Your business may be growing just fine on the surface. Revenue is coming in. Clients are happy. Payroll goes out. Taxes get filed.

But inside the back office, things feel less stable than they should.

You ask simple questions and get complicated answers. Can you afford another hire? Why did profit look healthy last quarter but cash feel tight? Why does your payroll report say one thing while QuickBooks seems to say another? At that point, the issue usually isn't effort. It's that the business has outgrown basic bookkeeping and needs stronger financial oversight.

When Your Business Outgrows Basic Bookkeeping

It often starts with a normal question on a busy Tuesday. Can we afford to hire one more project manager? You open the profit and loss statement, glance at the bank balance, and still do not get a clear answer.

That is usually the moment basic bookkeeping stops being enough.

A solid bookkeeper keeps the records current, reconciles accounts, and helps make sure tax season is not a mess. That work matters. But as a company grows, the question changes from "Are the books up to date?" to "What are these numbers telling us about the next decision?"

A growing service business feels this shift quickly. Headcount increases. Payroll has more moving parts. Clients pay on different timelines. Expenses spread across teams, projects, and software tools. The owner wants to know which work is profitable, whether cash can support another hire, and why margins look different from one month to the next. If you are still sorting out whether your business needs cleaner transaction support or stronger oversight, it helps to understand what outsource bookkeeping for small business usually covers, and where that support reaches its limit.

At that stage, financial reporting should work like a dashboard, not a box of receipts. You should be able to look at the numbers and answer practical questions in plain English.

Many owners cannot.

What this feels like in real life

A few signs tend to show up together:

- Reports arrive too late: You get monthly numbers after the window to act on them has already passed.

- Hiring feels like a guess: Revenue looks healthy, but you cannot tell whether cash flow can carry another salary.

- Systems disagree: Payroll, bookkeeping, and management reports do not line up cleanly.

- You are doing the translation yourself: Every decision depends on asking someone to explain what changed and why it matters.

The problem is not just missing data. It is missing interpretation.

GAAP-based financials are built to be accurate and consistent. That matters. But most owners do not need a stack of technically correct reports with no context. They need someone who can read those reports, spot what is driving the result, and explain it in operating terms. For example: "Your profit improved because of one large project, but collections slowed, so hiring right now would strain cash." That kind of translation is what helps you decide whether to spend, hire, pause, or push.

Growing companies rarely struggle because activity is low. They struggle because financial signals are delayed, unclear, or hard to use.

Once that gap appears, better bookkeeping alone usually does not solve it. The business needs stronger financial oversight and someone who can turn clean accounting into clear decisions.

What Exactly Is a Fractional Controller

A fractional controller is a senior accounting professional who oversees the quality, structure, and reliability of your financial operation on a part-time or outsourced basis. They don't replace bookkeeping. They make bookkeeping useful.

The cleanest analogy is this: a controller is the air traffic controller of your finances.

Your bookkeeper records the flights. Your payroll platform sends another stream of information. Your bank feeds bring in more movement. Bills, reimbursements, sales receipts, contractor payments, and tax entries all arrive from different directions. The controller makes sure those streams land in the right place, in the right order, under the right rules.

What the role actually covers

A fractional controller usually owns the accounting function at a management level. That often includes:

- Month-end close oversight: making sure accounts are reconciled and reports are ready on time

- Financial statement review: checking the profit and loss statement, balance sheet, and cash flow statement for accuracy

- Controls and consistency: setting rules so coding, approvals, and reconciliations happen the same way every time

- Reporting for management: turning raw accounting output into information the owner can use

- System design: making sure tools like QuickBooks and Gusto pass clean data across the workflow

What the role is not

A controller usually isn't your top-level strategist for fundraising, acquisitions, or capital structure. That leans more toward CFO work. And a controller usually isn't the person doing every transaction entry either. That remains core bookkeeping.

Simple definition: A fractional controller makes sure your numbers are accurate, timely, and organized well enough to support real business decisions.

That last point matters most. Many owners think accounting accuracy means compliance only. It doesn't. Accuracy is what lets you compare labor costs across months, trust margin reports, and decide whether a new hire is affordable before the offer goes out.

Why owners often get confused

The confusion comes from overlap. A strong bookkeeper may handle payroll support, reconciliations, and some reporting. A hands-on CFO may comment on controls or close timing. But the controller's lane is distinct. This person builds the bridge between recorded transactions and managerial insight.

If you've ever said, “My books are technically done, but I still don't know what to do,” you're describing the gap a controller fills.

Controller vs Bookkeeper vs Fractional CFO

You approve a hire on Monday because revenue looks solid. By Friday, you learn cash is tighter than expected, last month's margin was overstated, and payroll taxes still have not been fully posted. The problem is not always effort. It is often role confusion.

A bookkeeper, controller, and CFO all work with financial information, but they answer different business questions. The easiest way to separate them is to ask what decision each role supports.

- A bookkeeper answers, “Was the transaction recorded?”

- A controller answers, “Is the financial picture accurate, current, and clear enough to use?”

- A fractional CFO answers, “Given that picture, what should the business do next?”

Financial Roles at a Glance

| Role | Primary Focus | Key Responsibilities | Best For |

|---|---|---|---|

| Bookkeeper | Transaction recording | Categorizing entries, reconciling bank accounts, processing routine accounting tasks | Businesses that need clean day-to-day records |

| Controller | Accuracy, oversight, reporting | Closing books, reviewing statements, building controls, translating reports for management | Businesses that need dependable monthly visibility and stronger processes |

| Fractional CFO | High-level strategy | Planning, forecasting, capital decisions, pricing, growth modeling | Businesses making bigger financial bets or preparing for expansion |

The practical difference is less about seniority and more about translation.

Bookkeeping is the scorekeeping. Controller work is quality control plus interpretation. A CFO uses that interpreted financial picture to make bigger calls about growth, risk, and capital. If you are weighing broader strategic support, this overview of fractional CFO services explains where CFO work begins once reporting is reliable.

Where owners usually feel the gap

Owners rarely say, “I need a controller.” They say things like, “My P&L changes every time I look at it,” or “I have reports, but I still do not know whether I can afford another salesperson.”

That is the controller gap.

A good controller takes GAAP-based financial data and translates it into plain English. Instead of handing you a report full of account names and variances, they explain what changed, why it changed, and what it means for decisions you need to make now. Can you hire? Is spending ahead of plan? Are margins slipping because of pricing, labor, or project mix? That is the level where accounting starts helping run the business.

If you want a useful outside example of how that translation shows up in practice, strong management reporting connects the numbers to operating choices, not just month-end statements.

Later in the section, it helps to hear another perspective on how these roles relate in practice:

Which role do you likely need right now

If transactions are behind, accounts are unreconciled, or basic records are inconsistent, start with bookkeeping.

If the books are current but reports arrive late, numbers keep changing, or financial statements do not help you decide on hiring, spending, or profitability, you likely need a controller.

If reporting is already dependable and the next questions involve financing, expansion, pricing strategy, or long-range planning, you are moving into CFO territory.

Bookkeeping records the activity.

Controller oversight confirms it is right and explains what it means.

CFO guidance helps you choose the next move.

Core Responsibilities and Key Deliverables

Most owners don't buy fractional controller services because they want a job title. They buy outcomes. They want reports they can trust, a close process that doesn't drag, and fewer financial surprises.

The controller's work becomes visible through deliverables.

What you should actually receive

A competent fractional controller usually produces a repeatable monthly finance package, not a pile of disconnected files. That package often includes:

- Closed books on a defined schedule: not “when we get to it,” but a real monthly cadence

- Reviewed financial statements: profit and loss, balance sheet, and cash flow statements that tie out

- Budget versus actual analysis: what changed, where, and why it matters

- Balance sheet support: reconciliations and backup for major accounts

- Cash visibility: enough clarity to see near-term obligations and pressure points

- Owner-ready commentary: plain-English notes that explain the numbers

If you want a good outside example of what strong management reporting looks like, look for reporting that connects accounting output to operational decisions, not just a polished PDF.

The month-end close is a product, not a chore

A weak close process creates downstream confusion. Revenue gets booked late. Payroll entries sit in suspense accounts. Reimbursements land in the wrong period. Then the owner gets a report that is technically finished but practically unusable.

A controller treats month-end close like an operating system. They define who does what, which accounts need review, what gets reconciled, how exceptions are flagged, and when management sees the final package.

That structure matters because accounting mistakes usually aren't random. They come from broken workflows.

Data shows that 40% of small business financial errors stem from manual data entry and software integration failures, according to Rework Capital's review of fractional controller services.

The technology integrator role

This is the part many articles skip. A controller isn't only checking reports after the fact. They often design the path the data takes before it ever reaches the report.

Take a common setup: Gusto for payroll and QuickBooks for accounting. That sounds straightforward until payroll taxes, benefits, reimbursements, and department coding need to flow into the general ledger correctly. If mappings are weak, labor costs look distorted and liabilities don't reconcile cleanly.

A controller steps in by asking practical questions:

- Which payroll categories should map to which accounts?

- Should classes or departments track labor by team?

- How will benefits and employer taxes be separated?

- What review happens before and after the payroll sync?

- Where do exceptions go when the software doesn't post cleanly?

The software doesn't create financial clarity on its own. Someone has to design the rules that tell the software what “correct” means.

That's why a good controller improves not just reporting, but the machinery underneath it.

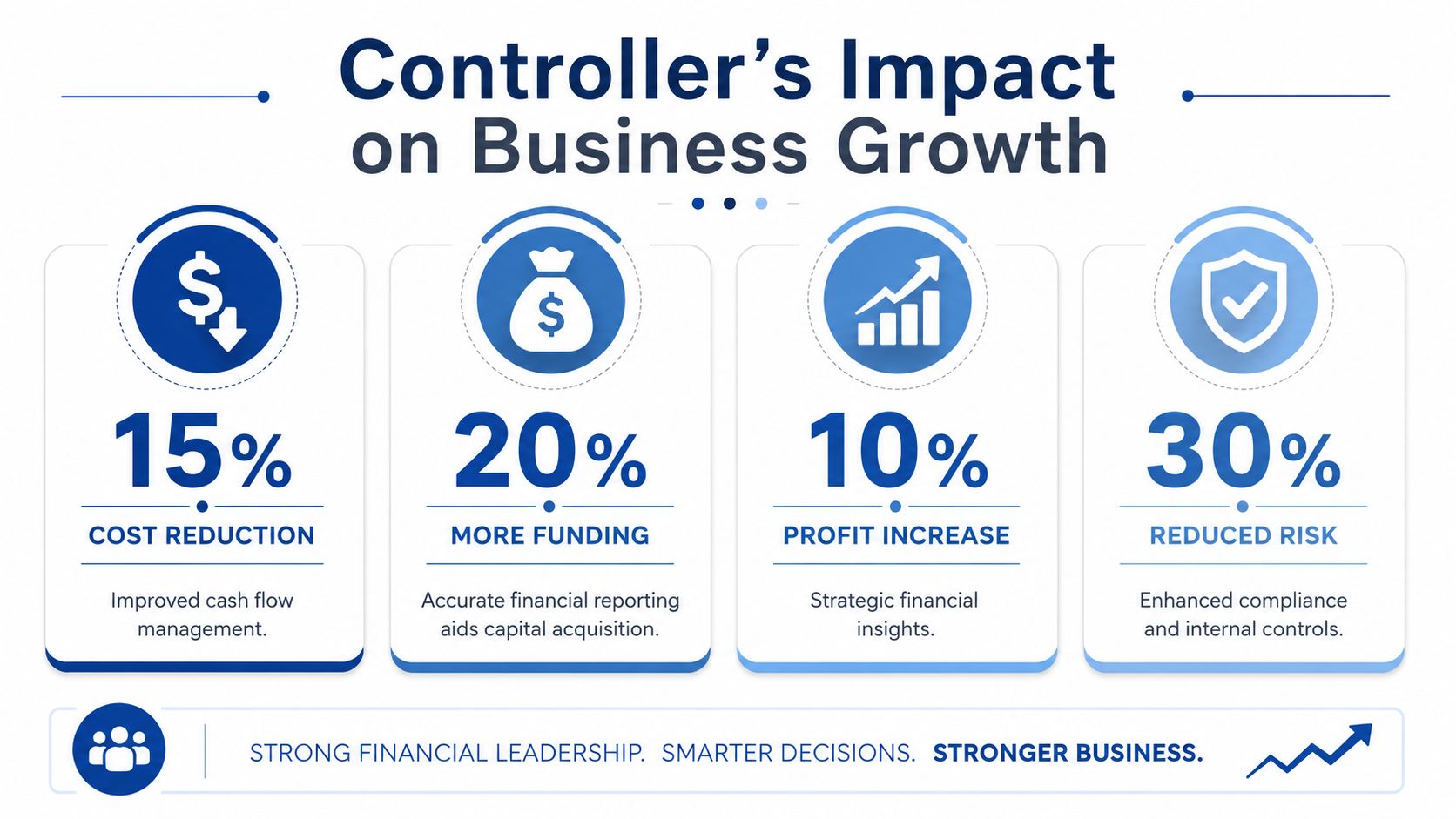

The True Value How a Controller Drives Growth

It's the first week of the month. Sales look strong, your bank balance looks decent, and a department lead asks to hire one more person. On paper, the business seems ready. In reality, the answer depends on timing, margin, collections, and whether your reports reflect what is happening in the business.

That is where controller work creates growth. A controller turns financial statements from recordkeeping documents into decision tools.

Turning GAAP into decisions

GAAP gives your numbers rules and consistency. That matters. Lenders, investors, tax professionals, and owners all need reports built on a standard framework.

But owners rarely make day-to-day decisions in GAAP language. They make them in operating questions.

- Can we afford this hire without creating a cash squeeze?

- Should we commit to this annual software contract?

- Which service lines are making money after labor and overhead?

- How much room do we have if a major client pays late?

A controller acts like a translator between the rulebook and practical decisions.

A profit and loss statement might show acceptable net income. A controller may explain that result very differently in plain English: project margins are thinner than they appear, payroll costs are climbing faster than revenue in one team, and cash collections are too slow to add fixed costs safely this month. Same numbers. Better guidance.

That is why many growing companies pair controller oversight with broader accounting services for small businesses so the books stay accurate and the advice stays useful.

What plain-English advice sounds like

Useful controller advice is specific, practical, and tied to a decision.

Instead of saying, “Your accruals need refinement,” a controller says, “We should wait two weeks before making the hire because cash from those open invoices has not hit yet.”

Instead of saying, “Payroll burden allocation appears inconsistent,” they say, “Your project margins look better than reality because employer taxes and benefits are sitting in overhead instead of being assigned to delivery labor.”

A controller also helps owners separate profit from cash. That confusion causes a lot of bad decisions. Profit is the score at the end of the game. Cash is the oxygen during the game. A business can show a profit and still feel short of breath if receivables are slow or expenses hit before customer payments arrive.

If the monthly close is still inconsistent, a practical resource like this actionable close process playbook helps explain why faster, cleaner month-end reporting leads to better decisions all month long.

Why that translation drives growth

Growth rarely stalls because an owner lacks reports. It stalls because the reports do not answer the next business question.

When a controller does the job well, several things change at once:

- Hiring gets safer. Headcount decisions are based on cash timing, utilization, and margin, not optimism.

- Spending gets more disciplined. New tools, contractors, and recurring commitments are tested against actual operating capacity.

- Pricing gets sharper. Owners can see whether revenue is covering delivery costs, support time, and overhead, not just direct labor.

- Management meetings get shorter. The numbers come with interpretation, so the team spends less time decoding reports and more time choosing a course of action.

The true value is not the report itself.

The primary value is clarity. A strong controller helps you move from “What happened?” to “What should we do next?”

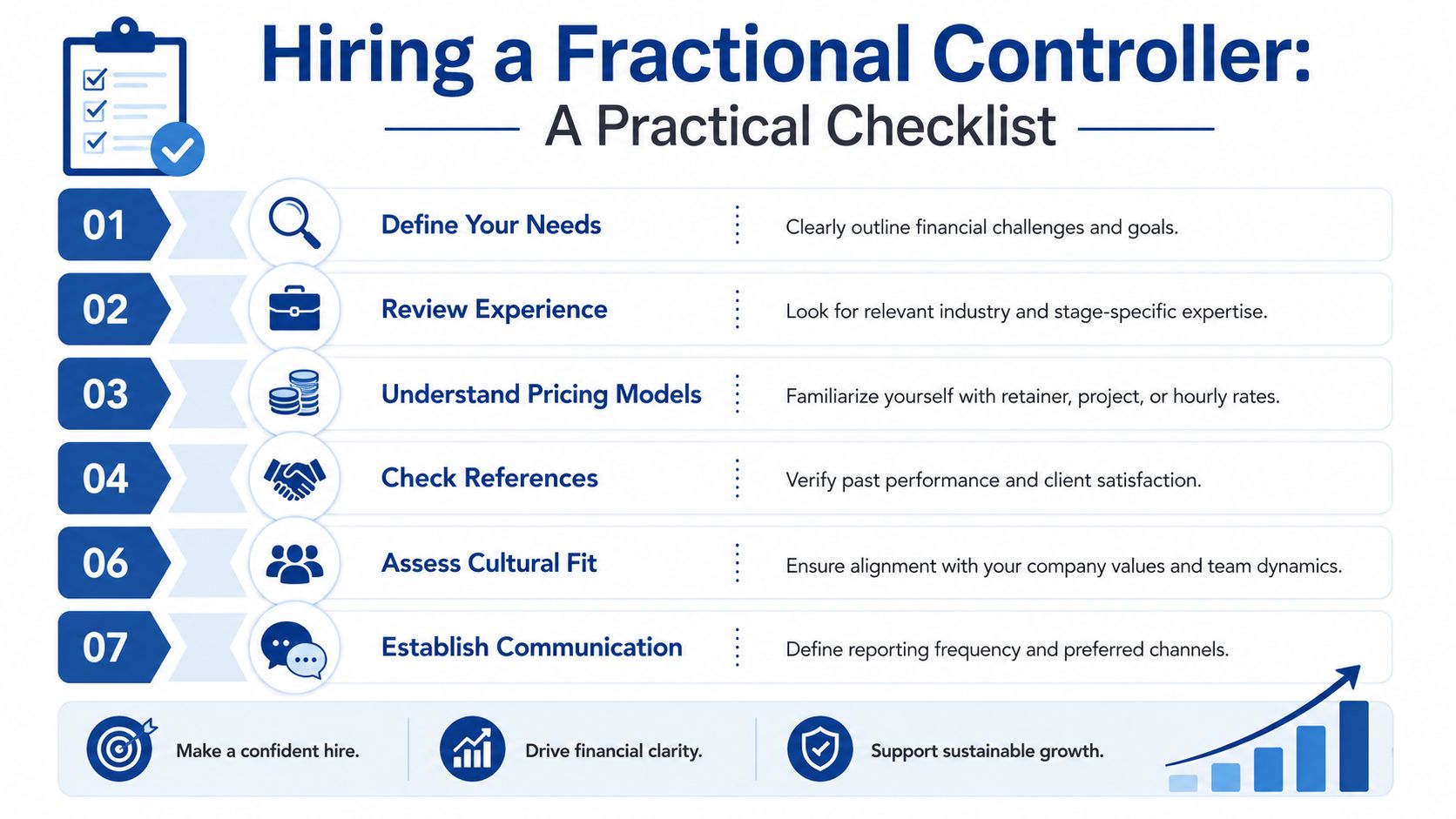

Hiring a Fractional Controller A Practical Checklist

You interview someone who says all the right finance words. A month later, you still get reports that tell you what happened, but not whether you can hire, increase owner pay, or commit to a new software contract. That is usually the main hiring risk. The problem is not the title. The problem is paying for controller help and getting bookkeeping output.

A strong fractional controller brings three things together. They keep the books clean enough to trust, they build a repeatable close process, and they translate GAAP-based reporting into plain-English advice you can use in the next management meeting.

What pricing usually looks like

Pricing depends on scope and starting condition.

Some companies need steady monthly oversight. Others first need cleanup work, a better chart of accounts, or a repaired month-end close before ongoing controller support will produce useful answers. That is why two businesses of similar size can receive very different proposals.

As noted earlier, fractional finance support often costs far less than a full-time hire. The practical question is not just monthly price. It is whether the engagement gives you decision-ready reporting, clear accountability, and fewer expensive mistakes around hiring, cash use, and margin.

If you're comparing outsourced support options more broadly, this guide to accounting services for small businesses can help you see where controller work fits relative to core accounting support.

The checklist I'd use before signing

Treat the interview like a working session, not a credentials review. You are trying to learn how this person thinks when the numbers are messy and the decision is time-sensitive.

- Ask them to walk through the close. What happens after month-end? Who reconciles bank accounts, credit cards, payroll, and accruals? How do they catch errors before reports go out?

- Test whether they can translate financials into action. Hand them a sample P&L and ask, “Would you recommend hiring now?” A real controller should explain the answer in business terms, not accounting jargon.

- Check system fluency. If you use QuickBooks, Gusto, bill pay tools, or expense apps, ask how they review mappings, payroll entries, and sync problems that can distort reporting.

- Look for service-business judgment. Labor-heavy companies need visibility into utilization, gross margin, contractor mix, and revenue timing. A controller who mainly serves product businesses may miss those pressure points.

- Clarify deliverables. Ask whether you will get only financial statements or also commentary, variance explanations, and recommendations.

- Set the communication rhythm. Decide in advance how often you meet, what gets flagged between meetings, and how urgent issues are handled.

Listen for clear teaching. If they cannot explain the numbers clearly during the sales process, they probably will not explain them clearly once you are paying them.

What to prepare on your side

A good engagement starts faster when the controller can see how your business runs, not just what sits in the general ledger. Financial statements are the map. Your workflows explain the terrain.

Bring these into the first conversation:

| Item | Why it matters |

|---|---|

| Current financial statements | Shows report quality, account structure, and likely trouble spots |

| Accounting software access | Reveals workflow gaps, reconciliations, and close history |

| Payroll setup details | Helps assess labor coding, benefits, and liability handling |

| Org chart or team list | Gives context for headcount planning and reporting needs |

| Top business concerns | Keeps the work tied to real decisions instead of generic cleanup |

Start with one or two decisions that matter right now.

For example, “Can we afford a senior hire in the next 90 days?” is a better starting point than “We want better reporting.” The first question gives the controller something concrete to test: cash timing, revenue stability, payroll burden, and margin capacity. That is where controller work becomes useful. It turns accounting records into a practical answer an owner can act on.

Building Your Financial Foundation with Steingard

At the point where bookkeeping alone no longer answers key questions, controller-level support changes the way a business operates.

It gives you cleaner closes, stronger reporting discipline, and a working translation from accounting language into owner language. Instead of waiting for month-end and hoping the reports make sense, you get a finance function that helps you decide. Hiring. Spending. Payroll planning. Growth pacing. All of it gets easier when the underlying numbers are timely and dependable.

That matters even more in service businesses, where labor, software, and timing can distort profitability quickly if the back office isn't built well. Businesses using QuickBooks, Gusto, and similar tools don't just need someone to “use the software.” They need someone who understands how those systems should connect so the reporting reflects reality.

Steingard Financial fits that need with a blend of meticulous bookkeeping, payroll and HR support, chart of accounts design, cleanup work, and ongoing reporting discipline. The team works inside the platforms many service businesses already use and helps create a finance workflow that can scale without creating confusion.

The result isn't just cleaner books. It's a stronger operating foundation.

If your business has reached the point where bookkeeping is no longer enough, Steingard Financial can help you build a more reliable back office with accurate reporting, payroll support, and controller-level oversight that turns complex financial data into practical decisions.