Mastering Financial Reporting for Small Business

You check your bank balance on Monday, see money in the account, and assume the month is going fine. By Thursday, payroll hits, two clients are late paying, a software renewal clears, and suddenly your “we're okay” feeling turns into stress.

That's a common place for service business owners to operate from. You're busy delivering work, managing staff, sending proposals, and keeping clients happy. The bank balance becomes your shortcut. The problem is that your bank account only shows cash at one moment. It doesn't tell you whether your pricing works, whether your receivables are slipping, or whether your next hiring decision is safe.

That's where financial reporting for small business stops being an accounting chore and starts becoming a management tool. Good reports help you answer practical questions: Which service lines make money? Are late-paying clients squeezing cash flow? Can you afford to add another employee? Are you ready to show a lender numbers you can stand behind?

That last point matters more than many owners realize. Accurate financial reports are critical for accessing capital. 40% of firms under $500,000 in revenue cite interest rates and debt repayment as top challenges, and polished reporting such as cash flow forecasts can directly affect loan approval success, especially as policy proposals continue focusing on underserved entrepreneurs, according to Third Way's report on unlocking capital for underserved businesses.

If you're also trying to make sense of bookkeeping and tax responsibilities beyond the U.S., this comprehensive UK accounting guide for small businesses is a useful companion because it shows how the same reporting habits support compliance and decision-making in another market.

Why Financial Reports Are Your Business Compass

A service business usually sells time, expertise, and trust. That makes financial blind spots easy to miss. You can stay busy every day and still underprice your work, overhire too early, or carry too many overdue invoices.

Think about a marketing agency owner deciding whether to hire an account manager. The calendar is full, the team feels stretched, and revenue looks solid from the bank feed. But the decision is incomplete without reports. If several large invoices haven't been collected yet, or if payroll already absorbs too much of monthly revenue, that hire may create pressure instead of relief.

What the bank balance hides

Your bank balance can't separate these three realities:

- Profitability: Are your services priced well enough after wages, software, contractors, and overhead?

- Timing: Are clients paying fast enough to cover payroll and other near-term obligations?

- Trend: Are things improving, flattening, or slipping over the last few months?

That's why I call reports your compass. A compass doesn't do the walking for you. It gives you direction you can trust.

Practical rule: If you're making pricing, hiring, or borrowing decisions from the bank balance alone, you're managing with a flashlight when you need a dashboard.

What good reporting changes

When financial reporting for small business is set up well, the conversation changes. Instead of saying, “I think we're doing okay,” you can say, “Our design retainer work is carrying margin, project work is uneven, receivables are stretching, and cash will be tight if we don't speed up collections.”

That level of clarity helps with everyday choices and bigger ones. You can decide when to raise rates, which clients deserve follow-up, whether to shift staff utilization, and whether you're ready to talk to a bank or community lender.

For a busy service owner, that's the true value. Reports don't just describe the past. They help you avoid expensive guesses.

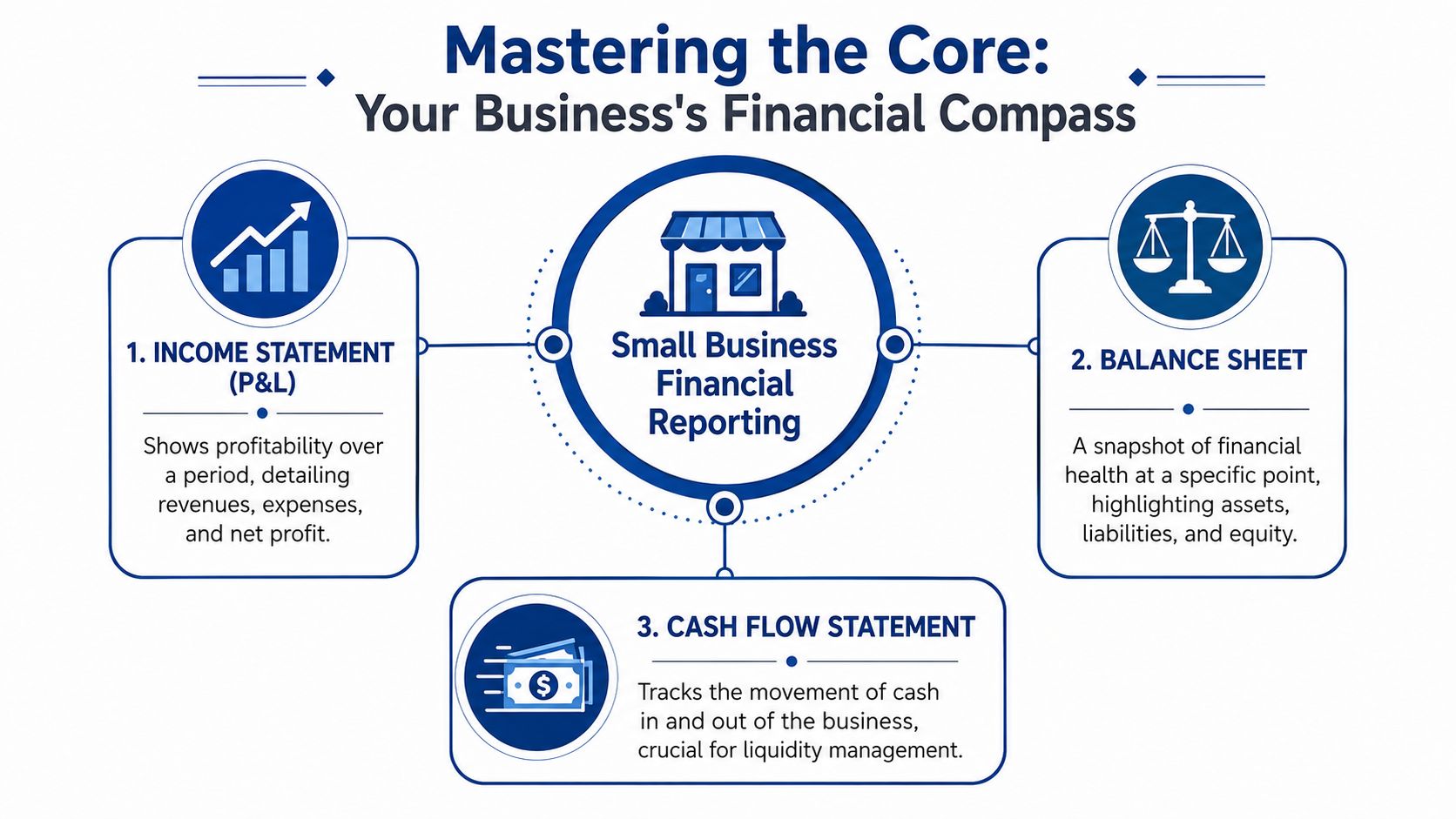

The Three Core Financial Reports You Must Master

Most financial reporting for small business comes back to three reports. If you understand these, you can read your business with much more confidence.

Here's the visual big picture.

Income statement

The income statement, often called the profit and loss statement or P&L, is your business's report card for a period of time. It shows revenue, expenses, and what's left over as profit or loss.

For a service company, this is usually the first report to review every month. It helps you see whether your work is producing enough gross profit to cover overhead and leave a healthy net result.

A plain-language example helps. If your firm billed clients for monthly retainers and one-off projects during April, your P&L gathers that April activity into one picture. It then subtracts payroll, contractor costs, software, rent, insurance, and other expenses. What remains tells you whether April was operationally strong or weak.

Balance sheet

The balance sheet is a snapshot taken on a specific date. It shows what the business owns, what it owes, and the owner's equity. In simple terms, it answers: what shape is the company in right now?

This report often confuses owners because it doesn't feel as intuitive as the P&L. The easiest way to read it is as a health snapshot:

| Part | What it means | Service business example |

|---|---|---|

| Assets | What the business has | Cash, accounts receivable, prepaid software |

| Liabilities | What the business owes | Credit cards, payroll liabilities, loans |

| Equity | The owner's stake | Retained earnings and owner contributions |

If your P&L says you're profitable but your balance sheet shows growing liabilities and weak cash, that tension deserves attention.

For a deeper walkthrough of how these statements fit together, this practical guide to preparing financial statements is worth keeping handy.

Cash flow statement

The cash flow statement tells the story of your cash. It shows where cash came from and where it went. That's different from profit.

A service business can post a profit on the P&L and still feel squeezed because invoices haven't been paid yet, owner draws were high, or debt payments pulled cash out of the business.

According to Reach Reporting's guide to financial reporting by business size, the income statement, balance sheet, and cash flow statement are the three essential pillars of financial health, and small businesses that neglect regular cash flow reporting are 2.5 times more likely to face unexpected liquidity crises within 12 months.

That's why I tell owners to stop asking only, “Did we make money?” and start asking, “Did cash move the way we expected?”

Later, if your business has contracts, deferred revenue, or more specialized billing logic, a narrower topic like this guide for SaaS revenue recognition can help you understand why booking revenue and collecting cash aren't always the same thing.

A short walkthrough can help reinforce the concepts:

A practical review rhythm

You don't need to stare at every report every day. A simple cadence works well for most service businesses:

- Monthly P&L review: Check revenue, direct labor, overhead, and net income.

- Monthly cash flow review: Watch collections, payroll timing, and cash pressure points.

- Quarterly balance sheet review: Confirm receivables, liabilities, loans, and equity all make sense.

A useful test is simple. If someone asked how your business performed last month, could you answer without opening your bank app?

Essential Reports for Modern Service Businesses

The big three matter to every company. Service firms need a few supporting reports even more urgently because the business runs on labor, billing, and collection speed.

A plumber, design studio, law practice, consultancy, or therapy group can all look profitable on paper while struggling operationally for the same reason: they earn revenue through people's time, then wait to collect it.

Accounts receivable aging

Your A/R aging report is your client payment scorecard. It shows which invoices are current and which are drifting into overdue buckets.

In QuickBooks Online, this report gives you a fast answer to a practical question: who owes you money, and how late are they? That matters because old receivables can, over time, become a cash flow problem and a client management problem at the same time.

Watch for patterns like these:

- One chronically late client: You may need stricter terms, deposits, or autopay.

- Many invoices aging at once: Your billing process may be delayed or inconsistent.

- Large old balances: Revenue may look stronger than actual cash reality.

For service businesses, this report often matters more than owners expect. If your team delivers the work quickly but billing goes out late, or invoices go unpaid without follow-up, your reporting is already warning you.

Payroll reports

Payroll is often the biggest cost in a service business. That makes payroll reports from Gusto, QuickBooks Payroll, or a connected system more than an HR document. They're a labor cost dashboard.

Look at payroll reports alongside your P&L, not in isolation. You want to understand total wages, payroll taxes, benefits, and how labor costs compare with revenue by month. For firms with a mix of billable and admin staff, this becomes especially useful.

A few review habits help:

- Compare labor cost to revenue: If revenue rises but labor rises faster, margin gets squeezed.

- Separate owners from staff where possible: That makes trend analysis cleaner.

- Watch overtime and bonus timing: A single payroll run can distort a month if you don't understand it.

Project and class reporting

QuickBooks also lets many service businesses use classes, locations, customers, or projects to make reporting more useful. Instead of one big P&L, you can view results by office, department, or service type.

For example, a consulting firm might track strategy retainers separately from implementation projects. A home services company might compare maintenance plans against one-time jobs. A multi-location clinic might separate performance by office.

That extra layer turns reporting from bookkeeping into management. It helps you see where your team's time produces healthy returns and where it gets absorbed by work that feels busy but doesn't support margin.

Key KPIs to Track in Your Financial Reports

Once your reports are clean, you can stop reading them passively and start using them to spot patterns. That's where KPIs, or key performance indicators, become helpful.

For service businesses, the most useful KPIs usually tie back to pricing, labor efficiency, collections, and client profitability.

Gross profit margin

Gross profit margin tells you how much revenue remains after the direct costs required to deliver the service. In a service business, direct costs often include direct wages or contractor payments tied to client work.

If this margin looks thin, your pricing may be too low, your labor delivery may be inefficient, or a certain service line may be harder to fulfill than you realized.

In QuickBooks, many owners pull this from the P&L, especially if they've set up the chart of accounts so direct labor and direct contractor costs sit above the gross profit line.

Billable versus non-billable time

This KPI often lives partly outside the accounting system. You may pull it from your time tracking app, project software, or payroll platform, then compare it with financial results.

A service company doesn't just need staff to be busy. It needs enough of that time to connect to client revenue. If too much payroll supports internal work, rework, meetings, or admin tasks, profit gets squeezed even when revenue looks decent.

A simple review can reveal a lot:

| KPI | What it tells you | Where to look |

|---|---|---|

| Gross profit margin | Whether service pricing and delivery are working | P&L |

| A/R aging trend | Whether client collections are slowing | A/R report |

| Billable utilization | Whether labor time is producing revenue | Time tracking plus payroll |

| Profit by service line | Which offers help or hurt the business | Class, project, or segment reports |

Client and service line profitability

Segment reporting offers significant advantages. According to The CJ Group's article on segment reporting for SMBs, 59% of small businesses rate their financial condition as fair or poor, and segment reporting helps uncover hidden profit by breaking results down by product line or customer type.

For service businesses, that might mean profitability by:

- Service line: Bookkeeping versus payroll support

- Client type: Retainers versus one-off projects

- Location: Office A versus Office B

- Team: One department compared with another

Don't ask only which clients bring the most revenue. Ask which clients leave the most profit after labor, revision cycles, and payment delays.

Customer lifetime value

Customer lifetime value helps you think beyond a single invoice. A client who starts small but stays for years may be more valuable than a large project client who creates lots of hand-holding and never returns.

The exact setup varies by business. Some owners track this in a CRM, some in spreadsheets, and some through reporting layers added on top of QuickBooks. The point is not to chase a perfect formula on day one. The point is to connect revenue history, service effort, and retention so you can see which relationships support growth.

That's the shift from raw reporting to strategic reporting. You're no longer asking, “What happened?” You're asking, “What should we do next?”

Building Your Month-End and Year-End Reporting Rhythm

Messy reporting usually isn't caused by one giant mistake. It comes from small delays that pile up. A missing receipt here, uncategorized transactions there, unreconciled accounts at month-end, and suddenly the reports don't feel trustworthy.

The fix is rhythm. Not intensity. A steady close process each month keeps your books usable.

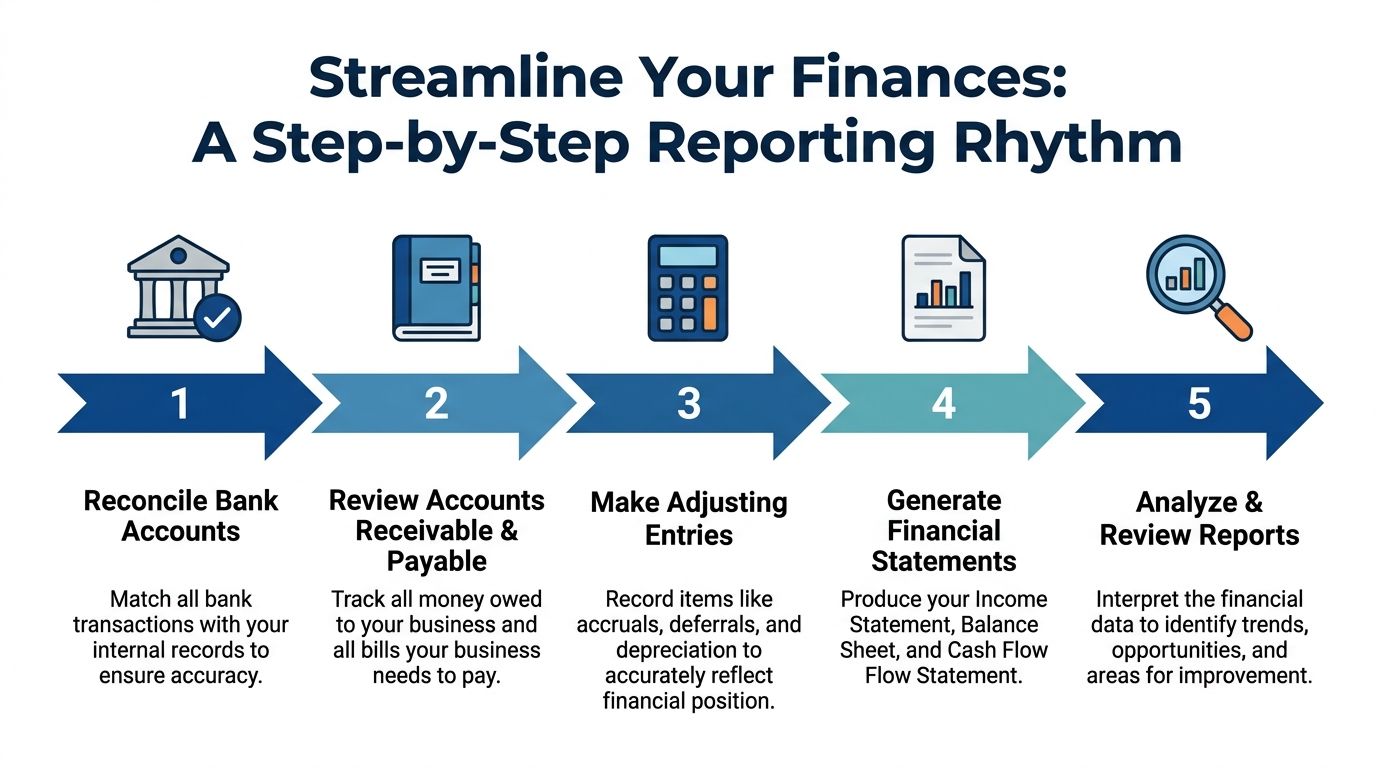

A practical month-end checklist

For most service businesses, month-end should follow the same order every time.

Categorize all transactions

Review bank feeds in QuickBooks Online. Confirm income, expenses, owner activity, loan payments, and transfers are coded correctly. Don't approve transactions in bulk without checking patterns.Reconcile bank and credit card accounts

Match your books to each statement. Duplicate entries, missing charges, and uncaught bank items usually show up during this process.Review accounts receivable and accounts payable

Make sure open invoices are real and unpaid bills are complete. If an invoice was paid but still appears open, your reports will mislead you.Post adjusting entries if needed

Record payroll accruals, prepaid expenses, loan interest splits, and other month-end adjustments. This step is where many DIY books drift off course.Generate the reporting package

Pull the P&L, balance sheet, cash flow statement, and any service-specific reports such as A/R aging, payroll detail, or project profitability.

If you want a structured planning document for the annual cycle too, this year-end close checklist can help you separate routine monthly work from final year-end cleanup.

What this looks like in QuickBooks and Gusto

QuickBooks Online handles the accounting side. Gusto or QuickBooks Payroll supplies payroll detail, tax information, and employee cost data. The key is making sure those systems talk to each other cleanly.

Owners often get confused here. They assume payroll is “handled” because wages were paid. But clean payroll reporting means more than processing paychecks. It means the wage expense, employer taxes, benefits, and liabilities post accurately to the books so month-end reports make sense.

A useful supporting tool is a bank reconciliation template for medical billing managers. Even if you're not in medical billing, the structure shows how to compare statement activity against internal records in a disciplined way.

Month-end versus year-end

Month-end is your pulse check. Year-end is your annual physical.

Month-end helps you manage the business while the year is still in motion. Year-end finalizes the books for tax preparation, owner distributions, lender conversations, and strategic planning. If month-end is skipped repeatedly, year-end becomes a cleanup project instead of a review.

Clean year-end books are usually the result of ordinary monthly discipline, not a heroic January scramble.

Keep the workflow repeatable

A good close process doesn't have to be fancy. It just has to be consistent.

- Use a recurring checklist: Don't rely on memory.

- Set a reporting deadline: Many owners aim to review the prior month shortly after statements are available.

- Assign ownership clearly: Decide who reconciles, who reviews payroll sync, and who approves final reports.

- Save reports in one place: A monthly PDF packet or shared folder keeps trends easy to compare.

That consistency turns reporting into a habit instead of a rescue mission.

Common Reporting Pitfalls and Quick Cleanup Tips

Most bad reports aren't caused by complicated accounting rules. They come from everyday habits. The danger is that those habits make reports look finished when they are unreliable.

Inconsistent categorization

One month software gets coded to office expense. The next month it lands in cost of goods sold. Contractor payments bounce between subcontractors and payroll clearing. That kind of inconsistency makes trend analysis almost useless.

The fix is simple but important. Build a stable chart of accounts, use account rules carefully, and review exceptions instead of letting automation guess too much. If you need a reference point for tighter processes, these financial reporting best practices are a solid benchmark.

Stale records

Reports lose value quickly when the data isn't current. Bank accounts may be unreconciled, invoices may still be open after payment, or payroll entries may not have posted properly.

According to Biz2Credit's overview of small business financial reporting, failing to validate data using the four C's of Correct, Current, Complete, and Consistent leads to a 15 to 20% increase in reconciling errors during month-end close. The same source says that implementing consistent monitoring schedules can reduce reporting errors by 30%.

That's not a technicality. It's the difference between trusting your reports and second-guessing them.

Mixed business and personal activity

This one is extremely common in small service businesses. An owner pays a business expense from a personal card, runs a personal expense through the business account, or transfers money without labeling it clearly.

The symptom shows up later as confusion. Profit looks off, owner draws are messy, and the balance sheet no longer tells a clean story.

A few cleanup moves go a long way:

- Separate accounts fully: Use dedicated business bank and credit card accounts.

- Book owner activity explicitly: Label draws and contributions correctly.

- Attach notes for unusual items: Future you, or your bookkeeper, will need the context.

- Reconcile monthly without skipping: Don't let unresolved items roll forward.

If a transaction needs a verbal explanation every month, the books probably need a cleaner account structure.

When these issues pile up, QuickBooks can still be cleaned. But the longer they sit, the less useful your financial reporting becomes for pricing, staffing, and cash planning.

When to Outsource Your Financial Reporting

It's 8:30 p.m. on the last day of the month. You're trying to answer a simple question, “Did we make money this month?” QuickBooks says one thing, payroll says another, and your bank balance adds a third opinion. At that point, financial reporting has stopped being a back-office task and started slowing down decisions.

For many service business owners, outsourcing becomes the right move when the reporting process needs more structure than your schedule can give it. A bookkeeper or reporting partner can keep the numbers current, tie QuickBooks and Gusto together correctly, and turn scattered transactions into reports you can use for staffing, pricing, and cash planning.

A few signs usually show up first:

- Reconciliations are late or getting skipped

- You hesitate to trust the P&L before making a decision

- Payroll reports and accounting reports do not match

- You need cleaner reporting by client, service line, or location

- Month-end feels like rebuilding the books instead of reviewing them

- Owner time keeps getting pulled from sales, delivery, or team management into bookkeeping cleanup

A helpful way to judge this is to compare bookkeeping to maintenance on your service vehicle. Basic upkeep is manageable for a while. Once breakdowns become frequent, the cheaper option is often a qualified mechanic. Financial reporting works the same way. If you are spending hours patching account mappings, fixing payroll entries, and explaining unexplained swings in profit, the process has outgrown the DIY stage.

Steingard Financial is one example of the kind of support service businesses often look for at this stage. Their work includes transaction categorization, reconciliations, AP and AR management, QuickBooks and Gusto workflows, and recurring reporting. The practical value is dependable monthly numbers, fewer manual fixes, and a clearer handoff path if you want to move from owner-managed books to outsourced reporting support.