Your service business is finally throwing off consistent cash. You've cleaned up operations, payroll is stable, and now a landlord is raising the lease again or a broker is showing you a small office, warehouse, or mixed-use property that looks like a smart long-term move.

Many owners at this point shift from operating company decisions to investment decisions, and the math changes fast.

A real estate purchase can look sensible from the street and still be wrong on paper. Rent assumptions can be off. Debt can squeeze cash flow. Repairs can arrive at the wrong time. Tax benefits can help, but only if the model captures them correctly. Good financial modeling real estate work turns that uncertainty into an actual decision framework, especially when it connects to the systems you already use, like QuickBooks and Gusto.

Why Your Business Needs a Real Estate Financial Model

If you're buying your first property through your service business or alongside it, gut instinct isn't enough. You need a model that tells you what the property earns, what it costs, how it behaves under financing, and what happens when assumptions move against you.

Most owners already have part of the answer in their bookkeeping. QuickBooks shows how cash moves through the business. Gusto shows payroll and benefits. A real estate model becomes more useful when it pulls from those habits of clean recordkeeping instead of living as a one-time spreadsheet no one trusts six months later.

What the model needs to answer

A workable model should answer a short list of business questions:

- Can the property support itself: That means estimating property income, operating costs, and debt service without relying on vague optimism.

- What happens to business cash: Even a good asset can create strain if principal payments, tenant improvements, or payroll timing collide with seasonal swings in your operating company.

- How risky is the downside: A model should show what happens if rent growth disappoints, occupancy softens, or financing changes.

- Will the reporting stay usable after closing: If the model can't tie back to your chart of accounts, it usually gets ignored.

A clean model doesn't predict the future. It gives you a disciplined way to test decisions before real money is committed.

Why this matters for service business owners

Service businesses often enter real estate for practical reasons. You want control over occupancy costs. You want to stop renegotiating leases. You may want a property that supports operations and builds long-term equity at the same time.

That creates a hybrid decision. You're not underwriting like a full-time real estate fund. You're balancing an operating company, payroll obligations, tax reporting, and growth plans. That's why the model has to be grounded in systems you already understand.

If you're comparing template-driven underwriting with more automated workflows, tools like the PropLab AI underwriting tool can be useful for scenario testing, but they still depend on clean assumptions and clean books.

What works and what doesn't

What works is a model that starts simple and ties to actual records. What doesn't work is a spreadsheet full of broker language, hidden formulas, and assumptions nobody can trace.

A practical setup usually includes:

- An assumptions tab with every key input in one place.

- An operating forecast that mirrors how income and expenses are categorized.

- A financing section that separates operations from debt.

- A returns section that shows whether the deal clears your hurdle.

- A reporting bridge so budget versus actual can later flow from your books.

If your business already does rolling planning, the same discipline used in budgeting and forecasting for operating decisions should carry into property analysis. Real estate just adds more timing risk and more capital intensity.

Setting Up Your Model's Core Assumptions

Bad real estate models usually don't fail because Excel is complicated. They fail because the inputs are scattered, inconsistent, or copied from an email chain without structure.

The fix is simple. Build one assumptions tab and treat it like the control room for the entire workbook. Every major formula should point back to that tab.

Start with deal structure

At the top of the assumptions tab, place the items that define the transaction itself. Keep them grouped and clearly labeled.

Use sections such as:

- Purchase assumptions including price, closing costs, due diligence costs, and timing

- Capital structure including equity contribution, debt amount, interest rate, and amortization terms

- Operating assumptions including rent, reimbursements if applicable, vacancy treatment, and expense behavior

- Exit assumptions including hold period and sale logic

- Tax and accounting assumptions including depreciation treatment and entity structure notes

For development or heavy repositioning deals, a proper Sources and Uses table matters early. Successful development models begin with a Sources and Uses table that typically outlines 20-30% equity and 60-70% debt, with a 5-10% contingency, and failing to model contingencies correctly is a primary driver of the 22% average cost overrun seen in projects, according to this real estate financial modeling guide.

Separate fixed inputs from judgment calls

Not every input has the same reliability. Some numbers come from signed documents. Others come from your best current estimate. Don't mix them together.

A practical approach is to mark:

- Document-backed inputs such as lender quotes, tax bills, insurance quotes, and lease terms

- Historically informed inputs such as maintenance patterns pulled from prior books

- Judgment-based inputs such as rent growth, lease-up speed, and future repair timing

That distinction matters because assumptions with the weakest evidence are usually the ones that need the hardest stress test.

Practical rule: If changing one assumption requires hunting through multiple tabs, the model isn't ready.

Build for edits, not for elegance

Owners often ask for a “professional” model when what they really need is an editable one. Fancy formatting doesn't protect you from errors. Clear structure does.

Use a layout like this:

| Assumption group | What belongs there | Why it matters |

|---|---|---|

| Deal terms | Purchase date, basis, fees | Controls the initial cash outlay |

| Financing | Debt terms and payment setup | Drives debt service and lender risk |

| Operations | Income and expense drivers | Feeds the pro forma |

| Capital items | Repairs, replacements, improvements | Prevents false cash flow |

| Exit | Sale timing and sale assumptions | Determines terminal value and returns |

Pull the first draft from your existing systems

QuickBooks is often the best starting point for expense assumptions because it reflects how your business spends money. Gusto helps when payroll sits inside occupancy costs, building support staff, or shared administrative labor.

For a service business owner, this is the primary advantage. You're not building financial modeling real estate work from scratch. You're translating known bookkeeping patterns into property assumptions.

That's also why the assumptions tab shouldn't be crowded with formulas. Inputs belong there. Calculations belong elsewhere.

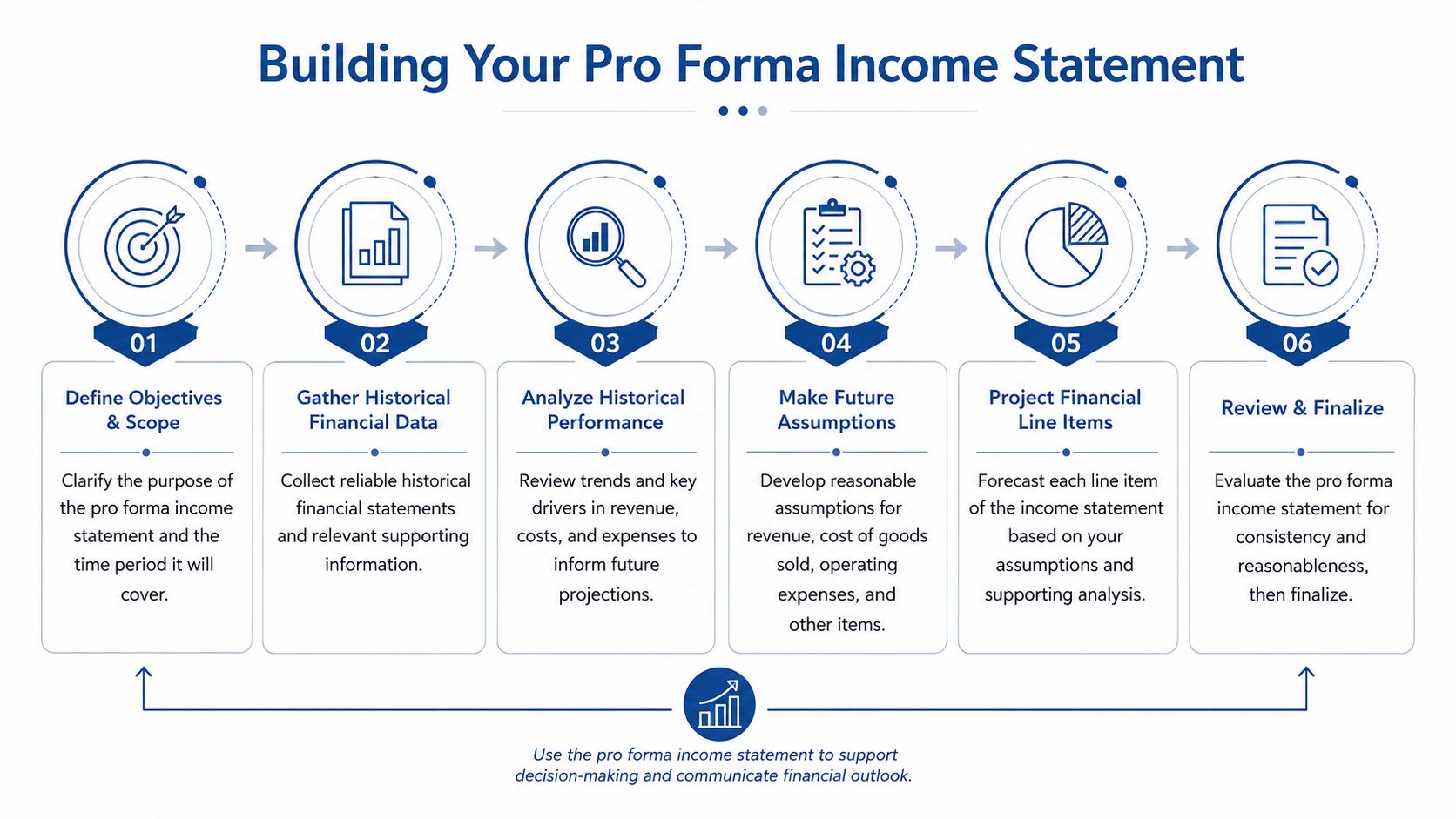

Building Your Pro Forma Income Statement

This is the part of the model that most owners recognize first. It looks like an income statement, but it's forward-looking. Done well, it becomes the operating engine for the rest of the analysis.

Build the pro forma from the top down. Start with income you could earn, subtract what you likely won't collect, then deduct operating expenses that belong to the property itself.

Start with revenue before realism kicks in

Begin with gross potential rent or total scheduled income. If the property has multiple tenants or mixed uses, break income streams apart rather than forcing them into one line. That keeps later updates cleaner.

After that, reduce income for vacancy and collection issues. Don't bury this inside a net number. Show it clearly so you can test it later.

If your property has less predictable income, especially short-term or seasonal components, it can help to review modern tools for property income forecasting as a reference point for structuring occupancy and rate assumptions, then adapt that thinking to your own model.

Use QuickBooks to build expense lines you can defend

The fastest way to make a bad pro forma is to guess at operating expenses in broad buckets. The better approach is to map actual bookkeeping categories into model line items.

Pull historical or analogous categories such as:

- Property taxes

- Insurance

- Repairs and maintenance

- Management fees

- Utilities

- Janitorial or site services

- Administrative overhead tied directly to the property

If the property will share overhead with your operating company, decide early whether you'll allocate those costs into the estate model or keep them outside as a separate business decision. Mixing the two midstream causes confusion.

Focus on NOI as the operating truth

Net Operating Income, or NOI, is the core output of the operating section. It measures what the property earns after operating expenses but before financing and taxes.

A clear example from Macabacus on real estate financial modeling shows the logic: a property with $1,200,000 in gross rent and $400,000 in operating expenses produces $800,000 of NOI. At a 6% cap rate, that implies a fair market value of $13.33 million.

That example matters because it shows why owners shouldn't jump straight to cash flow after debt. NOI isolates property performance first. Debt comes later. Taxes come later. If you don't trust NOI, nothing beneath it is reliable.

When I review first-time models, the most common issue isn't formula error. It's that owners mix property economics with owner-specific financing too early.

Keep your pro forma readable

A useful pro forma isn't just accurate. It's auditable. If someone else can't follow it, you'll stop trusting it yourself.

A simple structure often works best:

| Pro forma section | Purpose |

|---|---|

| Gross potential income | Shows full earning capacity before loss assumptions |

| Vacancy and credit loss | Makes collection risk visible |

| Effective gross income | Establishes usable operating revenue |

| Operating expenses | Captures recurring property costs |

| NOI | Measures property-level profitability |

What belongs here and what doesn't

Keep these items out of NOI:

- Loan payments

- Depreciation

- Income taxes

- Major capital improvements

- Owner distributions

Those belong later in the model. The pro forma should answer one clean question: how does the property operate on its own merits?

For first-time buyers, that separation is often the difference between a model that supports a real decision and one that just rationalizes a purchase.

Layering in Financing, CapEx, and Depreciation

A property can produce solid operating income and still disappoint the owner because financing, capital spending, and tax treatment weren't modeled correctly. As a result, many first-time investors discover that NOI is only the midpoint, not the finish line.

Debt service changes the timing of cash available to you. Capital expenditures absorb cash without showing up as ordinary operating expense. Depreciation reduces taxable income without using cash in the period. Each one matters for a different reason, so they should stay separate in the workbook.

Debt needs its own schedule

Don't hardcode annual debt payments into one line. Build an amortization schedule that separates principal and interest. In Excel, PPMT and IPMT are useful for this because they let you model each payment period cleanly.

Interest affects your income statement and cash flow differently than principal. Principal is balance sheet movement. Interest is financing cost. If you combine them, your analysis gets blurry fast.

Below is a simple illustration of how a loan schedule is organized.

| Year | Beginning Balance | Total Payment | Interest Paid | Principal Paid | Ending Balance |

|---|---|---|---|---|---|

| 1 | $1,000,000 | $71,946 | $59,677 | $12,269 | $987,731 |

| 2 | $987,731 | $71,946 | $58,932 | $13,014 | $974,717 |

| 3 | $974,717 | $71,946 | $58,142 | $13,804 | $960,913 |

| 4 | $960,913 | $71,946 | $57,304 | $14,642 | $946,271 |

| 5 | $946,271 | $71,946 | $56,415 | $15,531 | $930,740 |

That table is labeled as an example schedule format. In your actual model, the payment timing, compounding, and loan structure need to match the lender term sheet.

CapEx is not OpEx

This distinction sounds basic, but it causes repeated problems. Operating expenses keep the property running in the ordinary course. Capital expenditures improve, replace, or extend the life of the asset.

Examples of CapEx often include:

- Roof replacement

- HVAC replacement

- Major parking lot work

- Tenant improvement packages

- Large building systems upgrades

These costs should usually sit below NOI because they aren't part of recurring property operations in the same way as taxes, insurance, or regular repairs.

If you want a clean accounting framework for this distinction, it helps to review how capital spending is calculated and categorized. The accounting treatment needs to match the logic in the model.

A model that pushes major replacements into routine maintenance often makes a deal look safer than it is.

Depreciation helps, but don't let it hide cash needs

Depreciation is a non-cash expense. That means it can reduce taxable income while not reducing current-period cash in the same way that repairs, payroll, or debt service do.

For owner-users and service businesses, this matters because tax savings can make the investment more attractive, but depreciation does not fund a roof replacement or a lender payment. Keep the tax view and the cash view separate.

Bring payroll into the right place

Some properties require dedicated labor. That may be a building manager, maintenance support, front desk coverage, or shared administrative time. If those costs exist, pull them from your payroll system rather than guessing.

Gusto data is especially useful when you need to identify:

- Wages tied to property operations

- Payroll taxes

- Benefits costs

- Recurring staffing patterns

If labor is shared between the business and the property, document the allocation method. Even a rough but consistent method is better than a hidden assumption.

Calculating Returns and Running Sensitivity Analysis

After the model incorporates property operations, debt, capital spending, and sale assumptions, you can ask the fundamental question. Does this investment justify the risk and the use of your cash?

At this point, many owners look only at annual cash flow. That's too narrow. Real estate returns depend on timing, financing, and exit proceeds, not just one year's surplus.

The return metrics that matter most

For most owner-investors, three outputs deserve attention:

- Cash-on-cash return shows current annual cash yield on the equity invested.

- NPV helps compare projected cash flows against a required return.

- IRR captures the annualized return while accounting for timing.

IRR is usually the most useful summary metric when the cash flow profile changes over time. According to this guide to real estate return metrics, investors often target 15-25% IRR for equity, and the 2022-2023 interest rate hikes compressed typical IRRs by 300-500 basis points. The same source notes that a 1% rate change can impact IRR by 2-4%.

For real-world deal timing, XIRR is usually better than plain IRR because contribution dates, refinance events, and sale timing rarely land in perfect annual periods.

Sensitivity analysis is where the decision gets honest

A single output is not a decision. It's a snapshot. Sensitivity analysis shows what happens when the assumptions move.

The most useful tests for a first property purchase usually include:

| Variable | Why test it |

|---|---|

| Interest rate | Debt cost can change quickly and alter levered returns |

| Vacancy or occupancy | Small collection changes can pressure NOI |

| Exit assumptions | Sale value often drives a large share of total return |

| Expense pressure | Insurance, labor, and maintenance rarely move in a straight line |

Many business owners use this stage to shift from “this deal looks good” to “this deal only works under one narrow set of assumptions.” That's valuable. A model that kills a weak deal early saves more than one that makes a marginal deal look elegant.

If the deal only works when every assumption cooperates, it doesn't really work.

AI can speed up the testing, not replace judgment

Manual sensitivity tables still work. They're easy to audit and easy to explain. But newer tools can speed up scenario generation, especially when you're testing combinations rather than one variable at a time.

If you want a simple primer on how this style of analysis is framed in property finance workflows, Domus property finance tools offer a useful reference point.

The key is discipline. AI can help run more scenarios, but it cannot fix weak inputs, inconsistent bookkeeping, or a model that mixes CapEx, debt, and operating costs in the wrong places.

What a good decision looks like

A good investment is not necessarily the one with the highest headline IRR. For a service business owner, the better deal may be the one that:

- creates predictable occupancy cost,

- doesn't strain working capital,

- survives tougher assumptions,

- and still aligns with your operating plans.

That's why financial modeling real estate decisions should be judged in context. You're not only buying an asset. You're deciding how much uncertainty your business can absorb.

Common Modeling Pitfalls and QuickBooks Integration

Most bad models don't fail because the math is advanced. They fail because the workflow breaks. Inputs aren't updated, categories don't match the books, and actual results can't be compared to the forecast.

That's why the final step isn't more Excel. It's operational integration.

The mistakes that distort the answer

Some errors are technical. Others are judgment errors disguised as spreadsheet work.

Watch for these issues:

- CapEx buried in operating expenses. This depresses NOI in one place and understates future capital planning in another.

- Transaction costs omitted from the initial investment. Returns then look cleaner than reality.

- Overly smooth assumptions. Real costs and occupancy don't move in straight lines.

- Shared business expenses allocated inconsistently. That makes budget versus actual reporting unreliable.

- No version control. Owners end up debating which file is current instead of discussing the deal.

The model should also reflect how you'll monitor the property after closing. If the forecast and books use different category structures, your reporting loses value immediately.

Mirror the model inside QuickBooks

The easiest way to keep a model alive is to align your chart of accounts with the pro forma structure. That doesn't mean turning QuickBooks into a real estate software platform. It means using enough discipline that budget-to-actual comparisons can be produced without rebuilding reports by hand.

A practical checklist:

- Match major expense categories between the model and the chart of accounts.

- Separate repairs from capitalizable improvements so operating reports remain clean.

- Use classes, locations, or consistent account groupings if the property and service business share one file.

- Track payroll-related occupancy costs clearly when labor supports the property.

- Reconcile monthly so model updates use closed numbers, not guesswork.

If your file structure needs work first, a clean setup process for QuickBooks Online configuration and account structure makes later property reporting much easier.

AI makes clean books more valuable

Post-2025, AI-driven sensitivity analysis is emerging as a more practical layer for owner-operators. According to Adventures in CRE's modeling best practices discussion, growing firms can use clean payroll data from Gusto and expense data from QuickBooks to feed AI tools that model nuanced risks, including how a 4.5% rise in local labor costs could affect NOI and reduce IRR by 200 bps.

That trend is useful, but only after the bookkeeping foundation is right. AI can test scenarios. It can't clean a chart of accounts that mixes rent, repairs, and tenant improvements in one bucket.

The better your books map to the model, the faster you can move from underwriting to actual asset management.

Turn the model into a living report

A one-time acquisition model has limited value. A living model gets updated with actuals, revised assumptions, and current debt balances. That's where the ultimate payoff comes from.

For service business owners, this creates one operating habit across both sides of the business. Your company already reviews payroll, expenses, and cash flow. The property should sit inside that same reporting discipline, not outside it.

Frequently Asked Questions About Real Estate Modeling

What's the difference between a pro forma and a budget

A pro forma is investment-oriented. It forecasts how the property might perform over a longer hold period and supports valuation, financing, and return analysis. A budget is operational. It manages the next reporting cycle and compares expected results to actual bookkeeping activity.

How often should I update the model

Update it when there's a meaningful event. That usually means after monthly close, after major capital spending decisions, after financing changes, or when leasing assumptions change. The model stays useful when it reflects current facts, not last quarter's guess.

Should I use a template or build my own

Start with a template if it saves time, but don't rely on one you can't audit. A useful model has clear inputs, transparent formulas, and categories that match your books. If you can't explain how a line flows from assumption to output, the template is too opaque.

Do I need QuickBooks and Gusto data in the model

Not always directly, but the model should align with those systems. QuickBooks gives you expense structure and actual reporting. Gusto helps when payroll is part of occupancy or building operations. Without that connection, updates become manual and error-prone.

If you're buying a property, building a model, or trying to make your QuickBooks and payroll data usable for better investment decisions, Steingard Financial can help you clean the books, structure reporting, and create a back office that supports real analysis instead of spreadsheet guesswork.