The debtors turnover ratio measures how many times your business collects its average receivables during a period, using Net Credit Sales / Average Accounts Receivable. If your ratio is 8, that means you collect your average receivables about eight times per year, or roughly every 45 days.

If you run a service business, you've probably felt the disconnect. Revenue looks solid on your profit and loss statement. Your team is busy. Clients are being invoiced. But your bank balance still feels tighter than it should.

That gap usually comes down to timing. You've earned the revenue, but you haven't collected the cash yet. That's why understanding what is debtors turnover ratio matters so much. It helps you see whether your invoicing and collections process is turning work completed into cash you can use.

Why Your Revenue and Bank Balance Tell Different Stories

A service business can look profitable and still feel cash-starved.

You might have signed new clients, delivered projects, and sent invoices on time. On paper, the business is moving. In the bank, though, payroll, software, rent, contractors, and taxes don't wait for clients to pay. That's where many owners get frustrated. They assume the issue is profitability when the issue is often collections.

Revenue is not cash

Accounting records revenue when you earn it. Cash only shows up when the client pays.

If you send a large invoice today and the client pays next month, your income statement may look healthy now while your checking account stays flat. That delay is exactly what the debtors turnover ratio helps you evaluate. It tells you how efficiently your business is converting invoiced sales into collected cash.

Practical rule: If you regularly ask, “Why are sales up but cash still tight?” your receivables process deserves a closer look.

For a busy owner, this ratio isn't just an accounting term. It's a working-capital signal. It can help you spot whether the problem is slow-paying customers, loose payment terms, inconsistent billing, or a mismatch between how you bill and how clients prefer to pay.

Why service businesses feel this more sharply

Service firms often carry more collection risk than they realize.

A consultant may invoice after the work is done. An agency may bill monthly but wait on client approvals. An IT firm may bill by milestone, which means one delayed sign-off can hold up a meaningful invoice. If your costs are hitting every week but your collections arrive unevenly, cash flow gets lumpy fast.

This is why owners benefit from pairing their ratio analysis with straightforward reporting. A resource like Elyx AI for financial reporting can help clarify how profit and cash can move in different directions. And if you want to connect collections back to operating cash needs, this guide to cash flow calculation is a useful next step.

Understanding the Debtors Turnover Ratio Formula

The simplest way to think about the metric is this: how often do you empty the bucket of unpaid customer invoices?

The formal formula is straightforward.

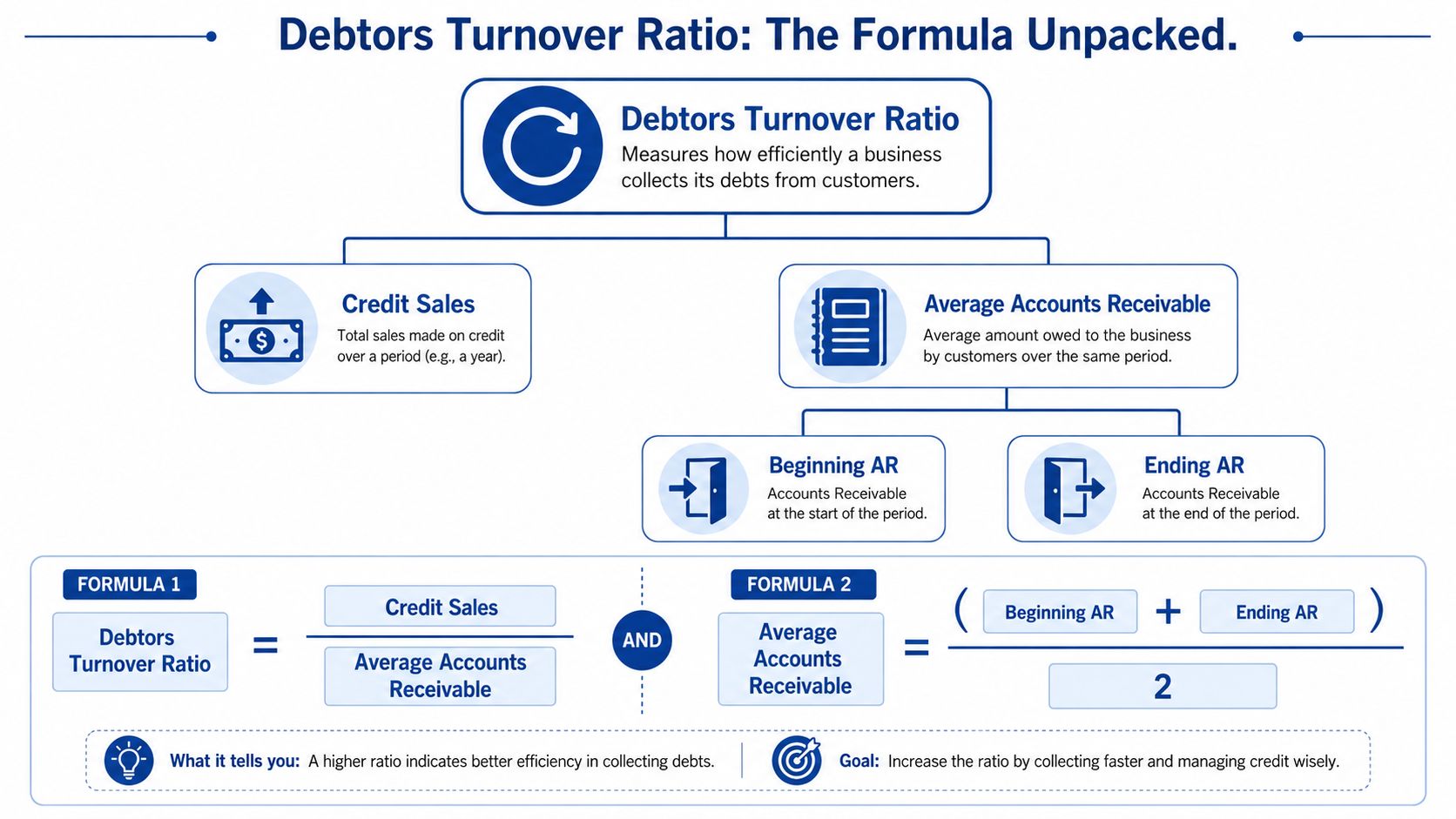

Debtors Turnover Ratio = Net Credit Sales / Average Accounts Receivable

What goes in the top number

Net credit sales means sales made on credit, not cash sales. It should also exclude returns and allowances, and both the numerator and denominator should cover the same accounting period, as explained by NetSuite in its overview of the accounts receivable turnover ratio.

That matters because owners often grab total revenue from the profit and loss statement and plug it into the formula. That shortcut can distort the ratio. If part of your revenue was collected immediately, it shouldn't be treated as receivables that still needed collection.

Here's a practical perspective:

- Include credit sales that created an invoice or receivable

- Exclude cash sales collected right away

- Back out returns or allowances so the sales figure reflects what you expect to collect

What goes in the bottom number

Average accounts receivable is usually the beginning AR balance plus the ending AR balance, divided by two.

That average matters because receivables move throughout the period. Looking at only one month-end balance can be misleading, especially in a business with uneven billing.

Here's the supporting formula:

Average Accounts Receivable = (Beginning AR + Ending AR) / 2

Turning the ratio into days

Many owners understand time faster than ratios. The debtors turnover ratio is often paired with days sales outstanding, or DSO. The standard formula is 365 / turnover ratio, according to Corporate Finance Institute's explanation of the accounts receivable turnover ratio.

That same source gives a useful benchmark for interpretation: a ratio of 8 means receivables are collected about eight times per year, or roughly every 45 days. If you think more naturally in terms of “how long does it take us to get paid,” DSO usually makes the result easier to grasp.

If you want a more operational look at the time side of receivables, this guide to accounts receivable days is a helpful companion.

A Worked Example for a Service Business

Let's make this practical with a simple service business example.

Assume a digital agency wants to understand whether collections are supporting its cash flow. The owner pulls three figures from the books for the same year:

- Net credit sales from the income statement

- Beginning accounts receivable from the balance sheet

- Ending accounts receivable from the balance sheet

Step one through step three

Start by identifying sales that were invoiced on credit. Don't use cash collected at the point of sale, and don't mix in anything outside the period you're analyzing.

Next, calculate average receivables:

Average AR = (Beginning AR + Ending AR) / 2

Then divide net credit sales by that average AR balance.

If the final number comes out high relative to the company's own history, that generally suggests invoices are converting to cash more quickly. If it comes out lower than prior periods, that can point to slower collections, longer terms, or delays in billing.

What owners usually miss

The math itself isn't hard. The main challenge is using clean inputs.

For service businesses, these problems come up all the time:

- Mixed billing types. Part of revenue may come from retainers, part from project invoices, and part from usage-based charges.

- Timing gaps. Work may be completed in one month but invoiced in the next.

- Deposit treatment. Upfront client payments may sit as deferred revenue rather than accounts receivable.

That's why a good AR review doesn't stop at one formula. It also checks the aging of open invoices. If you need that layer of detail, an accounts receivable aging report template can help you see which balances are current and which ones are drifting.

A simple calculation can tell you the pace of collection. The aging report tells you where the drag is coming from.

How to Interpret Your Turnover Ratio

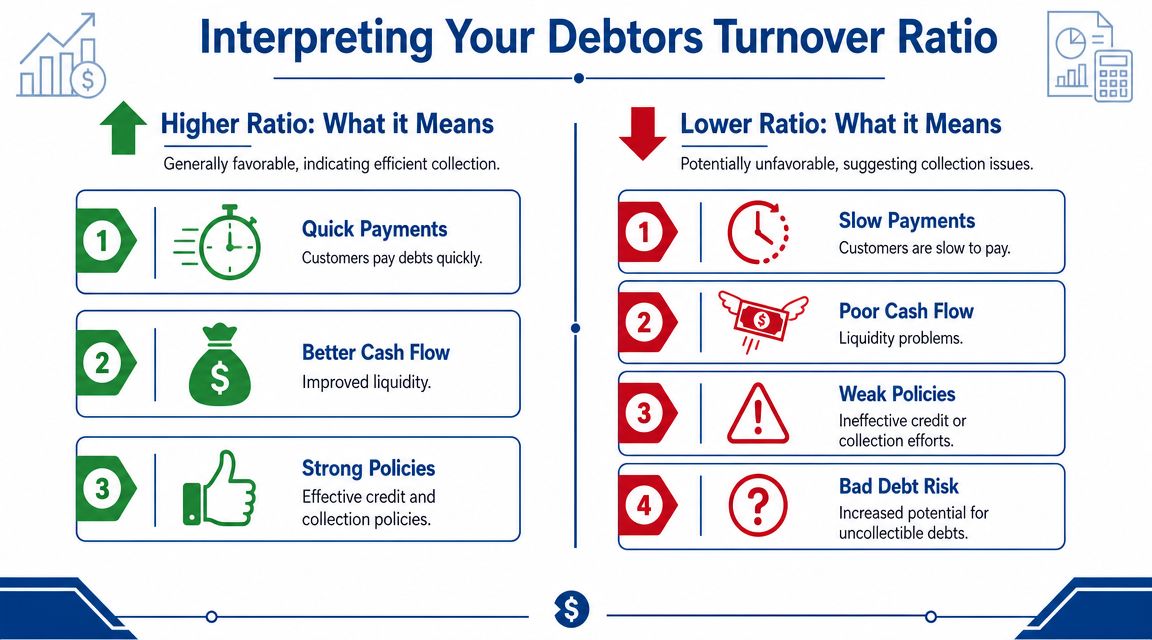

A ratio by itself doesn't make a decision for you. It gives you a signal.

In general, a higher debtors turnover ratio suggests faster collection, better cash conversion, and tighter control over receivables. A lower ratio can suggest slower-paying clients, loose follow-up, or terms that don't fit how the business operates.

Start with the time meaning

Most owners understand this metric better when it's translated into days.

If your turnover ratio rises, your DSO generally falls. That means clients are paying faster. If the ratio falls, DSO generally rises, which means cash is taking longer to arrive.

Here's the business interpretation:

| Result | What it often means for cash flow |

|---|---|

| Higher turnover | Cash comes in faster, which supports payroll, taxes, and operating expenses |

| Lower turnover | More cash stays tied up in receivables, which can create pressure even when sales look healthy |

A “good” number only matters in context. The better question is whether your collections are getting faster or slower over time.

Why service businesses need extra caution

Generic explanations often fall short.

For service businesses, interpreting the debtors turnover ratio requires care because timing can distort the picture. If invoices are tied to retainers, usage billing, progress billing, or large upfront deposits, the ratio can look artificially high or low depending on timing rather than true collection quality, as noted in Stackwealth's discussion of what is debtors turnover ratio.

A few examples make that clearer:

- Retainer model. If clients prepay at the start of the month, AR may stay low. The ratio can look strong even if profitability or delivery timing is under pressure.

- Milestone billing. If a major invoice goes out only after approval, receivables may suddenly spike. The ratio may weaken even though clients are paying according to contract.

- Subscription billing. If invoices are automated and charged quickly, turnover may improve because of billing design, not because collections staff changed anything.

What to review alongside the ratio

One number won't tell you the full story. Service owners should pair turnover with a few other views:

- DSO so you can translate the result into the average time to collect

- Deferred revenue so you can separate prepaid cash from true receivables

- AR aging so you can see whether the problem is broad or concentrated in a few late invoices

- Billing cycle analysis so you can tell whether the issue starts before collections, at invoice creation

If you rely only on the ratio, you might celebrate too early or worry unnecessarily. The useful question isn't “Is this number high or low?” It's “Does this number match how we bill, how clients pay, and how quickly cash should arrive?”

Limitations of the Debtors Turnover Ratio

The debtors turnover ratio is useful, but it's still an average. Averages hide things.

A healthy-looking number can conceal one large client who pays slowly every cycle. A weak-looking number can reflect billing timing rather than a collections problem. That's why the common rule “higher is better” needs some skepticism.

What the ratio doesn't show

The ratio won't tell you which invoices are overdue. It also won't tell you whether one customer represents too much of your receivables balance.

Those blind spots matter in service firms because a handful of clients often account for most revenue. If one account starts stretching payments, the ratio may not fully show the concentration risk until the cash strain is already visible.

Here are the main limitations:

- It compresses many customer behaviors into one average

- It doesn't identify the age of specific invoices

- It can be skewed by seasonality or uneven billing

- It may mislead in businesses with prepayments, deposits, or milestone billing

The ratio is a dashboard light, not the mechanic's report.

That's why experienced finance teams review turnover together with invoice aging, customer concentration, collections notes, and billing process details. The ratio helps you know where to look. It doesn't replace the deeper review.

Practical Strategies to Improve Your AR Turnover

If your ratio is weaker than it should be, the goal isn't to pressure every client harder. The goal is to remove friction from billing and payment.

Recent treasury guidance makes that point clearly: improving AR turnover is no longer just about chasing invoices. It also depends on how billing systems, payment methods, and follow-up automation are configured. Faster electronic settlement, customer payment portals, and automated receivables workflows can shorten collection cycles and improve working-capital metrics, according to J.P. Morgan's guidance on AR turnover and DSO.

Process changes that usually matter most

Some fixes are operational, not financial.

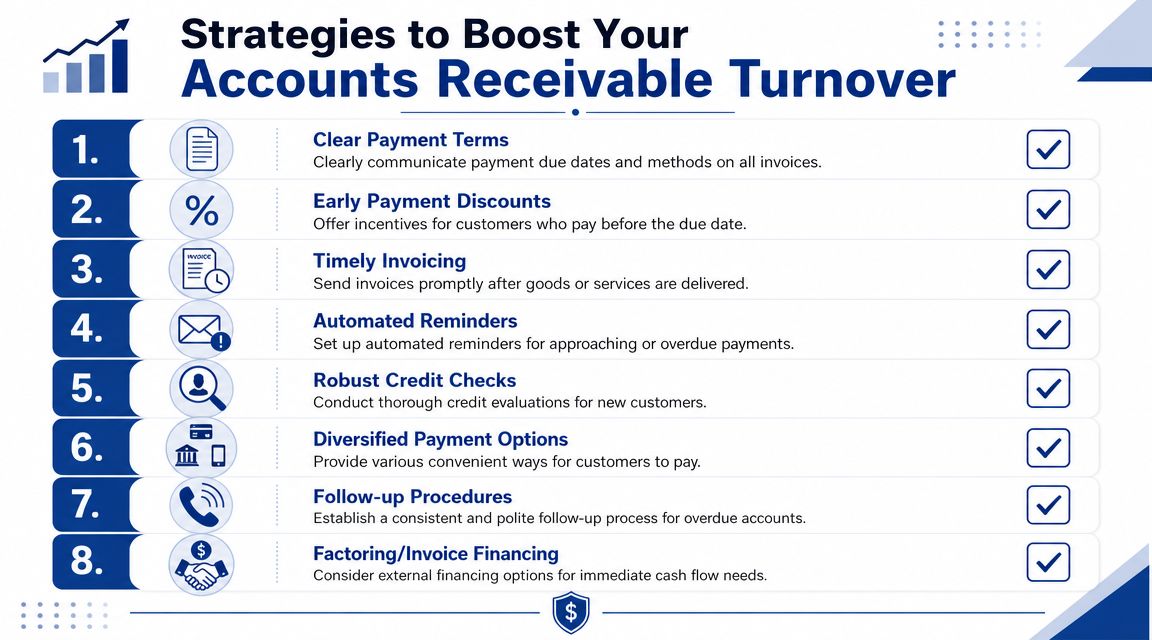

- Invoice faster. If work is done but the invoice sits in draft, collections haven't even started.

- Clean up payment terms. Clients should know exactly when payment is due and how to pay.

- Offer easier payment methods. Portals, card payments, and electronic transfers reduce delay.

- Automate reminders. A consistent follow-up sequence works better than ad hoc chasing.

- Review AR aging every week. Small delays are easier to fix than old balances.

For service businesses, billing design matters too. If milestone invoices depend on internal approvals, shorten that approval path. If retainers are standard, invoice before the service period starts. If recurring work is stable, automate recurring invoices in QuickBooks or your billing platform.

This short video gives a useful overview of AR turnover and how businesses think about improving it:

Strategy by business model

Different service models need different fixes.

| Service model | Useful AR improvement focus |

|---|---|

| Monthly retainers | Bill before the service month begins and store payment methods when appropriate |

| Project work | Tie invoice triggers to defined deliverables and approval deadlines |

| Hourly or usage billing | Reduce lag between time capture and invoice release |

| Managed services | Use recurring billing and client payment portals |

A broader review of accounts receivable best practices can help you turn those ideas into repeatable workflow changes.

The important point is simple. If you want a better debtors turnover ratio, improve the system that produces receivables in the first place. Clean invoices, clear terms, fast delivery, easy payment, and disciplined follow-up usually do more than last-minute collection pressure.

If your revenue looks healthy but cash still feels unpredictable, Steingard Financial can help you tighten the link between invoicing, receivables, and real cash flow. Their team works with service businesses to clean up books, improve reporting, manage AR processes, and give owners a clearer view of what the numbers mean before cash problems turn into operating problems.