When a business starts growing, bookkeeping usually breaks before the owner admits it. Revenue is coming in, invoices are going out, payroll is running, and the bank balance still feels like the main financial report. Then the friction shows up. Transactions sit uncategorized in QuickBooks. Reconciliations lag behind. Tax questions pile up. Nobody can answer a simple question like, “What did we earn last month?”

That's the point where bookkeeping stops being an admin task and starts affecting decisions. Hiring gets delayed because cash flow isn't clear. Pricing stays unchanged because margins aren't trusted. Tax season becomes a cleanup project instead of a filing process.

A lot of owners assume this is just part of growth. It isn't. Messy books are a systems problem, and systems can be fixed. The right fix usually isn't more owner effort. It's a CPA-led back office that can clean up the past, tighten the present, and give the business reliable numbers going forward.

Moving Beyond Financial Chaos

Most owners I talk with don't start by asking for “CPA bookkeeping services.” They ask for help with symptoms.

They say their books are behind. They don't trust the profit and loss statement. Their previous provider “did the basics,” but payroll entries don't tie out, credit cards weren't reconciled correctly, and year-end turns into a scramble to explain old transactions. The business may be selling well, but financially it still feels reactive.

That pattern is common because growth creates complexity faster than informal bookkeeping can handle. More customers means more invoices, more payment timing issues, more software subscriptions, more payroll changes, and more pressure to close the books on time. That's one reason demand for professional bookkeeping has expanded so quickly. The global bookkeeping services market is projected to grow at a 9.8% CAGR from 2023 to 2030, and the bookkeeping segment accounted for 43.2% of the global accounting services market in 2025, according to Cognitive Market Research's bookkeeping services market report.

The real shift happens when the owner stops treating bookkeeping as historical recordkeeping and starts treating it as management infrastructure.

Clean books don't just reduce stress. They change how quickly you can make a decision and how much confidence you have in it.

A CPA-led approach is built for that shift. It doesn't stop at categorizing transactions. It looks at whether the books support taxes, lender conversations, payroll accuracy, owner draws, accrual decisions, and monthly reporting that management can use.

If your current process depends on memory, inbox searches, and a burst of effort before tax deadlines, you don't need minor tweaks. You need a better financial operating system.

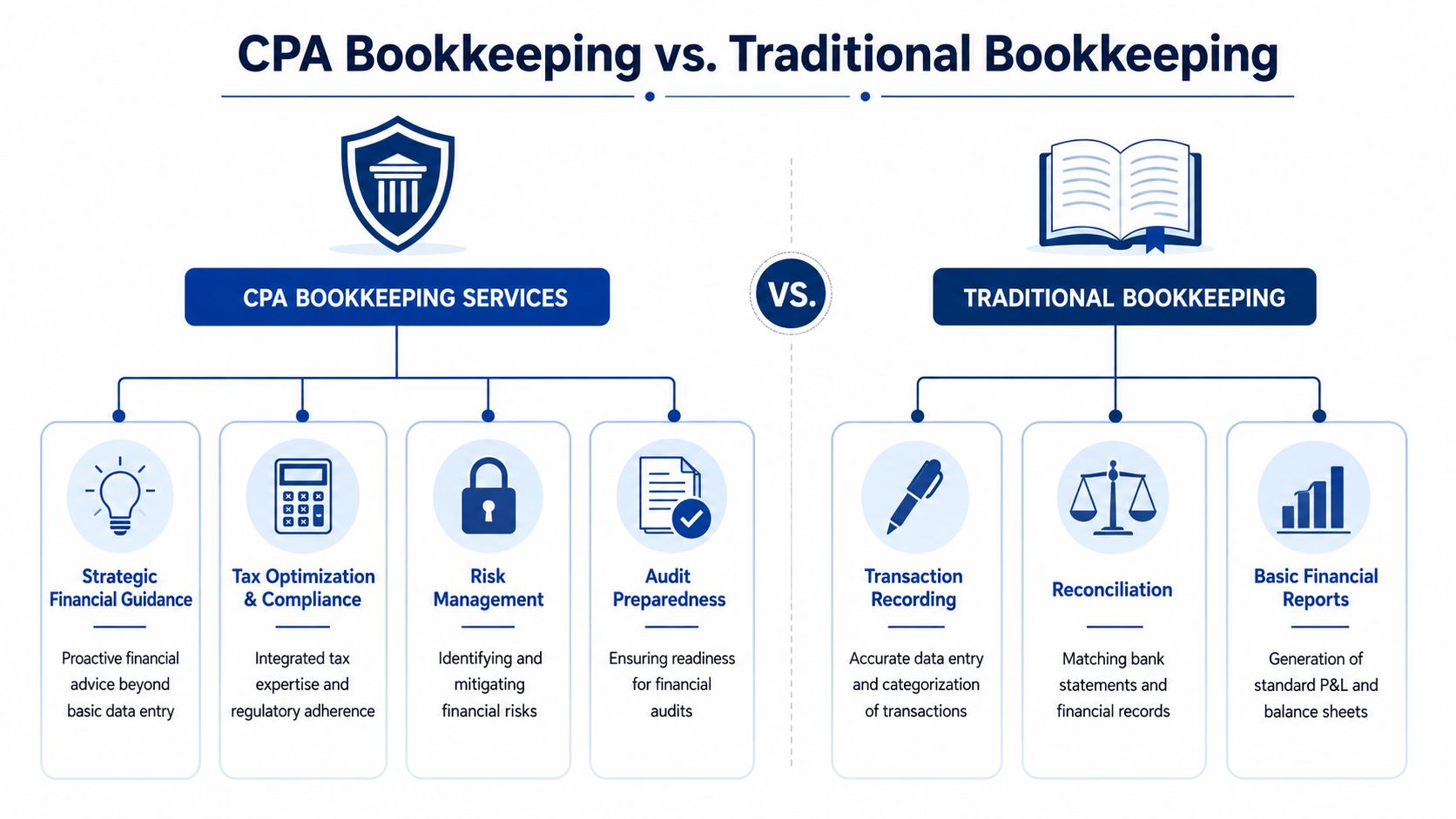

What CPA Bookkeeping Services Truly Are

A traditional bookkeeper records what happened. A CPA-led bookkeeping team records it correctly, reviews what it means, and keeps the business aligned with tax and reporting requirements while the year is still in motion.

That distinction matters.

The work goes beyond data entry

A good way to think about it is general care versus specialist care. Basic bookkeeping can keep a ledger moving. CPA bookkeeping services bring a higher level of review when the business needs financial statements, tax awareness, cleaner closes, and fewer compliance surprises.

According to Velan's explanation of CPA bookkeeping versus traditional bookkeeping, CPA bookkeeping services integrate transaction recording with advanced financial oversight, tax compliance, and strategic advisory. They also involve full financial statement packages and a compliance-first approach to GAAP procedures, which helps reduce audit risk.

In practice, that usually means the work includes:

- Transaction categorization with intent. Expenses aren't just posted somewhere plausible. They're coded in a way that supports reporting, tax treatment, and consistency month after month.

- Bank and credit card reconciliations. Not eventually. On a regular close schedule so missing items, duplicate charges, and stale balances don't sit unresolved.

- Accounts payable and receivable management. Bills need approval flow, timing discipline, and visibility. Receivables need follow-up, aging review, and clean customer-level records.

- Payroll integration. Payroll journals, tax payments, benefits, reimbursements, and owner compensation need to land correctly in the books.

- Month-end close and financial statements. A balance sheet, income statement, and cash flow statement only help if the underlying accounts are current and reviewed.

The CPA difference shows up in judgment

Many business owners face severe consequences. The books may look complete on the surface, but the accounting logic underneath is weak. Revenue may be recognized inconsistently. Loan balances may be off. Payroll liabilities may linger. Owner transactions may distort results.

A CPA team catches those issues earlier because it reviews bookkeeping through the lens of downstream consequences.

Practical rule: If your bookkeeping process can't support a lender packet, tax return prep, and management reporting without a last-minute cleanup, it isn't finished bookkeeping.

That's also why month-end work matters so much. If you want a useful reference on the mechanics behind cleaner closes, this guide to monthly accounting adjustments for businesses is worth reviewing. Adjustments are where a rough set of books starts becoming decision-grade financials.

The Strategic Benefits of a CPA-Led Back Office

The biggest benefit of CPA-led bookkeeping isn't that your books are “organized.” It's that the business can operate with fewer blind spots.

Modern companies create huge volumes of financial activity, even when they aren't large by headcount. In the United States, businesses generate over 400 billion invoices annually, and that figure climbs by 5% to 15% each year, according to this industry trend summary on accounting and bookkeeping demand. That level of transaction flow is exactly why casual bookkeeping breaks down. Owners need systems that can scale without losing visibility.

Better tax decisions during the year

Most tax problems don't start with the tax return. They start with poor bookkeeping in prior months.

When the books are current, a CPA can see patterns early. Maybe owner distributions need to be handled differently. Maybe payroll mix needs attention. Maybe expenses are being coded in a way that creates cleanup work later. Good bookkeeping turns tax planning into an ongoing process instead of a year-end scramble.

That doesn't mean every month becomes a tax strategy meeting. It means the underlying records are accurate enough for strategic conversations to happen when there's still time to act.

Stronger lender and investor readiness

Lenders and outside stakeholders don't just want financial statements. They want financial statements that hold together.

If receivables don't tie out, liabilities are stale, and the balance sheet is full of unexplained items, the issue isn't only presentation. It's credibility. CPA oversight improves the odds that your reporting package reflects actual business performance, not guesswork assembled from bank feeds.

For companies that need a higher level of financial decision support, a bookkeeping function often works best when paired with broader planning. That's where fractional CFO services can complement the back office by turning accurate books into budgeting, cash planning, and scenario analysis.

More confident operating decisions

The owners who benefit most from CPA bookkeeping are often not the ones with the most complicated tax returns. They're the ones trying to make frequent operating decisions.

Consider the kinds of questions that come up every month:

- Hiring questions. Can we afford another employee now, or do we need to wait?

- Pricing questions. Are margins improving, or are rising overhead costs hiding the truth?

- Cash timing questions. Is this a temporary dip, or a structural issue in collections and payment timing?

- Expansion questions. Can the current back office support another location, service line, or legal entity?

Timely reporting shortens the distance between what happened and what management does next.

That is where a CPA-led back office earns its value. It gives owners numbers they can use before the moment has passed.

Choosing Between a CPA Firm and a Bookkeeper

Not every business needs the same level of support. A solo operator with a simple service model may be fine with a traditional bookkeeper for a while. A business with payroll, multiple accounts, financing activity, or messy historical records usually needs more oversight.

The right question isn't “Which one is cheaper?” It's “Which one fits the current complexity of the business?”

CPA Firm vs. Traditional Bookkeeper Comparison

| Criterion | Traditional Bookkeeper | CPA Bookkeeping Firm |

|---|---|---|

| Scope of work | Day-to-day transaction entry, basic reconciliations, standard reports | Bookkeeping plus review, financial statement oversight, tax-aware treatment, and higher-level accounting judgment |

| Tax alignment | May prepare records for an outside tax preparer | Bookkeeping is handled with tax and compliance consequences in mind |

| Financial reporting | Often limited to standard software-generated reports | Reports are more likely to be reviewed, adjusted, and tied to management use |

| Complex issues | May struggle with payroll cleanup, loan accounting, accruals, or historical corrections | Better fit when the business has cleanup work, multi-step closes, or stakeholder reporting needs |

| Best fit | Early-stage business with low transaction complexity | Growing business that needs cleaner books, stronger controls, and better decision support |

| Communication style | Can be task-based and transactional | Often more structured around close process, review, and advisory context |

When a bookkeeper is enough

A traditional bookkeeper may be appropriate if the business has a narrow service offering, minimal monthly complexity, and an owner who's comfortable handling gray-area questions with a separate CPA at year-end.

That setup usually works only while operations remain simple.

When a CPA firm becomes the better choice

Once the business starts adding employees, carrying more liabilities, using financing, or needing reliable month-end reporting, a basic bookkeeping setup often stops being enough. The work needs more review, clearer processes, and someone who can tell the difference between a bookkeeping issue and an accounting issue.

If you're evaluating options, a practical starting point is to compare service models such as outsourced bookkeeping for small business. The main issue isn't outsourcing itself. It's whether the provider can handle both the daily detail and the financial judgment your business now requires.

Understanding CPA Bookkeeping Pricing and Engagement

Business owners often focus on price first because bookkeeping feels like a back-office function. That's understandable, but pricing structure tells you a lot about what the relationship will feel like after you sign.

The two most common models are hourly billing and fixed monthly subscription pricing.

The problem with hourly billing

Hourly billing sounds straightforward. You pay for time used. In practice, it can create the wrong incentives.

If every question, adjustment, and follow-up call starts a meter, owners tend to wait too long to ask questions. Small issues sit unresolved. Communication becomes narrower than it should be. The provider may complete assigned tasks, but the client still feels alone when decisions need context.

That frustration is reflected in buyer sentiment. Small business owners with CPAs charging by the hour often feel “underserved” if those professionals aren't “readily available,” and buyers increasingly value integrated, subscription-based services that combine compliance, advisory, and technology for real-time visibility and support, according to this discussion of hourly versus managed service expectations.

Why subscription pricing often works better

A fixed monthly arrangement tends to fit ongoing bookkeeping better because the work itself is ongoing. Transactions don't stop. Payroll doesn't stop. Reconciliations, closes, and financial reviews don't stop.

A managed monthly engagement usually works best when it includes a clear scope such as:

- Routine bookkeeping operations like categorization, reconciliations, and close support

- Scheduled reporting so the owner knows what arrives and when

- Defined communication channels for questions that come up during the month

- Technology oversight around QuickBooks Online, payroll systems, bill pay, and workflow tools

- Cleanup protocols when older periods need correction

If you're afraid to email your accountant because you might get billed for asking a simple question, the engagement model is working against you.

That doesn't mean every business should choose the same package. Some need only monthly close support. Others need bookkeeping, payroll coordination, and regular financial review. The key is predictability. You should know what's included, what triggers extra work, and who handles your account day to day.

The best pricing model is the one that supports accurate books, timely communication, and a process you'll use.

The Onboarding and Data Cleanup Process

Switching providers feels risky when the books are already messy. Many owners stay with a weak setup longer than they should because they assume the transition will be worse than the current pain.

A good onboarding process prevents that. It breaks the work into stages, assigns responsibility clearly, and fixes the books in a controlled order.

Discovery before changes

The first step should never be random recoding. A CPA-led team should review the current file, identify where reporting is unreliable, and determine what's merely incomplete versus what's wrong.

Common problem areas include uncleared bank accounts, duplicate transactions from feed sync issues, payroll entries posted inconsistently, loan balances that don't match statements, and balance sheet accounts carrying old items no one has explained in months.

A structured intake matters here. If you want a general operational reference, this Formzz client onboarding guide shows why documented onboarding steps reduce confusion and handoff errors.

Historical cleanup in the right order

Cleanup work has to be sequenced. Start with account access and source documents. Then tie out bank and credit card accounts. Then fix payroll and liability accounts. Then review revenue, expenses, loans, and owner transactions. Only after that should month-end statements be treated as reliable.

This is also the stage where a provider's technical discipline shows. At bookkeeping cleanup services, for example, the stated focus is on correcting historical books, reconciling accounts, and restoring usable reporting. That's the kind of defined cleanup scope owners should look for from any provider.

Building the ongoing system

Once the file is accurate, the next job is making sure it stays that way.

That usually means:

- Refining the chart of accounts so reports are useful, not cluttered.

- Connecting the tech stack correctly across QuickBooks Online, Gusto, bill pay tools, and banking feeds.

- Setting a close rhythm with recurring reconciliations, review points, and reporting dates.

- Defining who owns what between the business and the bookkeeping team.

The cleanup phase fixes old errors. The operating phase prevents them from coming back.

That's the primary goal of onboarding. Not just getting moved over, but ending up with a back office that can handle growth.

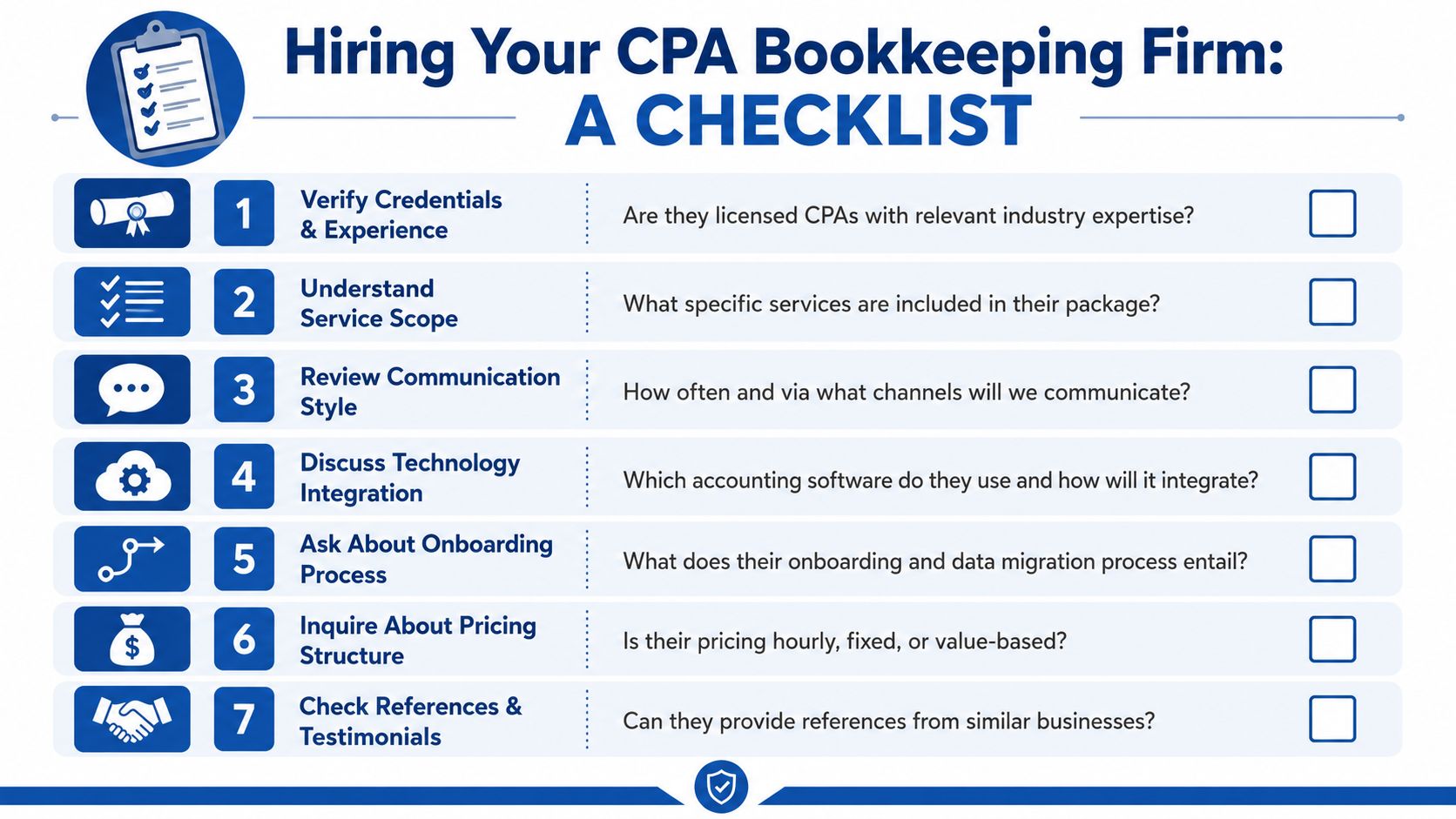

A Checklist for Hiring Your CPA Bookkeeping Firm

Hiring the right firm starts with better questions. Most bad engagements don't fail because the provider can't post transactions. They fail because the owner never got clear on staffing, review standards, deliverables, and communication.

A major issue to verify is who performs the work. A key vetting question is whether a CPA firm handles bookkeeping internally or outsources it to junior staff, especially because 74% of buyers are willing to pay more for firms that offer strategic advisory and data analytics, according to Greenwood CPA's discussion of signs you need CPA bookkeeping support. Those higher-value services depend on in-house expertise and real review capacity.

Questions worth asking in the first meeting

Use questions that reveal process, not just personality.

- Who will work on my account day to day. Ask for roles, not just titles. You want to know who categorizes transactions, who reviews reconciliations, and who answers accounting questions.

- What does your month-end close include. Listen for specific steps like reconciliations, review of uncategorized items, liability checks, and financial statement delivery.

- How do you handle cleanup work from prior periods. A solid firm should describe sequence and scope, not vague reassurance.

- What reports will I receive regularly. If they can't describe the reporting package clearly, expectations will drift later.

- How do you work with QuickBooks Online, Gusto, and related systems. Tool familiarity matters because bad integrations create bad books.

- What happens when something unusual comes up. Loan changes, owner transactions, payroll corrections, and tax notices shouldn't derail the process.

Red flags owners should take seriously

Some warning signs are easy to miss during sales conversations.

- Vague staffing answers. If you can't tell who does the work, assume turnover or outsourcing could become a problem.

- No sample workflow. A provider should be able to explain intake, close, review, and communication cadence.

- No clear service boundary. If everything is “custom,” nothing is defined.

- Weak industry understanding. Service businesses, agencies, consultants, and multi-entity operators often need different reporting logic.

- Technology resistance. Firms don't need every new app, but they should know how modern workflow supports accounting firms, and resources like platforms that support accounting firms can help owners understand what operational maturity looks like.

A short video can also help frame what to look for in a bookkeeping relationship before you commit.

The standard to hold a firm to

You're not hiring someone to “keep up with the books.” You're hiring a financial operator.

That means the firm should be able to tell you how it maintains quality, how it communicates, how it handles corrections, and how it keeps your books useful for management. If the answers sound improvised, keep looking.

If your books are behind, unreliable, or no longer supporting how the business operates, Steingard Financial is one option to evaluate. The firm works with service businesses on bookkeeping cleanup, ongoing bookkeeping, payroll coordination, and reporting processes designed to give owners clearer financial visibility and fewer operational headaches.