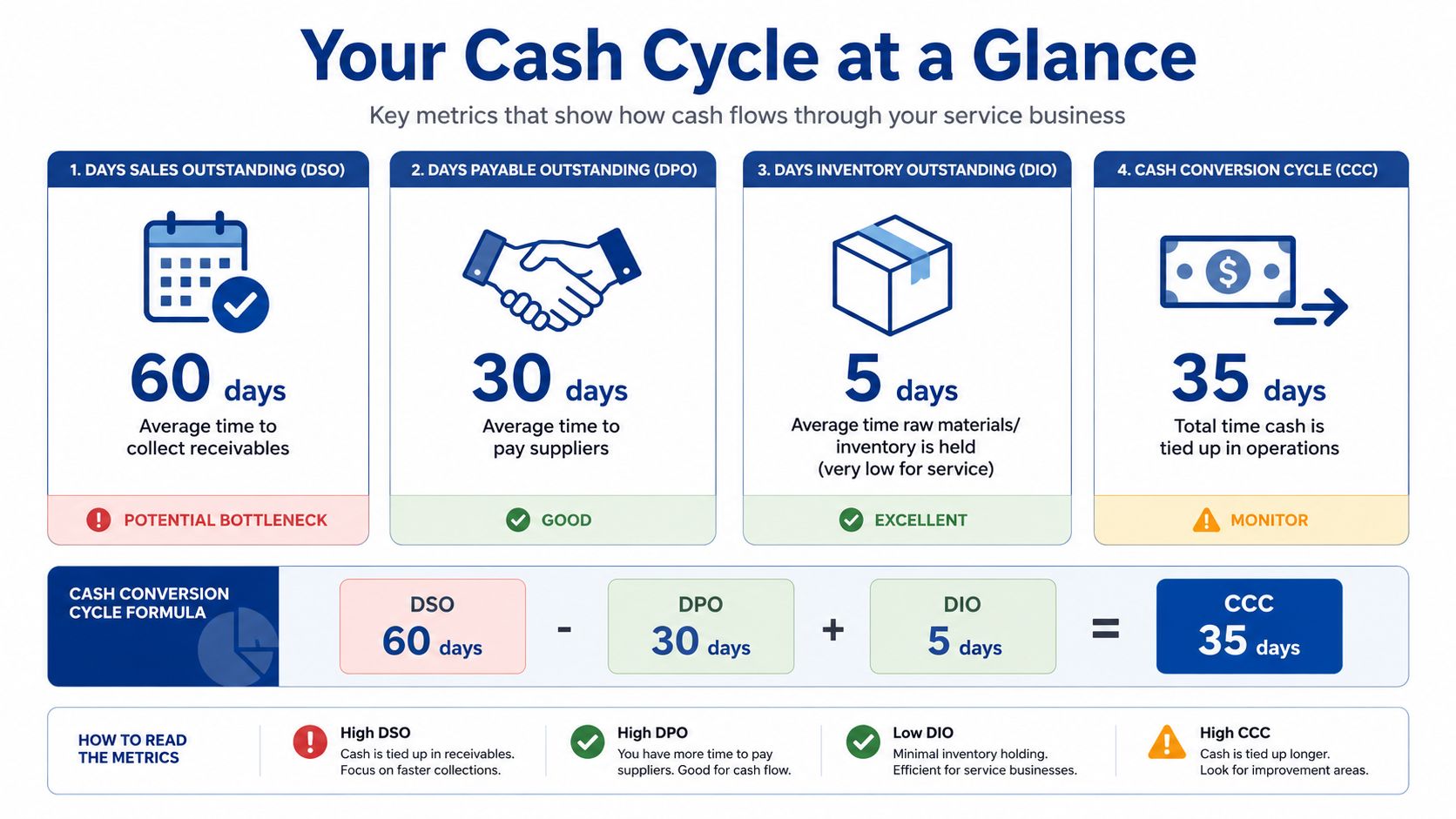

Before changing policies, measure what's happening now. Service owners often know cash feels uneven, but they haven't pinned down where the delay sits. The fastest way to diagnose it is to track three numbers: DSO, DPO, and CCC.

A balanced methodology starts by benchmarking core metrics across receivables, payables, and inventory. The technical formulas for Days Sales Outstanding and Days Payable Outstanding are laid out by Strategic Finance on a balanced approach to optimize working capital. For service businesses, inventory is usually minor, but the same discipline still applies.

The three numbers to calculate

Use a monthly, quarterly, or trailing-period view. Pick one period and stay consistent.

DSO

Formula: (Average Accounts Receivable / Total Credit Sales) × Days in PeriodThis tells you how long it takes to collect after you bill.

DPO

Formula: (Average Accounts Payable / COGS) × Days in PeriodThis tells you how long you take to pay vendors.

CCC

Formula: (DSO + DIO) – DPOThis is the Cash Conversion Cycle. It shows how long cash is tied up between earning revenue and paying obligations. In a service business, DIO is often low, so DSO and DPO do most of the work.

Where to find the numbers in QuickBooks

You don't need a fancy system to start. In QuickBooks Online, pull from:

- A/R Aging Summary for current receivables and past-due patterns

- Balance Sheet for accounts receivable and accounts payable balances

- Profit and Loss for credit sales and cost of goods sold or direct service costs

- Statement of Cash Flows for context when profit and cash don't match

If your books aren't clean, your ratios won't be either. That's why bookkeeping accuracy matters before analysis.

When DSO is high, the problem isn't always collections. Sometimes billing is late, approvals are slow, or invoices go out with missing detail and get parked by the client.

A simple service-business example

Take a small agency that invoices monthly retainers plus project work. It pulls the following from QuickBooks for a chosen period:

- average accounts receivable

- total credit sales

- average accounts payable

- cost of goods sold or direct costs

- very little inventory

Using the formulas above, the owner can see whether cash is getting trapped on the receivables side, released by payables timing, or both. If DSO is stretching while DPO stays short, the business is financing client work with its own cash.

A good side habit here is budgeting. Not because budgets solve collections, but because they help you spot whether recurring outflows are realistic for your current billing rhythm. If you want a simple personal-finance style resource that still reinforces discipline, Firacard's article on effective budgeting strategies is a helpful reminder that visibility changes behavior.

What to look for after the math

Don't obsess over perfection. Look for friction.

- Rising DSO often points to invoicing delays, weak follow-up, or poor contract structure.

- Very low DPO can mean you're paying faster than necessary.

- A long CCC means cash is staying tied up too long in operations.

The first pass doesn't need to be complex. It needs to be honest. Once you have a baseline, you can start pulling the right levers.

Pulling the Right Levers Accounts Receivable and Billing

For most service businesses, the strongest working capital lever is accounts receivable. You don't need to sell more first. You need to get paid on work you've already sold and delivered.

The cash impact can be substantial. Growth Operators on optimizing working capital and cash flow notes that most companies can realize 5 to 15% of annual revenue in cash through disciplined working capital optimization, and gives the example that a $10 million revenue business could free up $500,000 to $1.5 million by tightening collection processes. Service firms feel that principle quickly because labor costs keep moving whether clients pay or not.

Fix the contract before you chase the invoice

Collections problems often start in the proposal or SOW.

A service agreement should answer these questions before work begins:

- When is the first invoice issued

- Is there an upfront deposit

- Are payments tied to calendar dates or milestones

- Who approves invoices on the client side

- What happens if scope expands before the next billing point

If you bill only at the end of a long project, you're choosing to fund that project yourself. That's rarely the best use of your cash.

A healthier structure for service work often includes:

- Upfront deposit for scheduling and kickoff

- Milestone billing for longer projects

- Monthly retainers paid in advance when the relationship supports it

- Clear due dates instead of vague “payable upon receipt” language

Build a collections cadence that doesn't depend on memory

QuickBooks can automate part of this, but the process has to be intentional. A simple cadence might look like this:

- Before due date send a friendly reminder that payment is coming due

- A few days past due trigger an automated reminder with payment link

- Later in the cycle send a personal email from the account manager or owner

- If it continues call the client contact and confirm there isn't an approval issue

- For repeat offenders change future terms before doing more work

That sequence works because it removes ambiguity. Clients often don't ignore invoices out of bad intent. They delay because nobody made the next step clear.

For a stronger receivables process, Steingard's page on accounts receivable best practices is worth keeping handy.

Good collections feel boring. That's the point. If every overdue invoice requires a custom response, your process is too fragile.

Use early payment discounts carefully

Early payment discounts can work well when the client is reliable and the margin supports it. In QuickBooks, you can reflect the discount in the invoice terms or issue a credit when payment arrives within the agreed window. Keep it simple. If the discount terms are confusing, clients won't use them, and your team will spend time fixing avoidable errors.

This short video gives a useful overview of cash flow thinking in practice:

Clean billing beats aggressive collections

Service owners sometimes focus on chasing old invoices while ignoring why those invoices stalled.

Check these first:

| Billing issue | Cash effect |

|---|---|

| Invoice sent late | Collection clock starts later |

| Missing PO or contact | Client can't route approval |

| Vague line items | Finance team asks questions instead of paying |

| Unapproved scope changes | Client disputes amount |

When the invoice is accurate, timely, and easy to approve, collections becomes much less dramatic. That's what working capital optimization should feel like. Less scrambling, more system.

The Other Side of the Coin Managing Payables and Vendors

A lot of owners hear “optimize payables” and translate it as “delay paying everyone.” That's the wrong approach.

Accounts payable works best when you treat it as a scheduling tool, not a stress transfer tool. The goal is to preserve cash without damaging the vendors, contractors, and software partners you depend on. If you create mistrust on the payables side, the short-term cash relief usually comes back as tighter terms, slower service, or awkward conversations when you need flexibility most.

Why DPO matters

There is real cash value in extending payment timing responsibly. CSH & Co. on working capital optimization notes that moving Average Days Payable Outstanding from 45 to 60 days has been a meaningful milestone, and gives the example that a business with $5 million in annual purchases frees up about $205,000 in working capital by extending payables 15 days.

That doesn't mean every service firm should immediately push every vendor to longer terms. It means timing matters, and it has a measurable effect on liquidity.

Which vendors deserve which strategy

Not every payable should be handled the same way.

Core service vendors

Think critical contractors, essential software, and outsourced partners tied directly to delivery. Protect these relationships. If cash is tight, communicate early rather than going silent.Large stable vendors

These are often the best candidates for term discussions. If you pay reliably, you may be able to move from due-on-receipt habits to a more deliberate cycle.Vendors offering useful discounts

Sometimes paying early is the better move, especially when the discount is clear and the cash trade-off makes sense.Small local suppliers

These relationships can be fragile. Stretching them aggressively may save cash once and cost goodwill for years.

A vendor who trusts your process is more valuable than a vendor you've squeezed for a few extra days.

Practical ways to manage outflows better

A service business doesn't need a treasury department to improve payables. It needs discipline.

Consider this operating rhythm:

- Review bills weekly, not randomly every day

- Pay by due date, not as soon as the bill lands unless there's a real reason

- Use business credit cards thoughtfully for expenses that fit the billing cycle and are paid off predictably

- Separate approval from payment so owners aren't releasing cash in the same moment they approve a charge

- Track recurring vendors to catch subscriptions and contractor patterns before they surprise you

The best payables system feels fair. Vendors know what to expect. You hold cash as long as terms allow. Nobody is guessing.

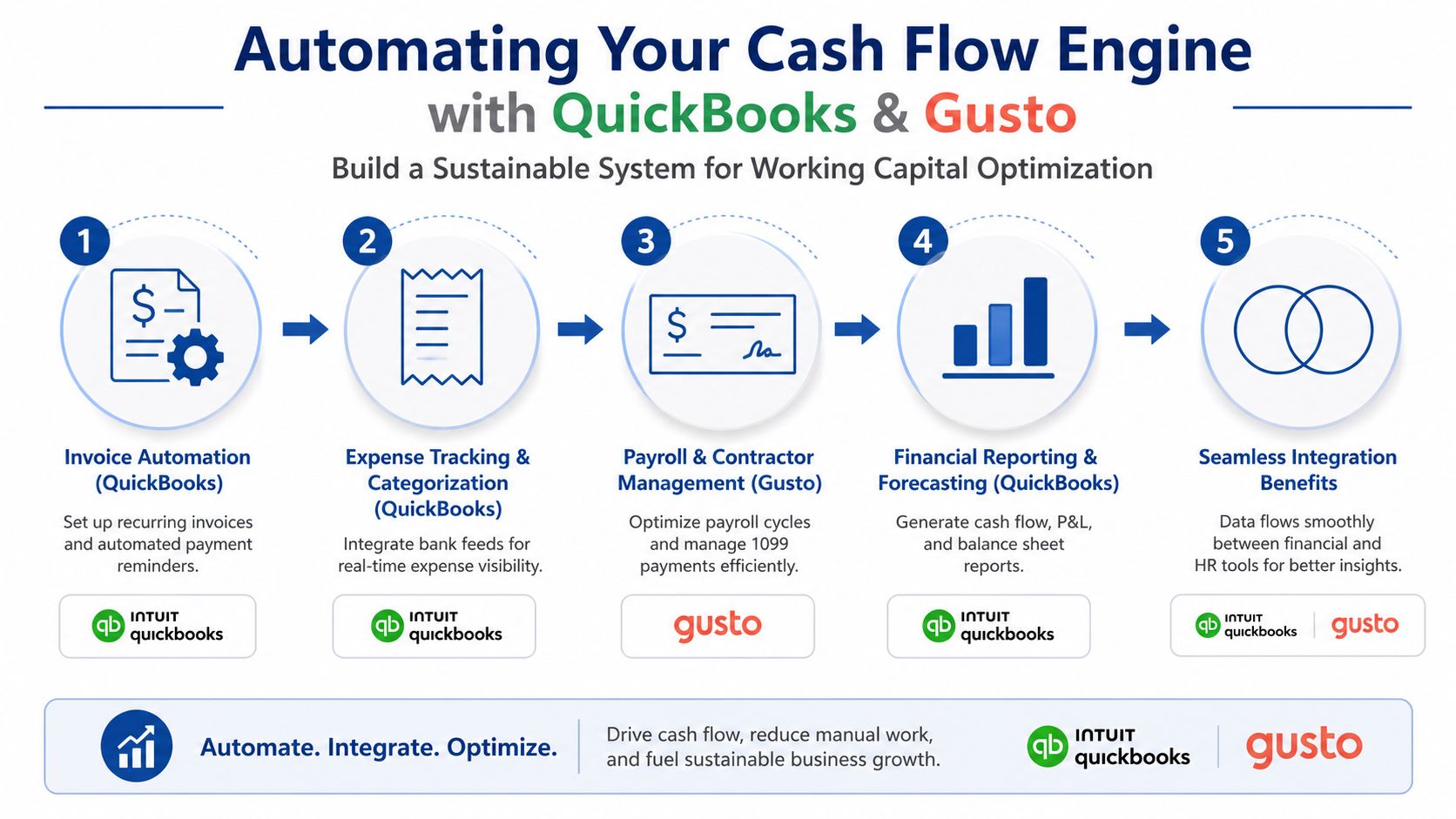

Building Your Optimization Engine in QuickBooks and Gusto

Working capital optimization sticks when it's built into the systems you already use. For many service businesses, that means QuickBooks Online for financial data and Gusto for payroll visibility.

Automation and forecasting improve decision-making. Bottomline on best-practice working capital management explains that strong programs are associated with automation and cash forecasting solutions that provide real-time variance analysis between forecasts and actual cash flow.

Set up the reports you should review every week

In QuickBooks Online, save a short list of reports so you're not rebuilding them each time.

A/R Aging Summary

Customize by customer and days past due. This becomes your collections dashboard.A/P Aging Summary

Use this to plan vendor payments based on due date, not inbox order.Statement of Cash Flows

This helps you see whether operations are producing cash.Profit and Loss by Month

Useful for spotting margin issues that can gradually worsen cash pressure.Balance Sheet

Review receivables, payables, and cash together. One report alone won't tell the story.

If you're still getting QuickBooks organized, this walkthrough on how to setup QuickBooks Online is a practical starting point.

Automate the parts that should never rely on memory

QuickBooks can remove a lot of friction if you configure it well.

- Recurring invoices for retainers and fixed-fee clients

- Automated payment reminders at set intervals before and after due dates

- Online payment options embedded in the invoice

- Bank feeds and expense categorization to keep reporting current

- Memorized report views so weekly review takes minutes, not an hour

The big benefit isn't convenience. It's consistency. Cash slips when billing and follow-up happen only when someone remembers.

Build a simple 13-week cash forecast

A rolling 13-week cash forecast is one of the most useful tools a service owner can maintain. It doesn't need to be fancy.

Create a spreadsheet with:

| Week | Starting cash | Expected collections | Payroll | Contractor payments | Vendor bills | Ending cash |

|---|

Export open invoices and due dates from QuickBooks. Then layer in known outflows.

Use Gusto to sharpen the payroll side of the forecast:

- upcoming payroll runs

- employer tax timing

- benefits deductions

- contractor payment dates if managed through payroll workflows

This gives you a forward-looking view that profit reports can't provide. You stop asking, “Are we profitable?” and start asking, “Will cash be tight three Fridays from now?”

Forecasting doesn't eliminate surprises. It turns surprise into lead time.

Compare forecast versus actual

The useful habit is not just making the forecast. It's comparing what you expected to what happened.

When you do that regularly, patterns appear:

- one client always pays later than promised

- payroll is heavier in certain periods

- software renewals bunch up

- contractor payments hit before project invoices are approved

Once you see those patterns, you can change terms, timing, or process. That's the engine. Not one heroic month of cleanup, but a repeatable system that keeps cash visible.

Measure Adjust and Win Creating a Culture of Cash Awareness

The last piece is cultural. Working capital optimization fails when the owner is the only person paying attention to cash timing.

Cash awareness doesn't mean everyone needs accounting training. It means the people affecting cash understand their role in it. Sales should know that weak contract terms create collection problems later. Project managers should know that unsigned change requests delay billing. Operations should know that rushed vendor approvals can pull cash out faster than planned.

Build a lightweight dashboard

Keep it simple and visible. A monthly dashboard can include:

- DSO trend

- DPO trend

- Cash conversion cycle trend

- Total overdue receivables

- Expected cash in the next few weeks

- Large vendor obligations coming due

You don't need dozens of KPIs. You need a few numbers the team can interpret quickly.

What to do when the numbers don't improve

If DSO isn't moving, don't just tell the team to collect harder. Trace the blockage.

Ask questions like these:

- are invoices going out immediately after work is completed

- are clients disputing line items

- is the wrong contact receiving invoices

- are account managers avoiding uncomfortable follow-up

- are your payment terms too loose for the kind of client you're serving

If DPO is too short, check whether bills are being paid from habit instead of schedule. If the forecast keeps missing, look at timing assumptions before blaming the model.

Tie operating behavior to cash outcomes

Through this, service firms acquire a significant advantage.

A few examples work well:

- give project leads visibility into unbilled work

- include invoice approval speed in client onboarding expectations

- tie part of sales accountability to whether the first invoice gets paid on time

- review past-due accounts in weekly operations meetings, not just finance meetings

That last point matters. Cash isn't only a bookkeeping issue. It's an operating discipline.

A similar idea shows up in revenue retention. If you're trying to understand whether client relationships are strengthening over time, it helps to also calculate NRR effectively. Retention quality and cash quality aren't the same thing, but they influence each other. Clients who renew, expand, and pay predictably are more valuable than clients who create constant collection drag.

The healthiest service businesses don't just watch revenue. They watch how fast revenue turns into cash.

Working capital optimization is ongoing. You measure, adjust, and keep the habits that shorten the delay between work performed and cash received. Do that well and the business gets steadier. Hiring gets less stressful. Growth decisions get clearer. And the bank balance starts reflecting the quality of the business you've already built.

If you want help turning this into a working system, Steingard Financial helps service businesses clean up their books, improve reporting, manage payroll, and build practical cash visibility in QuickBooks and Gusto so you can run with better data and fewer surprises.