Prepaid Debit Card for Business: Smart Spending

If you're running a service business, you probably know the pattern. An employee buys materials on the way to a job. Someone else pays for a client lunch. A team lead books a last-minute hotel, then forgets to send the receipt until month-end. What looked like a small pile of routine purchases turns into a bookkeeping mess.

Most owners don't object to the spending itself. They object to the lag, the missing backup, and the lack of control. Cash leaves the business in bits and pieces, and the finance work shows up later as reimbursement requests, uncategorized transactions, and awkward follow-ups.

A prepaid debit card for business can fix part of that problem. It can also create a new one if the card program is set up badly, funded inconsistently, or pushed into your books without a clear workflow. The difference comes down to operations, not marketing.

Controlling Spend in a Growing Service Business

A common breaking point shows up when a company outgrows informal spending. In the early stage, an owner can text approval, reimburse a few purchases, and move on. Once the business has project managers, technicians, account reps, or remote staff, that same system starts leaking time.

A field employee needs supplies now, not after a reimbursement cycle. A manager needs a lunch budget for client meetings. A remote hire needs a small equipment allowance. If every one of those expenses runs through personal cards and manual reimbursement, the business ends up chasing paperwork instead of managing spend.

Payment methods have transformed in a way that matches this need. The Federal Reserve reported that the share of prepaid debit card payments made by businesses rose from 1% in 2015 to 7% in 2022 by number, and from 3% to 20% by value in its Fed payments study on U.S. card use. That tells you prepaid cards are no longer a fringe workaround. They're part of how businesses control operational spending.

Where owners usually feel the pain

The friction tends to show up in a few places:

- Receipt chasing: employees forget, lose, or delay documentation.

- Slow visibility: you often don't know what was spent until reimbursement hits your inbox.

- Petty cash problems: loose cash creates weak controls and poor audit trails.

- Policy drift: people spend first and ask later because the business hasn't built guardrails.

If you're still using envelopes, spreadsheets, or ad hoc reimbursements, a tighter policy matters as much as the payment method. ReceiptGen's expense policy guide is a useful reference for setting rules employees can follow, especially around approvals and documentation.

Why prepaid cards replace old habits well

Prepaid cards work especially well when they replace the sloppiest parts of the process. They often outperform reimbursements for recurring employee purchases, and they usually beat informal cash handling for accountability. If your business still leans on a cash drawer for small operating expenses, it's worth reviewing how a petty cash fund should be controlled before deciding whether cards should take over that role.

A prepaid card doesn't solve a policy problem by itself. It works when the business decides who can spend, what they can buy, and how fast the transaction has to be documented.

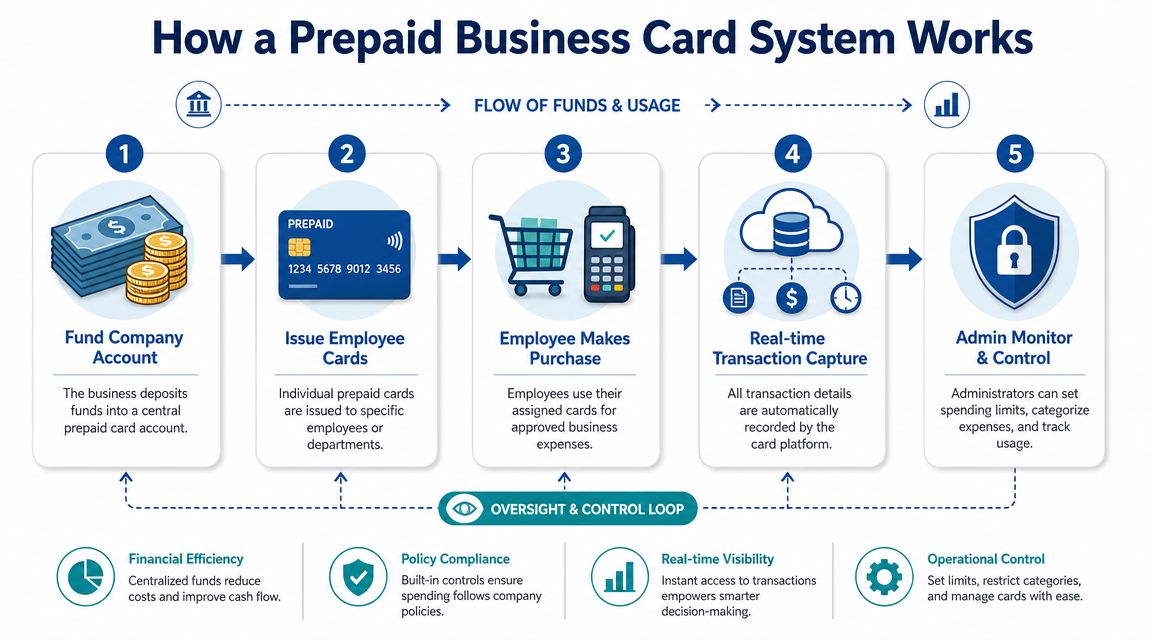

How a Prepaid Business Card Actually Works

A prepaid debit card for business is best thought of as a reloadable company wallet. The business puts money into the program first, then issues cards to employees, departments, or specific functions. Spending happens against that loaded balance, not against a credit line and not directly against the operating bank account.

That funding structure is what makes the product different. According to Ramp's explanation of prepaid business cards, a prepaid business card is funded from preloaded company funds. That eliminates credit risk and interest charges, but it also means available spend is capped by the amount you've loaded.

The money flow in plain English

Most programs follow a simple sequence:

The business funds a master account

Money moves from the company bank account into the prepaid platform.Cards are issued to people or purposes

One card might go to a technician for supplies. Another might be assigned to travel. A virtual card might be dedicated to one software vendor.Controls are added before spending starts

Limits can be set by person, by amount, by merchant type, or by time period, depending on the provider.Employees spend from the loaded balance

If the balance or rules don't allow the purchase, the card declines.Finance reviews the activity and reloads as needed

A strong process is essential here. Someone has to monitor balances and exceptions.

What makes it different from debit and credit

A business debit card pulls directly from a linked bank account. A business credit card lets you borrow and repay later. A prepaid card does neither. That sounds like a small distinction, but from a control standpoint it's major.

Here are the practical trade-offs:

- No borrowing: you won't carry card debt or interest.

- No direct bank access: a lost card doesn't expose the full operating account.

- Hard spending ceiling: employees can't spend beyond the loaded funds.

- More funding work: someone has to keep cards or the central account topped up.

Practical rule: If your team hates reimbursements but your cash flow is uneven, don't roll out prepaid cards until you've decided who owns reload timing.

This model is often a strong fit for businesses that need budget discipline more than rewards or credit-building. It also works well in operational environments where people need purchasing power but shouldn't have unrestricted access to company cash.

For owner-led service firms, it can pair nicely with other payment workflows. If you're also evaluating client-facing collections, tools that manage salon payments seamlessly show a related principle. The payment tool should fit the workflow, not force your staff into extra admin.

Key Benefits and Common Limitations

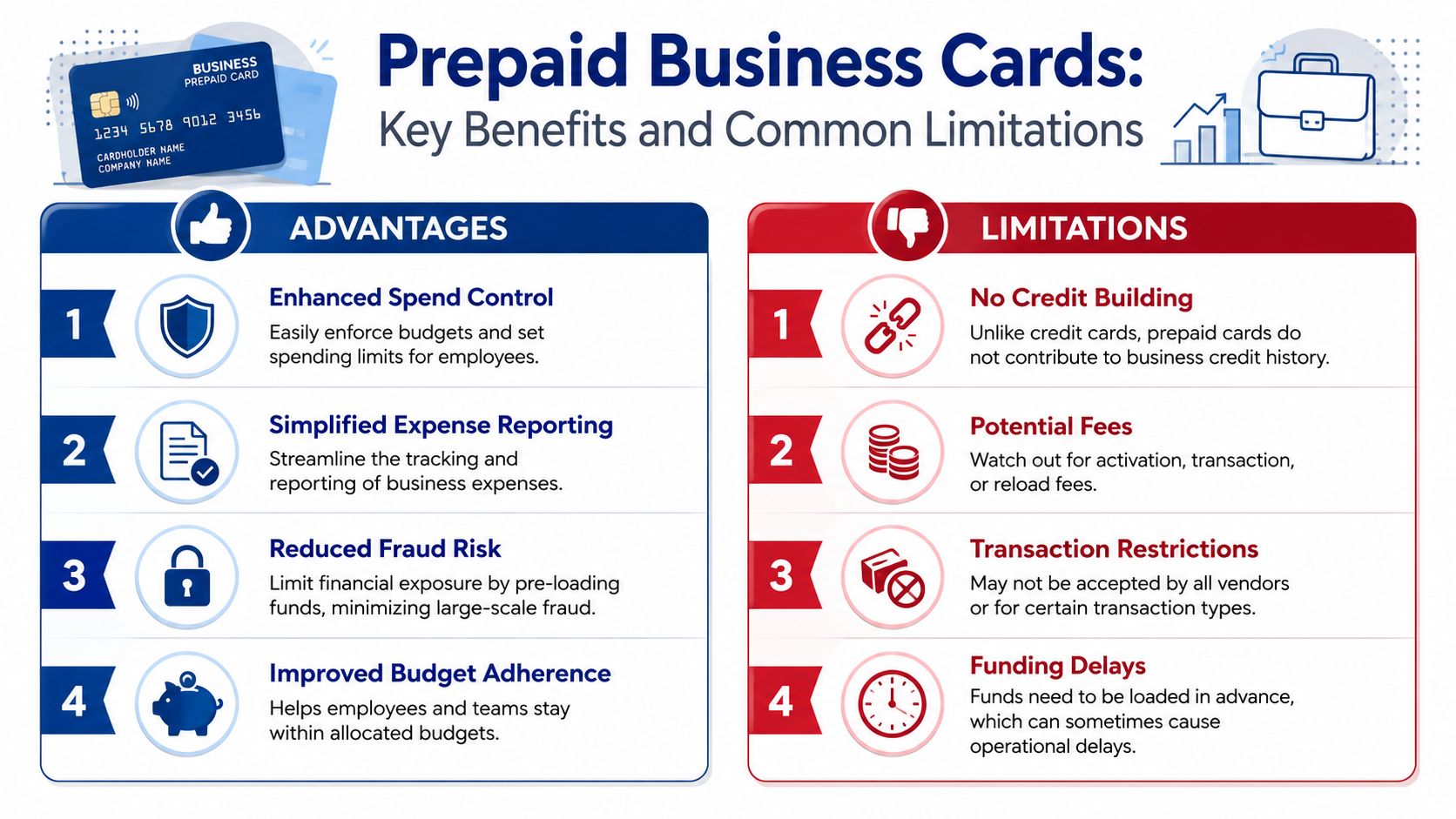

Prepaid cards are useful because they solve a specific problem. They give employees controlled spending power without exposing your full bank balance or opening a revolving credit account. That's the upside.

The downside is just as real. They don't build business credit, they need active funding, and they can create accounting confusion if the books treat loads and purchases as the same event. A lot of frustration comes from choosing the card for the right reason but operating it the wrong way.

What works well

The biggest advantage is control before the transaction happens. That's better than reviewing misuse after month-end.

- Budget discipline: if a team gets a fixed amount for travel, project purchases, or client meals, the card enforces the ceiling.

- Less reimbursement drag: employees don't have to front company costs on personal cards.

- Cleaner separation: vendor-specific or purpose-specific cards make spending easier to review.

- Lower exposure: if one card is compromised, only the loaded funds are at risk, not the whole operating account.

Another benefit is behavioral. Employees tend to follow policy better when the tool reflects the rule. A card assigned to fuel and supply merchants sends a clearer signal than a reimbursement policy no one reads.

Where prepaid cards fall short

The limitations matter more than most promotional pages admit.

- No credit building: this product doesn't help establish business credit history.

- Funding gaps: if nobody reloads a card in time, a legitimate purchase gets declined.

- Merchant issues: some vendors or transaction types can be awkward with prepaid products.

- Fee risk: depending on the provider, fee structures can become annoying if you don't review them carefully.

That doesn't make prepaid cards bad. It means they're operational tools, not universal replacements for every business card.

A useful way to think about the trade-off is this:

| Payment type | Best fit | Main weakness |

|---|---|---|

| Prepaid business card | Controlled employee spend and fixed budgets | Requires reload management |

| Business credit card | Larger recurring spend and credit-building goals | Can encourage overspending |

| Business debit card | Direct access to bank funds for trusted users | Less isolation from operating cash |

The short version is simple. If your priority is preventing overages and reducing reimbursement chaos, prepaid often wins. If your priority is rewards, float, or credit history, it usually doesn't.

A quick visual summary can help if you're comparing options internally.

Most prepaid card failures aren't product failures. They're management failures. The business skipped policy, assigned no owner, or treated the card feed like it would reconcile itself.

Practical Use Cases for Service Businesses

Service businesses tend to benefit most when they issue prepaid cards by workflow, not by job title alone. The question isn't just who needs a card. The better question is what type of spending should be isolated and controlled.

Field teams and mobile staff

A technician in the field may need to buy parts, fuel, or emergency supplies. Reimbursement is a poor fit there because it slows the work and shifts the burden to the employee. A prepaid card works better when the merchant categories align with the job.

For example, a plumbing or HVAC company might issue one card per truck or one card per technician. The business can then review purchases by route, by person, or by cost type without sorting through a pile of personal receipts and repayment requests.

Travel and client service

Consulting firms, agencies, and account teams often have moderate but frequent discretionary spend. Meals, parking, local transport, and small travel expenses can become messy when every trip runs through personal cards.

A prepaid card is often useful here because the budget can be loaded for the trip itself. When the trip ends, the spending window closes naturally. That keeps travel costs visible without giving someone a broad credit limit they don't need.

A travel card should have a narrow purpose. Don't mix trip spending, recurring software, and office purchases on the same card if you want easy reconciliation.

Project budgets and contractors

Project-based work is one of the cleaner use cases. A creative agency can assign a card to one client launch. A home services company can issue a temporary card for a subcontractor buying approved materials. A distributed operations team can give a remote worker a fixed setup allowance.

This structure reduces a common source of friction: using one payment method for many unrelated costs. When each card reflects one project, one vendor group, or one temporary role, the bookkeeping is simpler because the context is already built into the transaction stream.

Recurring vendor isolation

Some service businesses use prepaid cards for software subscriptions or marketing tools. That's not always the first use case owners think of, but it can be a good one. A dedicated virtual card for one platform makes renewals visible and keeps surprise charges from hitting your main account access path.

This also helps during cleanup. If a subscription should be canceled, you know exactly where to look. If a vendor changes pricing or renews unexpectedly, the card assignment makes that issue easier to catch.

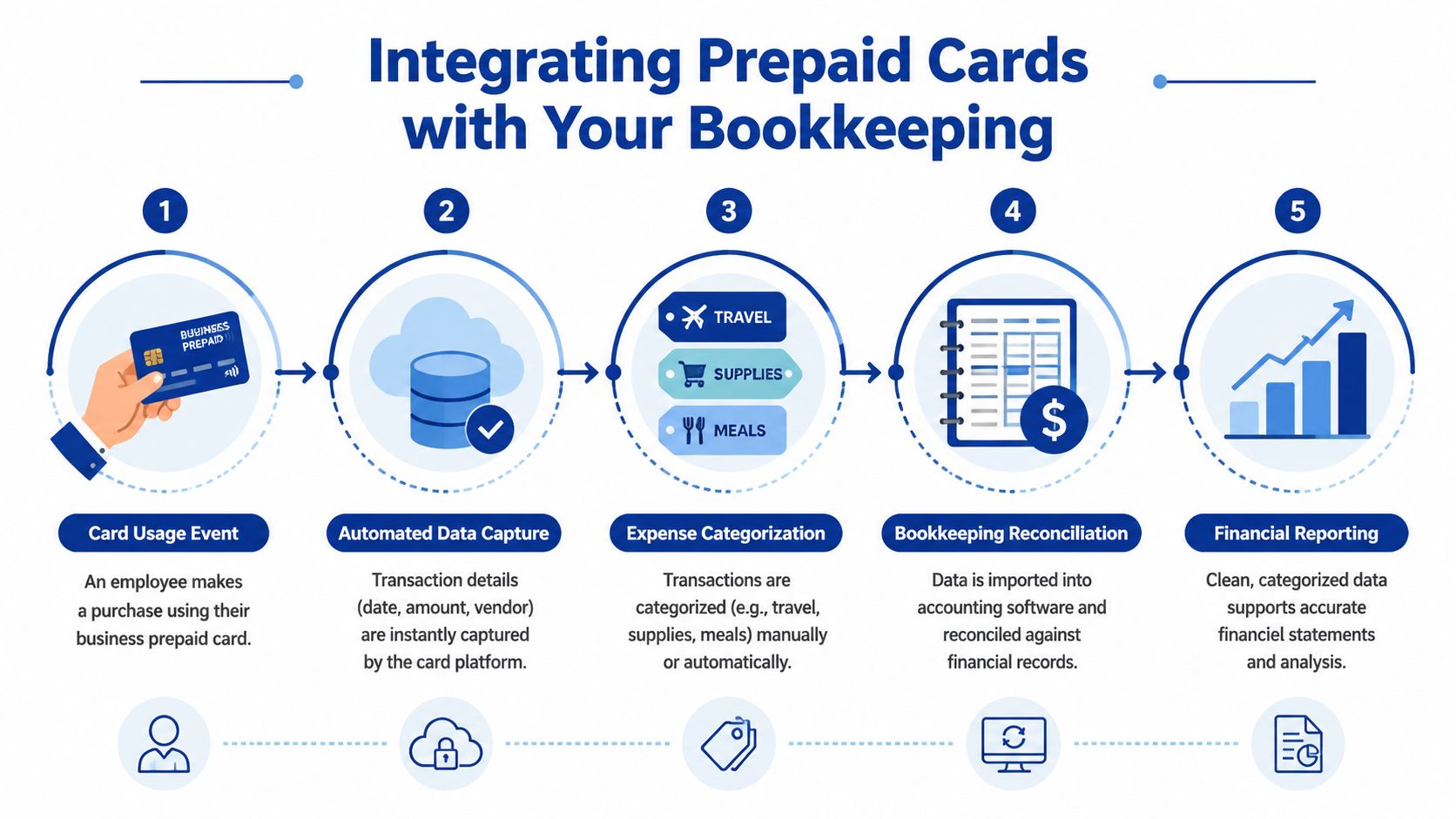

Integrating Prepaid Cards with Your Bookkeeping

Good intentions either turn into efficiency or into a reconciliation problem. The card itself isn't hard. The accounting treatment is where businesses get sloppy.

The main issue is that a prepaid program often creates two separate money events. First, the business moves cash into the prepaid platform. Later, employees spend from that balance. If your books record the initial load as an expense and then also record each purchase as an expense, you've double counted.

Use a clearing account, not an expense dump

In QuickBooks, the cleanest setup is usually a dedicated asset account for prepaid card funds. Some firms call it a clearing account. Others set it up as a prepaid card holding account. The label matters less than the logic.

The basic flow looks like this:

Transfer cash from operating bank to prepaid card asset account

This is not the expense yet. It's a movement of funds.Import or sync card transactions from the provider

Each swipe, charge, or subscription should hit the books as an actual expense event.Match receipts and code by category

Travel, meals, supplies, software, subcontractor costs, and so on.Reconcile remaining prepaid balance

The ending balance in the prepaid account should tie to the platform statement or dashboard.

This is the point many articles skip. The bookkeeping value of a prepaid debit card for business doesn't come from having cards. It comes from preserving a clean trail between funding, spending, and documentation.

Features that actually reduce accounting work

The strongest providers don't just issue cards. They support controls that make the accounting better. According to Wise's overview of prepaid business debit cards, some providers support customizable limits by time, merchant category, and cardholder, and also integrate with QuickBooks and Xero. That combination helps finance teams tighten coding and reduce uncategorized spend.

If you're trying to reduce cleanup time, the most useful features are usually:

- Direct accounting sync: fewer manual imports.

- Receipt capture tied to each transaction: easier audit support.

- Real-time visibility: problems get fixed during the month, not after close.

- Cardholder-level controls: cleaner coding patterns across the ledger.

For a broader process around expense handling, this guide on how to keep track of business expenses is a practical companion to card setup. The card should fit into the expense workflow you already want, not become a separate side system.

Bookkeeping warning: Never let the bank transfer into the prepaid platform post straight to meals, travel, supplies, or miscellaneous expense. That shortcut creates bad financials fast.

A simple month-end close routine

A prepaid card program stays clean when month-end follows a repeatable routine:

- Pull the provider statement or dashboard detail

- Confirm the prepaid asset balance

- Review missing receipts by employee

- Code exceptions and unusual merchants

- Check for duplicate entries from manual uploads or bank rules

- Lock the period after reconciliation

The goal isn't just tidy books. It's reliable reporting. If management wants job profitability, department spend, or project margin, prepaid card activity has to land in the right accounts the first time.

How to Choose a Provider and Set Up for Success

There are plenty of options in this market, which sounds helpful until you start comparing platforms. IBISWorld estimates the U.S. prepaid credit and debit card provider market was $18.6 billion in 2026 with over 460 businesses competing, according to its industry outlook for prepaid card providers. A crowded market gives you choice, but it also makes weak evaluation expensive.

Pick for workflow, not just features

A polished dashboard isn't enough. A provider can look modern and still create accounting friction if exports are clumsy, controls are thin, or support is poor.

Use this checklist before you commit:

| Feature | What to Look For | Why It Matters |

|---|---|---|

| Accounting integration | Native sync with QuickBooks or Xero, or at least a clean export format | Reduces manual entry and cleanup |

| Card controls | Limits by cardholder, merchant type, and time period | Helps enforce policy before spend happens |

| Receipt capture | Easy mobile upload attached to transactions | Improves audit trail and coding speed |

| Funding workflow | Clear reload process and easy balance visibility | Prevents purchase declines |

| User permissions | Admin roles, manager views, and cardholder restrictions | Keeps oversight organized |

| Reporting quality | Searchable transaction detail with useful exports | Makes review and month-end simpler |

| Fee transparency | Clear pricing for issuance, reloads, and usage | Prevents surprises that erode value |

| Support responsiveness | Real help when cards fail or transactions break | Important for staff in the field |

The setup decisions that matter most

The product choice is only half the work. The rollout determines whether the cards save time.

A good implementation usually includes these steps:

Write a short card policy

Spell out approved uses, prohibited purchases, receipt deadlines, and who approves exceptions.Assign one internal owner

Someone needs to manage issuance, reloads, missing receipts, and card shutdowns when roles change.Create card purpose categories

Travel, field supplies, software, project spend, client hospitality, and contractor purchasing should not all blur together.Build reconciliation into your close process

If nobody reviews the card ledger until quarter-end, the controls are mostly cosmetic.Train employees on declines and documentation

They need to know what happens if a merchant isn't allowed or a receipt is missing.

A lot of service firms also underestimate offboarding. If an employee leaves and the card remains active in some form, the admin risk climbs quickly. Card ownership has to stay current.

For the accounting side, your close process should include the same discipline you'd use for any other balance sheet item. A solid bank reconciliation workflow gives the right mindset here. Prepaid balances should be reviewed with the same care as checking accounts and credit card liabilities.

Red flags during vendor review

If a provider can't clearly show how transactions export, how balances reconcile, or how controls work by cardholder, keep looking. If the fee schedule feels opaque, keep looking faster.

The best provider for a service business is usually the one that makes everyday control boring. That's a compliment. Boring systems close cleanly.

Frequently Asked Questions About Business Prepaid Cards

| Question | Answer |

|---|---|

| Do prepaid business cards build business credit? | No. A prepaid card uses loaded company funds rather than borrowed money, so it generally isn't a credit-building tool. If building business credit is a major goal, a traditional business credit card usually fits that objective better. |

| Can I use prepaid cards for payroll or contractor pay? | Sometimes businesses use them around workforce spending, stipends, or approved purchasing, but you should be careful not to blur expense cards with payroll treatment. Wages, reimbursements, stipends, and contractor payments can have different accounting and tax implications. If you're considering anything beyond routine expense purchasing, get the structure reviewed before rollout. |

| What fees should I watch for? | Fee structures vary by provider. The practical review points are issuance fees, reload fees, transaction-related charges, ATM or cash access fees if applicable, and any maintenance or inactivity charges. The key isn't memorizing a fee list. It's making sure the pricing model matches how your team will actually use the cards. |

If your business is considering a prepaid debit card program and you want the books set up correctly from day one, Steingard Financial can help you build the workflow behind the card, not just record the aftermath. From chart of accounts setup to reconciliations, cleanup, and monthly reporting, their team helps service businesses turn expense activity into clean financial data you can trust.