An arm's length transaction is a deal where both sides act independently and in their own self-interest, like two strangers negotiating in a market. In tax practice, that standard is embedded in a framework used in over 140 countries, which is why it matters far beyond big multinational companies.

If you run a service business, this comes up more often than most owners realize. You might bill a spouse's company, reimburse yourself for an expense, lend money to the business, or move work between related entities you control. Those situations feel ordinary operationally, but they can create tax, bookkeeping, and valuation problems if the price or terms don't look like what unrelated parties would accept.

Most confusion starts because the phrase sounds legal and abstract. It's not. The simplest way to define arm's length transaction is this: would this deal still make sense if the other side were a stranger and not someone connected to you?

What Is an Arm's Length Transaction

To illustrate, consider a common service-business situation. You own a consulting firm, and your brother asks you to handle strategy work for his startup. He says, “Bill me something light for now, and we'll sort it out later.”

That request feels normal in family life. In your books and tax records, it creates a different question. Would an unrelated client get that same price, payment timing, scope, and level of flexibility?

That is the heart of an arm's length transaction.

An arm's length transaction is a deal structured as if the parties were independent businesses meeting in the open market. Each side is protecting its own interests. Each side can push back, compare options, or walk away. The final terms should look like something two unrelated parties would accept.

A practical way to understand it is to use the stranger test. Replace the related party with someone you do not know. Then ask whether the same fee, contract terms, deadlines, and risk sharing would still make sense. If they would, you are closer to arm's length treatment.

Price is only part of the answer.

For U.S. service businesses, this point causes trouble because the value is often less visible than it is in a product sale. You are not handing over a pallet of inventory with an obvious market price. You may be selling expertise, retainer access, project management, software setup, ongoing support, or the use of your team's time. That makes it easier to undercharge, overcharge, or use loose terms that look harmless operationally but create tax, bookkeeping, and valuation problems later.

A good mental model is a normal client engagement with a new customer who found you through the market. You would define the scope, set a fee, choose payment terms, and spell out who is responsible for what. An arm's length deal should hold together that same way, even if the other side is your spouse's company, your holding company, or another business you own.

Practical rule: Fair market value is not just the number on the invoice. It also includes normal terms, clear responsibilities, payment expectations, and a level of risk that fits the work performed.

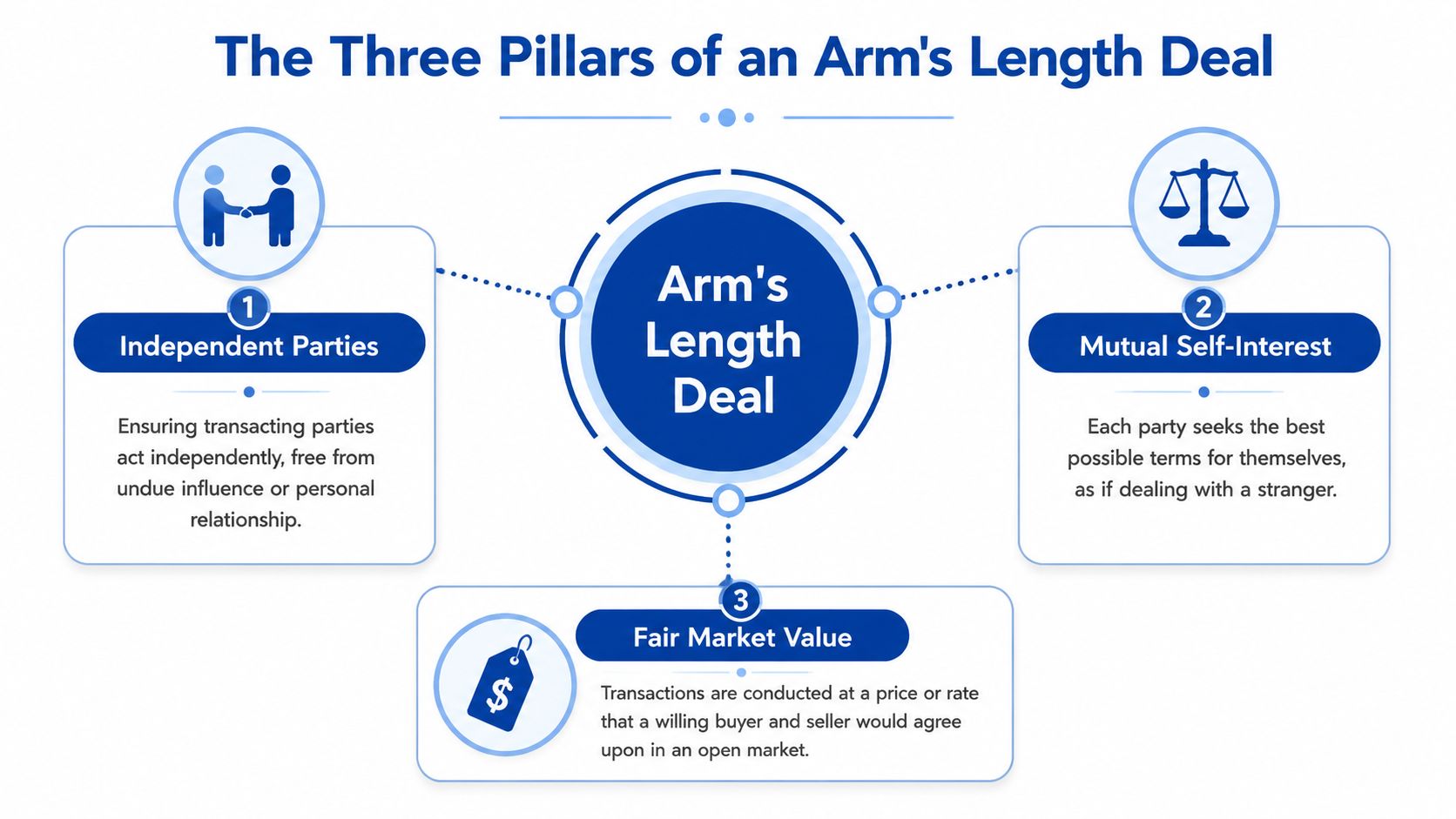

The Three Pillars of an Arm's Length Deal

The easiest way to understand this concept is to picture a used-car sale between two strangers. Neither side owes the other a favor. Each wants the best deal. The final price lands somewhere the market can support.

That same logic sits underneath an arm's length business transaction.

Related-party pricing is judged against this benchmark in transfer pricing. As noted by International TPS on transfer pricing, related-party prices should be set as if the parties were independent and negotiating in a competitive market, and that standard is applied in almost all countries under the arm's length principle.

Independent parties

Independence means the relationship itself doesn't drive the outcome.

If your agency hires a designer you found through a public proposal process, that starts from an independent footing. If you hire your cousin's studio because “we'll work out the money later,” independence is weaker from the start.

Independence doesn't require hostility. It requires separation. Each side should be free to say no, negotiate changes, and compare alternatives.

Mutual self-interest

In a real market, each party protects its own economics.

A buyer wants lower cost, cleaner terms, and less risk. A seller wants stronger pricing, faster payment, narrower scope, and less exposure. That tension is healthy. It often produces a believable result.

When self-interest disappears, arm's length credibility disappears with it. If one side accepts vague work scope, delayed payment, or a below-market fee just to help a friend or related company, the deal starts looking influenced rather than negotiated.

When terms feel unusually generous, ask why an unrelated party would ever accept them.

Fair market value

Often, many owners oversimplify the concept. Fair value doesn't always mean one exact number. It usually means a reasonable market-based result supported by comparable evidence.

For a service business, that evidence might include:

- Comparable client pricing: What you charge unrelated customers for similar work

- Outside quotes: Bids from other providers for similar scope

- Role-based rates: Internal support from salary cost, utilization, and margin expectations

- Scope and risk differences: Whether a project includes strategy, revisions, travel, supervision, or urgent turnaround

A common mistake is saying, “It's fair because we agreed to it.” Agreement alone isn't enough when the parties are related. The better question is whether the market would recognize the outcome as reasonable.

Why This Principle Matters for Your Business

Some owners hear “arm's length” and assume it's only for giant global corporations. That's too narrow. The principle matters anytime a relationship can distort price, timing, or terms.

The formal reason is tax. The arm's length standard is codified in Article 9 of the OECD Model Tax Convention, a framework used in over 140 countries to test whether internal prices reflect market reality rather than profit shifting, as summarized in this explanation of the arm's length transaction standard.

It affects IRS risk

For U.S. businesses, related-party pricing can attract attention because it changes taxable income. If one entity earns too little because it undercharged a related company, or if an owner takes unusual pricing on a personal or affiliated transaction, your books may stop reflecting ordinary business reality.

That doesn't mean every related-party deal is wrong. It means you need to show why the pricing and terms make sense.

If you already keep a year-end checklist, this is one more reason to tighten your process before filings and cleanups. A solid tax season preparation workflow helps you catch unusual owner payments, reimbursements, and related-company entries before they turn into bigger problems.

It affects your bookkeeping

A service business lives or dies by clean financial statements. If you discount work for a related party, skip invoices, absorb costs informally, or mix owner and company expenses, your profit and loss statement stops telling the truth.

That creates real operating problems:

- Pricing decisions get weaker: You may think a service line is profitable when you've subsidized it.

- Payroll planning gets distorted: Margin looks healthier or worse than it really is.

- Budgets become unreliable: Future forecasts sit on numbers that weren't market-based to begin with.

It affects valuation and lending

Buyers, lenders, and advisors want normalized earnings. They don't want books shaped by family pricing, casual intercompany charges, or undocumented owner arrangements.

A business can look less stable when revenue, expenses, or margins depend on special relationships rather than market behavior. That's especially true in service firms, where much of the value comes from repeatable pricing, dependable margins, and clean contracts.

Buyers don't just ask what you earned. They ask whether those earnings would hold up without related-party favors.

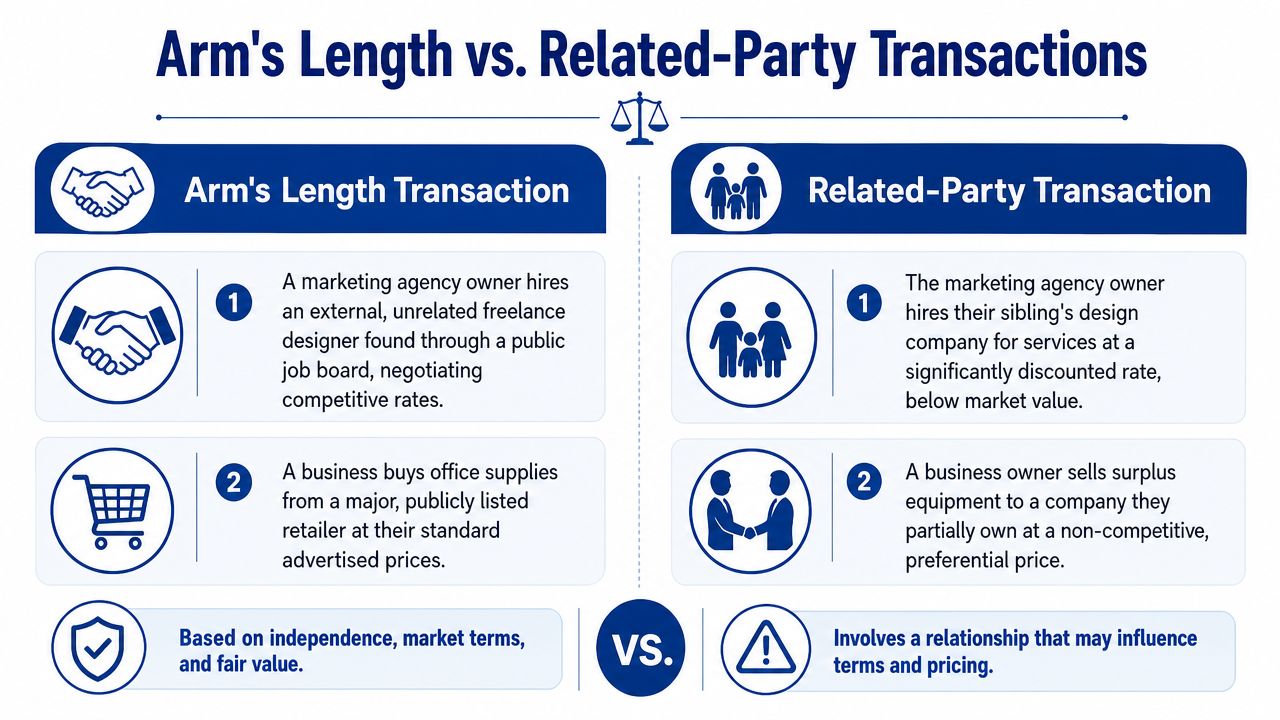

Arm's Length vs Related-Party Examples

Two transactions can involve the same service, the same team, and even the same price on paper, yet lead to very different tax and bookkeeping consequences. The difference is often the relationship behind the deal.

Example one with a spouse's startup

You run a marketing agency. Your spouse starts a software company and asks your agency to build the website, manage paid search, and produce monthly content. You charge a small amount, skip a formal scope, and send invoices only when cash is available.

That is a related-party transaction. It probably does not reflect an arm's length deal.

The easiest way to see why is to ask a practical question. Would you offer those exact terms to a stranger who found you through a referral? In most cases, no. A market client would usually get a proposal, a defined scope, revision limits, payment dates, and follow-up on overdue invoices. The family relationship changed the terms, so the transaction no longer looks like a regular market deal.

For a service business, this is not just a legal label. It affects revenue recognition, accounts receivable, owner distributions, and how believable your margins look later to the IRS, a lender, or a buyer.

A similar issue shows up with loans between connected parties. If money moves between an owner and the business, or between related companies, written terms matter. This overview of a promissory note gives helpful context for documenting repayment terms.

Example two with an unrelated client

Now use the same agency and nearly the same service package for a new client from your referral network. You send a proposal, define deliverables, discuss timing, agree on pricing, sign a contract, and invoice on your normal schedule.

That is much closer to an arm's length result.

The fee does not have to match every other client exactly. Service businesses rarely price that way. What matters is that the deal was shaped by a normal business process. Both sides had a reason to negotiate. Both sides could decline. Your file shows how the final number was reached, which is one reason good small business record-keeping practices matter so much in related-party situations.

Here's the side-by-side view:

| Transaction feature | Related-party version | Arm's length version |

|---|---|---|

| Relationship | Spouse's company | Unrelated client |

| Pricing basis | Favor or informal discount | Negotiated market-based fee |

| Documentation | Sparse or inconsistent | Proposal, contract, invoice trail |

| Payment terms | Flexible, undefined | Standard due dates and terms |

| Audit story | Hard to defend | Easier to explain |

One final point causes confusion for owners. A related-party transaction is not automatically improper. It becomes a problem when the price, terms, or documentation drift away from what independent parties would normally accept. That distinction matters a lot in U.S. service businesses, where the biggest risk often is not inventory or equipment valuation. It is informal billing, vague owner arrangements, and related-company charges that make the books harder to trust.

A short explainer may help if you want a visual walk-through of the concept:

How to Document and Demonstrate Fair Value

The best defense isn't a perfect memo written after the fact. It's a normal business file built while the transaction is happening.

The IRS says taxpayers must use the method that provides the “most reliable measure” of an arm's length result, often supported by comparability analysis and market data, with practice that can include an interquartile range and three-year average results, as outlined in the IRS international practice unit on arm's length analysis.

What to keep in the file

You don't need transfer-pricing jargon for every small business situation. You do need evidence.

- Signed agreements: Use a contract, statement of work, or service agreement that states scope, pricing, payment terms, and responsibilities.

- Comparable support: Keep outside quotes, prior client proposals, competitor pricing references, or internal pricing sheets that show how you arrived at the fee.

- Negotiation trail: Save emails, proposal revisions, and notes showing the price wasn't arbitrary.

- Clear invoices: Match invoices to the contract. If the scope changes, update the paperwork.

- Separate expense support: Reimbursements should have receipts, business purpose, and a clear policy or agreement behind them.

Common mistakes that cause trouble

Some patterns create headaches fast.

Watch for this: “We'll just book it as a reimbursement” is not a substitute for a documented agreement.

A few of the most common errors:

- Inconsistent pricing: Charging one rate to unrelated clients and a very different rate to a related company without a documented reason

- Missing contracts: Performing work first and trying to explain terms later

- Bundled services without support: Combining strategy, admin work, software, and management time into one vague number

- Owner-business blur: Paying personal costs through the company, or having the owner absorb business costs with no clear treatment

When lenders or buyers review your numbers, they often want to understand whether earnings are sustainable and market-based. If that's a live issue for you, these insights into SBA business valuation show why normalized financials and supportable pricing matter.

Good documentation also depends on routine discipline. A strong small business record-keeping system makes it easier to preserve contracts, receipts, invoice support, and related-party notes before details disappear.

Ensuring Your Books Are Audit-Ready

To define arm's length transaction in plain English, think “stranger pricing, stranger terms, stranger documentation.” That's the standard you're trying to approximate when a deal involves an owner, a family member, or another business you control.

For a U.S. service business, this isn't just tax vocabulary. It affects how revenue is recognized, how expenses are classified, how profit looks on paper, and how credible your books appear during diligence. If related-party activity is common in your business, internal review matters just as much as year-end cleanup.

That's why basic controls help. A practical system of approvals, documentation, and review makes unusual transactions easier to spot before they distort the books. Good internal controls for small business create that discipline.

When the records are clean, the story is clean. And when the story is clean, audits, loan reviews, and valuation conversations get much easier.

If you want help cleaning up related-party transactions, tightening documentation, and keeping your books accurate month after month, Steingard Financial can help you build a bookkeeping process that stands up to scrutiny and gives you numbers you can trust.